As you know, during an audit, tax authorities study the organization’s primary documents. If certain violations in their conduct are revealed, the taxpayer may be denied VAT deduction and recognition of income tax expenses. In addition, in recent years, tax authorities have been paying great attention to the process of interaction between the audited organization and its counterparties. And now the decisive factor in recognizing deductions and expenses is not so much the competent execution of the primary document, but rather how conscientiously the company prepared for the transaction and checked its partners.

In this sense, business transactions and actions of authorized persons will be checked for the following suspicions:

- in obtaining unjustified tax benefits;

- in dishonesty of the company and the counterparty;

- in collaboration with ephemera;

- failure to exercise due diligence when choosing a counterparty;

- in the creation of several interrelated organizations in order to optimize taxation;

- in the absence of business purposes for the implementation of which the transaction was carried out;

- in the unreality of the transaction.

As you can see, most of these suspicions are somehow related to the interaction between the company and its business partners. Today it is not enough to simply carefully select counterparties - you need to documentably convince representatives of the Federal Tax Service that you acted prudently and in good faith.

The principle of due diligence becomes paramount when choosing contractors. Therefore, it is advisable for taxpayers to develop and approve some provision to comply with this principle. It may be called, for example, the Due Diligence Regulation. What should be included in this document?

Due Diligence

According to the resolution of the Plenum of the Supreme Arbitration Court dated October 12, 2006 No. 53 “On the assessment by arbitration courts of the validity of the taxpayer’s receipt of a tax benefit,” a tax benefit may be recognized as unjustified if it is proven that the taxpayer acted without due diligence and caution and he should have been aware of violations committed by the counterparty.

But over the past 13 years, the term itself and the boundaries of due diligence have undergone significant changes. If previously, due diligence could be reduced to requesting a standard set of constituent documents from the counterparty, now this is not enough for the tax authorities and the court.

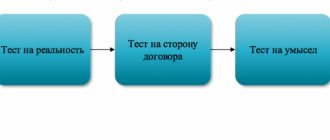

It is necessary to prove the reality of business activities and the reality of transactions and their execution with many documents: these are papers on pre-contractual interaction, as well as documents indicating the mutual fulfillment of obligations under the contract (not only shipping documents, but also, for example, passes to the warehouse, business correspondence, orders for shipments made through correspondence in instant messengers or by email, etc.). But even perfect paperwork may not help if the tax authorities, during the audit, receive statements from company employees that do not correlate with the documents.

Among other things, if additional taxes or other actions lead to the bankruptcy of a company, its manager and founder face quite significant risks of being held vicariously liable and having to compensate for losses to all creditors of the company.

Where to “dig”

In order to thoroughly check the entire VAT chain down to the nth link, Federal Tax Service specialists must prove the following:

- the counterparty is legally or economically dependent on the company being inspected, directly or through interdependence with other counterparties;

- the facts confirm that the parties to the transaction acted in collusion or that the transaction was not real.

So, the primary thing for tax authorities should be that the company being audited carefully chose a counterparty and carried out a real transaction with it. At the same time, for example, the fact that the person who signed the document denies this is not yet a reason to accuse the taxpayer of imprudence.

Blocking of accounts by the bank

Over the past 3-4 years, banks have increasingly begun to refuse to carry out transactions and disconnect from remote banking services (RBS) if, in their opinion, the client’s transactions are of a dubious or suspicious nature. This is required of them by Anti-Money Laundering Law No. 115-FZ. They assess the need to apply such measures according to two groups of criteria. These are, firstly, criteria that characterize the client himself, that is, the company - address, manager, tax burden, availability of funds to conduct the declared type of activity, as well as payment from the account for rent, office supplies, utilities, etc. The second group is criteria characterizing the operations being carried out, for example, the correlation between the declared type of activity and the purpose of payments, the frequency of payments, the volume of cash withdrawals or payments to individuals, transfers to organizations with a high level of risk, etc. It is the counterparties with a high level of risk who most often become cause of disconnection from service and blocking of operations. A harbinger of such developments is requests from the bank. If the counterparty is on the “black” list of the Bank of Russia, the likelihood of questions and problems with the bank is very high.

Court decisions

The mobile operator paid for the mistake

Robbery for robbery - discord: how to achieve a lenient sentence under a “harsh” article

Penalty from the developer Dalpiterstroy

The case of a refrigerator with a defect: a light bulb costing 53,964 rubles

The store refused to refund money for non-working goods

Car missing from the parking lot

Potential losses

In the activities of most companies, there are risks of non-receipt of payment from counterparties, which entails a long negotiation process, hanging accounts receivable and costs of litigation, after which it may turn out that the debtor has nothing to pay. Such situations, in addition to the costs of servicing them, entail the withdrawal of funds from the company’s turnover and, as a result, direct losses.

Assessing the solvency of the counterparty, even if it was recommended for cooperation by trusted persons, can promptly draw attention to risks and prevent losses.

How to check a counterparty correctly?

There is no universal solution: it all depends on the size of the company, its type of activity, the frequency of new counterparties and other factors. There are three verification schemes:

- independent, with the help of its employees

- outsourcing on an ongoing basis or outsourcing as needed

- engaging consultants to set up business processes within the company, develop individual regulations and other documents, as well as train employees.

On one's own

It is advisable to carry out verification of counterparties if there is a sufficient number of qualified personnel, the necessary software, developed regulations (which exist not just on paper from templates found somewhere, but actually work as part of the overall business process), and clearly organized document flow. Qualified personnel are needed to understand the essence of the audit, methodology, correctly record the results and communicate them to decision makers. As a rule, in large and some medium-sized companies this is done by security personnel with the assistance of lawyers.

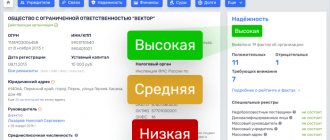

Organized document flow and regulations are necessary for quick and high-quality implementation of pre-contractual and periodic verification of counterparties. As a rule, an audit begins with a request from the counterparty for a list of documents, including, in addition to statutory documents, information about debts to the budget, tax returns, staffing, a certificate of material and technical resources, and others. At the same time, the counterparty is checked using open sources of information (SPARK, Kontur-Focus, etc. do this quickly and efficiently, with a little analytics on the company being checked).

The use of modern software significantly reduces the time required to verify a counterparty and helps to quickly check the company’s connections, assess the current financial condition, court cases, and obtain information about government audits and their results. Reports from such software became one of the evidence of due diligence in court in a dispute with the tax authorities (for example, cases No. A49-1953/2017; A03-2471/2017).

Involvement of third parties

has many advantages: your employees are not burdened with side work, you receive a comprehensive report, including information that is not available in open sources (for example, about the presence of a counterparty on the “black” list of the Bank of Russia).

This option is convenient and cost-effective for small companies that need to check up to 15-20 counterparties within a month. But outsourcing will not be suitable for companies that must check several dozen counterparties a day: it will be unprofitable compared to setting up the process in the company itself and dedicating several full-time employees. The option of hiring consultants to set up a business process for verifying counterparties within the company

is suitable for large, medium and small organizations. This is a universal solution that allows you to set up work and optimize processes and costs for their implementation to obtain fast and high-quality results on an ongoing basis. As a rule, the involvement of consultants includes the individual development of internal company regulations (regulations, orders, etc.), training of responsible employees using real examples and analysis of all issues, testing the performance of the implemented mechanism and, if necessary, debugging it to increase efficiency.

Customer Reviews

Gratitude from Evgeniy N. I express my gratitude to Alexander Viktorovich Pavlyuchenko for the qualified management of my case, competent advice and informed decisions, which led to compensation for all claimed losses.

Sincerely, Evgeniy N., November 17, 2017

Gratitude from Piskunov I.B. I just don’t have words to express my gratitude to Sergei Vyacheslavovich. Thank you for having such a lawyer. Thank you for your help regarding the issue regarding the employment contract.

Piskunov I.B. 12/12/2018

Gratitude to Vasily Anatolyevich Dear Lyubov Vladimirovna.

I would like to express my gratitude to Vasily Anatolyevich for his competent legal assistance in solving my difficult case. I wish you and your company further prosperity and success in your hard work.

From the bottom of my heart and with best wishes. 05/03/2018

Customer Feedback We thank the employees of Legal Agency of St. Petersburg LLC and, first of all, Yana Maksimovna Matveeva and Andrey Valerievich Ermakov for their highly qualified and thorough consideration of our issue and the prompt solution to our housing problem.

Also to Daria Valentivna Kutuzov for her attentive and friendly attitude towards visitors.

Gratitude from Tunnova L. Sergey Vyacheslavovich! Thank you for the qualified advice you provided regarding my question in the field of consumer protection (dispute with TC OPT, the kitchen was not delivered)

Lyubov Tunnova December 12, 2018

Letter of thanks

Gratitude from Volkotrub Yuri Vasilyevich Thank you very much for the quality advice on the issue that interests me. With best wishes to Denis Yuryevich Stepanov, who advised me.

Volkotrub Yuri Vasilievich

Thanks from Radhuan M.R. Dear Kavaliauskas Vasily Anatolievich. Let me express my sincere gratitude for the qualified legal assistance provided. Thanks to your professionalism, I was able to achieve a decision in my favor. I wish you further prosperity and professionalism.

Radhuan M.R. 06/08/2018

Gratitude from Marina Kuleshova I express my deep gratitude to Alexander Viktorovich Pavlyuchenko for his competent legal work and professionalism, as well as to his assistant Elena Vladimirovna for the qualified assistance provided. I wish you prosperity and achievement of professional heights.

Sincerely, Marina Kuleshova. 08/15/2018

Gratitude to Sukhovarov I, Dmitry Vladimirovich Korchagin, express my gratitude and appreciation to lawyer Yuri Vladimirovich Sukhovarov for high-quality and qualified advice. Thank you.

What to look for when checking a counterparty

There are a lot of red flags when checking a counterparty; it all depends on the type of activity and the selection criteria. The main risk factors may be:

- mass address;

- combination of different types of OKVED;

- short period of work of the counterparty;

- the coincidence of the founder and the manager in one person;

- “vicious” connections with previously liquidated companies;

- being on the “black” list of the Bank of Russia;

- lack of staff and resources to perform the proposed contract;

- low tax burden;

- negative financial indicators;

- increasing inspections of government agencies and identifying violations;

- invalid passport of the founder or manager;

- being in the liquidation stage;

- many unfulfilled enforcement proceedings;

- facts of blocking of accounts by the Federal Tax Service.

This is not a complete list of risk factors that may affect the assessment of the possibility of working with a counterparty. Each indicator has its own weight, and many of them individually are not an obstacle to cooperation, but if there are several factors, then it’s worth thinking about. For example, if you are only interested in the issue of reducing tax risks, then factors such as being on the “black” list of the Bank of Russia, negative financial indicators or increasing inspections by government agencies may not have any significance at all in assessing the counterparty. A properly conducted verification of the counterparty allows you to properly structure your work, set yourself up for possible communication with the bank regarding transactions carried out under the concluded agreement, and also prevent potential losses.

And setting up a business process for verifying a counterparty allows you to prepare for changes to the “anti-money laundering” law 115-FZ, which establishes a number of responsibilities for all legal entities without exception. Failure to comply with procedures aimed at establishing the integrity of counterparties leads to fines of 1 million rubles.

Subscribe to our channel in Yandex Zen.

Basic provisions

The first thing that needs to be indicated in the regulations is the purpose of its preparation, that is, the prevention (reduction) of risks associated with the choice of business partners. It is advisable to describe these risks - these are arrears of taxes, penalties and fines, that is, those payments that, as a result of an audit, a company may face for negligence.

It is also worth noting in the regulations that it is approved by order and is mandatory for execution by the parties to the transaction both before the conclusion of the contract and during its execution. This means that before an agreement with a counterparty is signed, he must be familiar with the provisions of the regulations. To ensure this, it is advisable to post the regulations on the company’s official website in the section for potential partners.