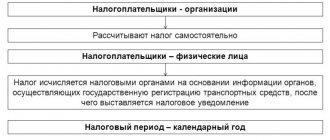

Everyone must pay taxes. These include not only companies and individual entrepreneurs, but also individuals. And if everything is clear with companies and individual entrepreneurs regarding tax payment. Not all individuals know what exactly they owe money to the budget for. It is for this reason that many individuals subsequently receive from the tax authorities a notification of a penalty, for the payment of which the KBK code 18210601020042100110 is used.

Of course, many will say, what should an individual pay for? The answer is simple, for the real estate that is in their possession. That is, every individual who is the owner of any immovable property is obliged to timely pay property taxes. At the moment, 3 types of rates are applied for taxation. Most properties classified as residential qualify for a 0.1% rate. But if the premises are used as an office, or its cadastral value is more than 300 million rubles, then the tax authorities apply a 2% rate. A 0.5% rate applies to all other properties.

KBK

In each transaction related to the payment of taxes, fines and penalties, a specific KBK code is used. Subsequently, it is he who helps tax authorities correctly distribute funds received from taxpayers. The KBK consists of 20 digits, and any error, even in one, suspends the receipt of payment to the budget. This means that after the end of the period allocated for payment of the tax, the individual will have to receive a notification of the accrual of penalties.

Of course, such trouble can be avoided, but only if, first of all, the KBK is entered correctly, as well as the recipient’s current account. And tax payment will occur within the specified time frame. Otherwise, it will be possible to get rid of the penalty only on the condition that in the payment documentation an error was made only in the KBK. Then, when submitting an application with the correct BCC, you must attach a copy of the payment document with an error.

In this situation, the accrued penalty under code 18210601020042100110 will not have to be paid, since after confirmation of the reason for the delay in payment, the tax services will cancel the accrued penalty. But such a good ending with the delayed tax amount does not always happen.

If, when filling out a payment document, an individual made errors in the current account and the cash register, then it is impossible to identify the amount and send it to the right place. Most often, this amount simply goes to the budget, and the tax service begins to accrue penalties for the individual. It will be impossible to find the amount sent previously. In this situation, the individual will have to come to terms and again pay the required amount of tax, according to a correctly completed payment document.

This also applies to accrued penalties. To pay for it, you must enter the code 18210601020042100110 in the payment document. Only in this case will the amount be transferred to the budget and the penalty repaid.

What is the code 18210602010022100110 for?

KBK 18210602010022100110, transcript 2021 is a 20-digit code used to pay penalties assessed to an organization by the tax authority in case of late payment of property tax not included in the Unified Gas Supply System. Payment of penalties occurs by filling out a payment document using the same form 0401060, which is also used for paying taxes. But it is worth considering that in both cases, filling out a payment form in 2021 is somewhat different in nature compared to previous years.

In total, 6 lines were changed in the payment document. Now line 16 is used to enter information about the recipient. On line 22, the organization’s accountant must enter the UIN. To enter information about the reason for carrying out a financial transaction, that is, payment of penalties, line 106 is used. Line 107 reflects the tax period, and in line 108 the accountant must reflect the document number for which the funds are transferred. In line 109 the date of the document for which the amount is deducted is entered.

In addition to such changes in filling out the lines, there are also some features that must be taken into account by the accountant when filling out the payment document for the payment of penalties. So line 16 should now reflect the territorial body of the Federal Tax Service. In line 106 you should enter the KBK code 18210602010022100110 .

Other sections of the KBK

- Pension contributions. Decoding codes for the budget classification of pension contributions for 2021.

- Contributions to compulsory social insurance. Decoding codes for the budget classification of contributions to compulsory social insurance for 2021.

- Contributions for compulsory health insurance. Decoding codes for the budget classification of contributions for compulsory health insurance for 2021.

- Personal income tax (NDFL). Deciphering the budget classification codes for personal income taxes (NDFL) 2021.

- Value added tax (VAT). Decoding the budget classification codes for value added tax (VAT) 2020.

- Income tax. Decoding the 2021 income tax budget classification codes.

- Excise taxes. Decoding the codes for the budget classification of excise taxes for 2020.

- Organizational property tax. Decoding the codes of the budget classification of property tax for organizations 2021.

- Land tax. Deciphering the codes for the budget classification of land tax for 2021.

- Transport tax. Deciphering the transport tax budget classification codes for 2021.

- Single tax with simplification. Decoding the codes of the budget classification of the single tax during simplification for 2021.

- Unified tax on imputed income (UTII). Decoding codes for the budget classification of the single tax on imputed income (UTII) 2020.

- Unified Agricultural Tax (USAT). Decoding the codes of the budget classification of the Unified Agricultural Tax (USAT) 2020.

- Mineral extraction tax (MET). Deciphering the budget classification codes for mineral extraction taxes (MET) 2021.

- Fee for the use of aquatic biological resources. Decoding the budget classification codes of the fee for the use of aquatic biological resources for 2021.

- Fee for the use of fauna objects. Deciphering the codes of the budget fee for the use of wildlife objects in 2020.

- Water tax. Decoding the codes of the budget classification of water tax for 2021.

- Payments for the use of subsoil. Decoding codes for the budget classification of payments for the use of subsoil for 2021.

- Payments for the use of natural resources. Decoding codes for the budget classification of payments for the use of natural resources for 2021.

- Gambling tax. Deciphering the budget classification codes for the gambling tax for 2021.

- Government duty. Decoding the codes of the budget classification of state duty for 2021.

- Income from the provision of paid services and compensation for state costs. Decoding codes for the budget classification of income from the provision of paid services and compensation for state expenses in 2020.

- Fines, sanctions, payments for damages. Decoding codes for the budget classification of fines, sanctions, payments for damages in 2021.

- Trade fee. Decoding the codes of the budget classification of trade tax for 2021.

- News. All news on changes in (KBK) budget classification codes for past and current years.

Decoding KBK 18210602010021000110

The legislation provides for taxes for entrepreneurs, individuals and legal entities. Companies pay fees under individual BCCs. Thus, KBK 18210602010021000110 is used to deposit the tax amount on property not included in the Unified Gas Supply System (UGSS). The UGSS is a technological complex that includes gas production, processing and storage facilities. For organizations participating in the Unified State Gas System, a separate tax base for payment is provided. Their budget classification code is different from others. An organization must calculate tax only on depreciated property, which is listed as fixed assets.

The code for paying the property tax consists of 20 digits, divided into combinations. Each combination corresponds to the value:

- 182 - department that controls the receipt of payments: Federal Tax Service Inspectorate.

- 1 - type of income: tax.

- 06 — revenue subtype: property taxes.

- 02010 - specifies the fee, indicates the budget: property tax of organizations on property that does not belong to the Unified State System, which is transferred to the regional budget.

- 02 - treasury category: budget of a subject of the Russian Federation.

- 1000 — purpose of payment: standard payment.

- 110 - specifies the income group: tax receipts.

How did the BCC change in 2020-2021 and were there any changes to the BCC for taxes?

If you want to send a letter to someone by Russian Post, you must indicate the address of the destination and recipient. The budget classification code plays the role of the address for payment to the budget or declaration. The payer indicates the BCC in 2020-2021 in the payment order, and the treasury sends the money to the budget of the appropriate level for a specific item and sub-item of income. The same is with reporting: the KBK 2020-2021 contains information both about the tax itself and about the taxpayer.

IMPORTANT! In 2020-2021, KBC is used not only by legal entities and businessmen. Ordinary citizens also use them, paying, for example, property taxes based on notifications received from the tax office.

The list of KBK changes regularly. It is approved by the Russian Ministry of Finance. Thus, in 2021, the procedure for generating codes, their structure and principles of assignment, approved by departmental order No. 99n dated 06/08/2020, is applied. The list of BCCs for 2021 is determined by Order of the Ministry of Finance dated November 29, 2019 No. 207n (initially, Order No. 86n dated June 6, 2019 was adopted for this purpose, but Order 207n replaced it). In 2019, the procedure and list from the Order of the Ministry of Finance dated June 8, 2018 No. 132n were in effect.

Despite the replacement of regulatory legal acts, the BCC for 2021 for taxes and contributions has not changed compared to 2021. But their list was expanded - new BCCs were introduced for fines under the first part of the Tax Code. In addition, the CBC for administrative fines imposed in accordance with Chapter 15 of the Code of Administrative Offenses of the Russian Federation has been updated.

The previous (significant) change to the BCC occurred in 2021 and was associated with the transfer of insurance premiums (except for injuries) under the control of the tax service. That is, the recipient of these funds was the budget, and not an extra-budgetary fund. Accordingly, changes were required in the main BCCs for such payments. Subsequently, the Ministry of Finance adjusted the BCC several times for contributions to compulsory pension insurance accrued at additional tariffs.

Since 2021, the BCC has been introduced for the NAP of self-employed citizens - 182 1 0500 110.

There were no other significant changes that would be significant in 2020-2021 in the BCC list.

You can find out more about decoding the KBK in the material “Deciphering the KBK in 2021 - 2021 - 18210102010011000110, etc.”

Changes in the BCC for corporate property tax in 2018

In 2021, the object of taxation has changed - movable property will no longer be taxed. This applies to all types of property of organizations - property owned and not owned by companies participating in the Unified Gas Supply System. The budget classification codes have not changed and remain the same. Tax residents pay the fee using base code 18210602010020000110.

Property tax is paid not only by organizations, but also by individuals. The BCC of property tax for ordinary citizens for all types of payments and for all categories owning property differ from each other.

KBC in 2020-2021: table of insurance premiums

Our KBK table in 2020-2021 reflects information regarding insurance premium codes that are most in demand among payers.

KBK for insurance premiums for employees

| Payment type | KBK | ||

| Contributions accrued for periods before 2021, paid after 01/01/2017 | Contributions for 2017-2021 | ||

| Contributions to compulsory pension insurance | contributions | 182 1 0200 160 | 182 1 0210 160 |

| penalties | 182 1 0200 160 | 182 1 0210 160 | |

| fine | 182 1 0200 160 | 182 1 0210 160 | |

| Contributions to compulsory social insurance | contributions | 182 1 0200 160 | 182 1 0210 160 |

| penalties | 182 1 0200 160 | 182 1 0210 160 | |

| fine | 182 1 0200 160 | 182 1 0210 160 | |

| Contributions for compulsory health insurance | contributions | 182 1 0211 160 | 182 1 0213 160 |

| penalties | 182 1 0211 160 | 182 1 0213 160 | |

| fine | 182 1 0211 160 | 182 1 0213 160 | |

| Contributions for injuries | contributions | 393 1 0200 160 | |

| penalties | 393 1 0200 160 | ||

| fine | 393 1 0200 160 | ||

KBK for insurance premiums of individual entrepreneurs

| Payment type | KBK | ||

| Contributions accrued for periods before 2021, paid after 01/01/2017 | Contributions for 2017-2021 | ||

| Fixed contributions to the Pension Fund, including contributions | contributions | 182 1 0200 160 | 182 1 0210 160* *Unified BCC for the fixed part and contributions from income over 300,000 rubles. valid from 04/23/2018 |

| Contributions to the Pension Fund of the Russian Federation 1% on income over 300,000 rubles. | contributions | 182 1 0200 160 | |

| penalties | 182 1 0200 160 | 182 1 0210 160 | |

| fine | 182 1 0200 160 | 182 1 0210 160 | |

| Contributions for compulsory health insurance | contributions | 182 1 0211 160 | 182 1 0213 160 |

| penalties | 182 1 0211 160 | 182 1 0213 160 | |

| fine | 182 1 0211 160 | 182 1 0213 160 | |

You can download the KBK table for penalties and fines for contributions to compulsory pension insurance at additional tariffs here.

Budget classification codes for taxes for 2020-2021

The BCCs for the taxes indicated in the tables below have not changed in recent years (the same for 2021 and 2021). So that you can easily and quickly find the CBC you need (among the most popular ones), we have divided them into groups:

KBK table for personal income tax for 2020-2021

| Personal income tax on employee income | 182 1 0100 110 |

| Penalties for personal income tax on employee income | 182 1 0100 110 |

| Personal income tax fine on employee income | 182 1 0100 110 |

| Personal income tax on individual entrepreneur income on OSNO | 182 1 0100 110 |

| Penalties for personal income tax on income of individual entrepreneurs on OSNO | 182 1 0100 110 |

| Personal income tax fine on income of individual entrepreneurs on OSNO | 182 1 0100 110 |

KBK income tax table

| Purpose of payment | Mandatory payment | Penalty | Fine |

| To the federal budget (except for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| To the budgets of the constituent entities of the Russian Federation (except for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| To the federal budget (for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| To the budgets of the constituent entities of the Russian Federation (for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 11 |

| When implementing production sharing agreements concluded before October 21, 2011 (before the law of December 30, 1995 No. 225-FZ came into force) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the income of foreign organizations not related to activities in Russia through a permanent representative office | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the income of Russian organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the income of foreign organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From dividends from foreign organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From interest on state and municipal securities | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the profits of controlled foreign companies | from the profits of controlled foreign companies | from the profits of controlled foreign companies | from the profits of controlled foreign companies |

KBK for VAT

| Payment type | Tax | Penalty | Fine |

| VAT on goods (work, services) sold in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| VAT on goods imported into Russia (from the Republics of Belarus and Kazakhstan) | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| VAT on goods imported into Russia (payment administrator - Federal Customs Service of Russia) | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

Read about algorithms for calculating fixed payments in the article “KBK - fixed payment to the Pension Fund in 2021 - 2021 for individual entrepreneurs for themselves.”

What to do if KBK made a mistake when paying a tax or contribution? Find out the answer to this question in the Ready-made solution from ConsultantPlus by receiving free trial access to the system.

BCC 2020-2021 for special regimes (simplified taxation, imputation, patent, agricultural tax), trade tax and tax on gambling business will be as follows:

| Name KBK 2020-2021 | KBK for transferring tax or contribution | KBK for penalties | BCC for fine |

| Single tax under the simplified tax system “income” | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Single tax under the simplified tax system “income minus expenses” (including minimum tax) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| UTII | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Unified agricultural tax | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Trade fee | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Patent (city district budget) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Patent (municipal district budget) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Patent (for residents of Moscow, St. Petersburg, Sevastopol) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Gambling tax | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

BCC for property taxes (transport, land, property tax)

| Name of KBK | KBK for transferring tax or contribution | KBK for penalties | BCC for fine |

| Transport tax for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Transport tax for individuals | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax for legal entities (for Moscow, St. Petersburg, Sevastopol) | 182 1 06 06 031 03 1000 110 | 182 1 06 06 031 03 2100 110 | 182 1 06 06 031 03 3000 110 |

| Land tax within the boundaries of urban districts for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on land within the boundaries of inter-settlement territories for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on land within the boundaries of rural settlements for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on land within the boundaries of urban settlements for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax for plots within the boundaries of urban districts with intra-city division for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax for plots within the boundaries of intracity districts for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Property tax for individuals (for Moscow, St. Petersburg, Sevastopol) | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of individuals located within the boundaries of urban districts | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of individuals located within the boundaries of inter-settlement territories | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of individuals located within the boundaries of rural settlements | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of individuals located within the boundaries of urban settlements | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of organizations (not included in the unified gas supply system) | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of organizations included in the unified gas supply system | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

There are a number of changes in the BCC for excise duties, but the main codes remain the same:

| Name of KBK | KBK for transferring tax or contribution | KBK for penalties | BCC for fine |

| Excise taxes on ethyl alcohol produced in Russia from food raw materials (except for those listed in the following paragraphs) | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on ethyl alcohol produced in Russia from food raw materials (distillates of wine, grape, fruit, cognac, Calvados, whiskey) | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on ethyl alcohol produced in Russia from non-food raw materials | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian-made alcohol-containing products | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian beer | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian alcoholic products with an ethyl alcohol content of more than 9% (except for beer and various wines) | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian alcoholic products with a share of ethyl alcohol up to 9% (except for beer and various wines) | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian wines | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian motor gasoline | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian diesel fuel | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

Other KBK from this category:

| 18210601010031000110 | Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of intra-city municipalities of federal cities (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) |

| 18210601010032100110 | Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of intra-city municipalities of federal cities (penalties on the corresponding payment) |

| 18210601010032200110 | Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of intra-city municipalities of federal cities (interest on the corresponding payment) |

| 18210601010033000110 | Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of intra-city municipalities of federal cities (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) |

| 18210601020042100110 | Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of urban districts (penalties on the corresponding payment) |

| 18210601020042200110 | Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of urban districts (interest on the corresponding payment) |

| 18210601020043000110 | Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of urban districts (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) |

| 18210601020111000110 | Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of urban districts with intra-city division (payment amount (recalculations, arrears and debt for the corresponding payment, including canceled ones) |

| 18210601020112100110 | Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of urban districts with intra-city division (penalties on the corresponding payment) |

| 18210601020112200110 | Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of urban districts with intra-city division (interest on the corresponding payment) |

| 18210601020113000110 | Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of urban districts with intra-city division (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) |

| 18210601020121000110 | Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of intracity districts (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) |

| 18210601020122100110 | Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of intracity districts (penalties on the corresponding payment) |

| 18210601020122200110 | Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of intracity districts (interest on the corresponding payment) |

| 18210601020123000110 | Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of intracity districts (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) |

| 18210601030051000110 | Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of inter-settlement territories (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) |

| 18210601030052100110 | Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of inter-settlement territories (penalties on the corresponding payment) |

| 18210601030052200110 | Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of inter-settlement territories (interest on the corresponding payment) |

| 18210601030053000110 | Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of intersettlement territories (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) |

| 18210601030101000110 | Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of rural settlements (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) |

| 18210601030102100110 | Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of rural settlements (penalties on the corresponding payment) |

| 18210601030102200110 | Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of rural settlements (interest on the corresponding payment) (interest on the corresponding payment) |

| 18210601030103000110 | Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of rural settlements (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) |

| 18210601030131000110 | Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of urban settlements (payment amount (recalculations, arrears and debt for the corresponding payment, including canceled ones) |

| 18210601030132100110 | Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of rural settlements (penalties on the corresponding payment) |

| 18210601030132200110 | Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of urban settlements (interest on the corresponding payment) (interest on the corresponding payment) |

| 18210601030133000110 | Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of urban settlements (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) |

KBK for payment of property tax for individuals

| Decoding the code | Budget classification code |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of intra-city municipalities of federal cities (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) | 182 1 0600 110 (original code) 18210601010031000110 (short code) |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of intra-city municipalities of federal cities (penalties on the corresponding payment) | 182 1 0600 110 (original code) 18210601010032100110 (short code) |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of intra-city municipalities of federal cities (interest on the corresponding payment) | 182 1 0600 110 (original code) 18210601010032200110 (short code) |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of intra-city municipalities of federal cities (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0600 110 (original code) 18210601010033000110 (short code) |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of urban districts (payment amount (recalculations, arrears and debt for the corresponding payment, including canceled ones) | 182 1 0600 110 (original code) 18210601020041000110 (short code) |

| Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of urban districts (penalties on the corresponding payment) | 182 1 0600 110 (original code) 18210601020042100110 (short code) |

| Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of urban districts (interest on the corresponding payment) | 182 1 0600 110 (original code) 18210601020042200110 (short code) |

| Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of urban districts (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0600 110 (original code) 18210601020043000110 (short code) |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of urban districts with intra-city division (payment amount (recalculations, arrears and debt for the corresponding payment, including canceled ones) | 182 1 0600 110 (original code) 18210601020111000110 (short code) |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of urban districts with intra-city division (penalties on the corresponding payment) | 182 1 0600 110 (original code) 18210601020112100110 (short code) |

| Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of urban districts with intra-city division (interest on the corresponding payment) | 182 1 0600 110 (original code) 18210601020112200110 (short code) |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of urban districts with intra-city division (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0600 110 (original code) 18210601020113000110 (short code) |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of intracity districts (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) | 182 1 0600 110 (original code) 18210601020121000110 (short code) |

| Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of intracity districts (penalties on the corresponding payment) | 182 1 0600 110 (original code) 18210601020122100110 (short code) |

| Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of intracity districts (interest on the corresponding payment) | 182 1 0600 110 (original code) 18210601020122200110 (short code) |

| Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of intracity districts (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0600 110 (original code) 18210601020123000110 (short code) |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of inter-settlement territories (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) | 182 1 0600 110 (original code) 18210601030051000110 (short code) |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of inter-settlement territories (penalties on the corresponding payment) | 182 1 0600 110 (original code) 18210601030052100110 (short code) |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of inter-settlement territories (interest on the corresponding payment) | 182 1 0600 110 (original code) 18210601030052200110 (short code) |

| Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of intersettlement territories (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0600 110 (original code) 18210601030053000110 (short code) |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of rural settlements (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) | 182 1 0600 110 (original code) 18210601030101000110 (short code) |

| Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of rural settlements (penalties on the corresponding payment) | 182 1 0600 110 (original code) 18210601030102100110 (short code) |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of rural settlements (interest on the corresponding payment) (interest on the corresponding payment) | 182 1 0600 110 (original code) 18210601030102200110 (short code) |

| Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of rural settlements (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0600 110 (original code) 18210601030103000110 (short code) |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of urban settlements (payment amount (recalculations, arrears and debt for the corresponding payment, including canceled ones) | 182 1 0600 110 (original code) 18210601030131000110 (short code) |

| Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of rural settlements (penalties on the corresponding payment) | 182 1 0600 110 (original code) 18210601030132100110 (short code) |

| Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of urban settlements (interest on the corresponding payment) (interest on the corresponding payment) | 182 1 0600 110 (original code) 18210601030132200110 (short code) |

| Property tax for individuals, levied at the rates applicable to taxable objects located within the boundaries of urban settlements (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0600 110 (original code) 18210601030133000110 (short code) |

KBC for payment of penalties and fines

In addition to codes for standard contribution amounts, KBC have been developed for the payment of fines and penalties. Some payers violate tax laws and pay monetary penalties for violating the Tax Code of the Russian Federation.

Penalty

Sometimes in the payment slip you need to indicate KBK 18210602010022100110. What tax for 2021 should I pay using this number? There is still a tax on the property of organizations on property that does not belong to the Unified State Grid, but there is already a penalty on collection.

Penalties are charged to the payer if funds are not paid on time or not paid at all. Unlike a fine, the amount of the penalty increases with each day of delay. The recovery is calculated depending on the refinancing rate of the Central Bank at the time when the penalties arose. Up to 30 days of delayed payment, the rate is 1/300, and from the 31st day - 1/150. At the final calculation, tax authorities do not have the right to exceed the amount of penalties greater than the amount of tax.

Fines

If the payer refuses to pay the penalty, the amount of the fee or the amount of the penalty already exceeds the amount of the tax, then the tax office charges the offender a fine. A fine is a monetary penalty in a fixed amount, which is calculated as a percentage or a specific amount in ruble equivalent. In addition to refusal to pay the fee, sanctions may be imposed for other reasons, for example, late submission of reports. Also, the payer will not be charged a penalty, but will be immediately assigned a fine if the resident committed the crime intentionally, or not for the first time.

To pay the fine, you must indicate KBK 18210602010023000110 on your payment slip.

You have to pay for the house

Any object is eligible for taxation. This even applies to country houses. Now, regardless of whether it is residential or non-residential, the house is taxable. Therefore, you will have to pay for all real estate for which there are title documents. Any individual can find out the amount of tax on an object in their possession from a notification or a personal visit to the tax service.

The fact is that even if the property was acquired quite recently, the tax office becomes aware of this after a while. Therefore, within a certain time, they receive a notification stating that the individual is obliged to pay tax within a specified period using a special KBK code.