To report to the Federal Tax Service on income for the past year, individuals must use form 3-NDFL. Since most people rarely have to file declarations, filling out some indicators causes certain difficulties. One of these values is the adjustment number in 3-NDFL. Often report writers will simply skip this line, but it must be completed. We will explain in simple words why this field is allocated in the document, and what the adjustment number in 3-NDFL means.

What does “adjustment number” mean in 3-NDFL?

Entrepreneurs, especially inexperienced ones, for the most part do not know what the adjustment number in the tax return means, as a result of which simply any number is entered in the corresponding field. Some even put three-digit numbers or something like “99”.

But this cannot be done under any circumstances, because the adjustment number in the certificate is data on the number of tax returns sent to the Federal Tax Service for the last reporting period . Thus, the more declarations with corrections were filed for a particular tax reporting period, the larger the number should be opposite the line “correction number”.

Adjustments are needed for:

- Corrections of minor errors, typos, data discrepancies;

- Declare additional income that has appeared since the initial submission of the declaration;

- Accounting for tax revenues so that they can later be used to obtain a tax deduction.

This number is needed because the number of adjustments is virtually unlimited, and data between declarations filed at different times can vary greatly. The number allows you to track how many VAT or other tax returns have already been filed during the reporting period.

Reduced tax

When filing an amended return to correct errors that led to an understatement of the amount of tax payable, several situations may arise.

First. The accountant noticed an error in the declaration in the current reporting period, immediately after its submission, but before the deadline for submission established in the Tax Code. If he manages to submit an “adjustment” before the end of this period, then it is considered submitted on the day the updated declaration is submitted. In this case, there is no penalty for violating the deadlines. In addition, if the amount of additionally assessed tax is not paid, only penalties () are charged on the arrears.

Second situation. The accounting specialist noticed the error after the deadline. In this case, in order to avoid penalties, when submitting corrective information, you need to calculate and pay the amount of penalties for the period from the date of the established deadline for submitting documents to the date of filing the “clarification”. Only after making sure that penalties have been paid can you send an updated declaration. What is the mystery of this particular sequence of actions? If penalties are paid and a return is filed on the same day, the money will not have time to get into the taxpayer’s card. The declaration will be registered as submitted without payment of sanctions, that is, in violation of the procedure. This threatens the company with a fine of 20 percent of the amount of additional tax accrued (clause 1, clause 4, article 81 of the Tax Code of the Russian Federation).

How to find out the number?

You can find out the final number that needs to be entered in the column by simple calculation using the formula:

total value = number of previously submitted declarations -1

As an example: if four declarations have already been filed during the reporting tax period, the adjustment number in the UTII declaration should be with the value “3”.

In this case, it does not matter in what form the document is executed: in 2nd personal income tax, 3rd personal income tax or the adjustment number in the certificate in form 6 personal income tax is always calculated using the above formula.

Attention: even if you submit reports to the tax authorities for the first time during the reporting period, you must still indicate the number of previously submitted papers.

How to make adjustments in the taxpayer program

The first step is to find out what the latest version of the program is. You can view and download the latest version of the program here.

Now let's find out which version we have.

We launch the program and look at the program version in the header.

Adjustment of calculation of insurance premiums 2019

→ → Current as of: February 20, 2021

You will have to submit a new Calculation if (): section 3 contains unreliable personal data of an individual; in section 3, errors were found in numerical indicators (in the amount of payments, base, contributions); the sum of the numerical indicators of sections 3 for all individuals does not coincide with the data for the organization as a whole, reflected in subsections 1.1 and 1.3 of Appendix No. 1 to section 1 of the calculation; the amount of contributions to the compulsory pension insurance (based on a base not exceeding the maximum value)

How to make an updated VAT return in 2021 - 2019?

> > > Tax-tax February 05, 2021 An updated VAT return must be submitted when errors are identified that lead to an understatement of the tax or an overstatement of its amount accrued for reimbursement.

Filing an updated VAT return in other cases is the right of the taxpayer, and not his obligation. We'll tell you how to make and submit a clarification.

Submitting an updated or corrective VAT return to the Federal Tax Service allows the taxpayer to correct errors made in the previously submitted version of this document. At the tax office when conducting

Taxpayer legal entity version 4.62 dated April 11, 2021

18948 Taxpayer of Legal Entities is a program that helps entrepreneurs, businessmen, and individuals in preparing reports to the tax authorities.

Bookmark this page to always have the latest updates! Launch the program by double-clicking on the downloaded installation file. Windows will most likely ask you if you agree to open the executable file, click yes or OK.

Next, a window with a license agreement will open in front of you:

Section 3 is subject to inclusion in relation to those FLs in which changes (additions) are made. Thus, the updated Calculation of the SV payer making payments must necessarily contain: - Section 1. Mandatory. The information must be updated to replace the previously submitted information - Appendix 1 to Section 1.

Required. When is it necessary to submit an updated

How to make an adjustment in a taxpayer's legal entity for insurance premiums

The Tax Code of the Russian Federation does not have exact deadlines for its submission.

- If an error is identified by tax officials, the policyholder is given 5 days to submit an adjustment. If this deadline is violated, a fine of 5,000 rubles is imposed.

- In order not to pay a fine of 20% of the amount of underpaid contributions (clause 1 of Article 122 of the Tax Code of the Russian Federation), before submitting the adjustment, you must pay the arrears on insurance premiums and accrued penalties (clause 4 of Article 81 of the Tax Code).

The adjustment is submitted in the same way as the initial DAM report.

- If the number of employees is more than 25 people, then the report is transmitted electronically.

- If the staff is less than 25 people, then it is allowed to submit the calculation in paper form.

Calculations of the amounts of accrued and paid contributions are transferred to the tax office at the place of registration of the enterprise based on the results of each quarter by the 30th day of the month following the reporting period.

Taxpayer legal entity

06/05/2019 11:30 The program is designed to automate the process of preparation by legal entities and individuals of tax and accounting documents, calculation of insurance premiums, certificates of income of individuals (form No. 2-NDFL), special declarations (declaration of assets and accounts), documents on registration of cash registers and others.

Data input

Entering a VAT return in the program from the Federal Tax Service is divided into separate entry sections.

Entering Sections 1-7 involves regular entry of a declaration, and entering Sections 8-12 and appendices Sections 8 and 9 involves tabular entry.

To enter the appropriate section, use the button related to this section.

Entering summary information for Sections 8 and 9 and their annexes also involves entering using the corresponding buttons (total data can also be entered when entering information in sections). If there is entered information for a section, then its quantity will be shown in the name of the button in brackets.

Adjustment of the declaration

When created for the first time, the declaration is created as a main calculation. Use the button (select the appropriate item in the context menu that appears):

- to submit a corrective VAT return;

- changes in the declaration adjustment number;

- deleting the declaration with the maximum adjustment number;

- viewing declaration data of previous payments

Clarified

If the declaration has updated calculations, you can go to the required calculation by selecting the appropriate item. In this case, only the declaration with the maximum adjustment number is available for editing, and the remaining calculations are only for viewing.

How to check the declaration

To control the declaration, use the button. This will produce:

1. Control of Sections 1-7 according to the control ratios of the declaration.

2. Control of Sections 8-12 is similar to control of these sections separately.

77 Moscow city

The program is designed to automate the process of preparation by legal entities and individuals of tax and accounting documents, calculation of insurance premiums, certificates of income of individuals (Form No. 2-NDFL), special declarations (declaration of assets and accounts), documents for registering cash registers and others.

You can download the program for filling out the calculation of insurance premiums by opening the Abstract.

The program allows all categories of taxpayers to prepare the following documents:

- Tax and accounting reporting;

- Calculations of insurance premiums;

- Documents on personal income tax (2-NDFL, 3-NDFL, 4-NDFL, 6-NDFL);

- Applications for taxpayer registration;

- Notifications of controlled transactions (transfer pricing);

- Special declaration;

- Documents for registering cash registers;

- Documents for the application of the Unified Agricultural Tax, the simplified tax system and the patent taxation system;

- Documents for registration of gambling business objects;

- Documents for registration of a foreign organization;

- Requests for information services;

- Information messages about the power of attorney;

- Information for the VAT declaration (invoices, books of purchases and sales, journal of invoices);

- Requirements for providing clarification on VAT;

- Registers of information on VAT (rate 0%);

- Notifications of financial market organizations (FMO).

The software also has the following features:

1. Question: During installation, a Windows reboot was required, after which the program does not start

Answer: Run the installer again.

2. Question: During installation, the program asks for drive F (can be E, B, H ... Z

Answer: Apparently the previous version was installed from this disk. Create drive F, it doesn’t matter what will be on it (for example, connect any resource as drive F - my computer / connect a network drive) and run the installation program again.

Answer: No. If you do not delete the folder where the program was installed, the installation program does not delete any entered data.

4. Question: After installation, I do not see the previously entered data (reporting forms)

Answer: Everything is fine. Options:

1. You installed the program in the wrong folder:

— on the computer where the program was installed, execute the menu item in the NP LE program Service/Miscellaneous/Search for folders with the program;

— after the mode has been running for as long as possible, a list of folders will appear where the program was ever installed and you worked with it;

— in the list of found folders you will see information about where the program was installed, when you last entered it, how many NPs were entered in it;

— remember the path to the option you need;

— delete the program — Start/Programs/Taxpayer Legal Entity/Delete a program;

— install the program according to the path you remember.

2. The entered data (report form) is in a different period from the current reporting period - this can be resolved by changing the reporting period in the upper right corner of the program window;

5. Question: It is impossible to install Taxpayer Legal Entity with the installation program. What to do?

Answer: the distribution files were damaged either when copied from an electronic medium or received via the Internet or as a result of a virus

— if you downloaded the version via the Internet, check that your computer has a stable connection to the Internet and download the program installation package again

- if the version was written to disk for you by the Federal Tax Service - try copying it from another computer or write it down again

Source: https://nalog-plati.ru/voprosy/kak-v-programme-nalogoplatelshhik-yul-sdelat-korrektirovku

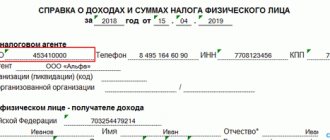

How to fill it out correctly?

Please note: The Federal Tax Service requires that if there are empty fields on the certificate, there should be dashes after the number.

That is, if you are submitting a declaration for the second time, the line indicating the number should contain the value “1 – -”; if the declaration is submitted for the eleventh time, you need to put “10-”. The Tax Service requires compliance with the rule, because otherwise, it will not be entirely clear to the inspection inspector whether the number is written in full or whether the entrepreneur forgot to add a few digits. Cross-throughs, mechanical damage to the paper (due to an attempt to erase a number with an eraser, for example), are not allowed, and “smearing” the number with a proofreader is also not encouraged.

If for some reason you entered the number incorrectly, but categorically do not want to write a new declaration, you can correct the document: just carefully cross out the incorrect inscription with red ink, and write the correct value on top with the same red ink.

There should be only one dash line, and it should be placed in such a way that the originally entered data is clearly readable. If you do not follow these rules, the tax inspector may not accept the document, requiring you to submit a new declaration.

What number should I indicate when submitting for the first time?

As of 2021, the Federal Tax Service has not changed the rules for indicating the number upon initial submission. Therefore, as before, you need to put “0” in the number column . If you are submitting a document for the second time, you need to put “1” - etc.

During the initial submission, the same registration rules apply as when entering corrective data. This means the following: corrections are not allowed, and if they need to be made, then only according to the instructions above; There should be dashes after the number “0”. The final appearance of the number should be: “0 – -”.

Date of submission of the clarification with a higher tax amount

Filing an amended return with a larger tax amount after the due date has expired indicates that the tax was not paid in full. And this is fraught with a fine of 20% of the amount of underpayment (clause 1 of article 122 of the Tax Code of the Russian Federation, clauses 19,20 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2013 N 57, Order of the Federal Tax Service of Russia dated August 22, 2014 N SA-4-7 /16692 ).

To avoid a fine, you must pay the arrears and penalties before submitting the updated declaration. Then, if, before submitting the clarification, the tax authorities do not find an error in the declaration you originally submitted and do not inform you about it, and also do not schedule an on-site audit of your organization, then you will not be held accountable (clause 4 of Article 81 of the Tax Code of the Russian Federation).

Is it necessary to submit clarifications?

First, the new return with adjustments should not take into account the information in the original return . In other words, the new document must contain only current information; there is no need to make calculations based on the difference between declarations.

You need to submit new papers as if you had not previously submitted any declarations for this reporting period. The only difference between the documents will be the same number - with each new document submitted to the Federal Tax Service, it will increase.

Secondly, making corrections in itself is a necessity if mistakes were made or important details were not taken into account : profitability for the reporting period, the amount of taxes paid and tax deductions, etc. If the initial submission containing factual errors is not corrected during the reporting tax period, the Federal Tax Service may collect a fine or penalty from the entrepreneur.

Thirdly, in most cases, the Federal Tax Service does not require additional clarifications (explanations) to new declarations . As a rule, if there are no significant discrepancies or incorrect calculations in the latest document, the Federal Tax Service simply does not take into account the data in the first declarations. In this case, the last submitted reports are accepted as the main document.

But in a number of situations, providing additional clarification is mandatory or at least desirable:

- If, compared to the initial delivery, the amount of tax deduction has decreased. Even a decrease of 1000-2000 rubles may result in a letter from the Federal Tax Service demanding clarification;

- If the data of the first and final declarations, submitted at approximately the same time, diverge too much - by amounts greater than 10% of the enterprise’s average annual turnover. Clarifications may be required if the initial and final declarations were filed, for example, within one to two months.

Remember that if factual errors are detected, the amount of tax deductions is reduced and other manipulations are made, the head of the enterprise may be fined in accordance with Art. 122 of the Tax Code of the Russian Federation.

Results

Errors in already submitted tax reports are divided into 2 groups: those requiring clarification and those left at the discretion of the taxpayer. For whatever reason the reporting is specified, it is formed in the same way as the original one (on the same form and according to the same rules), but filled in with the correct data. What distinguishes such a report from the original one is the serial number of the correction, which is entered in a special field on the title page. In the original report, 0 is indicated there, and the numbering of updated reports, therefore, begins with the number 1.

Sources: Tax Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Conclusion

So, what is this - the adjustment number in 3 personal income tax, and what should I write in this column? The number is the total number of previously submitted declarations. You can correctly calculate the value of the number using the formula: the number of previously submitted declarations is 1.

If the declaration is submitted to the Federal Tax Service for the first time during the reporting period, it is necessary to enter the value “0” in the column; after the number, whatever it is, there must be dashes (in empty fields). Russian entrepreneurs are strictly required to submit updated information with explanations if the amount of tax deductions as a result has decreased or the profitability of the enterprise has increased significantly in a short period of time.

And more about the nuances

Filing an updated VAT and excise tax return during a desk audit has its own characteristics. According to the explanations that the Federal Tax Service gave in a Letter dated July 16, 2013, the law requires the mandatory conduct of an independent “camera study” of the updated declaration. During an on-site audit, inspectors cannot take into account updated data. In addition, if the initial VAT return declares tax to be refunded, and then, before the desk audit report is delivered, an amendment is submitted (also with a refund), then the report on the initial declaration will still be issued. Moreover, if the amount of compensation in the “clarification” is less than in the original document, the companies will reimburse the smaller amount.

Elena Seledtsova

, for the magazine "Calculation"

How to save on VAT without violating the tax code

This e-book contains complete information about what legal ways to optimize VAT are provided for in Russian legislation. They are enough to

It is not uncommon for an accountant, when paying a certain amount to an employee, to ask the question: is this payment subject to personal income tax and insurance contributions? Is it taken into account for tax purposes?

If a taxpayer discovers an error in a declaration previously submitted to the Federal Tax Service, then sometimes he may not make an adjustment to it, and sometimes he is simply obliged to submit an updated declaration.

Clarified

If the declaration has updated calculations, you can go to the required calculation by selecting the appropriate item. In this case, only the declaration with the maximum adjustment number is available for editing, and the remaining calculations are only for viewing.

If an updated declaration is submitted, an indication of the relevance of the previously submitted information reflected in this section of the declaration becomes available. When adding an updated declaration calculation, this attribute is automatically set to the “current” state. If you change the section information while working, this flag will be removed automatically.

Possible errors and problems

The tax office immediately returns the incorrectly drawn up document, describing in the notification what exactly needs to be changed:

- lack of information on standard deductions;

- incomplete data about the taxpayer himself - his activity codes are not indicated (they must be entered in the directory);

- The correction number field is empty.

Anyone, even an experienced taxpayer, can make mistakes; it is useful to check a sample of the finished report and take your time when filling it out. Most problems arise due to inattention.

Is it necessary to submit a corrective return?

In the world of tax reporting, the concept of an “adjusting return” often appears. This term arose due to the frequent occurrence of various errors when filling out the main document by a taxpayer. Moreover, these errors and blunders are clarified already at the stage of verification of the document by tax authorities. If errors, omissions or typos are identified, tax inspectors contact the payer and ask the citizen to re-issue the declaration.

The reissued document is called a “corrective declaration.” After the payer reissues the form taking into account the identified errors, in the cell where the code is indicated, one more digit should be entered in the numbering. After which the document is again sent for verification to NI. It is worth considering that errors are possible when specifying the amount when filling out the declaration. Many taxpayers do not adjust deductions when resubmitting, resulting in major errors.

Be sure to double-check and recalculate the total deduction amounts. This rule is regulated by Article 181 of the Tax Code of the Russian Federation. If a taxpayer ignores this rule, he becomes a violator, which may entail large penalties . By the way, if according to the new (sophisticated version) of the declaration the tax amount has increased, it is recommended to pay the difference and attach the payment receipt (copy) to the main document.

Features of filling out the document

When preparing tax returns, you should know and use the rules and regulations adopted by law. In particular, they relate to the features of filling out the document. The main nuances include:

- Entering basic data. The 3-NDFL tax return consists of many empty boxes. They all require filling out. A person filling out this form for the first time may be confused, but in practice, filling out the document is not a difficult task. All the necessary information is simply copied from existing documents that must be attached to the 3-NDFL certificate.

- Requirements for registration. Here, too, everything is quite simple: you should enter data (texts, numbers) carefully and without errors. You can use a pen with blue or black ink. It is better to avoid typos or corrections. All amounts required to be filled out should be indicated in Russian rubles, and kopecks should also be noted (if any).

- Registration of details. It is worth making sure that each page of the declaration you fill out has a separate number in order. It is necessary to indicate the payer’s TIN, initials, completion date for filling out the document and personal signature. Also, the declaration must have up to 3 barcodes on each page.

What does a tax return form look like?