The operating cash desk can be used not only by banking institutions, but also by commercial enterprises. In both cases, it is assumed that the cash register is located at a distance from the central office of the organization, and the proceeds after the close of the work shift are transferred to the main cash register of the company. Legal regulation of issues related to the operation of operational cash registers for business entities is carried out by the provisions of the following documents:

- Directive of the Central Bank of the Russian Federation “On the procedure for conducting cash transactions” dated March 11, 2014 No. 3210-U (as amended on June 19, 2017).

- Law on CCP dated May 22, 2003 No. 54-FZ (as amended on July 3, 2018).

- Operating rules for cash register machines, approved by the Ministry of Finance of the Russian Federation, No. 104 of 08/30/1993.

- Chart of accounts, approved. By Order of the Ministry of Finance dated October 31, 2000 No. 94n (as amended on November 8, 2010).

Cash receipt

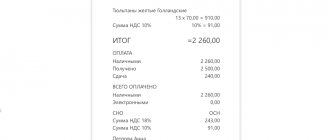

When receiving money for goods, the cashier is obliged to punch the cash receipt and give it to the buyer. The check must indicate:

- name and tax identification number of the company;

- KKM serial number;

- serial number of the check;

- date and time of purchase;

- the price of the product;

- a sign of fiscal mode (these are special characters that confirm that the cash register is registered and its memory operates in fiscal mode).

In addition to the required elements, the check may contain other data that the company or entrepreneur considers necessary (for example, the name of the cashier).

Why is it necessary?

The operating cash desk is a universal tool whose task is to facilitate the direct use of cash. Thanks to it, it is possible to ensure payment for goods or services in foreign currency. During the purchase process, it will be automatically converted into rubles and go to the organization’s balance sheet. In addition, you can abandon your personal cash register, which will eliminate shortages, daily reporting, re-counting of money, delivery of cash to the bank, paperwork, checking banknotes for counterfeiting. In addition, the speed of internal turnover of funds increases, and there is a good opportunity to save money by reducing internal costs. Upon sale, the money immediately goes to the company’s account. In addition, such close relationships make it possible to obtain quick and profitable loans. We should not forget about the possibility of paying for goods using plastic cards.

As you can see, operating cash desks are quite useful. The currency of any country can be used at any time, which has a positive effect on the level of convenience. At the same time, the management of the enterprise does not need to think about various points and nuances. It simply records that it receives money. Everything else is the responsibility of the banks, which are in charge of the funds received.

Daily CCP reports

When working at a cash register, the cashier-operator generates various reports. They are printed by the machine itself.

So, during the day you can take an X-report (sectional report) from it. It is needed to check the receipt of revenue for each department (section) or cash register during a particular shift. The X-report does not affect the readings of money counters, so it can be run many times.

At the end of the working day, the cashier-operator must take a Z-report (control tape). It contains data on the revenue received per day for a specific cash register. The cashier-operator reflects the Z-report readings in a special journal (form No. KM-4 or KM-5). As a rule, Z-reports are pasted into a special notebook and stored for 5 years.

When using cash register equipment, in addition to receipts and cash register reports, you need to prepare a number of other documents. Namely:

- act on transferring the readings of summing cash counters to zeros and registering control counters of the cash register (form No. KM-1);

- act on taking readings of control and summing cash counters when handing over (sending) a cash register machine for repair and when returning it to the organization (form No. KM-2);

- act on the return of funds to buyers (clients) for unused cash receipts (form No. KM-3);

- journal of the cashier-operator (form No. KM-4);

- a journal for recording the readings of summing cash and control counters of cash register machines operating without a cashier-operator (form No. KM-5);

- certificate-report of the cashier-operator (form No. KM-6);

- information on meter readings of cash register machines and the organization’s revenue (form No. KM-7);

- log of calls to technical specialists and registration of work performed (form No. KM-8);

- act on checking cash in the cash register (form No. KM-9).

Please note: The Accounting Law of December 6, 2011 No. 402-FZ, in force since January 1, 2013, abolished the mandatory use of unified forms of primary accounting documents. Therefore, organizations that do not want to use unified forms can develop their own “primary” forms. But not all forms of primary documents can be developed by companies independently. One of these exceptions is forms No. KM1 - KM9, used when working with cash register equipment. Since the use of these forms is related to control in the area of application of cash register equipment, the organization does not have the right to independently develop such forms and can only use standardized forms.

How much money should there be?

Typically, a monthly reserve of funds is provided for expenses. If this is not enough, then the reinforcement of the operating cash desk is used. This is the name of a series of actions that provide for the provision of additional amounts to cover existing requests. The use of this scenario is considered undesirable, so the situation is calculated and assessed in advance to minimize the likelihood of its occurrence. It should be noted that the cash received by the operating cash desk must be spent exactly on what it is intended for (salaries, business or travel expenses). If there is a deviation from this requirement, it is regarded as a violation with all negative consequences.

Act on transferring the readings of summing money meters to zeros (form No. KM-1)

The commissioning of a new cash register is formalized by an act of transferring the readings of summing cash counters to zero (form No. KM-1). A standard form is provided for this act. It was approved by Decree of the State Statistics Committee of Russia dated December 25, 1998 No. 132.

The act is drawn up by a commission appointed by order of the head. Moreover, a tax inspector must participate in the commission. The act is drawn up in two copies:

- the first one remains in the company;

- the second is transferred to the tax office at the place of registration of the cash register.

The completed act is signed by all members of the commission and the head of the company (entrepreneur). The document is stored in its archive for the entire period of operation of the CCP.

What to do if you forgot to take a report

Despite the fact that when using online cash registers, cashiers are not forced to keep journals and take Z-reports, the obligation to hand over the proceeds remains. It is necessary to generate a shift closure document for:

- Monitoring the work of the cashier.

- Quick revenue assessment.

- Transferring the proceeds to collectors.

- Report to the tax authority.

There are many examples from life when cashiers forgot to withdraw a check for closing a shift at the end of the day or did it late. From practice it follows that the tax inspectorate is not biased towards such a violation of discipline if the incident happens once. If violations are repeated systematically, penalties will be imposed.

Important! If the cashier-operator forgot to withdraw the report at the end of the day, he is obliged to draw up a report and an explanatory note.

Documents are kept in case of an audit. Reports on the closure of the shift, generated for the next day, are attached to the cash book.

The new model cash registers provide a document similar to Z-reporting - a report on the closure of a shift. It is adapted according to changes in the technical characteristics of KKM-online. The most important function of reporting is its rapid transfer to the Federal Tax Service.

Z-reports when using online cash registers are not compiled in the form in which they were generated on the old-style cash register with EKLZ. The main task of Z-reports was to reset data based on the results of a worked shift and record information about all operations performed (arrivals, returns, cancellations, discounts). This made it possible to obtain correct information on the volume of revenue for each shift and fill out cash reports.

Act on taking readings of control and summing money meters (form No. KM-2)

The delivery of the cash register for repairs and its return to the company is formalized by an act of taking readings from control and summing cash counters (form No. KM-2). A standard form is provided for this act. It was approved by Decree of the State Statistics Committee of Russia dated December 25, 1998 No. 132.

The act is drawn up by a commission appointed by order of the head. As a rule, it includes the head of the organization (individual entrepreneur), senior cashier, and cashier-operator. The document is drawn up in the presence of a tax inspector and a specialist from a cash register technical service center.

The act reflects the indicators of the summing cash counters at the time of the cash register breakdown. It is filled out in one copy and submitted to the accounting department.

Composition of the operating cash desk

This composition includes receipts, as well as expense cash desks, cash exchange desks, evening cash desks, and cash recalculation desks.

Receipt cash desks are a special type that accepts and transfers cash for the entire operating day. Money is accepted on behalf of enterprises, organizations, individuals, as well as the proceeds of enterprises for crediting funds to a bank account.

Expense cash desks are cash desks that issue cash from the bank's cash desk to organizations, institutions, individual borrowers who obtain loans from the bank, depositors, and individuals. persons receiving cash from personal current accounts.

Evening cash desk is a cash desk that accepts cash from businesses after the end of the working day, as well as collection bags with cash received from bank collectors.

Cash counters – cash desks that count, sort and package money from businesses and banks. Cash recalculation is carried out by cashiers of counting teams. Each individual team is regulated by a controller. The recounting cash office employees are fully financially responsible for the valuables they have acquired.

Depending on the various types of services, banks can create cash desks for accepting utility payments, depositary cash desks, as well as a variety of cash desks for selling commemorative or, for example, anniversary coins, and the like. Excess money from the operating cash desk of banks goes to the working cash desk of a certain territorial department of the National Bank. If the bank needs money, it goes to the bank’s operating cash desk from the working cash desk of the National Bank’s management. Within the predetermined time frame, as well as when there is a change in financially responsible persons, an audit of the cash of the operating cash desk is carried out.

Certificate-report of the cashier-operator (form No. KM-6)

A standard form is provided for this document. Its form was approved by Decree of the State Statistics Committee of Russia dated December 25, 1998 No. 132.

The report is prepared daily by the cashier-operator. Meter readings at the beginning and end of the day (shift) are certified by an administration representative (for example, the head of a section).

The report is drawn up at the end of the working day (shift) and submitted to the senior cashier along with the revenue. It is signed by the cashier-operator, the senior cashier and the head of the company (entrepreneur).

About the limit

But accumulating too much money is also not welcome. When an agreement is concluded, it is stipulated that the operating cash account should not exceed a certain value. There are often penalties if this clause is violated. The only exception is that you are allowed to exceed the limit by three days, but only when wages are paid. In the opposite case, from 40 to 50 thousand rubles can be recovered from the organization and in addition from its head from 4,000 to 5,000. Although the amounts are not very large, it is still better not to fall for them.

Information on meter readings of cash register machines and the organization’s revenue (form No. KM-7)

This document is drawn up if the company uses several cash registers. The form for it was approved by Decree of the State Statistics Committee of Russia dated December 25, 1998 No. 132. It is filled out daily in one copy by the senior cashier, and signed by both the senior cashier and the head of the company (entrepreneur).

Data on the revenue of each department or section must be confirmed by the signatures of the heads of departments (sections).

The completed document, along with certificates-reports from cashiers-operators, cash orders and acts on the return of money to customers, is transferred to the accounting department.

Accounting points

To summarize information about the movement and availability of funds, as well as related documentation, account 50 “Cash” is used. Cash inflows are shown as debits and expenses as credits. If cash transactions are carried out, then the corresponding sub-accounts must be opened, such as 50-1 (2,3...). How do you get cash? Initially, you need to issue a cash receipt order. Then a record of admission is made in Form N KO-4. How is cash issued? Initially, an expense cash order is drawn up. Then an entry is made about the issuance of money, using the same formula. This is how the operating cash desk operates.

It is important to carry out an inventory. In essence, this is a reconciliation of cash balances in the cash register with accounting data according to documents. It is imperative to take into account the debit of account 50. Regulatory documentation provides for mandatory inventory. For example, when there is a cashier change. To avoid confusion and ridiculous accusations, inventory is mandatory. Additional checks may be carried out in accordance with accepted accounting policies.

Journal of calls for technical specialists and registration of work performed (form No. KM-8)

It is used if:

- It is impossible to fix a cash register malfunction by the cashier. In this case, the administration calls a specialist from the KKM technical service center;

- A technical service center specialist carries out scheduled technical inspections, including checking the condition of the mechanisms of the electronic and software parts of the machine, as well as eliminating minor faults.

Entries in the log are made by a specialist from the KKM technical service center. This journal is kept by the head of the trade organization or his deputy.

The unified form No. KM-8 was approved by Decree of the State Statistics Committee of Russia dated December 25, 1998 No. 132.

Sample filling KM-Z

Any transactions involving cash require an application from the client.

Application requirements:

- the buyer's application is made in writing, in any form;

- in the upper part you need to indicate the name of the organization, address and yourself with a phone number, in the main part briefly state the reason for the return, put a date and signature with a transcript

- To issue funds, the cashier will need permission from a superior employee who has the authority to authorize the return of funds.

Important! If there is no resolution from the boss, a return is impossible and then drawing up an act is not required.

Drawing up an act is necessary in the following cases:

- the presence of the above-described reasons and grounds;

- the fact that the date the check was punched coincides with the date of the return;

- method of payment for the purchase.

The cashier, before starting to process the return and draw up the report, should check:

date of purchase, because refunds are possible only within two weeks

how was the item paid for?

If the payment was made by credit card, then it is impossible to return the funds in cash and there is no need to draw up a report in this case.

Important! Having completed the return certificate in accordance with the form, you must attach the client’s application with the receipt and make an entry in the cashier’s journal.

Thus, we can conclude that for old cash registers a return can be issued only on the day of purchase, and also precisely at the cash register where the goods were purchased.

Certificate of verification of cash at the cash register (form No. KM-9)

This act reflects the results of a sudden audit of cash in the operating cash desk.

As a rule, the results of the audit are compiled by the tax inspector and the cashier-operator. They are then brought to the attention of the head of the company.

The act consists of:

· in triplicate - if the audit is carried out with the participation of a tax inspector. In this case, one copy of the act is submitted to the tax office;

· in duplicate - if the audit is carried out on the initiative of the enterprise administration. One copy of the act is transferred to the accounting department, the second remains with the financially responsible person (cashier-operator).

The unified form No. KM-9 was approved by Decree of the State Statistics Committee of Russia dated December 25, 1998 No. 132.

general information

First, let's understand the term “operating cash desk”. What it is? This is the name of a special division of the bank that provides settlement and cash services on the territory of a certain company. It is necessary for enterprises that provide the public with access to services and goods, such as: wholesale and retail stores, car dealerships, points of sale of electronics, jewelry, travel agencies, etc.

The bank's operating cash desk acts as a tool for using cash. Why is it necessary? How is it settled? What are the requirements?

Return of goods on the day of purchase

If the buyer decides to return the goods one or more days after purchase, the money will be given to him from the main cash register. If he returns the purchased goods on the day of purchase, then the money is issued from the operating cash register. It goes like this.

First, the buyer who is returning the product must bring a sales receipt. The check is signed by the director or his deputy. After this, the cashier-operator is obliged to return the money to the person.

The receipt received from the buyer is glued to a separate sheet of paper.

The amount issued is recorded in column 15 of the cashier-operator’s journal. The proceeds for the day when the goods were returned to you will be reduced by this amount.

If a person bought several items of goods using one cash receipt, but returns only one of them (for example, he purchased an electric kettle and an iron, but returns only the iron), he will have to give you a receipt for two goods.

In this case, it is necessary to make a copy of the cash receipt, certify it (sign and affix the company seal) and give it to the buyer.

Secondly, you will need to draw up a certificate of return of the goods. Indicate in it the name of the returned product, its price, the number of the receipt issued to the buyer, the date and reason for the return. There is no unified form of such an act. To do this, you can use the invoice in form No. TORG-12 (approved by Decree of the State Statistics Committee of Russia dated December 25, 1998 No. 132).

And finally, thirdly, you will need to draw up an act on the return of money to buyers (clients) for unused cash receipts (Form No. KM-3).

The returned cash receipt (previously pasted on a sheet of paper), the act in form No. KM-3 and the act (invoice) on the return of the goods must be submitted to the accounting department.

Arrangement process

To build an operating cash desk, you need approximately three to five thousand US dollars. Maintenance every month additionally costs 750-900 green “presidents”. Also, to open an operating cash desk, you need to take care of the availability of a cash register that will meet all the requirements that apply to banks in the Russian Federation. Thus, the workplace must be fenced off from clients and the external premises with bulletproof glass that can withstand shots from firearms. In addition, you must have a special device for negotiations, a cash tray and an alarm button. It is also necessary to connect the premises to the centralized security monitoring console or to the police control room. We should not forget about the necessary equipment: computer, printer, modem.

It is important to note that banks carry out unique and individual technical work separately for each enterprise. Therefore, tariffs for servicing operating cash desks are in an unclearly defined range. Well, the bank in whose favor the choice is made has a certain influence.