Purpose of auxiliary production process

In fairly large companies and enterprises, auxiliary production is created, the task of which is to provide everything necessary, for example, resources, tools or work, to the main production process. These subsidiary units may also sell manufactured products and services to third parties.

The auxiliary production process is not directly involved in the creation of the key production product. However, its presence is necessary in order to maintain and ensure the uninterrupted process of manufacturing products and goods.

Thus, the organization of work of auxiliary structural units directly depends on the volume of work of the key unit that produces the final product, and the existing potential for providing services to third parties. The stability and rhythm of the enterprise as a whole will depend on how clearly the auxiliary process is organized. In this situation, the work plan of the designated division provides for the calculation of the volume of output, the need for inventories, labor and the cost of manufactured goods.

If we talk about the structure of the auxiliary part of the production process, then it includes the following elements:

- subsidiary farms, which include energy, repair and mechanical and other structural units, depending on the specifics of the enterprise’s activities;

- servicing facilities in key workshops, which should include transport and storage facilities.

All employees of these departments are listed as support workers.

Results

Postings in the format Debit 23 Credit 23 can be used to:

- reflect the transfer of products (services) of one auxiliary production to another auxiliary production;

- make adjustments in terms of the nomenclature of auxiliary production, for example, when identifying mis-grading.

The main posting for disposal from account 23 is Dt 20 Kt 23 - when the product of auxiliary production is sent to the main one.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Meaning of 23 accounts

Position 23 in the Chart of Accounts, known as “Auxiliary Production”, is intended to summarize information about the costs of departments that are considered non-core.

If we consider in more detail, it should be said that this account is used to reflect the expenses of those departments that provide:

- transport service;

- OS repair work;

- production of spare parts, tools, building structures;

- construction of temporary structures;

- canning, salting or drying agricultural products.

The debit part of the account should reflect direct costs that are directly related to the production of products, as well as indirect costs that occur due to the need to manage and maintain the work of auxiliary structures, as well as losses due to defects.

In the credit part of the invoice it is necessary to show the actual cost of the finished product. All these amounts should be written off to the debit side of such accounts as main production (20), sales (90), and release of goods (40).

Features of accounting policies

Accounting for this account is carried out in debit and credit directions; we will consider each of the points in more detail.

By debit

The debit of this account reflects direct expenditure areas for the manufacture of products, performance of work and provision of certain services. This also includes indirect costs that are interconnected with the management and maintenance of auxiliary production, and losses from defects.

As for indirect expenses, they are written off to account 23 from accounts 25, 26. Losses associated with defects are subject to write-off to account 23 from 28.

By loan

Within this area, the amounts associated with the actual cost of certified production products are reflected. These amounts can be written off from the position in question in the following lines:

- 20 – production process in case of product release according to the main process;

- 29 – service farms and production;

- 90 – “Sales” account;

- 40 – production of products, services, works.

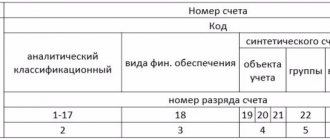

At the end of the month, there may be a balance in the area under consideration; it characterizes the cost of the unfinished production process. Maintaining analytical records in this area is carried out according to the main types and types of production.

Corresponding accounts

As for correspondence with other accounts, in the debit part these could be:

- depreciation charges (02);

- NMA (04);

- depreciation calculation for intangible assets (05);

- materials (10);

- settlements with suppliers and contractors (60);

- other expenses and income (91).

Speaking about the combination with accounts on the credit side, here it is worth highlighting:

- installation equipment (07);

- contribution to non-current assets (08);

- key production (20);

- manufacturing defects (28);

- finished products (43).

Accounting accounts for accounting of finished products

Information about manufactured products is stored in account 43 “Finished products”. This account is used by manufacturing enterprises that independently create products. In this case, the cost or complexity of the product does not play a role.

Finished products for one company may be raw materials for another. For example, for a flour mill, flour is a finished product. But for a gingerbread factory it is raw material.

Important! Trade enterprises do not use account 43. To account for goods for resale, they use account 41 “Goods”.

Basic postings

In practice, the following standard accounting entries are used to reflect the costs of auxiliary divisions of the enterprise:

1) Dt 23

Kt 02.01, 05 – accrual of depreciation of fixed assets and intangible assets used in the main workshops;

2) Dt 23

Kt 10.01 and 43 – release from warehouses of materials and finished products to utility shops;

3) Dt 23

Kt 97.21 – write-off of part of deferred costs for the reporting period;

4) Dt 23

Kt 60.01 and 76.05 – involvement of third parties to carry out work required by auxiliary workshops;

5) Dt 23

Kt 70 and 69 – payroll for employees of non-core departments;

6) Dt 10.01

Kt 23 - accounting for materials manufactured in auxiliary workshops or returned by them;

7) Dt 90.02

Kt 23 – write-off of the cost of goods in subsidiary workshops that were sold to third parties;

Dt 40

Kt 23 – actual cost of finished products of auxiliary departments.

Finished products in the balance sheet

In the balance sheet, the balance of the state enterprise at the end of the period is recorded on line 1210 “Inventories” at actual or planned cost.

The organization independently determines the level of detail of this line. For example, you can separately highlight the cost of raw materials, finished goods and work in progress if the company recognizes such information as significant.

For accounting of finished products and inventories in general, we recommend the web service Kontur.Accounting. The program will suggest the correct transactions and help you register the GP in accounting. We give all newbies a free trial period of 14 days.

Cases from practice

In order to have a clearer idea of how accounting is maintained for auxiliary departments, let's look at one of the practical cases.

Let's imagine that there is a certain enterprise that produces bakery products. On the balance sheet of this enterprise there is a workshop engaged in the maintenance of production equipment. During the reporting period, employees of the designated workshop carried out maintenance work on the equipment of another bakery. In accordance with the terms of the signed agreement, the cost of technical work is 157,300 rubles, the amount of VAT is 28,314 rubles.

The total costs incurred by the workshop in executing this order amounted to 76,050 rubles, including:

- wages of employees - 58,900 rubles;

- insurance premiums for accrued wages - 13,438 rubles;

- accrued depreciation on repair equipment - 3,712 rubles.

As a result, the accounting records for completed business transactions look like this:

1) Dt 23

Kt 10, 70 and 69 – 76,050 rubles, workshop costs incurred as part of the order;

2) Dt 62

Kt 90.1 – 157,300 rubles, revenue received for services rendered;

3) Dt 90.2

Kt 23 - 76,050 rubles, workshop costs when fulfilling the order;

4) Dt 90.3

Kt 68 – 28,314 rubles, accrued tax amount;

5) Dt 90.9

Kt 99 – 52,936 rubles, accounting for profit received.

Posting Debit 23 Credit 23

Posting Debit 23 Credit 23 is most often used in situations where one auxiliary unit transfers its products or provides services to another auxiliary unit. Thus, the entry Debit 23 Credit 23 is made in the context of analytics for various auxiliary productions.

Example

The flour mill has:

- own fleet of special vehicles;

- own sorting and loading shop for finished products;

- workshop for the production of equipment and tools;

- repair shop.

According to the accounting regulations of the enterprise, the inventory used in the main production and repair work are accounted for on account 20, and the costs of loading and delivering finished products to customers using their own transport are accounted for on account 44 “Sales expenses”.

1. The repair shop performed work on repairing the equipment of the loading shop in the amount of 100,000 rubles. In this case, equipment and tools from our own workshop were used in the amount of 20,000 rubles.

2. The repair shop also repaired the elevator equipment in the amount of RUB 500,000. In this case, the products of our own inventory and tool shop were used for 130,000 rubles.

In order to correctly distribute the amounts that form the actual value of the main production on account 20, sales expenses on account 44, as well as the balance of accounts of auxiliary production, it is necessary to make transactions of the type Debit 23 Credit 23 :

- Dt 23 (repair shop) Kt 23 (equipment and tools workshop) - 150,000 rubles. (20,000 + 130,000). The workshop's products were transferred to the repair shop.

- Dt 23 (loading shop) Kt 23 (repair shop) - 100,000 rubles. Repairs were carried out in the loading shop using our own repair shop.

- Dt 20 Kt 23 (repair shop) - 500,000 rubles. Current repairs of main production equipment were carried out using our own repair shop.

- Dt 44 Kt 23 (loading shop) - 100,000 rubles. The cost of routine repairs of equipment in the loading department is included in sales expenses.

In addition, the entry Debit 23 Credit 23 can be used to adjust data on the nomenclature and reflect the identified misgrading.

Example (continued)

Let's introduce additional conditions.

On the last day of the month, an inventory was taken in the equipment and tools workshop. The results revealed:

- excess items related to inventory - 4,000 rubles;

- shortage of nomenclature related to tools - 4,000 rubles.

The study of documents for internal movement showed that when releasing the production of the workshop to the repair shop, errors were made: the item items of inventory and tools worth 4,000 rubles were reflected with re-grading.

To eliminate inaccuracies, the accounting department will make a posting in the format Debit 23 Credit 23 by item: Dt 23 (tools) Kt 23 (inventory) - 4,000 rubles.