Individual entrepreneurs are required to pay taxes and fees to the appropriate budgets, depending on the chosen taxation system. In this article we will tell you how to correctly fill out a receipt for payment of UTII in 2021.

IMPORTANT!

Note! From January 1, 2021, the taxation system in the form of a single tax on imputed income ceases to exist! It was officially canceled by Federal Law No. 97-FZ of June 29, 2012. All individual entrepreneurs and LLCs that previously used it should switch to another regime (STS or PSN) by the end of 2020, otherwise, from January 2021, they will automatically be recognized as OSNO taxpayers.

Is it possible to pay taxes through Sberbank online?

Paying taxes via the Internet using online resources is the fastest and most convenient way to pay your budget. To do this, organizations enter into agreements with banks and connect an online resource called “Client-Bank”. “Client Bank” is a service that allows you to pay with any counterparties via the Internet, including the budget. “Client-Bank” is connected when opening an organization’s current account, payments are confirmed using an electronic signature. If everything is clear with organizations, then with individual entrepreneurs questions arise, for example, can individual entrepreneurs pay taxes from a personal account or do they need to open a current account?

Does an individual entrepreneur need to open a current account?

Currently, the law allows individual entrepreneurs not to open a current account. However, some regulations still introduce their prohibition, for example, Central Bank Instruction No. 153-I dated May 30, 2014, as amended on December 24, 2021, prohibits transactions related to business activities on current accounts. Also, the agreement for opening a personal account may contain such prohibitions, therefore, in order to avoid misunderstandings with the bank, it is better for individual entrepreneurs to open a separate current account for conducting their business activities. If an individual entrepreneur works exclusively with individuals, then in this case you can only use your personal account.

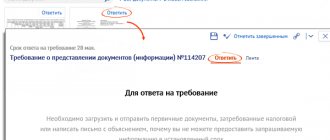

How to pay UTII through Sberbank

To pay the tax, you first need to get the details, without which it will be impossible to pay the tax . Details for paying taxes can be obtained from the tax office or can be found on the Internet. It must be remembered that different regions have different details. To pay taxes we take the following steps:

- We go to the online bank;

- Find it in the “Payments and Transfers” menu;

- Select the item “Payment: Taxes, Fines, Duties, Budget payments”:

- Next, select “Payment: Taxes, work patents”;

- Select the following menu item “Payment: Search and payment of taxes to the Federal Tax Service”;

- Next you are asked to select ;

- We take from the details and enter them into the fields - BIC, account number, KBK, recipient's TIN;

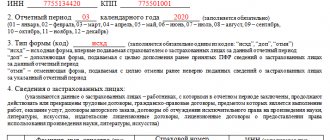

- After entering all the details, the bank requests data on OKTMO (regional details), basis for payment (where TP - current payments, PO - debt, etc.), tax period (for example, annual payments for 2021, indicated as GD.00.2021 ), TIN of the payer, payer status (13 for individuals, 02 for tax agents, 09 for individual entrepreneurs);

- Next, indicate the purpose of the payment, first name, patronymic, last name of the individual entrepreneur;

- After filling out all these fields, you must indicate the payment amount and confirm it with a code that will be sent to your phone;

- After this, the tax will be debited from your personal account.

How to generate a tax receipt for an individual entrepreneur: step-by-step instructions

Our fictitious individual entrepreneur Apollo Buevy, with the help of “Clerk,” learned to generate payment documents for the payment of contributions, and now we will tell him how to generate receipts for paying taxes through the “Pay Taxes” service on the website of the Federal Tax Service.

We select the document we want to fill out. We fill out a receipt for payment through a bank or the State Services portal, but the payment order is filled out according to the same principle.

Having marked the necessary lines, go to the next page

We are not filling out the KBK yet, it will appear in the required field after selecting the required payment

Many individual entrepreneurs cannot find taxes under special tax regimes (USN, UTII, PSN and Unified Agricultural Tax) in this list. And you need to look for them in the “Taxes on total income” group.

We choose the tax we need. Please note that the type may vary depending on the date. Thus, payments under UTII for periods before 2011 have other BCCs.

When choosing a BCC according to the simplified tax system, pay attention to the object of taxation. There are two of them: “income” and “income reduced by expenses.” There is no separate BCC for the minimum tax as of January 1, 2021; there is no need to look for it.

Now let's choose what will be paid. The tax (payment), penalty or fine. We are not interested in the interest line; taxpayers do not pay them. After making your selection, click the “Next” button and the required code will appear in the KBK field.

On the next page, fill in the address (select the required addresses from the list). The code of the Federal Tax Service and the municipality will appear automatically.

Now let's select the basis for the payment. If we pay the tax within the period established by law, without delay, then we indicate the TP. If tax is paid for previous tax periods, but the claim has not yet been submitted, then select ZD. If the request has already been received, then indicate the TR.

When choosing a tax period, you must take into account that with UTII the period is always a quarter. Those. There is no period of a year or half a year. With the simplified tax system, the periods in the payment document can be quarter, half-year and year. A period of 9 months is not provided, so they usually write the period “quarterly payments” and select the 3rd quarter. Click the “Next” button and proceed to filling out your personal data

The TIN field is not required in the payment document, however, if you are going to pay non-cash electronically, that is, through an online bank or State Services, then the TIN must be filled out.

By clicking the “Pay” button we get a choice of payment method. Please note that if the TIN was not specified, there will be no cashless payment option; you can only save or print a receipt. You can pay the receipt at the bank's cash desk or through a bank terminal that reads the bar code.

Deadline for payment of UTII tax

The reporting period for UTII is a quarter (three months). The UTII tax must be paid up to and including the 25th day of the month following the reporting period . When you need to pay this tax is clear from the following list:

- For the 1st quarter of 2021, payment must be made by 04/25/2021;

- For the 2nd quarter of 2021, payment must be made by July 25, 2021;

- For the 3rd quarter of 2021, payment must be made by October 25, 2021;

- For the 4th quarter of 2021, payment must be made by 01/25/2021.

If the last day for tax payment falls on a weekend or holiday, then the deadline for payment in this case is the first working day following the holiday or weekend.

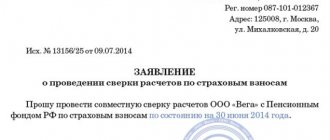

Information about details for paying insurance premiums for individual entrepreneurs

An individual entrepreneur can reduce the tax base/tax for contributions to compulsory pension insurance paid for himself:

| Tax | Procedure for reducing the base/tax on contributions |

| Personal income tax | Individual entrepreneurs have the right to include contributions to compulsory pension insurance for themselves as part of a professional deduction that reduces the personal income tax base |

| STS (object “income”) | Individual entrepreneurs with employees can reduce tax under the simplified tax system (advance payment) by the amount of contributions paid for themselves and for employees, but not more than 50% |

| Individual entrepreneurs without employees can reduce tax under the simplified tax system (advance payment) for the entire amount of the contribution paid | |

| simplified tax system (object “income minus expenses”) | Individual entrepreneurs have the right to include contributions to compulsory pension insurance for themselves as expenses that reduce the tax base under the simplified tax system |

| PSN | Individual entrepreneurs with employees can reduce the tax by the amount of contributions paid for themselves and for employees, but not more than 50% |

| Individual entrepreneurs without employees can reduce tax by the entire amount of the contribution paid |

Contributions reduce the tax/basis of the period in which they are actually paid, but to the extent of the amounts assessed.

It is also worth noting that when combining regimes, there are some nuances to reducing the tax/base for fixed contributions of individual entrepreneurs.

\r\n\r\n

There are innovations for individuals who pay taxes, fees, insurance and other payments administered by the tax authorities. The changes concern field 101 (the status of the payment originator is entered in it).

\r\n\r\n

Until October 2021, when filling out field 101, these individuals must select one of the following values:

\r\n\r\n

- \r\n\t

- “09” - individual entrepreneur who pays taxes, fees, insurance premiums and other payments administered by the tax authorities;

- “10” - a notary engaged in private practice, paying taxes, fees, insurance premiums and other payments administered by the tax authorities;

- “11” - a lawyer who has established a law office that pays taxes, fees, insurance premiums and other payments administered by the tax authorities;

- “12” is the head of a peasant (farm) enterprise who pays taxes, fees, insurance premiums and other payments administered by the tax authorities.

- “13” is an “ordinary” individual.

\r\n\t

\r\n\t

\r\n\t

\r\n\t

\r\n

\r\n\r\n

Starting in October 2021, the values "09", "10", "11" and "12" will be removed. Instead, the value remains, the same for all individuals (“ordinary”, individual entrepreneurs, lawyers, etc.) - “13”. Changes were made by order No. 199n.

When filling out the recipient's details, you need to take into account changes in two fields. Innovations are associated with the transition to a new treasury service and treasury payment system.

- Field 17: the account number of the territorial body of the Federal Treasury (TOFK) is changed;

- Field 15: starting from January 2021, it is necessary to indicate the account number of the recipient's bank (the number of the bank account included in the single treasury account (STA)). In 2021 and earlier, this field was not filled in when paying taxes and contributions.

A clear rule will come into effect in the event that the accounting department deducts money from an employee’s salary to pay off debts to the budget. Next, the withheld amount is transferred to the treasury by a separate payment order. In such a payment in the field “TIN of the payer”, from July 17, 2021, it is strictly prohibited to indicate the identification number of the employing company. Instead, you need to put the TIN of the employee himself (amendments made by Order No. 199n).

KBK that must be indicated when paying UTII

As already mentioned, in order to pay the tax you need to know the details for the transfer. One of these details includes KBK. KBK is an abbreviation for budget classification codes. The BCC is assigned to each tax separately, so it is not recommended to indicate this detail incorrectly, because in this case the tax will go to another budget and you will have to write a letter to the tax office with a request to count the tax according to another BCC. Budget classification codes are established by law and change frequently, so it is necessary to check the relevance of this detail so as not to make a mistake in payment. In 2021, BCCs were established by Order of the Ministry of Finance No. 132n dated 06/08/2021, they are shown in the following table.

| Designation | KBK |

| UTII tax | 182 1 0500 110 |

| Penalties for UTII tax | 182 1 0500 110 |

| Amounts of fines and penalties | 182 1 0500 110 |

What are the BCCs for paying individual entrepreneurs' insurance premiums in 2021?

- Since we entered KBK 18210202140061110160 , we received a receipt for payment of mandatory contributions to the pension insurance of individual entrepreneurs “for ourselves”.

- In order to issue a receipt for payment of the mandatory contribution for medical insurance of an individual entrepreneur “for yourself,” we repeat all the steps, but at the stage of entering the BCC, we indicate a different BCC: 18210202103081013160

Let me remind you once again that this payment must be made strictly before July 1, 2022 (based on the results of 2021, of course).

So here it is. There is no separate BCC for payment of 1%. This means that when it comes time to pay this 1%, you will need to generate exactly the same receipt as for paying contributions to compulsory pension insurance.

That is, when issuing a receipt for payment of 1%, indicate BCC 18210202140061110160 (but it is possible that this BCC will change in 2021. Therefore, follow the news and update your accounting programs in a timely manner).

In fact, you will receive exactly the same receipt as when paying a mandatory contribution to pension insurance. Only there will be a different payment amount, of course.

But finally, I will repeat once again that such payments need to be processed in accounting programs and services. There is no need to do everything manually in the hope of saving several thousand rubles...

For example, these two receipts can be issued in 1C. Entrepreneur" in literally three clicks. Without thoughtfully studying such boring instructions =)

Best regards, Dmitry Robionek.

Receive the most important news for individual entrepreneurs by email!

Stay up to date with changes!

Sanctions for late payment of taxes

If the tax is not paid on time, an organization or individual entrepreneur will be subject to penalties. Penalties consist of a penalty and a fine. Penalties are accrued for each day of tax delay; it is determined as a percentage of the unpaid tax amount. To pay a fine, the Tax Code of the Russian Federation has the concept of unintentional non-payment and intentional non-payment of tax. If there was an unintentional failure to pay the tax, then the penalties, namely a fine, will be 20% of the amount of the unpaid tax, and if there was an intentional failure to pay the tax, then in this case the organization or individual entrepreneur will be fined 40% of the amount of the unpaid tax.

Fixed contributions of individual entrepreneurs for themselves 2021

There are innovations for individuals who pay taxes, fees, insurance and other payments administered by the tax authorities. The changes concern field 101 (the status of the payment originator is entered in it).

Until October 2021, when filling out field 101, these individuals must select one of the following values:

- “09” - individual entrepreneur who pays taxes, fees, insurance premiums and other payments administered by the tax authorities;

- “10” - a notary engaged in private practice, paying taxes, fees, insurance premiums and other payments administered by the tax authorities;

- “11” - a lawyer who has established a law office that pays taxes, fees, insurance premiums and other payments administered by the tax authorities;

- “12” is the head of a peasant (farm) enterprise who pays taxes, fees, insurance premiums and other payments administered by the tax authorities.

- “13” is an “ordinary” individual.

Starting in October 2021, the values "09", "10", "11" and "12" will be removed. Instead, the value remains, the same for all individuals (“ordinary”, individual entrepreneurs, lawyers, etc.) - “13”. Changes were made by order No. 199n.

Starting in 2021, the authorities have abolished the link between fixed individual entrepreneur contributions and the minimum wage (minimum wage). The amount of payments is established by clause 1 of Article 430 of the Tax Code of the Russian Federation.

For 2021, the minimum wage was 7,500 rubles.

For 2021, the minimum wage was 6,204 rubles.

For 2015, the minimum wage was 5,965 rubles.

For 2014, the minimum wage was 5,554 rubles.

For 2013, the minimum wage was 5,205 rubles.

For 2012, the minimum wage was 4,611 rubles.

The amount of contributions to the funds in 2021 is 40,874 rubles, of which:

— the amount of insurance contributions to the Federal Compulsory Medical Insurance Fund in 2021 = 8,426 rubles.

— the amount of insurance contributions to the Pension Fund in 2021 = 32,448 rubles.

If the income of an individual entrepreneur exceeds 300,000 rubles. for 2021, the contribution to the Pension Fund increases by an additional 1% of the excess amount.

An example of calculating an additional contribution to the Pension Fund with an income of 1,000,000 for 2021:

(1,000,000 - 300,000) * 1% = 7,000 rub.

This payment to the Pension Fund must be made no later than April 1, 2021.

The amount of contributions to the funds in 2021 is 36,238 rubles, of which:

— the amount of insurance contributions to the Federal Compulsory Medical Insurance Fund in 2021 = 6,884 rubles.

— the amount of insurance contributions to the Pension Fund in 2021 = 29,354 rubles.

If the income of an individual entrepreneur exceeds 300,000 rubles. for 2021, the contribution to the Pension Fund increases by an additional 1% of the excess amount.

An example of calculating an additional contribution to the Pension Fund with an income of 500,000 for 2021:

(500,000 - 300,000) * 1% = 2,000 rub.

This payment to the Pension Fund must be made no later than April 1, 2020.