Conceptual apparatus

Before proceeding directly to carrying out repair work, the institution should determine what type of work being performed will be: major (current) repairs or reconstruction. Indeed, in case of incorrect qualification of work and payment for the wrong type of expenses, the institution may be held liable for misuse of funds.

To do this, it is necessary to refer to the regulations governing activities in the field of construction, since the current accounting and tax legislation does not contain definitions of these concepts.

In accordance with clause 3.8 of MDS 81-35.2004, major repairs of buildings and structures include work on the restoration or replacement of individual parts of buildings (structures) or entire structures, parts and engineering equipment due to their physical wear and destruction with more durable and economical, improving their performance.

For reference: preventive (current) repairs consist of systematically and timely work to prevent wear and tear on structures, finishes, and engineering equipment, as well as work to eliminate minor damage and malfunctions.

In the course of analyzing the above definitions, we can conclude that during routine repairs only minor work can be carried out, therefore, all major work must be performed during major repairs. For example, partial repair of the roof, taking into account the insignificance of material and labor costs, will be considered a current repair, and a complete change or replacement of all types of roofing will be a major one.

According to clause 3.4 of MDS 81-35.2004, during the reconstruction (reconstruction) of existing workshops of the enterprise and facilities of the main, auxiliary and service purposes, as a rule, without expanding the existing buildings and structures of the main purpose associated with improving production and increasing its technical and economic level and carried out Under a comprehensive project to modernize an enterprise in order to increase production capacity, improve quality and change the range of products, mainly without increasing the number of employees while simultaneously improving their working conditions and environmental protection, the following activities can be carried out:

- expansion of individual buildings and structures for main, auxiliary and service purposes in cases where new high-performance and more technically advanced equipment cannot be placed in existing buildings;

- construction of new and expansion of existing workshops and auxiliary and service facilities;

- construction on the territory of an existing enterprise of new buildings and structures of the same purpose to replace those being liquidated, the further operation of which, due to technical and economic conditions, is considered inappropriate.

Thus, if an institution plans to replace the roof covering, this will be recognized as a repair (current or major), and if it wants to equip offices in the attic or build an attic on the roof, then this work will already be a reconstruction.

Note that similar norms are in the Town Planning Code.

The list of main works carried out during current and major repairs in relation to social and cultural facilities is given in VSN 58-88(r), and in relation to production facilities - in MDS 13-14.2000.

In accordance with clause 1.1 of VSN 58-88(r), this provision applies to municipal and socio-cultural facilities, regardless of the form of ownership. According to Appendix B to SP 118.13330.2012 “Public buildings and structures. Updated version of SNiP 06/31/2009”, approved by Order of the Ministry of Regional Development of the Russian Federation dated December 29, 2011 No. 635/10, public buildings and premises include:

- buildings and structures for facilities serving the population;

- buildings of facilities serving society and the state (in particular, court buildings and prosecutor's offices, as well as law enforcement organizations (police, customs)).

Please note: the list of additional work carried out during major repairs is given in Appendix 9 to VSN 58-88(r).

According to clause 5.1 of VSN 58-88(r), major repairs must include troubleshooting of all worn-out elements, restoration or replacement (except for the complete replacement of stone and concrete foundations, load-bearing walls and frames) with more durable and economical ones that improve the performance of the buildings being repaired . At the same time, economically feasible modernization of a building or facility can be carried out: improving the layout, increasing the quantity and quality of services, equipping with missing types of engineering equipment, and improving the surrounding area.

When reconstructing buildings (facilities), based on the existing urban planning conditions and current design standards, in addition to the work performed during major repairs, the following can be carried out:

- changing the layout of premises, erecting superstructures, extensions, and, if necessary justification is available, their partial dismantling;

- increasing the level of engineering equipment, including the reconstruction of external networks (except the main ones);

- improving the architectural expressiveness of buildings (objects), as well as landscaping the surrounding areas.

When reconstructing municipal and socio-cultural facilities, it may be possible to envisage the expansion of existing and construction of new buildings and structures for auxiliary and service purposes, as well as the construction of buildings and structures for the main purpose included in the complex of the facility, to replace those being liquidated.

The list of main works performed during routine repairs is presented in Appendix 4 to VSN 58-88(r).

Consumption standards for building materials

The current system of pricing and estimate regulation in construction includes building codes and regulations: Part 4 of SNiP “Estimate Norms and Rules” and other estimate normative documents.

Estimated standards are a generalized name for a set of estimated standards, rates and prices, combined into separate collections. They are used to determine the estimated cost of construction and reconstruction of facilities.

An estimated norm is a set of resources (labor costs of workers, operating time of construction machines, requirements for materials, products and structures, etc.) established on the accepted meter for construction, installation or other work. The main function of estimate standards is to determine the standard amount of resources required to complete a particular job.

Estimated standards are based on the assumption that the work is performed under normal conditions, not complicated by external factors. If the work is carried out in special conditions (crowded conditions, gas pollution, near operating equipment, in areas with specific factors), then the coefficients given in the general provisions of the collections of standards are applied to the estimated standards.

The following estimate standards exist:

- federal (all-republican);

- departmental (industry);

- regional (local);

- user's own regulatory framework.

The cost of construction in estimates can be determined by various methods.

- Resource method. It consists in the fact that all costs are summed up in physical terms at current prices. In this case, indicators such as labor intensity (person-hours), time of use of construction machines (machine/hour), consumption of materials and components (pieces, sq. m, etc.) are used.

To determine these indicators, an organization can use its own data or use one of the collections of standard indicators, as well as the federal collection of estimated standards and prices for the operation of construction machines and vehicles.

- Basis-index method. According to this method, the cost of construction is determined as follows: the cost of enlarged types of construction products in basic prices is added up, and the result obtained is multiplied by the indices for converting basic prices into current ones.

- Resource-index method: the cost of construction is determined by the resource method in basic prices (as of January 1, 2000) and multiplied by indices that bring these prices to today's level.

- Basic compensation method: the cost of work and expenses at the basic price level and additional costs associated with changes in prices and tariffs for construction resources (material, technical, energy, labor, etc.) are added up.

- Data on previously constructed or designed objects is used.

Example 1 . Stroitel LLC entered into an agreement to perform repair work for Renata JSC.

In accordance with the agreement, Stroitel LLC must paint the walls in the workshop of Renata JSC with water-based paint. Previously, these walls were painted with oil paint.

The area of the walls to be painted is 600 square meters.

Justification of the work carried out

Particular attention should be paid to the validity of repair work. According to paragraph 6 of Art. 55.24 of the Civil Code of the Russian Federation, in order to ensure the safety of buildings and structures during their operation, institutions must provide maintenance of buildings, structures, their operational control and routine repairs.

Operational control over the technical condition of buildings and structures is carried out during the period of their operation through periodic inspections, control checks and (or) monitoring of the condition of foundations, building structures, engineering support systems and engineering support networks in order to assess the state of structural and other reliability characteristics and safety of buildings, structures, systems and networks of engineering support and compliance of these characteristics with the requirements of technical regulations and design documentation.

For reference: based on clause 3.2 of VSN 58-88(r), inspections are divided into scheduled and unscheduled. In turn, scheduled inspections are divided into general and partial.

During general inspections, the technical condition of the building or object as a whole, its systems and external improvements is monitored; during partial inspections, the technical condition of individual premises structures and elements of external improvements is monitored. Unscheduled inspections should be carried out after earthquakes, mudflows, rainstorms, hurricane winds, heavy snowfalls, floods and other natural phenomena that can cause damage to individual elements of buildings and objects, after accidents in heat, water, power supply systems and when deformations are identified grounds.

Please note: General inspections should be carried out twice a year (spring and autumn).

To carry out these inspections, the institution should create a commission, and their results should be reflected in documents recording the technical condition of the building or facility (technical condition registers, special cards, etc.). These documents must contain an assessment of the technical condition of the building or object and its elements, identified faults, their locations, the reasons that caused these faults, as well as information about the repair work performed during inspections. Generalized information about the condition of a building or facility must be reflected annually in its technical passport.

The basis for carrying out repair work should be property inspection reports and defective statements (defective statements) (Letter of the Ministry of Finance of the Russian Federation dated December 4, 2008 No. 03-03-06/4/94). In order to conduct inspections in an institution, it is necessary to form a commission or appoint responsible persons. It is advisable to show the following information in the defective statement:

- identification data of the fixed asset object (inventory number, brief description of the object, its location, etc.);

- identified defects and shortcomings;

- a list of necessary work to bring the fixed asset object into working condition;

- signatures of the commission members conducting the inspection.

At the same time, in our opinion, it is advisable to approve the forms of documents in the accounting policy of the institution. As an example, you can use a report on identified equipment defects, which is drawn up according to the OS-16 form, approved by Resolution of the State Statistics Committee of the Russian Federation dated January 21, 2003 No. 7.

Please note: the forms of these documents are not approved. This means that these documents can be drawn up in any form.

Repair work can be carried out either by the institution’s employees (as part of their performance of their official duties) or with the involvement of third-party organizations. Let us remind you that the involvement of a third-party organization must be carried out in accordance with the procedures provided for by federal laws dated 04/05/2013 No. 44-FZ “On the contract system in the field of procurement of goods, works, services to meet state and municipal needs” (hereinafter referred to as the Law on the Contract System ) and dated July 18, 2011 No. 223-FZ “On the procurement of goods, works, and services by certain types of legal entities.”

construction and installation work

The legislation of the Russian Federation does not provide a clear definition of the concept of “construction and installation works”. Following the provisions of Art. 11 of the Tax Code of the Russian Federation, the available explanations of officials and the conclusions of arbitration practice, work of a capital nature can be classified as construction and installation works if during them (Letter of the Ministry of Finance of the Russian Federation dated October 30, 2014 N 03-07-10/55074):

- new fixed assets are created, including real estate;

- the initial cost of objects in operation changes in the case of completion, additional equipment, reconstruction, modernization, technical re-equipment.

Details of what applies to construction and installation work and how VAT is calculated in this case

Design and permitting documentation

Once the institution has identified the deficiencies that must be eliminated, an estimate for repair work is drawn up and a government contract is concluded based on the procedures provided for in the Contract System Law. Let us recall that the construction contract must determine the composition and content of technical documentation, and must also stipulate which party must submit the relevant documentation and within what time frame.

The basis for determining the price of a contract for construction, reconstruction, major or current repairs of a capital construction project is design documentation (including the estimated cost of work), developed and approved in accordance with the legislation of the Russian Federation.

By virtue of Art. 48 of the Civil Code of the Russian Federation, design documentation is documentation containing materials in text form and in the form of maps (diagrams) and defining architectural, functional-technological, structural and engineering solutions to ensure the construction, reconstruction of capital construction projects, their parts, major repairs, if its implementation affects the structural and other characteristics of the reliability and safety of capital construction projects.

The composition of the design documentation is given in Part 12 of Art. 48 of the Civil Code of the Russian Federation and Decree of the Government of the Russian Federation dated February 16, 2008 No. 87 “On the composition of sections of project documentation and requirements for their content.” In the case of a major overhaul of capital construction projects, separate sections of design documentation are prepared based on the instructions of the developer or customer, depending on the content of the work performed during the overhaul of capital construction projects.

Please note: it should be taken into account that in the case of routine repairs, only an estimate justifying the cost of the work is sufficient.

In accordance with Art. 49 of the Civil Code of the Russian Federation, design documentation of capital construction projects is subject to state examination. An examination of design documentation is not carried out if construction or reconstruction does not require obtaining a construction permit, as well as when carrying out this examination in relation to the design documentation of capital construction projects that has received a positive conclusion from the state examination and is reused, or modification of this design documentation is not affecting the structural and other characteristics of the reliability and safety of objects.

After receiving a positive conclusion from the state examination, the project documentation is approved by the developer or customer.

According to paragraph 2 of Art. 51 of the Civil Code of the Russian Federation, construction and reconstruction of capital construction projects are carried out on the basis of a construction permit.

How to write off expenses in tax accounting

The cost of materials that are used to carry out work is classified as material costs (clause 1, clause 1, article 254 of the Tax Code of the Russian Federation). At the same time, no restrictions on the amount of consumable materials (in accordance with established norms, regulations, etc.) are established in this article of the Tax Code of the Russian Federation. The main thing is that expenses must be documented and justified. This follows from clause 1 of Article 252 of the Tax Code of the Russian Federation.

Thus, in tax accounting, the entire cost of the materials consumed is written off as expenses, and not what was included in the estimate. At the same time, the accounting policy of the construction organization must specify the procedure for determining the amount of material costs when writing off raw materials and materials used in the performance of work. In other words, it is necessary to choose one of the methods for assessing materials provided for in paragraph 8 of Article 254 of the Tax Code of the Russian Federation:

- valuation method based on the cost of a unit of inventory;

- average cost valuation method;

- valuation method based on the cost of first-in-time acquisitions (FIFO);

- valuation method based on the cost of recent acquisitions (LIFO).

Example 4 . Let's return to the conditions of examples 2 and 3, assuming that for both accounting and tax purposes, Stroitel LLC evaluates the materials used in performing the work at average cost.

In this case, the taxable profit in both examples is the same as the accounting profit.

R.P.Nichuk

Auditor

Registration of completed work

Let us remind you that payment for work performed must be made in the manner established by the concluded contract. It should be remembered that, according to Part 3 of Art. 94 of the Law on the Contract System, in order to verify the results provided by the supplier (contractor, performer) provided by the contract, in terms of their compliance with the terms of the contract, the institution is obliged to conduct an examination. The examination of the results provided for by the contract can be carried out by the institution on its own, or experts and expert organizations can be involved in its implementation on the basis of contracts concluded in accordance with the Law on the Contract System. In the case of repair work, the examination should be carried out in the form of control measurements of the work performed.

Please note: in the event that the documents do not fully contain the above information about work in the past, only the information available in the documents is entered into the duplicate work book.

The essence of this check is to compare the actual volumes of work performed in kind (at the construction or repair site) with similar volumes specified in the acts in the KS-2 form.

The initial documents for carrying out control measurements are:

- certificates of work performed in the KS-2 form, which reflect the types and cost of work performed;

- acts for hidden work.

According to Part 7 of Art. 94 of the Law on the Contract System, acceptance of the results of a separate stage of contract execution, as well as goods delivered, work performed or services rendered, is carried out in the manner and within the time frame established by the contract, and is documented in an acceptance document, which is signed by the customer (in the case of creating an acceptance commission, it is signed by all members of the acceptance committee and approved by the customer), or the customer within the same time frame sends to the supplier (contractor, performer) in writing a reasoned refusal to sign such a document.

In practice, there are cases when it is necessary to carry out additional work that was not originally envisaged. It should be remembered that when concluding and executing a contract, changing its terms is not allowed, except in cases provided for in Art. 34 and 95 of the Contract System Law.

In accordance with paragraphs. “b” clause 1 part 1 art. 95 of the Law on the Contract System, a change in the essential terms of the contract during its execution is possible if, at the customer’s proposal, the quantity of goods, volume of work or services provided for in the contract is increased by no more than 10% or the quantity of goods supplied, the volume of work performed or services provided is reduced by no more than 10%. than 10%. In this case, by agreement of the parties, it is allowed to change, taking into account the provisions of the budgetary legislation of the Russian Federation, the contract price in proportion to the additional quantity of goods, additional volume of work or service based on the price of a unit of goods, work or service established in the contract, but not more than by 10% of the contract price.

When reducing the quantity of goods, volume of work or service provided for in the contract, the parties to the contract are obliged to reduce its price based on the unit price of the goods, work or service. The price of a unit of additionally supplied goods or the price of a unit of goods in case of a decrease in the quantity of supplied goods provided for in the contract should be determined as the quotient of dividing the original contract price by the quantity of such goods established in the contract.

So, if the customer needs to increase or decrease the scope of work stipulated by the contract (if such a possibility was established by the procurement documentation), during the execution of the contract, it is possible to increase or decrease the scope of work for certain items of the local estimate by no more than 10% based on the price established in the contract units of work volume. In this case, the total cost of the estimate should be changed in proportion to the additional volume of work, but not more than by 10%.

As for the need to perform work not provided for in the contract, to carry it out the institution needs to carry out a new procurement using competitive methods for determining the supplier (contractor, performer) established by the Law on the Contract System.

To reflect transactions in the accounting (budget) accounting of fixed assets transferred (received) for repairs, an acceptance certificate for repaired, reconstructed and modernized fixed assets (form 0504103) (hereinafter referred to as the act (form 0504103)) should be used. .

The act (f. 0504103) contains information about the timing of work under the contract and, in fact, information about the fixed assets and the costs of repair, reconstruction and (or) modernization work.

The first copy of the act remains in the institution, the second copy is transferred to the organization that carried out the repairs. The act is signed by members of the acceptance committee or a person authorized to accept fixed assets, as well as a representative of the organization (structural unit) that carried out the repair or reconstruction. It is approved by the head of the organization or a person authorized by him and submitted to the accounting department.

Please note: if the repair is carried out by a third party, the report is drawn up in two copies.

If repair work is carried out by employees of the institution in accordance with their job responsibilities, the costs are documented in the following unified forms of primary documentation:

- consumption of materials - act on write-off of inventories (f. 0504230);

- labor costs - time sheets (f. 0504421), payroll and pay slips (f. 0504401, 0504403).

The result of repair work on an object of fixed assets that does not change its value, including the replacement of elements in a complex object of fixed assets (in a complex of structurally articulated objects that constitute a single whole), is subject to reflection in the accounting register - the inventory card of the object of non-financial assets (f. 0504031) of the corresponding fixed asset item by making entries about the changes made without being reflected in the accounting accounts (clause 27 of Instruction No. 157n).

The write-off of inventories used in the process of work, acquired by the customer independently and transferred to the performer (contractor), is formalized by a write-off act of inventories, which is drawn up on the basis of the list of materials used during the work, indicated in the acceptance certificate for repaired, reconstructed, modernized fixed assets. .

* * *

In conclusion, we note once again that during repair work, worn-out parts and parts are replaced with new ones, while the functions of the fixed asset do not change, that is, such a replacement does not expand or increase the capabilities of the fixed asset object and does not improve its technical characteristics. During the reconstruction, the initially adopted standard performance indicators are improved (increased). The costs of reconstructing a fixed asset after its completion increase the initial cost of such an object.

What other documents, besides the act (f. 0504230), are needed to confirm the write-off of building materials in the accounting records for routine repairs of the premises using an economic method?

March 22, 2018

Having considered the issue, we came to the following conclusion: The direct write-off of building materials used for the purpose of repairing premises in an economic way is formalized by the Act on the write-off of inventories (f. 0504230), which serves as the basis for reflecting in the records of the institution the disposal from the accounts of inventories. The current legislation does not provide for other mandatory unified forms of primary documents that serve as the basis for writing off inventories, including construction materials, from balance sheet accounts.

Rationale for the conclusion: The forms of primary accounting documents and accounting registers that are mandatory for use by public sector institutions are established in accordance with budget legislation (Part 4, Article 9 of the Federal Law of December 6, 2011 N 402-FZ, hereinafter referred to as Law N 402-FZ, p. 28 of the Federal Standard “Conceptual Fundamentals of Accounting and Reporting of Public Sector Organizations”, approved by Order of the Ministry of Finance of Russia dated December 31, 2016 N 256n, hereinafter referred to as the GHS “Conceptual Fundamentals”). Taking into account the provisions of the Instruction approved by Order of the Ministry of Finance of Russia dated December 1, 2010 N 157n (hereinafter referred to as Instruction N 157n), clause 25 of the GHS “Conceptual Framework”, public sector institutions are required to use unified forms of primary accounting documents and accounting registers: - approved by order of the Ministry of Finance Russia dated March 30, 2015 N 52n (hereinafter referred to as Order N 52n); - established by legal acts of authorized bodies on the basis of federal laws. In other cases, forms developed by the budgetary institution independently may be used (the procedure for their application and completion must be provided for in the accounting policy). The main point in the most efficient use of resources will be the division of the entire range of material reserves used in a government agency into two large groups, as well as the widespread use of such a tool as rationing of material consumption. Thus, material reserves can be divided into: - consumables (office supplies; household materials; food products; construction and fuel and lubricants, etc.); — non-consumable (clothes and shoes; bed linen and bedding; computer components, including keyboards, mouse-type manipulators; gas-powered saws, etc.). When determining in the accounting policy the procedure for writing off various material assets, it is advisable for a government agency to proceed primarily from how important it is to ensure control over the safety of a specific group (type) of material assets and how significant they are. It should be understood that the current regulatory legal acts do not establish clear boundaries between: - consumable and non-consumable inventories; - property that is subject to write-off as a direct expense upon release from storage places, and valuables that can be written off from the balance sheet only after additional documents are prepared. Regarding the situation under consideration, we note the following. In order to avoid claims and disagreements on the part of the inspection authorities, the need for repairs in the premises must be documented. Such a document may be a report of identified defects and (or) a defect sheet. Since Order No. 52n does not establish a unified form for such a document, you can use a self-developed form indicating the faults of the object and proposals for their elimination. At the same time, it is advisable for the public sector institution to draw up an estimate for the repair work, which determines the volume and criteria of non-financial assets necessary for the repair, as well as other expected costs. The issuance of construction materials to employees of the institution for the purpose of carrying out routine repairs of the premises in an economic way, including the return of remaining materials to the warehouse, is formalized by the Request-invoice (f. 0504204) and (or) the Statement for the issuance of material assets for the needs of the institution (f. 0504210). In turn, the write-off of inventories used for repairs, in accordance with the direct norms of Order No. 52n, is formalized by the Act on the write-off of inventories (f. 0504230), which serves as the basis for reflecting in the records of the institution the disposal from the accounts of inventories. The current legislation does not provide for other mandatory unified forms of primary documents that serve as the basis for writing off inventories, including construction materials, from balance sheet accounts. Such documents can be developed by the institution independently containing the mandatory details listed in Part 2 of Art. 9 of Law No. 402-FZ, clause 25 of the GHS “Conceptual Framework”, clause 7 of Instruction No. 157n, and are enshrined within the framework of the formation of accounting policies. However, they do not cancel the execution of the Act on the write-off of inventories (f. 0504230), but can only serve as an addition to it for the purpose of disclosing information about written-off inventories. After completion of the repair work, the objects repaired using economic methods are accepted for accounting in the generally established manner on the basis of the relevant primary documents, in particular the Act on the acceptance and transfer of non-financial assets (f. 0504101), the Act on the acceptance and delivery of repaired, reconstructed and modernized fixed assets ( f. 0504103) (see, in particular, the decision of the Arbitration Court of the Krasnodar Territory dated 01.09.2017 in case No. A32-27793/2017). Thus, the direct write-off of construction materials used for the purpose of repairing the premises is formalized by the Act on the write-off of inventories (f. 0504230), which serves as the basis for recording in the records of the institution the disposal from the accounts of inventories. However, to justify the repairs, as well as the volume of costs incurred, including written-off material assets, it is advisable for the institution to draw up the relevant documents developed by the institution independently and fixed as part of the formation of its accounting policy. Such documents may be a report of identified defects and (or) a defect sheet, as well as an estimate for repair work.

Answer prepared by: Expert of the Legal Consulting Service GARANT Olga Emelyanova

Response quality control: Reviewer of the Legal Consulting Service GARANT Sukhoverkhova Antonina

How to write off expenses in accounting

As stated in paragraph 11 of the Accounting Regulations “Accounting for Agreements (Contracts) for Capital Construction” PBU 2/94, approved by Order of the Ministry of Finance of Russia dated December 20, 1994 N 167, the contractor’s costs consist of all expenses associated with the performance of contract work under contract. In other words, in accounting, expenses must include the entire cost of materials consumed during construction or repairs (even if this expense exceeds the norm included in the estimate). Materials are written off in a similar way when the developer performs the work on his own (clause 8 of PBU 2/94).

Example 2 . Let's return to the conditions of example 1.

Let us assume that, in fact, when performing work on painting walls in the workshop of ZAO Renata, the following expenses were incurred:

- materials were spent in the amount of 30,000 rubles;

- wages were accrued to employees (including unified social tax, contributions to the Pension Fund and accidents) in the amount of 10,101 rubles;

- depreciation of fixed assets was accrued - 50 rubles;

- General business expenses attributable to this order were written off - 4895 rubles. (in accordance with the accounting policy, account 26 is closed to account 20).

In the accounting of Stroitel LLC, the accountant will make the following entries:

Debit 20 Credit 10

- 30,000 rub. — consumed materials are written off;

Debit 20 Credit 70 (69)

- RUB 10,101 — wages to employees have been accrued (taking into account the unified social tax, insurance contributions to the Pension Fund of the Russian Federation and from industrial accidents);

Debit 20 Credit 02

- 50 rub. — depreciation of fixed assets used during repairs was calculated;

Debit 20 Credit 26

- 4895 rub. — general business expenses attributable to this order are written off;

Debit 62 Credit 90 subaccount “Revenue”

- 55,000 rub. — revenue from repair work for Renata CJSC is reflected;

Debit 90 subaccount “Cost of sales” Credit 20

- RUB 45,046 (30,000 + 10,101 + 50 + 4895) - expenses for repair work for Renata CJSC were written off;

Debit 90 subaccount “Profit/loss from sales” Credit 99

- 9954 rub. (55,000 - 45,046) - profit from repair work for Renata CJSC is reflected.

If an organization performs work using materials provided by the customer, then the materials received from the customer should be considered as customer-supplied raw materials and reflected in off-balance sheet account 003 “Materials accepted for processing.”

Example 3 . Let's change the conditions of examples 1 and 2. Let's assume that water-based paint costs 11,076 rubles. was provided by the customer - ZAO Renata. Other materials for a total estimated amount of 18,091.4 rubles. (29,167.4 - 11,076.0) Stroitel LLC acquired independently. In fact, materials worth 18,500 rubles were purchased. All these materials were used to paint the walls. The remaining costs are the same as in example 2.

Since part of the work was done from the customer’s material, the cost of the work was not 55,000 rubles, but 43,924 rubles. (55,000 - 11,076).

In this case, the accountant of Stroitel LLC must record the transactions as follows:

Debit 003

- RUB 11,076 — water-based paint was received from JSC Renata;

Debit 20 Credit 10

- 18,500 rub. — consumed materials are written off (except for water-based paint provided by the customer);

Credit 003

- RUB 11,076 — water-based paint used during the work was written off;

Debit 20 Credit 70 (69)

- RUB 10,101 — wages to employees have been accrued (taking into account the unified social tax, insurance contributions to the Pension Fund of the Russian Federation and from industrial accidents);

Debit 20 Credit 02

- 50 rub. — depreciation of fixed assets used during repairs was calculated;

Debit 20 Credit 26

- 4895 rub. — general business expenses attributable to this order are written off;

Debit 62 Credit 90 subaccount “Revenue”

- RUB 43,924 — revenue from repair work for Renata CJSC is reflected;

Debit 90 subaccount “Cost of sales” Credit 20

- RUB 33,546 (18 500 + 10 101 + 50 + 4895) - expenses for repair work for Renata CJSC were written off;

Debit 90 subaccount “Profit/loss from sales” Credit 99

- RUB 10,378 (43,924 - 33,546) - profit from repair work for Renata CJSC is reflected.

Material write-off act

Materials are a type of inventory. These include raw materials, basic and auxiliary materials, purchased semi-finished products and components, fuel, containers, spare parts, construction and other materials (clause 42 of the Guidelines, approved by Order of the Ministry of Finance dated December 28, 2001 No. 119n).

We talked about synthetic and analytical accounting of inventories (including materials) in our consultation. In this material we will tell you how to draw up an act for writing off materials and a sample of such an act will be given below.

What laws set limits on the write-off of building materials?

There is no firm rule in accounting laws according to which materials must be written off for production. However, paragraph 92 of the Order of the Ministry of Finance dated December 28, 2001 No. 119n states that materials must be released from the warehouse in accordance with the standards of the production program. This rule assumes that write-offs cannot be uncontrolled. The volumes during the operation must comply with approved standards. There is also Article 252 of the Tax Code of the Russian Federation, according to which all expenses of an enterprise must be supported by documents. Spending must also be reasonable from an economic point of view.

The company independently approves consumption standards based on the following documents:

- SNiP 82-01-95. Here are the general rules.

- RDS 82-201-96. Here you can find answers to specific questions, as well as examples of calculations.

When approving standards, specific papers may also be used:

- GESN . The document specifies standards for specific types of construction.

- MDS . Here you can find recommendations for using GESN.

The basic volumes for write-off will depend on the construction project. For example, the concrete used in the construction of a residential or industrial building will vary. The standards regarding this aspect are given by GOST and SanPiN. Expert opinions may also apply.

The limits approved by the enterprise must be fixed in estimates and various internal documents. Documents are compiled by the department responsible for the technological process. After the papers are developed, the director of the company must approve them. Write-offs must be made in accordance with established standards. It is possible that the approved limit may be exceeded, but this situation should alert the manager. In particular, he will need to establish the reasons for exceeding the standards. For example, this could be defective materials or technological losses.

IMPORTANT! Writing off materials in excess of approved standards can only be done with the permission of the manager. On the primary documentation (invoice, act), a note is placed on the supply of building materials in excess of the limit and the reasons for such an operation. If the write-off is carried out without complying with these rules, it will be unlawful. Such actions can lead to distortion of costs and the entry of incorrect data in tax reporting and accounting.

What is meant by write-off of materials?

Methodological guidelines for accounting of inventories (approved by Order of the Ministry of Finance dated December 28, 2001 No. 119n) stipulate that materials are written off in the following cases (clause 124):

- materials have become unusable after expiration of storage period;

- materials are obsolete;

- when identifying shortages, thefts or damage to materials, including due to accidents, fires, and natural disasters.

However, in a broader sense, the write-off of materials also refers to their release into production and even the disposal of materials when they are sold. In other words, in all those cases when materials are written off from the organization’s accounting records, that is, reflected in the credit of account 10 “Materials” (Order of the Ministry of Finance dated October 31, 2000 No. 94n). For example, in correspondence with the debit of accounts 20 “Main production”, 91 “Other income and expenses”, 94 “Shortages and losses from damage to valuables”, etc.

Reconstruction

The definition of reconstruction is given in paragraph 14 of Art. 1 of the Town Planning Code of the Russian Federation, it includes:

- changing the parameters of the object (height, number of floors, area, volume), including superstructure, reconstruction, expansion of the object,

- replacement, restoration of load-bearing building structures of a capital construction project, with the exception of replacement of individual elements of these structures.

That is, reconstruction does not consist in maintaining the condition of the object, but in its reconstruction. Moreover, during reconstruction, the initial cost of an object may increase if its functional indicators have changed (clause 27 of PBU 6/01).

Read more about changing the initial cost of the OS in the following articles:

- Upgrading the OS with increasing SPI

- Upgrading the OS without increasing the SPI

When is an act for writing off materials needed?

The organization must document the write-off of materials with a primary accounting document (Part 1, Article 9 of Federal Law No. 402-FZ of December 6, 2011). The organization decides itself which form of document to use (Information of the Ministry of Finance No. PZ-10/2012). Usually, when materials are sold, a consignment note is drawn up in form No. TORG-12 (approved by Resolution of the State Statistics Committee of December 25, 1998 No. 132). We talked in more detail about this form in a separate consultation, where we also provided a sample for filling out the primary document. When materials are transferred from one structural unit (or MOL) to another, and even when writing off materials for production and other cases, the requirement of an invoice in form No. M-11 is used (approved by Resolution of the State Statistics Committee of October 30, 1997 No. 71a). We have provided a sample of how to fill out this form. To write off materials for production, for example, a limit-fence card in form No. M-8 is also used. As for the act of writing off materials, it can be used both in the above cases and, more often, in cases of writing off materials other than transfer to production or sale. For example, when writing off fuel and lubricants or office supplies.

List of requirements for materials and calculation of the cost of materials for the object and sections of the estimate

| N p/p | Material codes | Name of materials | Unit change | Quantity | Unit cost measured material, rub. | Total estimated cost, rub. |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 |

| 1 | 101-9844 | Water-based paints | kg | 71 x 6 = 426.00 | 26,00 | 11 076,00 |

| 2 | 101-0623 | Laundry soap | PC. | 5.1 x 6 = 30.60 | 2,80 | 85,68 |

| 3 | 101-0620 | Ground chalk | kg | 25.5 x 6 = 153.00 | 12,90 | 1 973,70 |

| 4 | 101-1712 | Putty | kg | 72 x 6 = 432.00 | 33,50 | 14 472,00 |

| 5 | 101-1916 | Sanding paper | sq. m | 1.6 x 6 = 9.60 | 45,00 | 432,00 |

| 6 | 101-0639 | Pumice | cube m | 0.0044 x 6 = 0.0264 | 6 000,00 | 158,40 |

| 7 | 101-1840 | Painting glue | kg | 4.02 x 6 = 24.12 | 40,20 | 969,62 |

| Total | 29 167,40 | |||||

We are developing an act for writing off materials (form)

For what purposes and what form of act for writing off materials the organization will use, it decides for itself and enshrines this in its Accounting Policy for accounting purposes. Since the act of writing off materials is the primary accounting document, it is necessary to ensure that it contains the following mandatory details (Part 2, Article 9 of Federal Law No. 402-FZ dated December 6, 2011):

- Title of the document;

- date of document preparation;

- name of the organization that compiled the document;

- content of the fact of economic life;

- the value of the natural and monetary measurement of a fact of economic life, indicating the units of measurement;

— the names of the positions of the persons who performed the transaction and are responsible for its execution;

- signatures of these persons indicating their last names and initials.

When writing off materials, the organization usually creates a special commission. We provided an example of an order to create such a commission in a separate article. If the same form of act is used for different types of write-off of materials, it is advisable to provide an indication of the reason for the write-off of materials in the write-off act.

An approximate form of an act for writing off materials (form) can be downloaded for free using the link below.

For the act of writing off materials, we will provide a sample of its completion for the case of writing off fuel and lubricants.

Prev. / Next A new form of the act for write-off of materials (sample form) can be found here. Only subscribers of the Main Ledger magazine can download document forms.

- I am a subscriber: electronic magazine printed magazine

- I'm not a subscriber, but I want to become one

- I want to download document forms for free and try all the features of a subscriber

Standardization procedure

Standardization includes the following stages:

- Analysis of the circumstances of construction work . Includes the selection of building materials, establishment of a unit of work, and planning of the construction execution process.

- Establishing limits for each material per unit of work . The types of standards are specified in RDS 82-201-96.

How to set consumption standards for detergents used for cleaning premises?

- Control over the implementation of limits . If limits are violated every now and then, it makes sense to adjust them. Norms must correspond to objective reality.

- N – write-off limit per unit of building material.

- ni is the spending limit for the work process.

- Ki is a coefficient that establishes a unit of work process in the total volume of building materials. It is found according to the following formula: elementary unit of an object/enlarged unit of building materials.

FOR YOUR INFORMATION! When normalizing, the concept of normal is often used. There are standards for standard forms of work that can be used to set limits.

Methods for establishing elementary norms

The limit per unit of building material is calculated based on consumption rates per unit of work process. The following formula is used for calculations:

It uses the following notations:

All the nuances of calculations are set out in paragraph 5 of RDS 82-201-96.

When approving basic standards per unit of work, the following methods are used:

- Production . Similar work is being observed at the construction site. The ratio of the volumes of operations performed with the materials consumed is measured. The production technique is usually used for building materials in which losses may be difficult to eliminate.

- Laboratory . It is assumed that measurements will be carried out under special circumstances. The technique is usually used when it is necessary to calculate the influence of a certain factor on the work.

- Calculation and analytical . The essence of the methodology is the implementation of theoretical calculations based on existing statistical data.

IMPORTANT! When taking measurements, you need to take several approaches. Their minimum number is 5.

Approval of material write-off limits

The following persons can approve standards:

- Head of VET.

- Chief engineer of the construction site.

- Director of the enterprise.

The standards are entered in separate columns of the act for disposal of building materials. Opposite them is information about the actual decommissioned objects. Based on the act, an order for the disposal of materials can be issued.

Do-it-yourself repairs

Open the document in your ConsultantPlus system: Selection of court decisions for 2021: Article 9 “Insurance risk, insured event” of the Law of the Russian Federation “On the organization of insurance business in the Russian Federation” (LLC legal) Guided by Article 9 of the Law of the Russian Federation of November 27, 1992 N 4015- 1 “On the organization of insurance business in the Russian Federation” and having established that during the restoration work the plaintiff independently replaced a faulty input on the insured property, while the amount of expenses incurred in connection with the performance of the work in an economic way was confirmed by the evidence presented in the case materials, the arbitration courts came to a reasonable conclusion that the costs claimed by the plaintiff for reimbursement were due to the occurrence of an insured event, the work performed was aimed at restorative repairs of the insured equipment in order to bring it to its original condition, and not change and/or improve it, and therefore the insurance compensation was legally collected under the insurance contract property of legal entities “from all risks”, since there is no evidence in the case materials that reliably confirms the inclusion in the cost of restoration of the insured property of expenses not related to the insured event.

conclusions

Based on the above, if your organization has carried out work aimed at eliminating malfunctions and maintaining the premises, then they will be considered repairs and do not increase its cost. According to clarifications from regulatory agencies, such work does not fall under construction and installation work.

If you independently carried out construction work, during which the initial cost of the premises changed, they are recognized as construction and installation works. Don’t forget to add VAT on the cost of such construction and installation work, which can be immediately deducted.

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge

Related publications

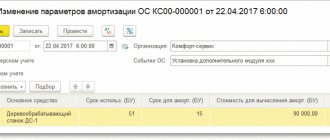

- Repair of a production facility, carried out using a self-help method in 1C Good evening, please tell me what documents you can use in 1C 8.3...

- Expenses for repairing equipment in BU and NU, if a repair reserve is not created in 1C Good afternoon. To repair the equipment, spare parts were purchased at a price of 52,000...

- Repair of premises, inseparable improvements or materials Good day. We rent premises. We entered into a contract for...

- How to arrange the installation of equipment using a household method Accounting for a KORP enterprise, edition 3.0 (3.0.63.22) how to arrange the installation of equipment...

Acceptance of services under the act

The customer must accept the services provided by the contractor. An algorithm has been established for this:

- The administrative document appoints an acceptance commission.

- A check is being carried out.

- An acceptance document is prepared in the absence of any comments; if the latter are found, then the deadline for their elimination can be indicated in the act.

- The certificate of completed work from the self-employed is signed by the members of the commission and approved by the chairman, after which payment is made. This condition should be discussed with the contractor.

Carrying out routine repairs in an economic way

To organize and manage work on capital construction and major repairs, enterprises have a deputy head of the enterprise for capital construction, to whom the capital construction department and construction and installation areas are subordinated. In most cases, capital construction, if it involves significant capital investments, is carried out by special construction organizations (contractors). In this case, the capital construction department issues an order to the contractor for work, monitors the progress of work and accepts completed construction projects. When carrying out work in an economic way, the capital construction department directly manages these works. The functions of the capital construction department are planning all capital construction and repair work, determining how to carry them out, ensuring the most efficient conduct of these works, as well as accounting and reporting on capital construction. [p.64]

All costs for completed major repairs of individual inventory items, regardless of the method of repair (economic or contract), are written off as a reduction in the depreciation fund intended for major repairs using the following entry [p.100]

When an enterprise carries out major repairs in an economic way, the amount of intangible costs to be transferred from a special loan account to a current account is reduced by the amount of depreciation deductions intended for this purpose. [p.395]

When carrying out construction using the economic method, construction usually uses subcontracted means of mechanization. They enter into agreements with mechanization departments (trusts). These organizations carry out certain types of construction and installation work using a mechanized method, allocate machines with service personnel to construction sites for certain periods, or rent out machines. They carry out installation and dismantling of machines, installation of rail and trackless tracks for them, transportation of machines from one construction site to another, carry out maintenance and repair of machines and other work. [p.427]

The lack of qualified personnel at some oil depots leads to a decrease in the quality and increased cost of repairs. Meanwhile, repairing process pipelines, tanks and power equipment in some cases is much more difficult to carry out than carrying out new construction. At the same time, the lack of the required number of various types of mechanisms leads to the use of a large amount of manual labor in the economic method of repair. Carrying out repairs and capital construction of small pipeline facilities and oil depots by specialized contracting organizations encounters difficulties due to the absence of such organizations in certain areas or their reluctance to carry out small-scale but complex repair work at existing oil depots. [p.213]

If costs are incurred at the expense of the tenant, then they are debited to the production cost accounts (25 General production expenses, 26 General business expenses, etc.) or to the debit of account 31 Deferred expenses (with the gradual inclusion of costs in production costs) from the credit of accounts 23 Auxiliary production (for the economic method of performing work) or 60 Settlements with suppliers and contractors (for the contract method of performing work). When carrying out major repairs of leased fixed assets at the expense of the lessor, repair costs are written off to the debit of the financial results account from the credit of account 76 Settlements with various debtors and creditors. [p.184]

The costs of major repairs carried out in an economic way (mechanical repair or repair and construction workshop) are taken into account on the debit of the synthetic active account 23 Auxiliary production in correspondence with the credit of accounts 05 Raw materials and supplies, 08 Spare parts, 70 Settlements with workers and employees, etc. The balance of account 23 is written off monthly to account 03 Major repairs. When repairs are carried out directly by the tank farm, all costs are written off to account 03. [p.98]

Carrying out repairs and reconstruction in an economic way [p.252]

Write-off of the actual cost of repairs carried out economically using account 23 is recorded by posting [p.89]

Write-off of the actual cost of repairs carried out economically using account 23 is recorded with the following posting: debit to account 89, credit to account 23. [p.253]

The final section of the report on the availability and movement of fixed assets and depreciation fund characterizes the planned and actual costs for current, major repairs and modernization of fixed assets. It indicates the costs of major repairs of buildings and structures, reconstruction of units and modernization of equipment. In the total amount of expenses, the costs of major repairs carried out in an economic way are highlighted, and its planned (estimated minus the specified reduction) cost is indicated. The total cost of unfinished capital repairs includes expenses that are not covered by sources of financing. In addition, this section contains reference information on the costs of equipment modernization, carried out through capital investments, and the amount of a given reduction in the cost of overhauls carried out in an economic way. [p.110]

At existing enterprises, a directorate for enterprises under construction is not created. The implementation of technical supervision functions and the customer’s responsibilities for capital construction are assigned to the capital construction departments. These departments carry out technical supervision of construction carried out by contract, but they are also entrusted with the execution of work on construction carried out by economic means, as well as major repairs of fixed assets. [p.651]

Work on each type of repair of fixed assets can be carried out in-house (with the organization’s own resources) or contracted (with the help of third-party organizations). In any case, the basis for their implementation are estimates - calculations of planned costs based on the volume of repair work to be performed. [p.315]

Synthetic accounting transactions transferred to GENSIS from the Fixed Asset Accounting subsystem contain operations on the receipt and disposal of fixed assets (ONO accounts, 0120, 0130), on the movement of depreciation of fixed assets (accounts 0210, 0220, 0230), on accounting for actual costs for current repairs and capital repairs of fixed assets carried out by an economic or contract method (accounts 0310, 0320, 0330, 0340), according to the movement of funds allocated for economic activities and assigned to enterprises as the authorized capital (account 8500), and others, which are based on standard correspondence . [p.138]

Source

How to reflect the costs of carrying out repairs on your own

Reflect these operations as current economic repairs.

1. For current expenses. The list of expenses under the simplified tax system has changed. We . Read the details in the journal Debit 10 Credit 60 - laminate was purchased Debit 26 Credit 10 - the write-off of laminate for the purposes of current repairs is reflected. 2. To formalize the fact of replacement, the following documents will be required: - a report of identified defects (or a defect sheet); - order from the manager about the need to replace the floor; — requirement-invoice for write-off of materials.

The cost of restoration work does not matter to distinguish between such concepts.

What matters here is the purpose for which such work is carried out (see.

table below): Type of work Purpose Repair Eliminate the malfunction that prevents the operation of the object, restore functionality. In this case, the properties of the object do not change ()* Modernization Change the technological and service purpose of the object, improve some of the properties of the fixed asset.

For example, in order to be able to work with it under increased loads () Reconstruction Rearrange the facility so that its capacity increases, the quality of products improves, or its range becomes wider () To determine whether the restoration of real estate is repair, reconstruction or modernization, be guided by the following documents:

This is stated in letters from the Russian Ministry of Finance, and.

Types of repairs Repairs are classified as follows. Depending on who is doing the work: it can be repaired on its own (self-employed) or with the involvement of a contractor.

And depending on the frequency and complexity, repairs can be current or major.

The first division is clear.

If the work is done poorly

If deficiencies are discovered in the services provided, the following steps must be taken:

- If any shortcomings or deviations from contractual obligations are noticed, you must inform the self-employed person about this.

- If the document does not indicate any defects, then the customer has no right to refer to it.

- When defects are discovered after the self-employed and the customer have signed the work completion certificate, the latter is deprived of the right to make claims or can try to resolve this issue in court.

Documentation of write-offs

All operations performed must be confirmed by primary documentation. The write-off of building materials is also accompanied by paperwork. The head of the enterprise has the right to independently determine the list of primary documentation drawn up upon disposal. However, in any case, all details must be indicated in the document. The list of necessary details is contained in Article 9 of Law No. 402 “On Accounting”.

Let's consider the documents that are usually drawn up when writing off building materials, as well as their standard forms:

- Requirement-invoice . Relevant if the enterprise has no restrictions on obtaining building materials. Compiled according to form No. M-11. The document can be used to record the movement of values within an enterprise.

- Limit fence card . Used when there are limits. Prepared according to form No. M-8.

- Invoice for the release of building materials to the side . It is used if the material is sent to a separate division of the enterprise. Compiled according to form No. M-15.

The list of details used can be modified in accordance with the needs of a particular enterprise. The invoice is issued in two copies. The financially responsible person is engaged in this. One copy of the document is used when writing off building materials, the second - when registering.