In early August, Vladimir Putin signed a law changing the procedure for calculating property taxes for individuals...

The document prohibits increasing the amount of property tax calculated on the basis of the cadastral value by more than 10% per year - from a coefficient of 0.2 to 1. The law will come into force at the beginning of 2019, but in the regions new rules may be introduced this year.

The new procedure for property taxation, taking into account the cadastral value, has been applied since January 1, 2015. Previously, tax calculation was based on inventory value. In some regions of Russia, a new tax calculation mechanism began to be used in 2021 (for the tax period of 2015). Initially, it was assumed that the transition to the new order would last 5 years, during this period the tax amount was to increase annually by 20%. It was planned to reach the full tax amount from 2021.

Thanks to the new law, Russians will be able to reduce tax costs. The real estate portal superrielt.ru found out what changes have been made to the procedure for calculating property taxes, what benefits are provided for by the new law, and what other innovations await Russians.

Legislative aspects of property tax

The analyzed tax falls within the purview of Chapter 30 of the Tax Code of the Russian Federation. Property assets are included in the tax base according to the conditions declared in Art. 374 Tax Code of the Russian Federation. Clause 4 of this article provides a list of objects for which this tax is not required to be paid. Art. 381 of the Tax Code of the Russian Federation considers certain types of activities that do not involve the collection of this tax from the entrepreneur.

In general, Russian organizations, as well as foreign ones with a representative office in the Russian Federation, are required to pay tax on property on their balance sheet, movable, capitalized before 2013, and/or immovable. Some categories of organizations are beneficiaries.

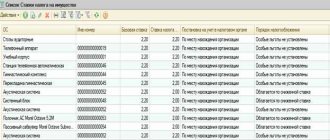

This tax is regional, which means that the constituent entities of the Russian Federation can independently reduce the tax rate of 2.2% established by the Government.

REFERENCE! If an entrepreneur wants to find out the tax rate of his region, he can refer to the official website of the Federal Tax Service, which contains background information on various rates and benefits, including property tax.

Receipts are not sent with tax notices

Previously, along with tax notices, receipts for payment were sent by mail - separate for each tax. These were completed documents with details and amounts. They could be taken to the bank or given to relatives for payment.

Since 2021, receipts have not been sent: they are not in postal envelopes or in your personal account. The tax notice contains details for paying each tax.

Details for paying tax and unique identification number (UIN) are indicated below the table with charges

To pay taxes without receipts, use the State Services service to pay by UIN - with or without authorization. The details are filled in automatically.

Pay taxes according to UIN

Who will make and submit payments?

According to the legislation of the Russian Federation, payers of property tax are those organizations in respect of which three conditions are met:

- ownership, temporarily, by power of attorney or part-time ownership of real estate and/or movable property included in the balance sheet before 2013, not included in depreciation groups 1 and 2;

- accounting of these property assets is carried out in accounts 01 “Fixed assets” or 03 “income investments in tangible assets”;

- all these assets are provided for by the corresponding article of the Tax Code (Article 374) and are not included in the list of exceptions.

ATTENTION! The specific person in the organization responsible for the calculation and timely payment of property tax is the founder of the trust management (Article 378 of the Tax Code of the Russian Federation).

Grounds for revising the cadastral value

In the cases described in paragraph 15 of Article 378.2 of the Tax Code of the Russian Federation, a new cadastral value may be established for a real estate property.

Firstly, this is a change in the characteristics of the object in terms of quality and quantity (paragraph 2, paragraph 15, article 378.2 of the Tax Code of the Russian Federation). For example, in cases of division or merger.

Secondly, correction of errors that occurred during the determination of the cadastral value of the object (paragraph 3, clause 15, article 378.2 of the Tax Code of the Russian Federation). Errors may be technical and cadastral. Their characteristics are given in Article 61 of the Federal Law of July 13, 2015 No. 218-FZ “On State Registration of Real Estate”.

A technical error (a clerical error, a typo, a grammatical or arithmetic error, or a similar error) is an error made by the cadastral registration authority when carrying out state cadastral registration and (or) state registration of rights, leading to a discrepancy between the information contained in the Unified State Register of Real Estate and the information in the documents on on the basis of which information was entered into the Unified State Register.

Cadastral (registry error) is:

- an error reproduced in the Unified State Register of Real Estate in the boundary plan, technical plan, map-plan of the territory or survey report, which arose as a result of an error made by the person who performed the cadastral work;

- an error contained in documents sent or submitted to the rights registration authority by other persons and (or) bodies in the order of information interaction, as well as in other established procedures.

And thirdly, the adoption of a decision by a commission or a judicial act based on the results of a dispute about determining the size of the cadastral value of an object (paragraph 4, clause 15, article 378.2 of the Tax Code of the Russian Federation).

Who doesn't have to worry about property taxes?

Some business entities are legally exempt from the obligation to pay property tax. These include the following groups of businessmen.

- Organizations whose balance sheet accounts do not have fixed assets that can be recognized as objects of property tax.

- The organization's property is associated with oil production in offshore fields.

- Property of individual entrepreneurs and individuals.

Rules for calculating property tax

The tax base is the book value of the property subject to tax accounting. The average annual value of the residual value is taken into account, which must first be calculated according to the procedure established in the regulatory acts of the organization.

To find out the residual value, you need to subtract the depreciation amount from the original balance sheet estimate.

ST.rest. = ST.first – Ananum.

Where:

- ST.rest. – total residual value of property assets subject to taxation;

- ST.first – initial book value of assets;

- Ananum. – accrued depreciation.

And to calculate the average annual cost, you need to know the balance on the 1st day of the month, as well as the final cost at the end of the year. For this, the following principle applies:

ST.WED-year. = (ST.start.1 + ST.start.2 + … + ST.start.12 + ST.fin.) / 13

Where:

- ST.beginning 1-12 – residual value of property on the 1st day of each month;

- ST.fin. – residual value as of the 31st day of the last month of the year.

Then the tax base must be multiplied by the tax rate adopted in the region and by 100%.

Submission of advance payment calculations

Filing quarterly declarations on advance payments of property tax is the responsibility of all its payers (Article 386 of the Tax Code of the Russian Federation). In this case, it does not matter what the value of the declared property is, it may even be zero - you still need to submit calculations (letter of the Federal Tax Service of the Russian Federation dated February 8, 2010 No. 3-3-05/128).

If a taxable object is accounted for not at its residual value, but at its cadastral value, calculations of advance tax payments for it are made on a general basis.

Calculations must be submitted to the tax authority at the place of registration, and if the object is recorded at the cadastral value, then to the tax authority at the location of such objects.

From January 1: apply for a personal income tax refund if you bought a home

If you bought a home in 2021 and never received a tax deduction, then in 2019 you can apply for a personal income tax refund of 13%. You will be refunded an amount of up to 260 thousand rubles (plus 13% of the overpayment on the mortgage loan) provided that you previously received income subject to personal income tax. (Learn more about tax refunds when buying a home.)

Is it possible to get a tax deduction again?

Does selling an apartment prevent you from getting a tax deduction?

Correct calculations

The Federal Tax Service of the Russian Federation has developed a special form for submitting calculations of quarterly payments for property tax (approved by Order of the Federal Tax Service dated November 24, 2011 No. ММВ-7-11/895). According to this order, this can also be done electronically, and for organizations with a large number of personnel this requirement is mandatory.

NOTE! If the organization has more than 100 personnel for the reporting year, it is impossible to submit calculations in paper form, such documents will not be considered submitted, and the organization will be fined (clause 3 of Article 80 of the Tax Code of the Russian Federation).

Filling out the form requires entering the following data.

The title page should include:

- company details;

- correction code (is it a primary or updated document);

- reporting period code and year;

- Tax office code (look on the Federal Tax Service website);

- full name of the company;

- OKVED code;

- contact number;

- number of pages in calculation;

- number of application sheets (if any);

- the date of recieving;

- signature of the responsible person.

Section 1 – justification of the amount contributed to the budget as an advance payment for property tax. Section 2 – calculation of property tax on objects reflected at book value (separately for each category of assets). Section 3 – calculation of property tax on objects reflected at cadastral value.

Before April 30: submit a tax return if you sold or rented out real estate

If you sold real estate or rented it out in 2018, then by April 30 you need to declare your income, that is, submit a tax return in form 3-NDFL.

If you rented out housing as an individual, the tax will be 13% of all income received for 2021. The lessor is required to pay income tax in form 3-NDFL.

The calculation of income tax on the sale of housing is calculated depending on the period of ownership of the property, its value, and also takes into account the tax deduction. (The lawyer talks about tax calculation in more detail in this article.)

The return must be filed even if you are eligible for benefits or have zero income.

If you not only sold, but also bought housing with the right to return personal income tax, indicate this in the declaration. When filing a declaration in 2021, a citizen has the right to reflect expenses simultaneously with declaring income, returning the tax, the amount of which can be up to 13% of the income received. When declaring income and expenses at the same time, there will be an offset of the amounts to be paid to the budget and to be returned from the budget.

What expenses should be included in the declaration to reduce tax?

What is the tax on the sale of an apartment obtained after demolition?

Don't miss deadlines

The reporting period for this tax is a quarter.

- For objects with a reflected book value, time goes “increasingly” - for 1 quarter, for half a year, for 9 months.

- For property with cadastral value, calculations are made quarterly.

Calculations and advance payments must be submitted no later than 30 days of the first month of the next quarter. If it coincides with a holiday or weekend, you are allowed to submit the invoice on the next working day.

Late deadlines are fraught with a fine: 200 rubles. for each report not submitted on time, and if the deadlines required by the tax authorities are violated, the organization may be fined 300-500 rubles.

IMPORTANT! Calculation of an advance payment is not a tax return, therefore responsibility for late filing occurs not under Article 119 of the Tax Code of the Russian Federation, but under clause 1 of Art. 126 of the Tax Code of the Russian Federation and Part 1 of Art. 15.6 Code of Administrative Offenses of the Russian Federation. The property tax return is submitted only at the end of the year.

At the end of the accounting year, you need to calculate the annual payment and subtract from it the amount already paid as advance payments. This is the number that will appear on your annual tax return.

Until July 15, 2021: pay tax according to the declaration

Once you have submitted your return, it will take some time to process it. As a rule, the amount payable is fixed no later than the end of June, but there may be delays.

In any case, you must pay the tax yourself; the tax office will not send any notification. You can pay tax on the 3-NDFL declaration at Sberbank, on the government services website, and you can generate a receipt on the tax website. Your X-day on this issue is July 15th. This is the deadline for paying taxes.

If you miss this deadline, the next day the tax amount will turn into a debt, and a penalty will be charged on it. “First, the tax office will wait, then it will send a demand for payment and may collect the amount of debt by court order,” says the State Services website. - That is, it will simply be written off from your account. If the debt is more than 30 thousand rubles, the bailiffs may restrict travel abroad.”

Example of calculating advance payments

On the balance sheet of Metal-Service LLC there is equipment, the residual value of which as of January 1, 2021 is equal to 90,000 rubles. Every month the equipment is depreciated by 3,000 rubles. The tax rate is the maximum. Let's calculate the advance payment for the 1st quarter.

At the end of January 2021, the residual value of the equipment will be 90,000 - 3,000 = 87,000 rubles, at the end of February 2021 - 87,000 - 3000 = 84,000 rubles, and at the beginning of March - 84,000 - 3000 = 81,000 rubles. Let's find the average quarterly value of the asset, which will be the tax base: (90,000 + 87,000 + 84,000 + 81,000) / 4 = 85,500 rubles.

We multiply the resulting tax base by the rate of 2.2 and find the percentage: 85,500 x 2.2/100 = 1881 rubles. This amount will be an advance payment for the equipment of Metal-Service LLC for the 1st quarter.