Accounting services in Moscow are very common and in demand. Accounting services for companies is the transfer of responsibility for accounting and interaction with the tax service and social funds to a professional third-party organization. Such a company is an accounting company. We provide services for submitting personalized records, submitting all types of reports and maintaining internal documentation.

In order to provide quality services, our specialists:

- Receive additional training

- Monitoring changes in the legislation of the Russian Federation

- React promptly to new regulations

Every new year brings changes that we need to be aware of. Quite a lot of new regulations have been issued recently.

What are fixed individual contributions

Fixed contributions are payments made by individual entrepreneurs “for themselves.” A fixed payment is established annually and is mandatory for all registered individual entrepreneurs.

In 2021, the mandatory payment consists of two parts - the first, which is paid mandatory (contributions to pension insurance (26%) and health insurance (5.1%) from the current minimum wage for each month of the year), the second - upon receipt of income in amount over 300 thousand rubles.

In 2021, the amount of fixed contributions for individual entrepreneurs is RUB 27,990.

And from income exceeding 300,000 rubles. per year, in addition to the fixed payment, the individual entrepreneur pays an additional contribution of 1%.

The income taken into account in the calculation is determined:

- for OSNO, all income of an individual entrepreneur received by him both in cash and in kind, as well as income in the form of material benefits, taking into account professional deductions, are taken into account. In this case, you can reduce income for expenses, i.e. for the calculation, the same base is taken as for calculating personal income tax;

- for the simplified tax system, income is taken into account in accordance with Art. 346.15 Tax Code of the Russian Federation. The ability to reduce income for expenses is not provided, but the courts think otherwise;

- for UTII, the object of taxation is the taxpayer’s imputed income (Article 346.29 of the Tax Code of the Russian Federation);

- for PSN, the object of taxation is the potential income of an individual entrepreneur for the corresponding type of business activity from which the patent is calculated (Article 346.47 of the Tax Code of the Russian Federation);

- For insurance premium payers applying more than one tax regime, insurance premiums are calculated based on the total amount of taxable income received from all types of activities.

Calculation for simplified taxation system Income minus Expenses

In this mode, contributions can only be taken into account as part of other expenses, i.e. The calculated advance payment itself cannot be reduced. Let’s figure out how to calculate an advance payment under the simplified tax system with the tax object “income reduced by the amount of expenses.”

For example, let’s take the same entrepreneur without employees, but now we will indicate the expenses incurred by him in the process of activity. Contributions are already included in general expenses, so we will not list them separately.

| Month | Income per month | Reporting (tax) period | Income for the period on an accrual basis | Cumulative expenses for the period |

| January | 75 110 | First quarter | 168 260 | 108 500 |

| February | 69 870 | |||

| March | 23 280 | |||

| April | 117 200 | Half year | 325 860 | 226 300 |

| May | 14 000 | |||

| June | 26 400 | |||

| July | 220 450 | Nine month | 657 010 | 497 650 |

| August | 17 000 | |||

| September | 93 700 | |||

| October | 119 230 | Calendar year | 854 420 | 683 800 |

| November | 65 400 | |||

| December | 12 780 |

The standard rate for the simplified tax system Income minus Expenses for 2021 is 15%, let’s take it for calculation.

- For the first quarter: (168,260 – 108,500) * 15% = 8,964 rubles. Payment must be made no later than April 25th.

- For half a year: (325,860 – 276,300) * 15% = 14,934 rubles. We subtract the advance payment paid for the first quarter (14,934 - 8,964), we find that 5,970 rubles will remain to be paid no later than July 25th.

- For nine months, the calculated tax will be (657,010 – 497,650) * 15% = 23,904 rubles. We reduce by advances for the first quarter and half of the year: 23,904 – 8,964 – 5,970 = 8,970 rubles. They must be transferred to the budget before October 25th.

- At the end of the year, we calculate how much more needs to be paid before April 30: (854,420 * 683,800) * 15% = 25,593 minus all advances paid 23,904, we get 1,689 rubles.

Now we check whether there is an obligation to pay the minimum tax, i.e. 1% of all income received: 854,420 * 1% = 8,542 rubles. In our case, we paid more into the budget, so everything is in order.

Let's compare whose financial burden was higher:

- at a simplified rate of 6%, the entrepreneur paid 22,570 (tax) plus 28,697 (contributions), a total of 51,267 rubles.

- at the simplified 15% tax rate was 25,593 rubles plus 28,697 (contributions), a total of 54,290 rubles.

We can say that the load in the two modes in our examples turned out to be comparable, but this is because the share of costs is quite high (80%). If the share of expenses turns out to be lower, then the simplified tax system of 15% is less profitable than the simplified tax system of 6%.

Before choosing a tax regime, we recommend that you receive a free consultation from 1C:BO, where they will help you choose the best option for you.

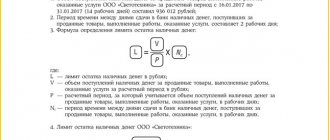

Deadline for payment of fixed contributions IP-2017

For 2021, a fixed payment of 27,990 rubles. must be paid by the end of the year. That is, for 2021 - no later than January 9, 2021 (because December 31, 2021 is a day off). You can pay in installments throughout the year or in one lump sum. For those who pay taxes quarterly, it is often more profitable to pay contributions every quarter to reduce taxes

Deadline for paying an additional contribution for yourself on income over 300 thousand rubles. for the year - no later than July 1 of the year following the reporting year. For 2021 - no later than July 2, 2021 (because July 2 is a day off).

Advance payment under the simplified tax system: deadlines missed, what to do?

Of course, it is highly undesirable to miss the deadline for making an advance payment. However, if this happens, you should not despair. It is necessary to do this as quickly as possible, since subsequent sanctions depend on how strong the debt is.

What kind of sanctions are these? According to the Tax Code, penalties will be charged on the amount that had to be paid for each overdue day, amounting to one three hundredth of the refinancing rate of the Bank of Russia. The fewer days that pass after the deadline for paying the advance payment, the less the penalty will be. Thus, we recommend that you pay them immediately after detecting a delay.

Fixed contributions IP-2018

In 2021, fixed contributions of individual entrepreneurs will be “unlinked” from the minimum wage . The amount of the fixed part of contributions will be established annually by government decree. The annual amount of contributions must provide the entrepreneur with at least 1 point of the individual pension coefficient.

For 2021, the fixed part of insurance pension contributions will be established by law itself and will amount to 26,545 rubles. per year (i.e. calculated based on the amount of 8,508 rubles per month), you will have to pay 5,840 rubles for health insurance.

That is, 2018 individual entrepreneurs will be paid 32,385 rubles. This is 4395 rubles. more than in 2021.

No changes are provided for contributions in the form of 1% on income over 300 thousand rubles.

How to fill out a payment form for individual entrepreneurs to pay contributions

We have provided instructions for filling out payment slips for contributions for individual entrepreneurs.

Our invented entrepreneur Apollo Buevy decided to pay the insurance premiums himself, without turning to an accountant for help. I went to the Federal Tax Service website, started filling out receipts and got confused in the KBK. We decided to help him and other individual entrepreneurs and compiled step-by-step instructions for filling out payment documents.

See detailed instructions.

KBK for payment documents

KBK is a budget classification code that is indicated on receipts or bank documents for tax payment. The BCC of advance payments for the simplified system is the same as for the single tax itself. In 2021, the budget classification codes approved by Order of the Ministry of Finance of Russia dated July 1, 2013 N 65n (as amended on June 20, 2016) continue to apply. You can always verify their relevance on the Federal Tax Service website.

If you indicate an incorrect BCC, the tax will be considered paid, because Article 45 of the Tax Code of the Russian Federation indicates only two significant errors in the payment document:

- incorrect name of the recipient's bank;

- incorrect Federal Treasury account.

However, paying using the wrong classification code will result in an incorrect distribution of the amounts paid, which will result in you being in arrears. In the future, you will have to search for the payment and communicate with the Federal Tax Service, so be careful when filling out the details.

- KBK simplified tax system 6% (tax, arrears and debt) - 182 1 05 01011 01 1000 110;

- BCC simplified tax system 15% (tax, arrears and debt, as well as the minimum tax, starting from January 1, 2021) - 182 1 05 01021 01 1000 110.

IP pensioners

The Ministry of Finance, in its letter No. 03-15-09/9884 dated February 21, 2017, criticized the proposal to exempt entrepreneurs of retirement age from fixed contributions.

As noted by the Ministry of Finance, this could lead to abuses in the re-registration of business activities for pensioners, which, on the one hand, will negatively affect the collection of insurance premiums and the balance of the budget system of the Russian Federation, and on the other hand, will lead to the loss of a targeted approach when providing such a preference.

Officials recalled that individual entrepreneurs pay insurance premiums regardless of age and type of activity.

We also have important material about fixed contributions of individual entrepreneurs in simplified form.

What is meant by simplified tax system?

A simplified taxation system is a type of special taxation regime, which is the replacement of several taxes for legal entities and individual entrepreneurs with one. First of all, this is necessary so that tax subjects do not find it difficult to prepare reports. However, not everyone has this option. So, for example, one of the conditions for applying the simplified tax system is no more than 100 people as the average number of employees, the absence of branches, etc.

USN and separate division 2016

It is extremely important to submit an application on time to switch to this tax regime. For a legal entity that has just been created, this must be done no later than the thirtieth day of tax registration. If an organization or entrepreneur wants to switch from another tax system to the simplified tax system, the period depends on the type of this regime.

Federal Tax Service vs Pension Fund: after submitting the declaration, the maximum contributions of individual entrepreneurs must be recalculated

As mentioned above, individual entrepreneurs were required to pay fixed contributions in the amount of 1% on income over 300 thousand rubles. To calculate these contributions, data on the income of entrepreneurs was transferred by tax authorities to the Pension Fund.

If the individual entrepreneur did not submit reports and, accordingly, there was no data on income, his contributions are calculated to the maximum, based on 8 minimum wages.

But if the reporting is ultimately submitted to the Federal Tax Service (regardless of the date of its submission), the amount of the insurance premium for compulsory health insurance is determined in accordance with the provisions of Part 1.1 of Article 14 of Federal Law N 212-FZ based on the amount of annual income indicated in such reporting. And if the Pension Fund has collected insurance premiums from the payer based on 8 minimum wages, a recalculation must be made.

But the Pension Fund is against it. And in July 2021, mass refusals began. The Pension Fund issued a sensational letter dated July 10, 2017 No. NP-30-26/9994, in which “pensioners” refused to recalculate the fixed contributions of individual entrepreneurs who submitted their declarations late.

This information shocked many individual entrepreneurs, who began to apply en masse to the Federal Tax Service. The tax authorities stood up for the individual entrepreneur and in their letter No. BS-4-11/ [email protected] dated September 1, 2017, they reported that the Pension Fund of the Russian Federation was wrong and the law does not contain restrictions on recalculation.

When the tax authorities recognize debts as bad

Entrepreneurs pay taxes and insurance premiums within the deadlines prescribed in the Tax Code. For example, tax under the simplified tax system for 2020 must be paid by April 30, 2021.

If an individual entrepreneur does not pay on time, he has a debt with interest and a fine, and the tax office has the right to forcefully receive what is due.

In an ideal world for tax officials, individual entrepreneurs have money on bank cards or cars in the garage that can be taken away to pay off the debt. Usually the tax office does this, or at least tries.

But there are a number of cases when the tax office loses the right to forcibly withdraw its money. Then she is obliged to recognize the debt, penalties and fines as hopeless, write them off and remove them from the taxpayer’s personal account.

The tax authority is obliged to recognize debts as bad in cases from Art. 59 Tax Code of the Russian Federation:

— The entrepreneur went bankrupt. As an individual entrepreneur or as an individual, it doesn’t matter. The main thing is that there was not enough money to fully repay the tax debt.

— The entrepreneur died. Debts on insurance premiums, simplified tax system, UTII and patents will be written off automatically. Land tax, personal income tax and trade tax will be written off if there are more of them than the entire inheritance of the entrepreneur is worth.

— The tax inspectorate missed the deadlines for blocking an account or receiving a writ of execution — and they are quite short. The delay was confirmed by the court. We will discuss below what an entrepreneur can do to speed up write-off.

— The bailiffs searched for the entrepreneur’s liquid property for more than five years, but did not find it. The debt to the tax office is less than 300,000 rubles, and it is impossible to bankrupt an individual entrepreneur with such an amount.

— The entrepreneur tried to go bankrupt. But the arbitration court closed the case because the entrepreneur did not have the money to pay the bankruptcy trustee.

— The bank wrote off the debt from his account, but did not have time to transfer it to the tax office because it was liquidated. Although the tax office did not receive the money, the entrepreneur’s obligation is removed.

❗ Just an old debt that has been hanging on an entrepreneur for several years, the tax office is not obliged to recognize as hopeless and forgive. It is useless to wait the mythical three years. A debt that the tax office has collected without violations does not have a statute of limitations.

However, sometimes the state arranges tax amnesties - it writes off debts at once. Typically, the amnesty applies to taxes that have become clear that they were beyond the means of the common man. Therefore, the state writes them off as hopeless. For individual entrepreneurs this was the case - we will say more below.

The tax office deals with each debtor in order from the Order of the Federal Tax Service No. ММВ-7-8/ [email protected]

First of all, the debtor brings to the tax office at his place of residence a document that confirms his right to write off the debt:

- a copy of the arbitration court ruling on the completion of bankruptcy proceedings or on the sale of a citizen’s property - for bankrupts;

- copies of the death certificate, heirs’ passports, certificate of inheritance and assessment of the value of the inheritance - if the heirs are dealing with the debts;

- a copy of the court decision, which states that the tax office has lost the right to collect arrears due to missed deadlines;

- a copy of the resolution on the completion of enforcement proceedings - if the bailiffs did not find the property;

- a copy of the court ruling on the return of the bankruptcy application - if the individual entrepreneur did not find the money for the procedure;

— an extract from the Unified State Register of Legal Entities on the liquidation of the bank.

In the next five days, the tax office issues a certificate of impossibility of collection. And on the next working day he makes a decision recognizing the debt as hopeless.

A debt can only be considered bad until it is repaid. If the tax office managed to withdraw money from the account, and then the reasons for the write-off became clear, the money cannot be returned. This is what the Supreme Arbitration Court said in paragraph 9 of Resolution No. 57.