Income tax in NPOs

NPOs, like any legal entity on OSNO, pay income tax. However, often a significant portion of NPO income (and sometimes all income) is exempt from this tax.

In accordance with paragraphs. 14 clause 1 art. 251 of the Tax Code of the Russian Federation, grants and other targeted income for conducting the main activities of NPOs are not subject to income tax.

It is necessary to submit a profit declaration even if the organization does not have a taxable base. In any case, the NPO must fill out sheet 07 of the report with information on the use of targeted proceeds.

But NPOs may also have income from “related” commercial activities, which are subject to taxation. In order to correctly calculate the taxable base, an organization must keep separate records of income and expenses.

There are usually no special problems with income. Earmarks, grants, and business revenue typically come from a variety of sources.

But it is important that those who transfer non-taxable income correctly write the purpose of the payment: “targeted financing”, “grant”, etc. With any wording that allows for double interpretation, such as “payment for...”, tax authorities will include this amount in the taxable base.

The situation with expenses is more complicated. You need to try to separate them as much as possible according to directions already during formation. It is better to carry out purchases for commercial and non-commercial needs using separate documents.

If the costs relate to both types of activities, then they should be divided in proportion to revenue (clause 1 of Article 272 of the Tax Code of the Russian Federation).

If the fixed assets of a non-profit organization are acquired at the expense of targeted revenues and are used for non-commercial activities, then depreciation is not charged on them (clause 2, clause 2, article 256 of the Tax Code of the Russian Federation).

If an object was purchased using funds from business activities and is used for commercial purposes, then it is subject to depreciation for calculating income tax (letter of the Ministry of Finance of the Russian Federation dated January 22, 2019 No. 07-01-09/2891).

General rules for the transition to the simplified tax system

To switch to “simplified”, you need to comply with several mandatory conditions.

- In tax accounting, a company’s income for 9 months should not exceed 112.5 million rubles.

- The average number of employees of the company should not exceed 100 people. You need to count everyone: full-time employees, workers on civil contracts and those who work part-time.

- The residual value of fixed assets should not exceed 150 million rubles in accounting.

- The company must not have branches.

- In the authorized capital of the company, the share of other organizations cannot be more than 25%.

- A company using the simplified tax system cannot be a bank or a budget organization.

If a company fulfills all these conditions, it can safely switch to “simplified”.

VAT in NPOs

A non-profit organization on OSNO pays VAT, like other legal entities.

However, targeted revenues for the main activities of NPOs are not subject to VAT (clause 2 of Article 146 of the Tax Code of the Russian Federation). If for its main activities an NPO uses goods and services purchased from VAT payers, then the tax cannot be deducted. VAT amounts must be included in the purchase price (clause 1, clause 2, article 170 of the Tax Code of the Russian Federation).

A VAT return must be submitted even if all income is not subject to this tax. Information on non-taxable revenue should be reflected in section 7 of the report.

If an NPO also conducts business activities, then it pays VAT on commercial revenues on a general basis. In this case, the “input” tax can be deducted.

In this case, the source of financing is not important. An NPO may purchase materials or services using earmarked funds, but use them for commercial activities. In this case, VAT can be deducted from the purchase (Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated September 4, 2007 No. 3266/07).

If a particular expense cannot be attributed only to taxable or non-taxable activities, then the “input” VAT should be distributed in proportion to the share of taxable revenue in the total amount of receipts for the current quarter (clause 4 of Article 170 of the Tax Code of the Russian Federation).

For certain types of non-commercial organizations, an exemption from VAT is provided for certain transactions (clauses 1.2, clause 3, article 149 of the Tax Code of the Russian Federation):

- Religious organizations do not pay VAT on income from rituals and the sale of religious items, including literature.

- Public organizations of disabled people are exempt from VAT on all revenue, except for excisable goods, minerals and luxury goods (Resolution of the Government of the Russian Federation of November 22, 2000 No. 884). To receive benefits, the number of disabled people in the organization must be at least 80%.

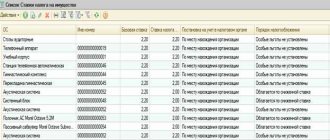

Tax base and procedure for its determination

The tax base is determined by the taxpayer independently as the average annual value of property recognized as an object of taxation, calculated on the basis of its residual value, formed in accordance with the established accounting procedure approved in the accounting policy of the organization. In general, to calculate the tax, you should take the debit balances on account 01 “Fixed assets” and subtract from them the credit balance on account 02 “Depreciation of fixed assets”. In a situation where depreciation is not provided for certain fixed assets, the cost of these objects for tax purposes is determined as the difference between their original cost and the amount of accumulated depreciation. Thus, fixed assets of a non-profit organization acquired at the expense of targeted funds are included in the tax base at their original cost (account balance 01 “Fixed assets”) minus the amount of depreciation accrued on off-balance sheet account 010 “Depreciation of fixed assets.” According to clause 17 of PBU 6/01 for fixed assets of non-profit organizations on an off-balance sheet account, information on the amounts of depreciation accrued in a straight-line manner is compiled in relation to the procedure given in clause 19 of this PBU. For objects put into operation before January 1, 2002, depreciation is calculated based on the Unified norms of depreciation charges, approved by Resolution of the Council of Ministers of the USSR of October 22, 1990 N 1072 “On the unified norms of depreciation charges for the complete restoration of fixed assets of the national economy of the USSR.” For objects put into operation after January 1, 2002, in our opinion, it is advisable to use Decree of the Government of the Russian Federation dated January 1, 2002 N 1 “On the Classification of fixed assets included in depreciation groups,” since this Classification can be used for accounting purposes. Please note that the tax base is determined separately in relation to property: - subject to taxation at the location of the organization; — each separate division of the organization, allocated to a separate balance sheet; - property taxed at different tax rates. If an object of real estate subject to taxation has an actual location in the territories of different constituent entities of the Russian Federation, the tax base for it is determined separately and is accepted when calculating tax in the corresponding constituent entity of the Russian Federation in a part proportional to the share of the book value of the real estate object in the territory of the corresponding constituent entity of the Russian Federation Federation. The principle for calculating the amount of property tax is as follows: the average annual value of the property is multiplied by the tax rate, the maximum amount of which is 2.2%. During the year (at the end of each quarter), organizations make advance payments on property taxes. The amount of advance payment paid for the reporting period is calculated using the following formula:

Average property value for the reporting period x Tax rate: 4.

The average value of property recognized as an object of taxation for the reporting period is determined as the quotient of dividing the amount obtained by adding the residual value of the property on the 1st day of each month of the reporting period and the 1st day of the month following the reporting period by the number of months in the reporting period, increased by one (example 3).

Example 3. Let’s assume that the cost of fixed assets listed on the balance sheet of the non-profit partnership “Ankhinoya” in 2011 was: as of January 1 - 172,000 rubles; as of February 1 - 160,000 rubles; as of March 1 - 148,000 rubles; as of April 1—RUB 520,000. The average value of property recognized as an object of taxation for the first quarter of 2011 is determined as follows: (172,000 rubles + 160,000 rubles + 148,000 rubles + 520,000 rubles): 4 = 250,000 rubles. The amount of the advance payment for property tax of the non-profit partnership "Ankhinoya" for the first quarter of 2011 will be 1375 rubles. (RUB 250,000: 4 x 2.2%).

You should know that the legislative (representative) body of a constituent entity of the Russian Federation, when establishing a property tax, has the right to provide for certain categories of taxpayers the right not to calculate or pay advance tax payments during the tax period. In addition, advance payments are not paid in those regions where the legislative (representative) body of a constituent entity of the Russian Federation has not established reporting periods in accordance with clause 3 of Art. 379 Tax Code of the Russian Federation. When determining the amount of the advance payment at the end of each quarter, advance payments calculated for the previous reporting period are not taken into account. Only at the end of the tax period (calendar year) the amount of tax payable to the budget is determined as the difference between the amount of tax calculated at the end of the tax period and the amounts of advance tax payments calculated during the tax period. The average annual value of property recognized as an object of taxation for the tax period is determined as the quotient of the amount obtained by adding the values of the residual value of the property on the 1st day of each month of the tax period and the last day of the tax period, by the number of months in the tax period, increased by one . In other words, you need to add up the residual value of the property on the first day of each month of the reporting year and on the last day of the year, then divide the resulting amount by the number of months in the year increased by one, i.e. for 13 months (example 4).

Example 4. Let’s assume that the residual value of fixed assets listed on the balance sheet of the Olympus fund and recognized as an object of taxation in 2011 amounted to: as of January 1 - 172,000 rubles; as of February 1 - 160,000 rubles; as of March 1 - 148,000 rubles; as of April 1 - 520,000 rubles; as of May 1 - 572,000 rubles; as of June 1 - 460,000 rubles; as of July 1 - 448,000 rubles; as of August 1 - 372,000 rubles; as of September 1 - 360,000 rubles; as of October 1 - 348,000 rubles; as of November 1 - 302,000 rubles; as of December 1 - 292,000 rubles; as of December 31, 2011 - RUB 248,000. The average cost of property for the first quarter of 2011 is 250,000 rubles. ((172,000 + 160,000 + 148,000 + 520,000) : 4). The amount of the advance payment for property tax for this period amounted to 1,375 rubles. (RUB 250,000: 4 x 2.2%). The average cost of property for the first half of 2011 is 354,286 rubles. ((172,000 + 160,000 + 148,000 + 520,000 + 572,000 + 460,000 + 448,000) : 7). The amount of the advance payment is 1949 rubles. (RUB 354,286: 4 x 2.2%). The average cost of property for nine months of 2011 is 356,000 rubles. ((172,000 + 160,000 + 148,000 + 520,000 + 572,000 + 460,000 + 448,000 + 372,000 + 360,000 + 348,000) : 10). The amount of the advance payment is 1958 rubles. (RUB 356,000: 4 x 2.2%). And finally, the average annual cost of property for 2011 will be 338,615 rubles. ((172 000 + 160 000 + 148 000 + 520 000 + 572 000 + 460 000 + 448 000 + 372 000 + 360 000 + 348 000 + 302 000 + 292 000 + 248 000): 13). The amount of property tax calculated at the end of the year is 7,450 rubles. (RUB 338,615 x 2.2%). The amount of tax payable to the budget at the end of the tax period by the Olympus Foundation will be 2,168 rubles. (7450 - 1375 - 1949 - 1958).

Please note that when calculating the average annual (average) value of property for organizations (or their separate divisions) created or liquidated during the tax (reporting) period, the total number of months in the calendar year, as well as in the corresponding reporting period, must be taken into account. The actual number of months that occurred during the period of activity of the organization or its separate division, which has a separate balance sheet, does not play any role here. A similar procedure for determining the average annual (average) value is applied when removing or placing on the balance sheet of an organization during the tax (reporting) period of property for which the tax base, in accordance with paragraph 1 of Art. 376 of the Tax Code of the Russian Federation, is determined separately. The deadlines for paying advance payments and taxes at the end of the year are determined by the legislative (representative) bodies of the constituent entities of the Russian Federation. In addition, they have the right to establish any tax rate ranging from zero to 2.2%, as well as differentiated (different) tax rates depending on the categories of taxpayers and (or) property recognized as the object of taxation. For example, one tax rate may be applied to buildings, and another to cars; in this case, the average annual value of property should be calculated for each type of property (example 5).

Example 5. The Pluto Association is registered in a constituent entity of the Russian Federation, where regional law provides for differentiated tax rates for different types of property. The tax rate for cars is 2.2%, and for all other fixed assets - 2.0%. Let us assume that the residual value of fixed assets listed on the balance sheet of the association and recognized as an object of taxation in 2011 amounted to: as of January 1 - 172,000 rubles. (including for cars - 72,000 rubles); as of February 1 - 160,000 rubles. (including for cars - 62,000 rubles); as of March 1 - 148,000 rubles. (including for cars - 42,000 rubles); as of April 1—RUB 520,000. (including for cars - 172,000 rubles). The average value of property recognized as an object of taxation for the first quarter of 2011 is determined as follows. First, the average cost of cars is calculated: (72,000 rubles + 62,000 rubles + 42,000 rubles + 172,000 rubles): 4 = 87,000 rubles. Secondly, the average cost of the remaining property is calculated: (172,000 rubles + 160,000 rubles + 148,000 rubles + 520,000 rubles - 72,000 rubles - 62,000 rubles - 42,000 rubles - 172,000 rubles. ): 4 = 163,000 rub. The amount of the advance payment for property tax for the Pluto association for the first quarter of 2011 will be 1294 rubles. ((RUB 87,000 x 2.2% + RUB 163,000 x 2.0%): 4).

A non-profit organization, which includes separate divisions that have a separate balance sheet, pays tax (advance tax payments) to the budget at the location of each of the separate divisions in relation to property recognized as an object of taxation, located on a separate balance sheet of each of them, in an amount determined as the product of the tax rate in force in the territory of the corresponding constituent entity of the Russian Federation on which these separate divisions are located, and the tax base (one fourth of the average value of property) determined for the tax (reporting) period in relation to each separate division. A non-profit organization that takes into account on its balance sheet real estate objects located outside the location of the organization or its separate division that has a separate balance sheet, pays tax (advance tax payments) to the budget at the location of each of the specified real estate objects in an amount determined as the product of the tax rate, in force on the territory of the relevant constituent entity of the Russian Federation on which these real estate objects are located, and the tax base (one fourth of the average value of the property) determined for the tax (reporting) period in relation to each real estate object.

Personal income tax and insurance contributions to non-profit organizations

Any activity, including non-profit, is impossible without employees. NPOs often employ volunteers, but almost always such companies also have full-time salaried specialists.

In general, personal income tax and insurance contributions do not need to be transferred from payments in favor of volunteers (for example, compensation for food, travel expenses, etc.). It is necessary to pay taxes and contributions only on excess payments for meals for volunteers: over 700 rubles per day in the Russian Federation and 2,500 rubles abroad (clause 3.1 of Article 217 and clause 6 of Article 420 of the Tax Code of the Russian Federation).

And from the remuneration of full-time NPO specialists, all established payments must be paid in full. Therefore, the organization must withhold personal income tax from these payments, as well as charge insurance premiums on a general basis.

Features of ANO affecting reporting

The following features of ANO influence the reporting of such companies:

- focus on achieving social goals;

- obtaining material benefits is not a priority;

- activities are regulated by the Civil Code of the Russian Federation, the Tax Code of the Russian Federation and industry legislation;

- there may be associations of individuals;

- the basis of accounting is the targeted revenues of the autonomous non-profit organization, which are necessarily reflected in the reporting;

- submission of reports is established according to deadlines typical for legal entities;

- mandatory content in reporting of information relating to the property of the autonomous non-profit organization, both in monetary and other forms;

- as income, the reporting reflects receipts from participants, voluntary donations, revenue from certain types of work, interest on stocks and bonds, and others;

- to generate reporting, they use data on the balances of property obtained through targeted investments;

- reporting is prepared using documents justifying transactions;

- it is necessary to have confirmation of the property transfer transaction;

- it is necessary to have documents confirming the expenses of the autonomous non-profit organization.

Other taxes: property, land, transport

NPOs, like other legal entities, pay all taxes related to property only if there are corresponding objects: real estate, transport, land. If there are no objects, then you do not need to pay tax or submit declarations.

accounting data reflected in the off-balance sheet account must be subtracted from the original cost of the object (clause 3 of Article 375 of the Tax Code of the Russian Federation)

Property tax benefits are provided for certain categories of non-profit organizations. In particular, they do not pay property tax and land tax (Articles 381 and 395 of the Tax Code of the Russian Federation):

- Religious organizations with property and land that is used for religious activities.

- All-Russian organizations of people with disabilities and NGOs established by them, working in the field of supporting people with disabilities. To receive benefits, people with disabilities or their representatives must make up at least 80% of the members of the NPO. Property and land must be used for statutory activities.

Organizational property tax and transport tax are regional, and land tax is local. Therefore, authorities of constituent entities of the Russian Federation or municipalities can establish additional benefits for these mandatory payments, including for non-profit organizations.

Tax return

By virtue of Art. 386 of the Tax Code of the Russian Federation, in general, taxpayers are obliged, at the end of each reporting and tax period, to submit calculations for advance tax payments and a property tax declaration to the tax authorities: - at their location; — at the location of each of its separate divisions, which have a separate balance sheet; - according to the location of each piece of real estate (for which a separate procedure for calculating and paying tax has been established). Tax calculations for advance tax payments are submitted no later than 30 calendar days from the end of the corresponding reporting period, and tax returns for the year - no later than March 30 of the year following the previous one.

Write-off of taxes and contributions for the 2nd quarter of 2021 for individual non-profit organizations

As part of the support measures taken in connection with the pandemic, some non-profit organizations will be completely written off the majority of taxes and insurance premiums for the 2nd quarter of 2021 (Article 2.3 of Law No. 172-FZ dated 06/08/2020).

You will only have to pay VAT and personal income tax withheld from employees’ salaries. Also, contributions “for injuries” will not be written off.

The benefit will be received by:

- Socially oriented non-profit organizations (SONCO). In order for taxes to be written off, SONCO must be included in a special register and receive grants or subsidies from the state in 2021.

- Centralized religious organizations, their structural divisions and SONCOs established by them.

- Other NGOs recognized as the most affected by the pandemic. Their register is formed by the Ministry of Economic Development (Resolution of the Government of the Russian Federation of June 11, 2020 N 847).

Reporting to statistical authorities for ANO

Autonomous non-profit organizations prepare statistical reports (clause 1 of article 32 of the Law of January 12, 1996 No. 7-FZ). Among these special forms are:

- 11-short, approved by Rosstat order No. 296 dated July 3, 2015;

- 1- NPO, approved by order of Rosstat dated August 27. No. 535. A sample form is presented in the appendix to the article.

Important! Statistical reporting forms are submitted by the ANO with a deadline limited to April 1 of the post-reporting year.

Conclusion

NPOs pay VAT and income tax only on income from commercial activities. To distribute income, expenses and input tax, separate accounting should be organized. You need to report on these taxes even if there is no taxable base.

If the organization has full-time employees, then personal income tax and contributions must be paid on a general basis. Payments to volunteers are only subject to compensation for meals that exceed the norm.

When calculating property taxes, NPOs must use depreciation instead of depreciation.

Additional benefits for VAT, property tax and land tax are provided for public organizations of people with disabilities and religious NGOs.

Socially oriented, religious and pandemic-affected NPOs will have the majority of taxes and contributions written off for the 2nd quarter of 2020.

General presentation and composition of accounting statements

Autonomous non-profit organizations (ANO), like others, are required to keep records and submit reports to the authorities annually.

According to legal norms, accounting reports of ANO consist of: (click to expand)

- balance. The difference between this report and commercial organizations is that the “Capital and Reserves” section is replaced by the “Targeted Financing” section. A sample reporting form is presented in the appendix to this article.

- report on the intended use of funds. This report contains information: the amount of financial resources used, the balance of funds at the beginning and end of the period, the amount of receipts;

- An explanatory note is not a mandatory element of reporting. It provides a breakdown of more detailed indicators. The form of such an entry may comply with the recommendations of the Ministry of Finance, but it is also possible to use your own template in the ANO.

Reporting can be submitted both electronically and in paper form.

In general, the reporting structure is formed in accordance with the applicable taxation regime.

Important! When applying the simplified tax system for autonomous non-profit organizations, the responsibility for submitting reports may be assigned to the manager. That is, the chief accountant may not be part of the staff.

FAQ

Question No. 1. If an independent non-profit organization does not have a bank account, what reports must be submitted?

Reporting is submitted in a simplified form, consisting of a balance sheet and a report on the intended use of funds.

Question No. 2. Do ANOs need to submit a report on financial results?

The financial results report is not required to be submitted. It can be replaced with a report on the use of funds. It is mandatory only in the following cases:

- ANO received a decent amount of income during the reporting year;

- Profit data does not fully reflect the financial condition of the ANO.

ANO reporting in the absence of activity

In the event that the activities of the autonomous non-profit organization were not carried out for any reason, there is no data on income and expenses, it is necessary to submit the following types of reports with zero indicators, which are reflected in the table below.

| Simplified accounting | · balance sheet; · report on intended use |

| Tax reporting | Declaration according to the simplified tax system |

| Reporting for employees | · 2 personal income taxes; · 6 personal income tax; · SZV-M; · SZV-experience; · ERSV; · 4 FSS |

| Statistical bodies | · Form 1-NKO; · Form No. 11 (short) |

Basic mistakes

Mistake No. 1. Very often, the management of an autonomous non-profit organization believes that having a chief accountant on staff is mandatory. However, this is a mistake, since autonomous non-profit organizations have the right to sign and submit reports directly to the manager.

Mistake No. 2. The mistake is that ANOs using the simplified tax system often believe that they no longer have to pay any taxes other than the simplified tax system. There are exceptions that need to be taken into account:

- property tax is also paid if there is property that is taxed at cadastral value;

- VAT is paid if the ANO is a VAT agent;

- transport tax is also paid if the ANO owns vehicles;

- if you own a plot of land, then you also pay land tax.

ANO reporting to the Ministry of Justice

Autonomous non-profit organizations are required to submit reports to the territorial branches of the Ministry of Justice, which are approved by order No. 72 dated March 29, 2010.

Submission of this reporting to the Ministry of Justice allows you to control the fact of the absence of foreigners among the members of the ANO, as well as the absence of foreign sources of funding.

Reporting forms include: (click to expand)

- form oNooo1 - information about managers;

- form oNooo2 – information on options for using ANO property;

- form oНоо1 – the amount of resources received from foreigners and international companies, stateless persons.

The first two forms are filled out by the ANO under the following conditions:

- no assets received from foreigners;

- the founders of the ANO are Russian citizens;

- revenues for the year are less than 3 million rubles.