The type of financial statements prepared depends on the purpose and time range. The essence of reporting documents is a comprehensive reflection of the company’s current property status, financial successes or problems. The obligations to prepare and submit reports to regulatory authorities are regulated by law; enterprises are not authorized to independently decide for what period to fill out reporting forms, where and when to submit them. Based on the data systematized in the reports, it is possible to diagnose threats to financial stability and identify reserves for increasing profitability.

What is the procedure for preparing consolidated statements ?

Interim financial statements 2021

From May 7, 2021, the preparation of interim reporting officially ceased to be mandatory for all organizations on the basis of Order of the Ministry of Finance dated April 11, 2018 No. 74n. The order canceled clause 29 of the Regulations on Accounting and Reporting, which required the preparation of interim reporting by everyone who is not exempt from it by law. Similarly, the decision of the Supreme Court of the Russian Federation canceled paragraph 48 of PBU 4/99. Currently, it is necessary to prepare and submit interim reporting only in cases where this obligation is provided for:

- legislation;

- regulatory legal acts;

- contracts;

- constituent documents or decisions of owners.

For example, quarterly reporting is required for insurance organizations and securities issuers. If your organization does not fall under these conditions, it is obligatory to prepare only annual reports, but it is possible and useful to prepare interim reports on your own initiative.

Submission of interim reporting to tax authorities and statistical authorities is not required. But interim reporting may be needed when concluding agreements with counterparties, obtaining a bank loan or the requirements of the founder. In addition, interim reporting helps to monitor the situation, forecast financial results and verify the reliability of accounting data.

What are consolidated financial statements

Consolidated reporting is a set of reporting documentation reflecting the activities of several interconnected organizations. Its preparation is typical for large companies with subsidiaries. The data is compiled in reporting forms on an annual basis. The documentation signed by the management of the parent company must be submitted to the tax authority.

Consolidated reporting is of a collective nature. It summarizes information from the parent structure and all branches and subsidiaries. The accounting department of the head office systematizes data from documents for all departments, summarizes the values of identical indicators and enters the final figures into a summary report.

How to disclose consolidated financial statements ?

A consolidated type of reporting documentation is necessary in a situation where:

- the organization is the parent of another structure, has a significant number of shares in the joint-stock company, which give it voting rights;

- the parent structure has the opportunity to influence decisions made by related firms.

NOTE! The criteria for the interconnectedness of organizations are the presence of a unified system for controlling the movement of assets, the existence of dependence of one structure on the decisions and actions of the parent enterprise, without whose approval it is impossible to carry out a number of operations.

Interim reporting period and submission deadlines

Interim reporting reflects all aspects of the organization's activities and includes summary data on the organization's property and finances and their current state. It is formed on a cumulative basis for a reporting period of less than a year, starting from January 1.

The reporting period is not established by law. Experts believe that the optimal period for interim reporting is a quarter. Monthly formation is too labor-intensive, and six months is a long period, and the information may not be timely. But when determining the period, be guided by the needs of owners, management and potential investors.

Interim reporting must be generated no later than 30 days after the end of the reporting period. The deadlines for submitting reports at the end of the reporting period are determined by the owners independently; they depend on the goals of the company. The decision on the reporting period and filing deadlines should be reflected in the accounting policy.

Menu

Article by lawyer of AKG Gorislavtsev and K. Chistyakova E.V. financial newspaper.

The rules currently in force establish the obligation to include in the financial statements information about events after the reporting date that occurred before the date of signing the statements. In practice, a situation is possible when, in the period between the dates of signing the financial statements and their approval, additional information about events after the reporting date will be received or new significant events will be identified (happened). In this case, the organization must somehow provide this information in writing to the persons to whom the financial statements have already been transferred.

Let's consider this situation in more detail.

According to clause 4 of the accounting regulations “Events after the reporting date” PBU 7/98, approved by order of the Ministry of Finance of Russia dated November 25, 1998 No. 56n, the date of signing of the financial statements is considered to be the date specified in the statements submitted to the addresses determined by the legislation of the Russian Federation, financial statements when signed in the prescribed manner.

In accordance with clause 2 of article 15 of the Federal Law dated November 21, 1996 No. 129-FZ, as well as clause 86 of the Regulations on accounting and financial reporting in the Russian Federation, approved by order of the Ministry of Finance of Russia dated July 29, 1998 No. 34n (hereinafter referred to as Order No. 34n), organizations are required to submit annual financial statements within 90 days after the end of the year, unless otherwise provided by the legislation of the Russian Federation. The submitted annual financial statements must be approved in the manner established by the constituent documents of the organization.

In accordance with paragraph 86 of Order No. 34n, within the specified time frame, the specific date for the submission of financial statements is established by the founders (participants) of the organization or the general meeting. In this case, annual financial statements must be submitted no earlier than 60 days after the end of the reporting year.

Based on clause 11 of Art. 48 of the Federal Law of December 26, 1995. No. 208-FZ “On Joint-Stock Companies” (hereinafter referred to as Law No. 208-FZ) approval of annual reports, annual financial statements, including profit and loss statements (profit and loss accounts) of the company, as well as distribution of profits (including including the payment (declaration) of dividends, with the exception of profits distributed as dividends based on the results of the first quarter, half a year, nine months of the financial year) and losses of the company based on the results of the financial year, falls within the competence of the general meeting of shareholders.

According to paragraph 2 of Art. 11 of Law No. 208-FZ, the company’s charter must contain information about the structure and competence of the company’s management bodies and the procedure for their decision-making.

Based on paragraph 1 of Art. 47 of Law No. 208-FZ, the annual general meeting of shareholders is held within the time limits established by the company’s charter, but no earlier than two months and no later than six months after the end of the financial year, i.e. from March 1 to June 30 after the end of the year.

Thus, since the procedure and deadlines for approval and submission of financial statements are established in the constituent documents of the company, then if there is a conflict with the provisions of clause 2 of Art. 15 of Law No. 129-FZ and paragraph 1 of Art. 47 of Law No. 208-FZ, the date of signing of the annual financial statements often does not coincide with the date of its approval.

In accordance with paragraph 3 of PBU 7/98, an event after the reporting date is recognized as a fact of economic activity that has had or may have an impact on the financial condition, cash flow or results of operations of the organization and which occurred in the period between the reporting date and the date of signing the financial statements for the reporting year. Clause 1 of the appendix to PBU 7/98 provides an approximate list of events confirming the economic conditions that existed at the reporting date in which the organization conducted its activities, among which is the discovery after the reporting date of a significant error in accounting or a violation of the law in the conduct of the organization’s activities, which lead to distortion of financial statements for the reporting period.

According to clause 11 of Order No. 67n of the Ministry of Finance of Russia dated July 22, 2003 “On Forms of Accounting Reports,” in cases of incorrect reflection of business transactions of the current period before the end of the reporting year, corrections are made by entries in the corresponding accounting accounts in the month of the reporting period when the distortions identified. If an incorrect reflection of business transactions is detected in the reporting year after its completion, but for which the annual financial statements have not been approved in the prescribed manner, corrections are made by entries in December of the year for which the annual financial statements are prepared for approval and submission to the appropriate addresses.

In cases where an organization reveals in the current reporting period that business transactions were incorrectly reflected in the accounting accounts last year, corrections are not made to the accounting records and financial statements for the previous reporting year (after the annual financial statements have been approved in the prescribed manner). There are gaps in the regulations of civil legislation regulating the accounting procedures and in the regulations regulating the activities of joint stock companies. Therefore, on the basis of Art. 6 of the Civil Code of the Russian Federation in cases where relations regulated by civil legislation are not directly regulated by legislation or agreement of the parties and there is no business practice applicable to them, to such relations, if this does not contradict their essence, civil legislation regulating similar relations is applied (analogy of the law ).

If it is impossible to use an analogy of law, the rights and obligations of the parties are determined based on the general principles and meaning of civil legislation (analogy of law) and the requirements of good faith, reasonableness and fairness. Since the accounting legislation does not contain a direct prohibition on the presentation by an organization of amended financial statements, which have already been submitted to the tax authority, but have not yet been approved at the annual general meeting of shareholders, then, guided by the general principle of civil law - what is not prohibited by law is permitted, it is possible , in the author’s opinion, to allow the replacement of the accounting statements submitted to the tax authority with corrected ones.

An additional argument in favor of the possibility of replacing the financial statements with an amended one is clause 12 of PBU 7/98, which establishes the organization’s obligation to inform the persons to whom these financial statements were presented if, in the period between the date of signing the financial statements and the date of their approval in the prescribed manner, new information has been received about events after the reporting date disclosed in the financial statements presented to users, and (or) events have occurred (identified) that may have a material impact on the financial condition, cash flows or results of operations of the organization.

It is worth paying attention to the fact that in November 2008, a draft of a new PBU “Correcting Errors in Accounting and Reporting” (PBU 22/2009) was posted on the official website of the Ministry of Finance of Russia.

The draft PBU 22/2009 notes that absolutely any identified error, not just a significant one, must be corrected. The procedure for correcting an error depends on the moment in time when it was identified and its significance.

For example, clause 8 of draft PBU 22/2009 considers the case of interest to us:

- a significant error of the previous reporting year, identified after the date of signing the financial statements for this year, but before the date of submission of such statements to shareholders of the joint-stock company, participants of the limited liability company, state or municipal body authorized to perform the functions of the owner, etc., is corrected in the procedure established by clause 6 of PBU 22/2009.

Paragraph 6 of PBU 22/2009 establishes that the error is corrected by making entries in the relevant accounting accounts for December of the reporting year for which the annual financial statements are prepared.

As for the actions of the auditor in the event of detection of events after the reporting date, Audit Rule (standard) M 10 “Events after the reporting date”, approved by Decree of the Government of the Russian Federation dated September 23, 2002 No. 696, establishes the rights, obligations and procedure for the actions of the auditor when detection of events after the reporting date (clauses 2, 3, 5. 7. 10, II, 14, 15, 16):

- the auditor should take into account the effect on the financial statements and the auditor's report of favorable and unfavorable events after the reporting date;

- the financial statements must reflect favorable and unfavorable events that confirm the economic conditions that existed at the reporting date or the economic conditions that arose after the reporting date in which the audited entity conducted its activities;

- procedures designed to identify events that may require adjustments to or disclosures in the financial statements are performed as close as practicable to the date the auditor's report is issued;

- If the auditor becomes aware of events that have a material effect on the financial statements of the entity being audited, the auditor should determine whether these events are properly reflected in the accounting records and whether they are adequately disclosed in the financial statements;

- When the management of the audited entity makes changes to the financial statements, the auditor should carry out the necessary procedures and provide management with a new audit report on the amended financial statements:

- If management of the entity being audited does not make changes to the financial statements when the auditor believes that they should be made, and the auditor's report has not yet been provided to the entity being audited, the auditor should express a qualified or adverse opinion in the auditor's report;

- If, after making the financial statements available to users, the auditor becomes aware of an event or fact that existed at the date of the auditor's report that, if such a fact had been known at that time, would have required the auditor to modify the auditor's report, the auditor should take action appropriate in the circumstances;

- If the management of the audited entity revises the financial (accounting) statements, the auditor should perform the necessary audit procedures, check the actions taken by the management of the audited entity to inform everyone who received the previously submitted financial statements along with the auditor's opinion on them about the current situation, and provide a new opinion on the revised financial (accounting) statements;

- The new auditor's report should include a disclaimer and a note to the financial statements detailing the basis for the revision of the previously presented financial statements and auditor's report. Thus, based on the above, neither the accounting legislation nor the legislation on joint stock companies contain a direct prohibition on replacing financial statements already presented to users in the period after they are signed, but until they are approved at the general meeting of shareholders. Moreover. The audit rule (standard No. 10 “Events after the reporting date” determines the procedure for the auditor to act in such a situation, and the draft PBU 22/2009 establishes the procedure for correcting and replacing financial statements presented to users.

Composition of accounting records for a period of less than a year

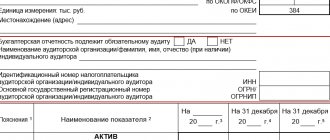

Unlike annual reporting, interim reporting includes fewer forms. It is mandatory to prepare an interim balance sheet and a financial performance report. It also includes explanations if without them it is impossible to form a complete picture of the financial position of the organization and the financial results of its activities. If required by federal or industry accounting standards, founders or owners supplement interim reporting with a cash flow statement, explanatory notes and other forms.

The balance sheet contains information about the financial condition of the organization as of the current date. Assets provide information about property and liabilities to the organization. Liabilities reflect own and borrowed funds, allowing you to form an idea of the sources of property formation and the financial stability of the company.

The financial results report gives an idea of the organization's profits and losses for the period, allows you to assess the structure and dynamics of profits and identify problem areas and prospects.

Interim reporting forms are not approved by law; an organization can develop them itself, based on annual reporting forms. The reporting forms and its composition must be reflected in the accounting policies.

Purpose and composition of consolidated reporting

Consolidated reporting may be produced more frequently than once a year if required by internal users. The reason for preparing interim reporting documents may be the desire of investors to analyze the results of the company’s financial activities and see its development prospects. The decision to fill out a report not for a year, but for a shorter interval, may be based on the order of management. This is possible in situations where the issue of changing the tactical or strategic development program of an enterprise is being considered.

How is the accounting policy formed by an organization that discloses consolidated financial statements prepared in accordance with IFRS or the financial statements of an organization that does not create a group?

IMPORTANT! Summary reporting data cannot be used to derive the tax base and analyze the effectiveness of the tax security system.

For tax purposes, data from consolidated reports cannot be used for a number of reasons:

- the values of the indicators are presented in a generalized form, which does not allow identifying the objective size of the tax base and can lead to its underestimation;

- the actual location of subsidiaries does not always coincide with the place of registration of the parent organization;

- applicable regional tax rates in organizations within the group may vary;

- a combination of companies is not sustainable in the long term.

Consolidated financial statements consist of standard reporting forms that contain generalized arithmetic indicators. The set of reporting documentation includes a balance sheet, a statement of financial results and additional forms with explanations.

Preparation of interim reporting

Like annual reporting, interim reporting must meet the requirements of reliability, timeliness, verifiability, integrity, simplicity and relevance. Preparation of interim reporting has its own characteristics.

- In the interim reporting there is no balance sheet reformation - write-off of profit or loss received for the previous financial year. At the end of a quarter or half a year, profit (loss) remains in account 99 and must be written off to account 84 only at the end of the reporting year.

- When preparing interim reporting, inventory is not required.

- Income tax is calculated using the tax rate that will be applied to annual earnings.

- Planned but not incurred expenses do not need to be recognized, just like income not received. As in the annual accounts, they should only be recognized when the recognition criteria are met.

- Assets are valued without the involvement of appraisers by extrapolation of data or independent calculation by the financial department of the organization.

- In interim reporting, employee bonuses can only be recognized early if, at the reporting date, the amount of the payment can be reliably measured or if the company has a legal obligation to pay that cannot be avoided.

Preparing for interim reporting

The preparation of interim reporting includes several stages. First of all, you should prepare for its preparation. At the preparation stage, summarize all available data from primary and other documents, study the rules for drawing up forms and prepare the necessary data.

Interim reporting is prepared according to the same rules as annual reporting. It must be compiled in Russian, reflect numerical data in thousands of rubles or millions, negative indicators must be indicated in parentheses. Completed reports must be signed by the manager.

When compiling, the following data is required: full name of the documents, name of the organization, meters used, positions of persons responsible for accounting and reporting, and their personal signatures.

Complete accounting transactions at the end of the reporting period, check all entries in the accounting accounts and correct any errors found. Close accounts for cost accounting and formation of product costs on an accrual basis from the beginning of the year. Also, the preparation stage includes tax calculation.