The tax office issued a demand for payment of tax, then a decision to write off from the current account (collection order-card file) and a decision to suspend transactions on the current account, then a decision to the bailiffs. We paid the bailiffs the tax and 7% fee, half a year passed, then when the money arrives in the current account, the tax office writes off the funds according to the collection order. The remaining amount under the decision to suspend hangs like a dead weight on the account. Tell me the rules of law that violate our rights. In theory, before handing it over to the bailiffs, the tax authority should revoke the collection orders, but where is this written? And how to deal with this?

In accordance with Art. 46 of the Tax Code of the Russian Federation in the case provided for in paragraph 7 of Article 46 of this Code (which in particular include insufficiency or absence of funds in the accounts of the taxpayer (tax agent), the tax authority has the right to collect tax at the expense of property, including at the expense of the taxpayer’s cash (tax agent) - an organization or individual entrepreneur within the limits of the amounts specified in the request for payment of tax, and taking into account the amounts in respect of which collection was made in accordance with Article 46 of this Code.

Collection of tax at the expense of the property of a taxpayer (tax agent) - organization or individual entrepreneur is carried out by decision of the head (deputy head) of the tax authority by sending on paper or in electronic form within three days from the date of such decision the corresponding resolution to the bailiff for execution in the manner prescribed by the Federal Law “On Enforcement Proceedings”, taking into account the features provided for in this article.

The decision to collect tax at the expense of the property of the taxpayer (tax agent) - organization or individual entrepreneur - is made within one year after the expiration of the deadline for fulfilling the requirement to pay the tax. A decision to collect tax at the expense of the property of a taxpayer (tax agent) - an organization or an individual entrepreneur, made after the expiration of the specified period is considered invalid and cannot be executed. In this case, the tax authority may apply to the court to collect from the taxpayer (tax agent) - an organization or individual entrepreneur - the amount of tax due for payment. The application may be filed with the court within two years from the date of expiration of the deadline for fulfilling the requirement to pay the tax. A deadline for filing an application missed for a valid reason may be reinstated by the court.

At the same time, based on the content of paragraph 7 of Art. 46 of the Tax Code of the Russian Federation establishing that if there is insufficient or absence of funds in the accounts of a taxpayer (tax agent) - organization or individual entrepreneur or his electronic funds or in the absence of information about the accounts of the taxpayer (tax agent) - organization or individual entrepreneur or information about his details corporate electronic means of payment used for transfers of electronic funds, the tax authority has the right to collect tax at the expense of other property of the taxpayer (tax agent) - an organization or individual entrepreneur in accordance with Article 47 of this Code, it does not follow that if a decision is made to levy execution on the property is subject to cancellation of the decision to foreclose on the funds.

In clause 4.1 of Art. 46 of the Tax Code of the Russian Federation, which enshrines the list of grounds for suspending collection orders, also does not provide for the possibility of suspending a collection order of the tax authority to write off and transfer funds from the taxpayer’s accounts or revoking this order after receiving from the bailiff service a copy of the resolution to initiate enforcement proceedings to collect arrears for account of other property of the taxpayer.

As for judicial practice, it is contradictory:

The Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated July 19, 2005 N 853/05 in case N A73-5478/2004-10 stated: the Tax Code of the Russian Federation does not contain rules that the tax authority’s recall of collection orders from banks is a mandatory condition for making a decision to collect tax for account of other property of the taxpayer. In addition, the statement of the appellate court that the simultaneous application of two collection procedures cannot be considered legal, since this may entail repeated withdrawal of the same amounts for payment of the same taxes, is presumptive in nature and is not confirmed by the case materials. The mechanism of interaction between tax authorities and the bailiff service in the execution of decisions of tax authorities taken in pursuance of decisions to collect taxes at the expense of the taxpayer’s property creates certain guarantees for taxpayers aimed at preventing excessive collection of taxes and penalties from them.

Thus, the possibility of suspending the collection order of the tax authority to write off funds from the taxpayer’s accounts or recalling unfulfilled (both fully and partially) orders after receiving from the bailiff service a copy of the resolution to initiate enforcement proceedings to collect arrears at the expense of other property of the taxpayer of the Tax Code of the Russian Federation not provided. Reason - clause 4.1 of Art. 46 of the Tax Code of the Russian Federation (as amended by Law No. 248-FZ). In this case, the condition of the absence of double collection of taxes and penalties should not be violated.

Another point of view, even the opposite one set out in the said Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation. Thus, the Resolution of the Federal Antimonopoly Service of the West Siberian District dated February 18, 2010 N A45-16660/2009 established that the tax authority simultaneously carried out two collection procedures, which contradicts Art. Art. 46, 47 Tax Code of the Russian Federation. Foreclosure of a taxpayer's property is permitted only after exhaustion of the possibilities for debt collection using funds in the taxpayer's bank accounts. The reference to the tax authority’s lack of obligation to revoke collection orders from the bank does not give it the right to simultaneously levy execution on the taxpayer’s funds and his property.

Therefore, you can try to challenge collection orders or the decision to foreclose on funds, but based on the content of the Tax Code of the Russian Federation and contradictory judicial practice, it is not possible to predict the decision.

Question: Should the tax authority revoke a collection order to transfer tax, provided that it has been in the bank for more than 6 years and has not yet been executed due to the organization’s lack of money in its account? Answer: Each person must pay legally established taxes and fees (Article 57 of the Constitution of the Russian Federation, paragraph 1 of Article 3 of the Tax Code of the Russian Federation). In case of non-payment or incomplete payment of the tax within the established period, the obligation to pay the tax is compulsorily fulfilled by foreclosure on the funds in the taxpayer’s bank accounts (Clause 1 of Article 46 of the Tax Code of the Russian Federation). The tax is collected by decision of the tax authority, by sending to the bank where the taxpayer’s accounts are opened, instructions from the tax authority to write off and transfer to the budget system of the Russian Federation the necessary funds from the taxpayer’s accounts (clause 2 of Article 46 of the Tax Code of the Russian Federation). In this case, funds are written off from the client’s account by the bank without the client’s order (Clause 2 of Article 854 of the Civil Code of the Russian Federation). If there is not enough money in the taxpayer’s current account or there is no money on the day the bank receives an order from the tax authority to transfer the tax, such an order is executed as funds are received in these accounts. This is done no later than one business day from the day following the day of each receipt of funds to ruble accounts, and no later than two business days from the day following the day of each such receipt to foreign currency accounts (clause 6 of Article 46 of the Tax Code of the Russian Federation). That is, until the entire amount of the arrears is repaid, the bank is obliged to execute the collection order of the tax authority and write off all funds received into the account to pay off the tax arrears. Also, if there is insufficiency or absence of funds in the taxpayer’s accounts, the tax authorities are given the right to collect tax at the expense of other property of the taxpayer (Clause 7 of Article 46 of the Tax Code of the Russian Federation). But the tax authorities are not obliged, before the collection procedure at the expense of property, to revoke instructions to write off and transfer to the budget system of the Russian Federation the necessary funds from the taxpayer’s accounts. The Presidium of the Supreme Arbitration Court of the Russian Federation also came to this opinion, pointing out that the revocation of collection orders is not a necessary condition for the tax authority to make a decision to collect tax at the expense of the taxpayer’s property (Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated July 19, 2005 N 853/05). However, if the tax authority decides to collect the amount of arrears from the property, then on the day it receives from the bailiff service a copy of the resolution to initiate enforcement proceedings, the tax authority must decide to suspend the write-off of funds in an indisputable manner from the taxpayer’s accounts and send it on the same day it to the appropriate bank (clause 3.2 of the Methodological Recommendations for organizing interaction between the tax authorities of the Russian Federation and the bailiff service of the Ministry of Justice of the Russian Federation when executing decisions of tax authorities on the collection of taxes (fees), as well as penalties at the expense of the property of a taxpayer-organization or tax agent - organizations approved by Order of the Ministry of Justice of Russia N 289, Ministry of Taxes of Russia N BG-3-29/619 dated November 13, 2003). It should also be taken into account that the tax authority’s order to write off and transfer the necessary funds from the taxpayer’s accounts to the budget system of the Russian Federation does not have a specific validity period. Such an order is considered executed at the moment of repayment of the taxpayer's arrears to the budget of the Russian Federation. Therefore, if the action of the above order in the manner established by the Methodological Recommendations is not suspended by the tax authority, then the bank is obliged to execute it. Otherwise, the bank may be held liable for failure to comply with the tax authority’s order to transfer taxes (Article 135 of the Tax Code of the Russian Federation). A.N. Krasnopeeva Publishing house "Glavnaya Kniga" 10/09/2007

In this article we will examine in detail what a collection order is and when it is issued. And also - what to do if a collection order from the tax authority has arrived at your account, and how to recall it. An example of filling out a collection order and a form can be found in our article.

collection order>>>

What is a collection order

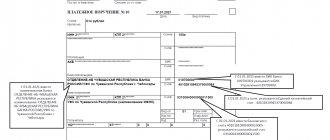

A collection order is a document that allows you to write off funds from accounts belonging to him without the payer’s consent. Thus, a collection document is a settlement document on the basis of which payment occurs without the acceptance of the account owner. Let's see what a collection order looks like.

Urgent news from the Central Bank of the Russian Federation: banks are prohibited from accepting payment orders with such words in the payment purpose>>>. Read more in the Russian Tax Courier magazine.

A collection order is very similar to a regular payment order to a bank. It is drawn up on form 0401071 (Order of the Ministry of Finance dated November 12, 2013 No. 107n).

Payment of the company's debt by third parties

There is another possible course of action - payment of tax by another person. Moreover, it does not matter from whom the payment comes (from an individual or a legal entity). The main thing is that the purpose of the payment must indicate: “payment of tax... for (period) for Romashka LLC TIN/KPP...”.

Despite the fact that the payer will be another person, the Federal Tax Service will determine the payment based on the information specified in the “Purpose of payment” field.

If the taxpayer-debtor decides to take this option, then immediately after the payment has been made, contact the tax service and notify that the payment of the tax or fee was made by another person (name of the enterprise or last name, first name and patronymic, who made the payment, TIN and checkpoint if available). You can also send a payment order to the Federal Tax Service to confirm payment.

Russian legislation has made it possible to pay taxes and fees for third parties from the end of 2021

, when Part 1 of Article 45 of the Tax Code of Russia was changed. Payment can be made through the special service “Payment of taxes for third parties” on the Federal Tax Service website.

If the tax payment was made by third parties, you should pay attention to documentary evidence of this transaction. If this is gratuitous assistance from the owner, then an appropriate agreement must be drawn up. If the parent organization or an interdependent person paid, then the payment of tax must be reflected in the reporting in accordance with the rules of PBU. Otherwise, a number of questions may arise

from the Federal Tax Service specialists.

What is a collection order used for?

A collection order is issued in the following cases.

If funds must be written off to pay off debts to executive bodies in a legal and indisputable manner.

Example

The company did not pay taxes on time and did not pay off debts voluntarily at the request of the tax authorities. Then the inspectorate sends a collection to the bank and forcibly writes off the money to pay off the tax debt.

If the bank has the right to write off funds without acceptance based on agreements with the payer. Most often, this happens if the parties to the contract agree and transfer to the bank the conditions for direct debit on the part of the payer, subject to the fulfillment of certain conditions of the contract.

Example

An example is payment of utility bills.

These tips will help you work without penalties:

Failure of the bank to fulfill the taxpayer’s instructions on time

If there are insufficient funds in the taxpayer's account to fulfill the order, the bank may allow the order to be non-executed. The bank may allow the order not to be executed due to insufficient funds in the correspondent account with the bank. The two situations are handled differently because they are different from each other.

In both cases, the bank is obliged to notify the taxpayer and the tax authority of the impossibility of executing the order. The form of such notification is established by the Central Bank.

Formal debiting of funds from the payer’s account, in which the corresponding amount does not go to the budget due to lack of funds in the accounts, is not permissible.

A bank that has committed a violation of the rules for conducting settlement transactions due to its own fault is obliged to:

- return the amount of money to the client for an unfulfilled bank order;

- compensate for all losses associated with this violation;

- pay interest that will be accrued on the amount of the unfulfilled order.

Collection order from the tax authority

The inspectorate has the right to issue collection orders to the company’s account if the company does not fulfill its obligation to pay taxes voluntarily (Article 46 of the Tax Code of the Russian Federation). Inspectors must make a decision on debt collection within two months from the date of expiration of the period for voluntary payment of tax upon request.

Simultaneously with the decision to collect, the inspectorate issues a collection order for the entire amount of the arrears and most often blocks the accounts. Next, there are three possible scenarios.

The company has the right to pay the debt voluntarily even after the tax authorities have sent collection to the bank. In this case, the company needs to quickly inform the inspectorate about the payment and show the payment slips with a bank statement. Then the inspectorate withdraws the collection from the bank.

If the company is not going to pay voluntarily, then the bank simply writes off the collection debts. Moreover, the bank is obliged to do this no later than the next business day after receiving it.

A situation may arise that there is no money in the account of the company to which the inspection sent the collection. Then the tax authorities send the documents for collection to the bailiff service, and they seize the debtor’s property, sell it and pay off the debt.

If tax authorities missed this deadline, they have the right to go to court to restore it. They are given six months to do this from the date of expiration of the period specified in the requirement to pay the tax (Clause 3 of Article 46 of the Tax Code of the Russian Federation).

To pay taxes on time, use ready-made payment slips:

- Samples of payment orders for insurance premiums in 2017

- Payment order for income tax in 2021: sample

- Payment order for VAT in 2021: sample

- Payment order for personal income tax in 2021: sample

Topic: How to revoke a tax collection

Quick link Documentation and reporting Up

- Navigation

- Cabinet

- Private messages

- Subscriptions

- Who's on the site

- Search the forum

- Forum home page

- Forum

- Accounting

- General Accounting Accounting and Taxation

- Payroll and personnel records

- Documentation and reporting

- Accounting for securities and foreign exchange transactions

- Foreign economic activity

- Foreign economic activity. Customs Union

- Alcohol: licensing and declaration

- Online cash register, BSO, acquiring and cash transactions

- Industries and special regimes

- Individual entrepreneurs. Special modes (UTII, simplified tax system, PSN, unified agricultural tax)

- Accounting in non-profit organizations and housing sector

- Accounting in construction

- Accounting in tourism

- Budgetary, autonomous and government institutions

- Budget accounting

- Programs for budget accounting

- Banks

- IFRS, GAAP, management accounting

- Legal department

- Legal assistance

- Registration

- Inspection experience

- Enterprise management

- Administration and management at the enterprise

- Outsourcing

- Enterprise automation

- Programs for accounting and tax accounting Info-Accountant

- Other programs

- 1C

- Electronic document management and electronic reporting

- Other tools for automating the work of accountants

- Clerks Guild

- Relationships at work

- Accounting business

- Education

- Labor exchange Looking for a job

- I offer a job

- Club Clerk.Ru

- Friday

- Private investment

- Policy

- Sport. Tourism

- Meetings and congratulations

- Author forums Interviews

- Simple as a moo

- Author's forum Goblin_Gaga Accountant can...

- Gaga's opusnik

- Internet conferences

- To whom do I owe - goodbye to everyone: all about bankruptcy of individuals

- Archive of Internet conferences Internet conferences Exchange of electronic documents and surprises from the Federal Tax Service

- Violation of citizens' rights during employment and dismissal

- New procedure for submitting VAT reports in electronic format

- Preparation of annual financial/accounting statements for 2014

- Everything you wanted to ask the electronic document exchange operator

- How to turn a financial crisis into a window of opportunity?

- VAT: changes in regulatory regulation and their implementation in the 1C: Accounting 8 program

- Ensuring the reliability of the results of inventory activities

- Protection of personal information. Application of ZPK "1C:Enterprise 8.2z"

- Formation of a company's accounting policy: opportunities for convergence with IFRS

- Electronic document management in the service of an accountant

- Time tracking for various remuneration systems in the program “1C: Salary and Personnel Management 8”

- Semi-annual income tax report: we will reveal all the secrets

- Interpersonal relationships in the workplace

- Cloud accounting 1C. Is it worth going to the cloud?

- Bank deposits: how not to lose and win

- Sick leave and other benefits at the expense of the Social Insurance Fund. Procedure for calculation and accrual

- Clerk.Ru: ask any question to the site management

- Rules for calculating VAT when carrying out export-import transactions

- How to submit reports to the Pension Fund for the 3rd quarter of 2012

- Reporting to the Social Insurance Fund for 9 months of 2012

- Preparation of reports to the Pension Fund for the 2nd quarter. Difficult questions

- Launch of electronic invoices in Russia

- How to reduce costs for IT equipment, software and IT personnel using cloud power

- Reporting to the Pension Fund for the 1st quarter of 2012. Main changes

- Income tax: nuances of filling out the declaration for 2011

- Annual reporting to the Pension Fund. Current issues

- New in financial statements for 2011

- Reporting to the Social Insurance Fund in questions and answers

- Semi-annual reporting to the Pension Fund in questions and answers

- Calculation of temporary disability benefits in 2011

- Electronic invoices and electronic primary documents

- Preparation of financial statements for 2010

- Calculation of sick leave in 2011. Maternity and transition benefits

- New in the legislation on taxes and insurance premiums in 2011

- Changes in financial statements in 2011

- DDoS attacks in Russia as a method of unfair competition.

- Banking products for individuals: lending, deposits, special offers

- A document in electronic form is an effective solution to current problems

- How to find a job using Clerk.Ru

- Providing information per person. accounting for the first half of 2010

- Tax liability: who is responsible for what?

- Inspections, collection, refund/offset of taxes and other issues of Part 1 of the Tax Code of the Russian Federation

- Calculation of sick sheets and insurance premiums in the light of quarterly reporting

- Replacement of unified social tax with insurance premiums and other innovations of 2010

- Liquidation of commercial and non-profit organizations

- Accounting and tax accounting of inventory items

- Mandatory re-registration of companies in accordance with Law No. 312-FZ

- PR and marketing in the field of professional services in-house

- Clerk.Ru: design change

- Building a personal financial plan: dreams and reality

- Preparation of accounting reporting. Changes in Russia accounting standards in 2009

- Kickbacks in sales: pros and cons

- Losing a job during a crisis. What to do?

- Everything you wanted to know about Clerk.Ru, but were embarrassed to ask

- Credit in a crisis: conditions and opportunities

- Preserving capital during a crisis: strategies for private investors

- VAT: deductions on advances. Questions with and without answers

- Press conference of Santa Claus

- Changes to the Tax Code coming into force in 2009

- Income tax taking into account the latest changes and clarifications from the Ministry of Finance

- Russian crisis: threats and opportunities

- Network business: quality goods or a scam?

- CASCO: insurance without secrets

- Payments to individuals

- Raiding. How to protect your own business?

- Current issues of VAT calculation and reimbursement

- Special modes: UTII and simplified tax system. Features and difficult questions

- Income tax. Calculation, features of calculus, controversial issues

- Accounting policies for accounting purposes

- Tax audits. Practice of application of new rules

- VAT: calculation procedure

- Outsourcing Q&A

- How can an accountant comply with the requirements of the Law “On Personal Data”

- The ideal archive of accounting documents

- Service forums

- Archive FAQ (Frequently Asked Questions) FAQ: Frequently Asked Questions on Accounting and Taxes

- Games and trainings

- Self-confidence training

- Foreign trade activities in harsh reality

- Book of complaints and suggestions

- Diaries

Reference

Question: In accordance with Article 46 of the Tax Code of the Russian Federation, tax collection is carried out by sending to the bank in which the accounts of the taxpayer (tax agent) - an organization or individual entrepreneur - are opened, an order from the tax authority to write off and transfer to the budget system of the Russian Federation the necessary funds from the accounts taxpayer (tax agent) - organization or individual entrepreneur.

In accordance with Article 30 of the Tax Code of the Russian Federation, tax authorities constitute a single centralized system of control over compliance with legislation on taxes and fees, the correctness of calculation, completeness and timeliness of payment (transfer) to the budget system of the Russian Federation of taxes and fees, and in cases provided for by the legislation of the Russian Federation Federation, for the correctness of calculation, completeness and timeliness of payment (transfer) to the budget system of the Russian Federation of other obligatory payments. This system includes the federal executive body authorized for control and supervision in the field of taxes and fees, and its territorial bodies.

In accordance with the Regulations on non-cash payments in the Russian Federation, approved by the Central Bank of the Russian Federation on October 3, 2002 N 2-P, collectors have the right to revoke settlement documents accepted by the bank in the order of settlements for collection (collection orders), not paid due to insufficient funds for client’s account and placed in the file cabinet under off-balance sheet account N 90902 “Settlement documents not paid on time.” Revocation of collection orders is carried out by sending a written application from the collector to the payer's bank.

The Joint-Stock Investment Commercial Bank (closed joint-stock company) receives applications from territorial bodies (inspections) of the Federal Tax Service of Russia to revoke collection orders that were sent to the bank by other territorial bodies (inspections) of the Federal Tax Service of Russia.

In order to have a uniform understanding of the procedure for revoking collection orders by tax authorities, we ask you to provide clarification on the following issue:

Does a territorial body (inspectorate) of the Federal Tax Service of Russia have the right to send to a bank an application for the revocation of collection orders that were sent to the bank by another territorial body (inspectorate) of the Federal Tax Service of Russia?

Answer: The Department of Tax and Customs Tariff Policy reviewed letter No. 6955 dated May 13, 2009 on the issue of the powers of tax authorities to revoke collection orders and reported the following.

In accordance with paragraph 2 of Article 46 of the Tax Code of the Russian Federation (hereinafter referred to as the Code), tax collection is carried out by decision of the tax authority by sending to the bank in which the taxpayer’s accounts are opened, instructions from the tax authority to write off and transfer to the budget system of the Russian Federation the necessary funds from taxpayer accounts.

Based on the meaning of this paragraph, an order to write off and transfer tax amounts to the budget system of the Russian Federation is drawn up and sent to the bank by the tax authority that made the decision to collect the tax from funds in the taxpayer’s bank accounts. Consequently, the same tax authority has the right to revoke the specified order.

Clause 2.17 of the Regulations on non-cash payments in the Russian Federation dated October 3, 2002 N 2-P, approved by the Central Bank of the Russian Federation, stipulates that recipients of funds (collectors) have the right to revoke their settlement documents accepted by the bank in the procedure for collection settlements (payment requests, collection orders) not paid due to insufficient funds in the client’s account and placed in the file cabinet under off-balance sheet account N 90902 “Settlement documents not paid on time.”

According to paragraph 1 of Article 30 of the Code and Articles 1 and 2 of the Law of the Russian Federation dated March 21, 1991 N 943-1 “On the Tax Authorities of the Russian Federation,” the tax authorities constitute a single centralized system of control over compliance with the legislation on taxes and fees, the correctness of calculation, completeness and timely payment (transfer) of taxes and fees to the budget system of the Russian Federation, and in cases provided for by the legislation of the Russian Federation, the correctness of calculation, completeness and timeliness of payment (transfer) to the budget system of the Russian Federation of other obligatory payments. This system includes the federal executive body authorized for control and supervision in the field of taxes and fees, and its territorial bodies.

By virtue of paragraph 3 of Article 31 of the Code, higher tax authorities have the right to cancel and change decisions of lower tax authorities if these decisions do not comply with the legislation on taxes and fees.

Taking into account the above, we believe that the revocation of an order to write off and transfer funds from a taxpayer’s account to the budget system of the Russian Federation can be carried out both by the tax authority that sent such an order to the bank, and by a tax authority that did not send the specified order, for example, by a successor tax authority in connection with the reorganization of the tax authority that sent the order to the bank.

| Deputy Director of the Department | S.V. Razgulin |

Letter of the Department of Tax and Customs Tariff Policy of the Ministry of Finance of the Russian Federation dated October 22, 2009 N 03-02-07/1-474

The text of the letter was not officially published

In 2021, it will be easier for inspectors to collect debts

From June 1, 2021, if inspectors did not have time to issue a collection, the entire procedure from going to court to collecting the debt will take two months. This applies to debts whose amount does not exceed 100,000 rubles. (Part 3 of Article 229.2 of the Arbitration Procedure Code of the Russian Federation).

Having received an application from the inspectorate, the judge issues a court order within 10 working days. There is no need for any proceedings to summon both parties. Only a single decision of the court (Part 4 of Article 229.5 of the Arbitration Procedure Code of the Russian Federation). Next, five working days are allotted to send the order to the debtor. And the debtor is given 10 working days to file his objections. After another 10 working days, the court order comes into force. Based on it, bailiffs will collect debts on their own.

What is included in a collection order

Depending on the specific situation, the collection order must include:

- The number of the law on the basis of which the collection order was issued, as well as the corresponding number of the article of the law.

- Number and date of the writ of execution, name of the organization, case number in legal proceedings.

Important: if the collection was issued on the basis of a writ of execution, the original or a duplicate of the writ of execution must be attached to it.

- Agreement indicating the details and conditions on the basis of which the collection order was inserted