The company must set the maximum amount of cash that can constantly be in the cash register: for this, the cash register limit is determined. A sample order with a calculation attached is below on the page.

Running a cash register is convenient and easy in MySklada: cash transactions, tracking balances, printing outgoing and incoming orders, registering retail sales through the cashier’s workplace, as well as automatically creating a PKO when closing a shift and generating a Z-report at the point of sale. Try MoySklad - in the first two weeks all features of the service are completely free.

Try it

Here you can download the cash limit order for 2021 for free.

Download the order for free!

Register in the online document printing service MoySklad, where you can: completely free of charge:

- Download the form you are interested in in Excel or Word format

- Fill out and print the document online (this is very convenient)

The order is issued by the head of the organization for any period - month, quarter, year, etc. The validity period of the cash register limit may not be specified. Then you can work with him until a new order is issued. Calculation formulas and illustrative examples are given below.

We decipher the concept of “cash limit”

In simple terms, the phrase “cash limit” is deciphered quite simply: this is the maximum allowable amount of cash in the cash vault, safe or cash register of a commercial company at the end of the day. This norm was introduced by the Central Bank of the Russian Federation, and the accounting department of an enterprise must set this limit individually at the beginning of each calendar year.

Setting and maintaining a cash limit is a headache for many accountants. In order to avoid surpluses, they have to constantly monitor cash, and if in the evening there is suddenly more money in the cash register than the established norm, then the accounting representative needs to go to the bank to deposit funds into the company’s current accounts. Otherwise, it is unlikely that you will be able to avoid administrative punishment during any inspection.

conclusions

Establishing, approving and subsequently enforcing a maximum limit on cash balances are important aspects of maintaining financial discipline in an organization.

Limiting the maximum amount of cash allowed for storage (withholding) in the cash desk of an enterprise at the end of the operating day is the prerogative of the management of the business entity.

You just need to follow the generally binding rules contained in the Directive of the Central Bank of the Russian Federation, which regulates the procedure for calculating and applying this limit.

This limit can be set for any period, revising the specified standard if necessary. However, it should be remembered that exceeding this limit, approved by order of the enterprise management, may result in the imposition of fines.

As it was before

Previously, absolutely all enterprises and organizations dealing with cash had to limit the remaining funds in the cash register. Since June 2014, this practice has changed: now some business representatives may not set limits. It is not surprising that many wanted to exercise this right.

However, audits carried out by tax authorities discovered some violations caused by insufficient knowledge of the legislative framework regarding the unlimited maintenance of cash balances and, as a result, applied penalties to a number of enterprises and organizations.

That is why, in order to avoid claims from tax authorities, you need to exercise your right to an unlimited cash register competently and with a clear understanding of all the rules of this process.

Procedure for filling out the form

The document must contain lines with initial data, which can be formatted as a table.

After this, a direct calculation of the cash balance limit in the cash register is recorded. The company has the right to round the resulting value to whole rubles.

The limit is signed by the chief accountant, and the date of its preparation is indicated.

Based on the calculation, an order is issued for its approval, which includes the date and place of preparation and title. In the preamble it is necessary to make a reference to the current regulatory act that regulates this issue.

In the administrative part of the document, the limit amount is introduced and the time period for depositing the proceeds (receiving money) to the bank is indicated. The date from which this restriction comes into effect is also indicated here.

The order must be recorded in the document registration book.

Control over the use of this order, as well as bringing it to the attention of cashiers, is assigned to the chief accountant or other authorized official.

The appendix to this order must include a calculation of the cash limit.

Newly created organizations must calculate the limit on storing cash in the cash register on a general basis. However, they do not have the necessary initial data to determine it. These firms can use the expected volume of cash receipts for goods sold, services rendered, work performed, or the expected volume of cash issued.

For companies whose activities were interrupted, it is allowed to use data for previous periods, or when these indicators reached their maximum value.

When determining the period between collections or receipt of funds, force majeure may act (for example, a bank or enterprise was temporarily closed). Then this indicator should be determined after the influence of these factors ceases.

In what cases is exceeding the limit at the cash register acceptable?

As stated in the law, on strictly defined days, enterprises and organizations can quite legitimately allow cash surpluses. In particular:

- If payment of wages, social, material assistance, scholarships, etc. is expected, but no more than five working days from the date of withdrawal of money for these purposes from the company’s current account;

- If cash transactions are carried out on non-working holidays or weekends, there may also be amounts in the cash register above the limit values.

Any other circumstances cannot serve as an excuse for exceeding the limit and will inevitably entail administrative punishment in the form of fines.

Why do you need a cash limit and how is it set?

Establishing a limit limits the amount of cash that may be in the operating cash desk at the end of the working day (clause 2 of Bank of Russia Directive No. 3210-U). The limit may be exceeded on days when employees are paid salaries, scholarships, social benefits, and on weekends if the legal entity carries out cash transactions there.

Determining the amount of the limit is mandatory for legal entities and separate divisions that independently deposit money to the bank. If separate divisions deposit money at the cash desk of a legal entity, then the total amount of the limit established by the organization also takes into account those limits that are provided for the divisions. Individual entrepreneurs and legal entities classified as small businesses have the right not to set such a limit.

Read about the cases in which a legal entity can be classified as a small business entity here.

The legal entity independently calculates the cash balance limit (for divisions and its total value) and approves its size with an administrative document. One of the copies of this document is sent to the division.

If you can’t, but really want to: the right to refuse the cash limit

The law gives some categories of enterprises and organizations, as well as individual entrepreneurs, the right to refuse to maintain the maximum established financial indicators at the cash desk.

Commercial companies classified as small businesses, as well as all individual entrepreneurs, can take advantage of this right, regardless of the tax regime they apply.

Waiving the limit at the cash register does not imply any special actions; it is quite enough to simply meet certain parameters:

- maximum income - no more than 800 thousand excluding VAT for services performed and goods sold;

- limited personnel - for the last calendar year, the number of employees at the enterprise should not exceed 100 people;

- participation in the authorized capital - no more than a quarter of the share of other legal entities.

If a company meets these requirements, then it can safely keep unlimited funds in the cash register.

In cases where the right to no cash limit arises not from the moment of registration of the enterprise, but, for some other reasons, in the course of its activities, then in order to use it, the management of the enterprise needs to take the following steps:

- In a written resolution, cancel the previously issued order establishing a cash limit;

- Issue a new order stating that from such and such a date there is no cash limit.

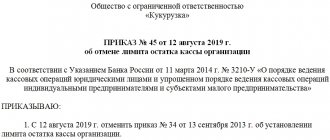

Sample order

Let's look at samples of an order establishing a cash limit for two companies: a new one and an existing one.

The document is printed on the organization’s corporate letterhead, if any, and must be numbered, dated and signed by both the manager who issued the order (general director, individual entrepreneur) and the officials responsible for compliance (accountant, cashiers).

The order may also contain additional clauses regarding liability for exceeding the limit or procedures for preventing such situations.

A detailed calculation of the established limit can be included both in the text of the document itself and in the appendix.

you can order here.

Setting a cash limit: procedure and rules

As mentioned above, all large enterprises and organizations are required to introduce cash restrictions. If this is not done, then by law the cash limit is considered zero. In order to set a limit on the finances stored in the cash register, the head of the enterprise or organization needs to issue a corresponding order. There is no need to submit any applications or notifications to the tax authority.

Attention! Individual entrepreneurs or legal entities working in the field of small and medium-sized businesses can set a cash limit on their own initiative.

As a rule, the justification for such actions is the desire to ensure control over the safety of cash. At the same time, you need to understand that if the corresponding order is issued and the cash limit is set, then the accounting department of the enterprise or individual entrepreneur is obliged to comply with it, and take all the excess to the bank. If any violations are discovered during the audit, tax inspectors will certainly resort to administrative punishment.

What document is required for an individual entrepreneur?

Despite the democratic nature of the new CBR act, individual entrepreneurs were not exempted from all documents drawn up during cash transactions. The issuance of money on account must still be documented. Such accounting is mandatory. The basic rules of the Central Bank of Russia in this regard establish the following:

- When an individual entrepreneur himself takes money from the cash register for any needs, for example, for a taxi, then an application is not drawn up, and a report on the money issued is drawn up at the discretion of the entrepreneur. You can draw up a separate document or display the issuance of money in KuDiR as an expense.

- If an individual entrepreneur gives money to his employee, then he must first receive a statement from him about the need to issue funds for certain needs. The employee must later submit a report on the funds received and return the balance.

It is worth noting that the new Directive of the Central Bank introduced ambiguity in the situation with hired employees. It does not clarify whether similar requirements apply to persons working under an employment contract, for example, freelancers, online workers. Therefore, it is not yet clear what to do with such agreements and how to register them.

However, the issuance of money to such persons is recognized as the issuance of funds on account. Therefore, even if there is not an employment, but a civil law contract with a person, the issuance of money is carried out exclusively on account. For convenience, an individual entrepreneur can determine an example of filling out such a document independently.

How to calculate cash limit

This is the question that most interests novice accountants. There is no need to rack your brains over it - calculation options are provided for by law:

- Based on the volume of cash receipts using the formula:

Limit = Revenue / Billing period x Days - By the volume of cash issuance (if there is no cash proceeds) using the formula:

Limit = Issues / Billing period x Days

Explanations:

Revenue is the amount of funds from the sale of services and the sale of goods. If the enterprise has just been created, then here you need to indicate the expected amount of revenue;

The billing period is from 1 to 91 days inclusive. It can be chosen absolutely arbitrarily;

Days – from 7-14 working days between cash deposits. It should be remembered that the fewer the number of days, the less money should remain in the cash register.

Thus, if an enterprise, due to circumstances established by law, is obliged to strictly observe cash discipline, carry out nightly calculations of daily revenue and deposit balances with the bank, then this must be done in accordance with all the rules and regulations established by the legislator. Otherwise, it is unlikely to be able to avoid administrative sanctions from regulatory authorities.

Cash discipline for online cash registers in 2021

Cash discipline presupposes compliance with the rules for cash payments, including the determination of the cash limit.

Since cash is used not only in trade organizations, but also where there is movement of cash, cash discipline applies to all legal entities. For example, CCT is needed when:

- payment of wages,

- money collection,

- return or issuance of borrowed funds,

- receiving or depositing cash at the bank,

- settlements with accountable persons.

In 2021, all LLCs and individual entrepreneurs were required to start using online cash registers for cash payments, except for PSN and UTII payers with services and vending. By July 1, 2021, entrepreneurs on UTII and PSN without hired employees had to switch to online cash registers. If a decision was made to hire an employee before July 1, 2021, you need to install a cash register within a month from the moment the contract was signed. Read more: Online cash registers and small businesses.

When using an online cash register, legal entities must still fill out the PKO, RKO, cash book and determine the cash limit. But some documents may not be kept.

So, after installing an online cash register, it is no longer necessary to use the register and certificate of the cashier-operator.

Failure to comply with the limit does not affect the recognition of expenses

So, we found out that cash payments in excess of the limit are an administrative offense and are punishable by a fine.

At the same time, the question often arises: can violation of cash payment restrictions lead to withdrawal of expenses? After all, tax authorities use all the tricks to do this.

If this happens, you can go to court. The court will support you if the transactions performed are real, the expenses are justified and the documents supporting them are in order (see, for example, the Determination of the Volga District Court of April 28, 2021 No. F06-23175/2015 in case No. A65-14760/2014).

If the transaction is real and the costs are justified, violations of cash limits should not be reflected in tax liabilities.

Example of calculations based on revenue volume

Let's look at how to calculate the cash register limit using the following data: the trading cash desk receives revenue daily. The calculation period is the first quarter of last year. The proceeds are handed over once every 4 days. The company works seven days a week. Let's do the following:

- Let's calculate the number of working days in a quarter. The condition states that the company operates throughout the working week, therefore, the billing period consists of 90 days.

- The volume of revenue received, which was identified on the basis of data from accounts 50, 90 and 62, amounted to 4,856,548 rubles, namely: in January - 1,558,884 rubles, in February - 1,240,058 rubles, in March - 2,057,606 R.

- Let's calculate the cash register limit for the first quarter: L = 4,856,548 ÷ 90 × 4 = 215,846 rubles.

Based on the results, the head of the company issued an order approving the limit.