All payers of the simplified tax system annually submit a declaration in which they inform the tax authority about the amount of income received, as well as accrued and paid tax. In 2021, legal entities are required to submit a report no later than March 31 , and entrepreneurs no later than April 30

We talked about how subjects applying the simplified tax system with the taxable object “income” fill out the declaration in a separate article. Today we will talk about those who reduce their income by the amount of their expenses.

Deadlines for paying taxes and filing returns

Tax is paid in advance for each reporting period no later than the 25th day of the month following its end. Tax reporting periods under the simplified tax system are the first quarter , half a year and 9 months . Thus, the taxpayer makes three advance payments during the year.

The tax period for tax under the simplified tax system is a year . When it ends, taxpayers recalculate the tax amount. The difference between the tax payable and the amount of advances actually transferred must be paid within the following terms:

- organizations - no later than March 31 of the following year;

- entrepreneurs - no later than April 30 of the following year.

Important nuance! For payers of the simplified tax system with the object “income minus expenses,” there is a minimum tax amount. It is equal to 1% of the amount of income received during the tax period . This is exactly the amount that must be paid to the budget if at the end of the year the tax is calculated in a smaller amount.

The simplified tax system is applied voluntarily, but has limits on the number of employees, income and some other indicators. If these limits are exceeded, the subject loses the right to apply the simplified tax system . In this case, you must report for the period worked in the year by submitting a declaration no later than the 25th day of the month following the loss of the right to the special regime.

The same reporting date is provided for cases of termination of activities in respect of which the simplified tax system was applied . The declaration must be submitted no later than the 25th day of the month following the one in which the activity was terminated.

You can find out about other important reporting dates in our tax calendar.

Types of tax reporting

All reporting of individual entrepreneurs and LLCs can be divided into the following categories:

- Tax office. It reflects business income for a certain period and, in accordance with the selected regime, calculates the amount of tax payable. An entrepreneur and an organization will need data from the Income and Expense Book to calculate the amount of budget contributions.

- Accounting. LLCs on the simplified tax system are required to keep accounting records. This document in a simplified form (compared to accounting on OSNO) is submitted to the Federal Tax Service at the end of the tax period.

- For the workers. This reporting on the simplified tax system for LLCs and individual entrepreneurs is no different from enterprises of other organizational forms. You need to send documentation to the Social Insurance Fund, Pension Fund and Federal Tax Service.

- Statistical. To monitor the real state of the economy in the country, Rosstat periodically collects data selectively or mandatory for all business entities.

- Reporting on other taxes.

If an entrepreneur or company did not operate during a certain period, then it is still necessary to submit reports. In this case, the fields are filled with zero indicators or dashes. It is also necessary to maintain KUDiR with zero indicators for a given period, and at the end of the year the document must be stitched, signed and stored for at least 5 years.

Organizational reporting on the simplified tax system

Legal entities must submit to regulatory authorities:

- reporting for the selected tax regime;

- reporting for employees;

- statistical reporting;

- accounting statements of LLC on the simplified tax system.

At the request of the tax authorities, you will need to provide a Book of Income and Expenses. You can maintain it electronically in a special program or in Excel, but to check the document you will need to print and format it.

The table below shows what kind of reporting an LLC needs to submit to the simplified tax system and the current filing deadlines.

| Report name | Where to take it | Submission deadline |

| Tax reporting | ||

| Declaration according to the simplified tax system | To the Federal Tax Service | Until March 31st annual report for the past year |

| Reporting for employees | ||

| Report on average headcount | To the Federal Tax Service | Until January 20 for the past year |

| Unified calculation of insurance premiums (ERSV) report on contributions for compulsory pension and health insurance | To the Federal Tax Service | until April 30 for the first quarter; until July 30 for the second quarter; until October 30 for the third quarter; until January 30 per year. |

| Form 6-NDFL data on withheld amounts of taxes on personal income | To the Federal Tax Service | until April 30 for the first quarter; until July 30 for the second quarter; until October 30 for the third quarter; before March 1 for the past year |

| Form SZV-M data on employees working at the enterprise | To the Pension Fund | By the 15th of each month for the previous month |

| Forms SZV-STAZH and ODV-1 data on the insurance experience of employees | To the Pension Fund | Until March 1 for the past year. If an employee retires, then within 3 days from the moment he contacts the employer |

| Form SZV-TD data on employees of the enterprise when they are hired or fired, as well as when the employee’s qualifications change | To the Pension Fund | The next business day after the hiring or dismissal of an employee. Until the 15th day of the next month after the employee’s qualifications change |

| Calculation 4-FSS indicates deductions for compulsory insurance in case of injury | In the FSS | When submitting on paper:

When submitted electronically before the 25th of the same month |

| Certificate confirming the main type of activity | In the FSS | Before April 15th for the previous year |

| Financial statements | ||

| Balance Sheet and Income Statement | To the Federal Tax Service | Until March 31st for the previous year |

| Statistical reporting | ||

| MP-sp is mandatory in 2021. Rosstat selectively collects information from different enterprises | Rosstat | Until April 1, 2021. The timing of other inspections is indicated on the Rosstat website rosstat.gov.ru |

Like any legal entity, LLCs submit financial statements to the simplified tax system, while an enterprise under this tax regime has the right to keep accounting records and fill out final documentation in a simplified way.

Declaration form according to the simplified tax system and the procedure for filling it out

For 2021, according to the simplified tax system, you need to report according to the form from the order of the Federal Tax Service of the Russian Federation dated February 26, 2016 No. ММВ-7-3 / [email protected] . It is the same for payers with different tax objects, but the set of sheets to fill out is different. Typically, payers of the simplified tax system with the object “income minus expenses” fill out:

- title page;

- section 1.2;

- section 2.2.

If the subject is a recipient of targeted funds, then section 3 must also be completed.

Title page

Let's look at filling out the title line by line.

TIN . For an organization this is a 10-digit number, for an individual entrepreneur it is 12-digit, since individual entrepreneurs are individuals.

Checkpoint . Filled out by organizations; individual entrepreneurs do not have this code.

Page number. It must be specified in the format “001”, “002” and so on.

Correction number. When submitting the report for the first time, “0—” is entered. If an updated declaration is submitted, its serial number is indicated - “1—”, “2—” and so on.

Taxable period. The tax period code “34” is indicated, since the declaration is submitted for the year. Codes for reorganized companies and entities that cease operations or switch to another tax regime are given in Appendix No. 1 to the order approving the form.

Reporting year — 2021.

Tax authority code . Consists of two values:

- the first 2 digits are the region code;

- the last ones are the Federal Tax Service number.

Code at location (accounting) . Taken from Appendix No. 2 to the Order. There are three codes in total:

- 120 - for individual entrepreneurs;

- 210 - for the organization;

- 215 - for a successor who is not the largest taxpayer.

Title page (beginning)

Taxpayer . You must enter the full name of the organization as it is indicated in the constituent documents. If the declaration is submitted by an individual entrepreneur, his last name is indicated in the first line, his first name in the second, and his patronymic, if any, in the third.

Code of the type of economic activity according to the OKVED classifier. Can be found in the extract from the registry.

Information about reorganization and liquidation . The line is intended for reorganized companies; everyone else puts dashes in it. The codes are given in Appendix No. 3 to the Order.

Table 1. Codes for reorganized companies

| Code | Reorganization form |

| 1 | Conversion |

| 2 | Merger |

| 3 | Separation |

| 5 | Accession |

| 6 | Division with simultaneous accession |

| 0 | Liquidation |

Phone number. It is recommended to remember, because if you have questions about the declaration, the inspector may call.

Title page (continued)

The lower part of the title page of the declaration is intended for signature by the individual entrepreneur or company representative and confirmation of the accuracy of the information. Here you need to indicate:

- code “1” - if the declaration is submitted in person;

- code “2” - when submitted through a representative.

The following lines reflect the full name of the head of the company , and below is his personal signature and date. If the declaration is submitted by an individual entrepreneur, only a signature and date are added.

If the report is signed by a representative , then his full name is indicated. When the representative is a company, the full name of its employee authorized to file the declaration is indicated.

If the declaration is submitted through a representative, a document confirming his authority . A copy of it should also be attached to the report.

Title page (end)

Completing Section 1.2

This section collects summary information about income, advance payments and the amount of tax payable.

The top lines duplicate the INN and KPP, and also indicate the page number.

Lines 010, 030, 060 and 090 are for the OKTMO . It is necessary to indicate it in line 010; in the remaining lines it is necessary to indicate it only if it has changed. 11 categories are allocated for OKTMO. If the code is eight digits, the last three must have dashes.

In lines 020, 040, 070 tax advances are entered .

Lines 050, 080 reflect advance payments to be reduced.

Section 1.2

Next comes the final block of lines 100-120 . The calculation of indicators is made in Section 2.2 of the declaration. The value is indicated in one of the lines:

- Line 100 reflects the amount of tax to be paid additionally at the end of the year. This is the difference between the calculated tax amount and advance payments.

- Line 110 is intended to reflect the amount of tax to be reduced. This is the positive difference between the amount of advances paid and the calculated amount of the minimum tax.

- Line 120 reflects the amount of the surcharge if the taxpayer must pay tax under the simplified tax system “income minus expenses” in the minimum amount. This is the positive difference between the amount of the calculated minimum tax and advance payments.

Section 1.2 (continued)

Completing Section 2.2

In this section, the taxpayer reflects income and expenses for the year. They are indicated on an accrual basis for the quarter, half year, 9 months and year:

- lines 210-230 are intended to reflect income;

- lines 220-223 - to reflect expenses.

Section 2.2

Line 230 indicates the amount of loss from previous years, which reduces the tax base under the simplified tax system.

The following block of lines indicates the positive difference between income and expenses in each period:

- in line 240 - for the first quarter;

- in line 241 - by half year;

- in line 242 - based on the results of 9 months.

Line 243 reflects the tax base, which is calculated in the following way: income for the year (line 213) - expenses for the year (line 223) - the amount of losses from previous periods (line 230).

Section 2.2 (continued)

If, when calculating the values indicated on lines 240-242, amounts with a “-” sign are obtained, they are reflected accordingly in lines 250-252 (lines 240-242 are not filled in). Line 253 indicates the negative difference between income and expenses for the year (line 223 - line 213).

The next block is intended to reflect tax rates under the simplified tax system with the object “income minus expenses” . The standard rate is 15% , but regions are legally entitled to reduce it. The rate can be:

- 5-15% for all or certain categories of taxpayers.

- 0% for newly registered individual entrepreneurs from the sphere of production and consumer services, as well as from the social or scientific sphere. Tax holidays are established for 2 years.

The tax rate is reflected for each period separately in lines 260-263 .

The last block is intended to reflect the amounts of intra-annual advance payments and the tax calculated at the end of the year. Advance payments are calculated by multiplying the income for the relevant period by the tax rate. For example, for the first quarter the tax is calculated as follows: line 240 * line 260 / 100%. The corresponding rows are also multiplied for the remaining periods.

The amount of tax calculated for the year is indicated in line 273 .

Line 280 reflects the amount of the minimum tax equal to 1% of the income received for the year . The indicators of lines 273 and 280 are compared, and the larger one is selected. This will be the amount of tax that the subject must pay for the reporting year. This is well illustrated in the following image:

Section 2.2 (end)

The company in the example closed two periods at a loss, due to which the total tax amount for the year is zero. Therefore, she must pay the minimum tax ( line 280 ). To calculate the surcharge, the amount of advance payments made within the year is subtracted from this amount. The final value is reflected in line 120 of section 1.2 .

Zero balance sheet according to the simplified tax system

Formation of a zero balance sheet according to the simplified procedure will be required if the enterprise is registered, but no activity was carried out. The obligation to provide reporting remains with the company, regardless of actual activity, until the moment it is deregistered with the Federal Tax Service.

In order to figure out how to correctly fill out a balance under the simplified tax system in the absence of activity, the simplifier will need to clarify the following data:

- The amount of the authorized capital: its creation occurs at the time of the start of activity, therefore, information must be present even in the zero document.

- Debt of investors: if the shares are not repaid, then this fact is reflected in the liability side of the simplified balance sheet.

- Debt to the budget - to determine its size, the company’s accountant should contact the Federal Tax Service and other government agencies and carry out a reconciliation of payments and obligations. A company that has not started operations may have debts to the budget, for example, due to state duties when changing information in the charter.

You can find a sample and nuances of drawing up a zero balance on our website.

Special cases

If a loss is received

When filling out a declaration under the simplified tax system with the taxable object “income minus expenses” with losses, there are some peculiarities.

To reflect the loss, section 2.2 of the declaration provides a block of lines 250-253 . Here you need to indicate the negative difference between income and expenses for a certain period - quarter, half year, 9 months and year. The following image shows an example of reflecting a loss in section 2.2:

Section 2.2 (Loss)

Please note that even despite receiving a loss at the end of the year, the minimum tax must be paid .

If advance payments paid within the year exceeded the amount of the minimum tax, then this difference should be reflected in section 1.2 on line 110 . This will mean that at the end of the year the tax amount will be reduced.

If there is no activity

Lack of activity does not relieve an organization or individual entrepreneur of the obligation to file a declaration. It is submitted according to the general rules with only one difference - dashes .

Composition of individual entrepreneur reporting on the simplified tax system

It is much easier for entrepreneurs in the special regime to keep records and generate reports than for individual entrepreneurs in the general taxation system. Must be submitted:

- tax reporting;

- statistical reporting;

- reporting for employees (if any).

If an individual entrepreneur is required to pay water, transport or land taxes, then there is no need to submit reports on these payments. Individual entrepreneurs’ financial statements are not submitted to the simplified tax system, since entrepreneurs are not required to keep accounting records. At the same time, the law requires keeping a Book of Income and Expenses, where data on funds received and expenses for doing business should be entered (depending on the version of the simplified tax system).

The table below provides information on individual entrepreneurs’ reporting on the simplified tax system and the deadlines for submitting documents to regulatory authorities.

| Report name | Where to take it | Submission deadline |

| Tax reporting | ||

| Declaration according to the simplified tax system. Depending on the type of simplified tax system (“Income” or “Income minus expenses”), it displays information about income received or income minus expenses. In some cases, a preferential tax rate may be applied | To the Federal Tax Service | Until April 30 for the past year |

| Reporting for employees (if the individual entrepreneur has them) | ||

| Form 6-NDFL data on withheld amounts of taxes on personal income. | To the Federal Tax Service | until April 30 for the first quarter; until July 30 for the second quarter; until October 30 for the third quarter; before March 1 for the past year. |

| Unified calculation of insurance premiums (ERSV) report on contributions for compulsory pension and health insurance | To the Federal Tax Service | until April 30 for the first quarter; until July 30 for the second quarter; until October 30 for the third quarter; until January 30 per year. |

| Forms SZV-STAZH and ODV-1 data on the insurance experience of employees | To the Pension Fund | Until March 1 for the past year. If an employee retires, then within 3 days from the moment he contacts the employer |

| Form SZV-M data on employees working at the enterprise | To the Pension Fund | By the 15th of each month for the previous month |

| Form SZV-TD data on employees of the enterprise when they are hired or fired, as well as when the employee’s qualifications change | To the Pension Fund | The next business day after the hiring or dismissal of an employee. Until the 15th day of the next month after the employee’s qualifications change |

| Calculation 4-FSS indicates deductions for compulsory insurance in case of injury | In the FSS | When submitting on paper:

When submitted electronically before the 25th of the same month |

| Statistical reporting | ||

| 1-entrepreneur is required in 2021. Rosstat selectively collects information from different enterprises | Rosstat | Until April 1, 2021 The timing of other inspections is indicated on the Rosstat website rosstat.gov.ru |

The deadline for submitting documents is indicated as it is in the law, excluding holidays and weekends. Therefore, if the date falls on a non-working day, then the individual entrepreneur of the simplified tax system will also be able to submit reports on the following weekday.

Tax base calculation

At its core, determining the tax base under the simplified tax system “income minus expenses” is very similar to a similar process when calculating income tax.

Income is divided into those received from sales and non-sales . Sales income includes revenue from the sale of goods, works and services produced by an organization or individual entrepreneur, the sale of goods that were purchased, and property rights. Included in revenue are the amounts of advances transferred by buyers against future deliveries.

Non-operating income includes other income in accordance with Article 250 of the Tax Code . For example, such income is recognized as:

- rental income;

- gratuitously received valuables and property rights;

- interest on loans issued and more.

As for expenses, a closed list of them is translated into Article 346.16 of the Tax Code of the Russian Federation . If any expenses are not on this list, then they are not included in the calculation of the tax base.

Condition for recognizing expenses included in the list:

- Economic feasibility . If the tax inspectorate doubts the need for any company expenses, they may not be recognized and excluded from expenses taken into account for tax purposes. However, a businessman can make any expenses, but at the expense of net profit.

- Documentary confirmation . It is provided by two types of documents, which, with rare exceptions, must be completed for each operation:

- a primary document (act, invoice) that confirms the fact of economic activity;

- a document evidencing payment of expenses (payment order, account statement, cash receipt).

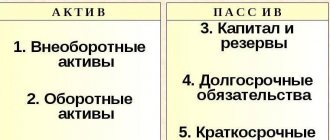

Simplified balance: how to fill out correctly under the simplified tax system

The balance sheet allows you to assess the actual financial condition of the company: economic growth or unprofitability. Information from the balance sheet is needed to evaluate the company as a borrower and a reliable partner for counterparties. Balance sheet data also informs business owners about the state of affairs in the company. Government agencies need a balance both for generating statistical data on the industry and for tax control.

The accounting forms used do not depend on the taxation system chosen by the enterprise. Special regime officers report on the same forms as companies on OSNO.

For small businesses, including those using the simplified tax system, simplified forms of accounting reporting are provided (Appendix 5 to the order of the Ministry of Finance of the Russian Federation dated July 2, 2010 No. 66n). Most of the lines that are not used by simplifiers have been removed from the form. Accounting information is provided without detail.

The table below will give you an understanding of how to fill out the balance sheet under the simplified tax system and what information you will need to collect:

| Balance line | Accounting information |

| Tangible non-current assets |

|

| Intangible, financial, other non-current assets |

|

| Reserves |

|

| Cash and cash equivalents |

|

| Financial and other current assets |

|

| Capital and reserves |

|

| Long-term borrowed funds |

|

| Other long-term liabilities |

|

| Short-term borrowed funds |

|

| Accounts payable |

|

| Other current liabilities |

|

The company provides information for the reporting year, as well as for the two periods preceding it.

Subscribe to our newsletter

Yandex.Zen VKontakte Telegram

Below you can find a simplified balance sheet.

All simplified accounting reporting forms are available for download on our website.

How to fill out a simplified balance sheet under the simplified tax system if there are no indicators? In this case, a dash is placed in the corresponding lines.

Fines

If you do not submit a declaration according to the simplified tax system on time, a fine will follow based on Article 119 of the Tax Code. This is 5% of the tax amount for each full or partial month of delay . The fine cannot be less than 1,000 rubles, but at the same time cannot exceed 30% of the tax amount.

For non-payment of tax, a fine is provided under Article 122 of the Tax Code of the Russian Federation in the amount of 20 to 40% of its amount. In addition, late payment threatens to accrue penalties in the amount of 1/300 of the refinancing rate for each day of delay.

However, the most unpleasant consequence may be the blocking of the current account of the tax inspectorate in accordance with Article 76 of the Tax Code of the Russian Federation. Such a decision can be made if the declaration is not received within 10 days after the deadline .

How to calculate taxes on the simplified tax system (object “Income”)

The tax amount must be calculated based on cash receipts for the reporting period. In this case, it is necessary to take into account only those incomes that are actually transferred to the cash desk or to the current account of the enterprise in the reporting period, including non-operating income - payment for rent of premises, return of old debt, etc.

Starting from 2021, there are two ways to calculate contributions to the budget:

- If all limits under the simplified tax system are met, then the tax is determined as 6% of income.

- If one of the limits under the simplified tax system is exceeded, then the tax is determined as 8% of income starting from the quarter in which the excess was detected.

For the calculation, the amount of income is taken on an accrual basis from the beginning of the year. For example, when determining the payment amount for a six-month period, you need to sum up all receipts for this period and multiply them by 6%. Then the amount of advance payments already paid since the beginning of the year is subtracted from this value.

Other taxes on simplified tax system 6%

In addition to the single tax, insurance premiums for themselves and their employees (if any), some individual entrepreneurs and simplified organizations are required to pay VAT and enter the corresponding declaration into the list of reporting under the simplified tax system 6%. This type of tax is required for:

- Tenants of state property.

- Tax agents are entrepreneurs or organizations that pay taxes for other taxpayers. For example, for a foreign tax evader company in Russia from which goods were purchased.

- Importers of goods to the territory of the Russian Federation.

- Individual entrepreneurs and LLCs that use VAT in mutual settlements with other enterprises that pay this tax.

- Participants in a partnership agreement are several enterprises pooling their capital for a specific activity.

Some organizations and individual entrepreneurs will also need to pay taxes on property, vehicles, and the use of natural resources. The Federal Tax Service independently calculates the amounts of contributions and sends payers notifications with the amounts and details for payment.

How to reduce tax with simplified tax system 6%

Despite the fact that the tax rate in this special regime is low, it can be further reduced by:

- Trade fee if the place of registration of the entity coincides with the place of actual business.

- Insurance premiums for employees and for yourself (for individual entrepreneurs). Entrepreneurs without hired employees can reduce the tax amount to zero, and LLCs and individual entrepreneurs with hired employees by no more than 50%.

- Contributions for employees under voluntary health insurance contracts.

- Sick leave payments to employees (for the first 3 days of illness).

- The transferred contributions must be paid in the same period when they will be deducted from the single tax.

An example of filling out a declaration under the simplified tax system “income minus expenses”

Let's look at filling out the declaration using the example of Romashka LLC.

Title page

Page 1

Section 1.2

Page 2

Section 2.2

Page 3

Regulations

- Order of the Federal Tax Service of Russia dated February 26, 2016 No. ММВ-7-3/ [email protected] “On approval of the tax return form for the tax paid in connection with the application of the simplified taxation system, the procedure for filling it out, as well as the format for submitting the tax return for the tax paid in connection with the application of a simplified taxation system, in electronic form.”

- Letter dated May 30, 2016 No. SD-4-3/ [email protected] “On the direction of control ratios of tax return indicators for taxes paid in connection with the use of a simplified taxation system.”

- Tax Code of the Russian Federation, Article 346.16. "Procedure for determining expenses."