As it was before

Before the introduction of the mentioned norm in the Civil Code of the Russian Federation, VAT, the deduction of which was denied, could not be recovered from the counterparty - the courts did not recognize such a right. The arbitrators indicated: the taxpayer receives a deduction if all conditions specified by law are met and does not have the right to shift responsibility for the refusal to his business partners . The requirement to receive a tax deduction can only be presented to tax authorities who refused to recognize it, and the counterparty has nothing to do with it (resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 23, 2013 No. 2852/13 in case A56-4550/2012, resolution 9AAS dated March 19, 2015 No. 09AP-605415).

At the same time, the arbitrators pointed out that Article 15 of the Civil Code of the Russian Federation, which talks about compensation for losses, cannot be applied to tax relations related to the refund of VAT from the budget. In addition, the fact that the tax authorities refused to accept a deduction due to the actions of the counterparty does not mean that they were illegal.

As a result, additional charges of VAT, other taxes, as well as penalties and fines that the company received due to the dishonest actions of the counterparty were not recognized by the courts as losses subject to compensation by the other party to the transaction.

What do tax authorities do when they find a VAT gap?

In case of any gap, tax authorities send requests to both parties to the transaction. And further actions of inspectors depend on the specific situation.

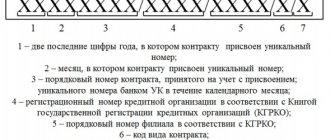

The ASK VAT-2 system builds a “tree of connections” in which not only the supplier “closest” to the taxpayer being checked is visible, but also the entire chain.

Each organization in the system is assigned its own color depending on the degree of tax risk (letter of the Federal Tax Service of the Russian Federation dated 06/03/2016 N ED-4-15 / [email protected] ).

- Green color – low risk. The organization fulfills its tax obligations, actually conducts business, and has assets.

- Yellow color – medium risk. The organization really works, but periodically violates its obligations to the budget.

- Red color – high risk. The company either does not pay taxes at all, or does so in a minimal amount; there are no assets.

Companies classified as medium and high risk are subject to enhanced control. The same applies to their counterparties throughout the chain.

What changed

After the appearance of Article 431.2 in the Civil Code of the Russian Federation, the situation changed. The concept of a “representation of circumstances” introduced by her allows the party that relied on those representations to claim damages or penalties from the party that made them. And if the assurances were significant, you can demand termination of the contract.

In an example it looks like this:

The company has secured the assurance of its potential counterparty that it pays all taxes on time, maintains accounting records and records, draws up all primary documents and, in general, is an exemplary taxpayer. The counterparty assured that he has the goods, and the documents in accordance with which they were received will be provided upon request. Relying on these assurances, the taxpayer decides to enter into an agreement with this counterparty.

Let's assume the delivery was successful and the deal is closed. However, by deducting VAT from this transaction, the taxpayer receives a refusal. Having checked the counterparty’s transactions with its suppliers, inspectors determined that the transactions were formal in nature with the aim of obtaining unjustified tax benefits.

Previously, the company would not have been able to recover VAT from the seller (for reasons stated above), but now this is possible. Let's look at how exactly - using an example from judicial practice.

To obtain a VAT deduction, it is not enough to prove that the transaction is real

Courts have begun to recognize the expenses of organizations to reduce the tax base for paying deductions on profits as justified, but at the same time they refuse to deduct VAT for the same transactions. Now it is not enough for firms to prove only the reality of the transaction.

In order to maintain deductions, it is necessary to convince inspectors and the court that the transaction was actually completed by the counterparty specified in the contract.

Example: it is not enough to prove that the cars that are recorded in the waybill entered the territory of the organization. You need to convince the court that the transport belongs to the counterparty. It is also not enough to simply provide data on the number of employees who usually order from the counterparty. It is necessary to prove that the employees who provide services are on the staff of the counterparty.

A new trend in judicial practice is clearly visible within the framework of transport expedition and transportation contracts.

Example: to prove its right to deduct VAT, an organization submitted an agreement for forwarding services, transport invoices, forwarder reports, invoices, delivery and acceptance certificates for transport services, applications.

At the same time, the Federal Tax Service established, but the organization did not deny, that the forwarder did not have vehicles, the names of the drivers and employees of the disputed counterparty do not match, the cars belong to entrepreneurs and citizens who do not pay VAT.

The court concluded: since the counterparty did not have the resources, it means that the service was performed by another organization. The cassation declared VAT deductions illegal.

The Supreme Court also confirms the findings of the lower courts. The LLC must prove not only the reality of the transaction itself, but also that it purchased the service from the counterparty, who is recorded in the documents.

In cases involving transactions with goods, judges also do not accept VAT deductions. Example: The Federal Tax Service removed the deduction from the organization because the counterparty did not have material and labor resources. This means that he signed the papers, but in fact the transaction was executed by someone else. That is, the company did not fulfill the condition regarding the reliability of documents from Article 169 of the Tax Code.

When forming a position on a dispute with fiscal authorities, use a special argument. It lies in the fact that it is impossible to simultaneously recognize a transaction as real in order to calculate the amount of deductions for profit, and at the same time unreal in order to refuse a VAT deduction. Arb made this conclusion. Central district. The decisions of this authority generally stand out from general judicial practice.

The judges justify their decisions with the following argument: if the inspectors recognized the transaction as legal and saved the organization’s expenses, then they cannot deduct VAT from it. Indeed, regarding the same operations, inspectors should not make mutually exclusive conclusions.

Facts of the case

The seller assured the buyer of his good faith, namely:

- in paying taxes and submitting reports;

- in accounting and preparation of “primary” documents;

- possession of the object of the transaction by right of ownership.

In addition, he promised the buyer the following:

- include the VAT paid by the buyer in tax reporting;

- provide all the necessary primary documents - invoices, delivery note, acceptance certificate and others.

In confirmation of his serious intentions, the seller promised, and this is enshrined in the contract, to provide documents that would confirm the guarantees given to him within 5 working days after receiving the corresponding request . In addition, he voluntarily accepted the obligation to compensate the buyer for losses that he incurs due to the seller’s violation of tax laws and/or his representations. In accordance with the agreement, the seller agreed to reimburse, among other things, additional VAT, penalties and fines imposed by the tax authorities on the buyer due to the actions of the seller.

When checking the legality of deducting VAT from this transaction from the buyer, the tax authorities examined transactions between the seller and his counterparties. They came to the conclusion that some of them were fictitious, that is, the products were not actually supplied, the transactions were carried out only “on paper” in order to obtain an unjustified tax benefit. As a result, the buyer was denied a VAT deduction for an amount exceeding 12 million rubles .

Having received such a decision from the Federal Tax Service, the buyer went to court. Moreover, he filed the claim not against the tax authorities, but directly against the seller himself. His claims were based on the establishments given by the seller on the basis of Article 431.2 of the Civil Code of the Russian Federation.

Conditions for tax refund

By choosing a transaction executor, the taxpayer takes on negative risks that may appear in the future when recovering VAT.

The Tax Code of the Russian Federation does not allow the use of incorrectly drawn up payment documents to confirm deductions (clause 2 of Article 169 of the Tax Code of the Russian Federation). Also, the Presidium of the Supreme Arbitration Court of the Russian Federation, in Resolution No. 9299/08 of November 11, 2008, noted that if an invoice is issued by a person who is not on the staff of the organization, then such a document is considered unreliable and should not be accepted as a justification for reducing the tax burden.

In the situation under consideration, the seller’s financial documents were signed by a person who does not have an employment relationship with Egida LLC, and therefore were considered unreliable. The plaintiff did not take any steps to verify the supporting documents for the transaction, that is, he acted imprudently.

In addition, the plaintiff did not present to the court any evidence of payment for the goods received and the fact of its delivery. This indicated the formality of the relationship between the parties, that is, both companies did not intend to create legal consequences as a result of the conclusion of the contract. This was also stated in the Plenum of the Supreme Arbitration Court of the Russian Federation dated October 12, 2021 No. 53.

Thus, the plaintiff did not exercise the right to confirm the legality of the reduction in the tax base with appropriate evidence, and also did not take care of the reliability of the transaction partner. This made it impossible to obtain a tax deduction. The risks of choosing an unreliable seller fall solely on the buyer. He must act with care and caution to demonstrate his good faith in the transaction. Before concluding any agreement, the parties must verify the legality of its conclusion by the person specified in the agreement. You should request the constituent documents and documents granting the right to sign the agreement, and also inquire about the financial viability of the counterparty. The plaintiff was unable to explain to the court the reasons for purchasing goods from Egida LLC and not from other organizations.

The court indicated that the Tax Code of the Russian Federation does not oblige the taxpayer to provide documents confirming payment for goods in order to receive a tax deduction. However, the unreliability of financial securities, combined with other circumstances, led to the conclusion that there was a non-commodity scheme between the parties to the transaction, the purpose of which was to obtain a tax benefit.

The legality of the decision was confirmed by the court.

Court decisions

The arbitrators found the Federal Tax Service's arguments about the fictitiousness of the transaction between the seller and its counterparty convincing. The seller could not prove that the transactions were real in nature, and also that he himself was responsible for failure to provide a tax deduction to the buyer. Given these circumstances, the courts concluded that the seller had unlawfully given the buyer an assurance of his good faith. In this case, the fact whether the buyer appealed the decision of the tax authority or not does not play any role .

As a result, the courts of all instances recognized that since the seller voluntarily gave assurances about the circumstances and knew that the buyer would rely on them, the latter rightfully demands compensation for losses in the form of VAT, the deduction of which was refused.

Non-payment of tax by the seller

Finally, the third part of the clarifications of the RF Supreme Court concerns the refusal to deduct input VAT due to the fact that the seller did not transfer the tax amount to the budget. Here the judges came up with a clear rule: in such a situation, it is possible to “remove” deductions from the buyer who actually received the goods (work or service) only if it is proven that he knew or should have known about the seller’s dishonest behavior.

The fact that the buyer should be aware of violations committed by the counterparty is confirmed, first of all, by the fact of their interdependence or affiliation (for more information, see “Tax risks: is it possible to conclude transactions between “friends”).

Carry out automatic reconciliation of invoices with counterparties Connect to the service

If the specified connection between the parties to the transaction is absent, then the results of the verification of the counterparty, carried out taking into account the above recommendations of the Armed Forces of the Russian Federation, should be taken into account. In other words, it is assessed how reasonably and conscientiously the buyer acted when concluding a specific contract (taking into account the regularity and price of the transaction, the specifics of the product, etc.). And during such an inspection, could he, in principle, establish facts of illegal behavior of the seller: nominal (i.e., the absence of real activity of the seller, in connection with which the contract will actually be fulfilled by another person), distortion of reporting, withdrawal of money using fictitious documents or cashing out, transfer funds to low-tax foreign jurisdictions, etc.

conclusions

So, the case A53-228582016 discussed above and the related Resolution of the Administrative Court of the North Caucasus District dated 06/05/2017 can be called a precedent, since in it the shortfall in VAT amounts was recognized for the first time as losses subject to compensation by the second party to the transaction. To take advantage of this in practice, experts recommend including in the contract provisions for assurance of the circumstances given in terms of taxes and fees . This makes it possible to receive compensation from the counterparty, and in a simplified manner:

- without challenging the decision of the Federal Tax Service in court, unless this is specifically provided for in the contract;

- without the need to establish the fact of the loss and its size (it will be indicated in the decision of the Federal Tax Service - additional assessment of taxes, fines, penalties);

- without the need to prove the guilt of the counterparty (the applicant is based on the assurances given to him that turned out to be unreliable).

When including provisions on assurance of circumstances in the contract, the following must be specified:

- the circumstances for which the assurance is given are significant for the second party to the transaction when concluding and executing the contract;

- the party that gave them understands that the counterparty will rely on them for its financial and economic activities;

In addition, as sanctions for the unreliability of these assurances, it is worthwhile to provide not a penalty, but rather compensation for losses. And then there is a chance to recover the VAT that was not accepted for deduction, along with penalties and a fine, from the other party to the transaction, who gave unfounded assurances.