When operating under the general taxation system, companies are required to pay many taxes, including the corporate property tax (hereinafter referred to as the tax). Timely, correct and complete calculation and payment of tax is guaranteed by accounting in the 1C system version 8.3. For this, it is also necessary that the solution be regularly updated, either by the customer (if we are talking about the basic version), or by a 1C franchisee company with which an ITS agreement has been concluded and which provides services for updating 1C versions of CORP and PROF.

When the version is up to date, that is, it reflects all the innovations in legislation, you can proceed to setting up the program. We will tell you below how to do this correctly and as efficiently as possible.

Tax base, rates

The object of taxation, as well as the rate, are established by Chapter 30 of the Tax Code of the Russian Federation. The maximum tax is 2.2%. At the level of constituent entities of the Russian Federation, the right has been granted to reduce the tax rate, as well as to provide additional tax benefits (Article 381 of the Tax Code of the Russian Federation provides for a list of federal tax beneficiaries). It is important to remember this when making settings in the 1C program, that is, before starting work, you need to check whether changes have been made in terms of tax regulation, both at the federal level and in regional legislation.

As a general rule, tax is calculated using the following formula: Tax = tax base (in rubles) * tax rate (in %) - the amount of advance payments (in rubles).

Profit reporting periods

The tax period for income tax, as well as for all other taxes, is the period at the end of which the tax base is determined and the amount of tax payable is calculated (Article 55 of the Tax Code of the Russian Federation).

The tax period for income tax is defined as a calendar year (Clause 1, Article 285 of the Tax Code of the Russian Federation). That is, this is the period from January 1 to December 31.

In addition to the tax period for profits, reporting periods are established.

The Tax Code of the Russian Federation establishes 2 types of reporting periods for income tax - quarterly and monthly. It depends on how the company pays advances on profits - quarterly or on actual profits.

For regular advances, the reporting periods are:

- 1 quarter;

- half year;

- 9 months.

For advances calculated from actual profits, the reporting periods are 1 month, 2 months, 3 months, and so on until the end of the year (January, January-February, January-March, etc.).

Thus, if a company pays ordinary advances on profits, the accrual of advances on property must be reflected:

- for the 1st quarter – as of March 31;

- hand over the ticket for half a year - on June 30;

- for 9 months - as of September 30.

If the company pays advances from the actual profit received, then the accrual of advances on property must be reflected:

- as of March 31, based on profits for January-March;

- as of June 30, based on profits for January-June;

- as of September 30, based on profits for January-September.

Let us remind you that the amounts of tax payments taken into account in other expenses are reflected in line 041 of Appendix No. 2 to Sheet 02 of the income tax return.

Read in the berator “Practical Encyclopedia of an Accountant”

How to fill out Appendix No. 2 to Sheet 02 of the income tax return

Setting up 1C

Calculation of property tax in 1C must begin with setting the necessary settings. You can configure the program in the menu “Main” - “Accounting Policy” - “Taxes and Reports Settings”.

Fig.1 Setting up 1C

On the left side, move the cursor over the line “Property Tax”.

Fig.2 Property tax

Settings for editing open on the right, which reflect the requirements of current legislation, but the user can adapt some of them, focusing on personal benefits and tax rates in force in the region. So, let’s assume that in the region where business activities are carried out, the current rate from January 1, 2021 is reduced to 1.9%.

If the organization has property that is subject to benefits, the code of the corresponding benefit must also be indicated in the “Benefits” section.

Also in this section it is possible to establish tax rates and establish benefits for individual fixed assets. To do this, click on the line “Objects with a special taxation procedure.”

Fig. 3 Objects with a special taxation procedure

In the window that opens, you can select a fixed asset object, set the date for applying the benefit, and also check a box confirming that this fixed asset object is not subject to taxation. In the “Registration” line (Fig. 4), there are three options to choose from:

- At the location of the organization;

- With a different OKTMO code (allows you to generate payment orders for tax payment using other details);

- In another tax authority.

Fig.4 Registration

In this tab, the accounting type code is also set. When you click on the active button, a window for selecting property groups opens by line.

Fig.5 Window for selecting property groups

In the “Tax benefit” line, you can choose to apply a reduced rate for the object, not apply benefits, or be exempt from taxation.

Fig.6 Tax benefit

As an example, we will reflect the application of a reduced tax rate for the “Shop building” object in the amount of 1% (Fig. 7). The initial cost of the object is 12.0 million rubles (incl. VAT 18% - 2,160.0 thousand rubles).

Fig. 7 As an example, we will show the application of a reduced tax rate for the object “Shop building” in the amount of 1%

Let's return to the "Taxes and Reports Settings" menu. When you click the line “Procedure for paying taxes locally” (Fig. 8), a menu opens that allows you to set settings for choosing a tax authority, the date of tax payment (by default - March 30) and making advance payments.

Fig.8 Procedure for paying taxes locally

In the line “Methods of reflecting expenses”, the default method for reflecting expenses is set to account 26 “General business expenses”; you can change it if desired.

Fig. 9 Methods of reflecting expenses

Changes in the property tax of organizations in 1C: Accounting 8 edition 3.0

Our article is devoted to corporate property tax. Federal laws of August 3, 2018 No. 302-FZ and No. 334-FZ amended Chapter 30 of the Tax Code of the Russian Federation (TC RF). Let's look at some of them.

The most important, pleasant change is that from paragraph 1 of Art. 374 of the Tax Code of the Russian Federation, the word “movable” was removed. Thus, starting from 2019, only real estate is recognized as an object of taxation for property tax for Russian organizations. Accordingly, paragraphs no longer apply. 8, paragraph 4 of the above article and paragraph 25 of Art. 381 Tax Code of the Russian Federation.

The second important change in legislation is related to the taxation procedure when changing the cadastral value of a real estate property.

In accordance with the new edition of paragraph 15 of Art. 378.2 of the Tax Code of the Russian Federation, a change in the cadastral value of a taxable object due to a change in the qualitative and (or) quantitative characteristics of this object is taken into account when determining the tax base from the date of entry of information into the Unified State Register of Real Estate.

And in accordance with the new clause 5.1 of Art. 382 of the Tax Code of the Russian Federation, in the event of a change in the above-mentioned characteristics of real estate objects during the tax (reporting) period, the calculation of the amount of tax (advance tax payments) is carried out taking into account the coefficient determined in a manner similar to that established by paragraph 5 of this article.

Clause 5 determines the procedure for calculating the amount of tax in the event of the emergence or termination, during the tax (reporting) period, of ownership of real estate objects. If we rephrase it for the case of a change in cadastral value, it turns out that this coefficient is defined as the ratio of the number of full months during which a property has a specific cadastral value to the number of calendar months in the tax (reporting) period. If a change in the cadastral value occurred before the 15th day of the corresponding month inclusive, then this month refers to the new cadastral value, if after the 15th day, then to the old cadastral value.

We got acquainted with the legislation. It remains only to figure out how the above legislative changes are implemented in the 1C: Accounting 8 edition 3.0 program starting from release 3.0.66.

With movable property everything is simple. Movable property is not subject to taxation. Therefore, starting from 2021, tax is not charged on it in the program and it is not reflected in property tax returns. But for the case of a change in the cadastral value of a real estate property during the tax period, we will consider an example. The organization "Rassvet" applies the general taxation regime - the accrual method and PBU 18/02 "Accounting for calculations of corporate income tax."

For example, an organization owns a real estate asset - a Building. The property was registered in the Unified State Register of Real Estate on March 13, 2021. The cadastral value of the property at the time of registration was 200,000,000 rubles, the tax rate was 1.5%. The organization does not enjoy tax benefits.

In accounting, real estate is taken into account as an object of fixed assets, and for profit tax purposes, as an object of depreciable property. In the program, to accept a fixed asset object for accounting, the document Acceptance for accounting of fixed assets is used. Information about the object is stored in the Fixed Assets directory. There has been a slight change in this guide. Previously, the fixed assets accounting group was used to separate property into movable and immovable. Now in the directory element you need to check the Real Estate checkbox. This approach simplifies the allocation of real estate in the event that there are taxation peculiarities, when both movable and immovable property may belong to one group of fixed asset accounting. When updating the program, the Real Estate checkbox is automatically selected in the following asset accounting groups: buildings, structures, perennial plantings, land plots, environmental management objects.

The Fixed Assets directory item used in our example is shown in Fig. 1.

Picture 1.

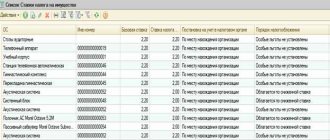

All the necessary information and settings for the automatic calculation and calculation of property taxes in the program, as well as for filling out declarations, can be found in the Taxes and reports form (Main section). To do this, on the left side of the form you need to select the desired tax - Property Tax. Here you can find general tax rates and general benefits, as well as three hyperlinks to special information registers (Fig. 2).

Figure 2.

For a real estate object for which the tax base is the cadastral value, it is necessary to create an entry in the information register Objects with a special taxation procedure.

In the created register entry, you must select the appropriate fixed asset and indicate the start date for applying the information in the program. Then you need to determine the place where the object will be registered. There are three options: At the location of the organization, With a different code according to OKTMO and In another tax authority. Accordingly, when choosing the second or third option, additional details will be requested in the register entry form. It is necessary to indicate the type of tax base - Cadastral value and then indicate the cadastral number of the property, the date of registration of ownership, cadastral value, tax rate and, if any, tax benefit.

The register entry with the initial registration of the property is shown in Fig. 3.

Figure 3.

To indicate the procedure for paying property taxes, the information register “Procedure for paying taxes locally” is used. In our example, the organization is required to make advance payments (Fig. 4).

Figure 4.

The account for allocating property tax expenses and its analytics are indicated in the information register Methods for recording expenses. For all fixed assets, our organization uses account 26 “General business expenses” with analytics (cost item) Property tax as an account for allocating property tax costs. The cost item used must have the expense type - Taxes and fees.

The entry of the above register is shown in Fig. 5.

Figure 5.

For 2021, tax was calculated in the amount of 2,500,000 rubles. Pay attention to the ownership ratio. The building was registered in the Unified State Register of Real Estate on March 13, 2021, that is, until the 15th of the month inclusive. Consequently, in accordance with paragraph 5 of Art. 382 of the Tax Code of the Russian Federation, the month of March (the month of emergence of ownership of the property) is taken as the full month of ownership. Therefore, the above coefficient has a value of 10/12.

Let's check the calculation of the tax amount: Tax = NOB * STni * Kv = 200,000,000 rub. * 1.5% * 10/12 = 2,500,000 rub.

That's right. But, please note that starting next year the ownership coefficient will look a little different. It will be a decimal number with four decimal places. For example - 0.8333. Therefore, the tax amount in an identical situation will be slightly different.

The property tax return for 2021 is shown in Fig. 6.

Figure 6.

The calculation and accrual of property tax in the program is carried out by the routine operation Calculation of property tax at the end of the month. Since the organization pays advance payments, this routine operation is performed in each last month of the quarter. Let's look at the calculation certificate for this regulatory operation for March 2021. The calculation certificate and the corresponding posting are shown in Fig. 7.

Figure 7.

In the first quarter of 2021, the advance payment for property tax will be, as in the second and third quarters of 2021, 750,000 rubles. The same amount will be calculated in the second quarter, but in the third quarter an event occurred that is of great interest to us. In July 2021, due to changes in the qualitative and (or) quantitative characteristics of the property, its cadastral value increased. Information about this was entered into the Unified State Register of Real Estate on July 16, 2021. The new cadastral value of the property is 250,000,000 rubles.

In the program, to reflect this event, you need to add a new entry to the information register Objects with a special taxation procedure (of course, this can also be done by copying the primary entry). The new entry must indicate the new cadastral value of the real estate, and the “Applies from” requisite must correspond to the day the information was entered into the Unified State Register of Real Estate.

The new information register entry is shown in Fig. 8.

Figure 8.

Let's see how the regulatory operation Calculation of property tax for the third quarter will react to this event. Let me remind you that until 2021, an increase in the cadastral value of a property was taken into account when calculating the tax base only from the beginning of the new tax period. Let's see the result of the routine operation.

In addition to the accounting entry, the routine operation creates entries in the auxiliary information register Calculation of property tax. These records are used when generating calculation certificates and tax returns. The register entries are shown in Fig. 9.

Figure 9.

In this quarter, two records are created for a property with an increased cadastral value: a record with the old cadastral value and a record with the new cadastral value. Let's pay attention to the number of months of use. Everything corresponds to clause 5.1 of Art. 382 of the Tax Code of the Russian Federation. Information about the increase in cadastral value was entered into the Unified State Register after July 15 inclusive, therefore, the old cadastral value is used this month. In the next two months, of course, the new cadastral value is used.

Let's look at the calculation certificate. The property tax calculation certificate and the corresponding posting for the 3rd quarter of 2021 are shown in Fig. 10.

Figure 10.

Two lines will also be generated in the calculation certificate: with the old and new cadastral value. Only instead of the number of months of use, the usage factor will be indicated - a decimal number with an accuracy of four decimal places. The tax amount was calculated using these coefficients.

In the declaration Calculation of advance payments for property tax in section 3 for this property, two pages will be filled out. One page for the old cadastral value and one page for the new one.

Fragments of the calculation of advance payments for property tax for 9 months of 2021 are presented in Fig. eleven.

Figure 11.

Let's see how everything looks at the end of the tax period. To do this, let us turn to the results of the regulatory operation Calculation of property tax for December. The regulatory operation will calculate the number of months of use of the old and new cadastral values during the tax period.

The entries in the property tax calculation information register are shown in Fig. 12.

Figure 12.

In the calculation certificate, as in the third quarter, two lines will be generated for the property: with the old and new cadastral value. Based on the number of months of use in the tax period, utilization rates will be calculated and the tax amount will be calculated. The regulatory operation will take into account the amounts of advance payments for the old and new cadastral values and calculate the amount of tax payable to the budget.

The property tax calculation certificate for 2021 and the corresponding accounting entries are shown in Fig. 13.

Figure 13.

In the Property Tax Declaration, as well as in the Calculation of Advance Payments for Property Tax for the third quarter, in Section 3, for a property with a cadastral value that has changed during the year, two pages will be filled out. One page with the old cadastral value of the property and one page with the new cadastral value.

Fragments of the Property Tax Declaration are presented in Fig. 14.

Figure 14.

As we can see, the developers correctly reflected the change in legislation we considered in the operating algorithm of the 1C: Accounting 8 edition 3.0 program, preparing it for work in the new 2019.

Payment of all advance payments leads to overpayment at the end of the year

Let's consider the option of paying property tax in the general case. The company makes advance payments at the end of each reporting period (Q1, half-year and 9 months). They are calculated in a manner similar to the calculation of property taxes. The amount on the basis of which advance payments are calculated is named in paragraph 4 of Article 376 of the Tax Code of the Russian Federation as the average cost of property. It is calculated by dividing the amount of the residual value of the property by the 1st day of each month of the reporting period and the 1st day of the next month by the number of months in this period (three, six and nine months, respectively), increased by 1. The resulting value (average value of property ) is multiplied by ¼ and by the property tax rate (clause 4 of Article 382 of the Tax Code of the Russian Federation).

At the end of the tax period, tax is paid taking into account advance payments. To do this, the amounts of advance payments paid at the end of the reporting periods are deducted from the calculated tax amount (clause 2 of Article 382 of the Tax Code of the Russian Federation).

on the numbers

Let's use the example data. Since May 2014, the residual value is 0. However, the total value is calculated for the entire reporting period, and the residual value of the first four months is taken into account each time. As can be seen from the calculation (see table), the tax base decreases as the number of months in which the residual value is equal to 0 increases. The amount of advance payments paid for three reporting periods is 8621 rubles (4373 + 2499 + 1749). It exceeds the calculated amount of property tax for the year.

As can be seen from the above calculation, at the end of the tax period the company has an overpayment. Moreover, it is obvious that it was formed based on the results of the advance payment for six months, and the advance payment for 9 months increased it even more.

However, in order to reimburse this amount from the budget, you will have to wait until the end of the tax period, submit a declaration, wait for the end of the desk audit, and only then will you be able to get the funds back. Thus, for a significant period of time, funds were withdrawn from the company’s turnover to pay advance payments for property taxes. If the tax is calculated on property of greater value, the company's losses may be more significant.

Submitting a declaration in the middle of the year is not prohibited

The Federal Tax Service of Russia, in letter No. BS-4-11/13835 dated July 30, 2013, explained that taxpayers have the right to fulfill the obligation to submit a declaration and pay tax ahead of schedule. This does not contradict the requirements established in paragraph 2 of paragraph 1 of Article 45 of the Tax Code of the Russian Federation regarding the timely payment of tax.

From this point of view, the procedure for calculating property tax is very convenient; it does not provide for separate provisions for calculating the average annual or average value of property depending on the number of months actually worked by the company in the reporting or tax period, as well as the months during which the property was an object taxation. Based on this, when determining the average annual and average value of property, the general procedure is applied (clause 4 of Article 376 of the Tax Code of the Russian Federation). When calculating the amount of the average annual and average value of property, a fixed number of months in the reporting and tax periods is taken into account - three, six, nine and twelve, respectively (Article 379 of the Tax Code of the Russian Federation, see also letter of the Ministry of Finance of Russia dated February 24, 2012 No. 07-02-06/ 28). Therefore, if all fixed assets are disposed of during the tax period, the company can calculate the final tax amount. And he has the right to submit a tax return for property tax in relation to the disposed object during the calendar year before the deadline for its submission established in paragraph 3 of Article 386 of the Tax Code of the Russian Federation, and to pay the amount of tax.

on the numbers

Let's use the example data. For the first quarter, advance payments are paid in accordance with the general procedure. But since the object was disposed of in April, and the company does not plan to acquire other fixed assets that may become subject to taxation, it has the right to submit a tax return early at the end of the six months. The tax amount is calculated in the general manner, and is paid taking into account the advance payment transferred at the end of the first quarter. At the end of the six months, tax is paid in the amount of 1.01 thousand rubles (see table).

Comparative table of options for paying advance payments, thousand rubles

| Reporting/tax period | Payment for all quarters | Payment for the period of ownership | ||

| The tax base | Due | The tax base | Due | |

| Based on the results of the first quarter | 795 ((840 + 810 + 780 + 750) : (3 + 1)) | 4,37 (795 × 2,2% × 1/4) | 795 ((840 + 810 + 780 + 750) : (3 + 1)) | 4,37 (795 × 2,2% × 1/4) |

| Based on the results of the half year | 454,29 ((840 + 810 + 780 + +750 + 0 × 3) : (6 + 1)) | 2,5 (454,29 × 2,2% × 1/4) | 244,62 ((840 + 810 + 780 + 750 + 0 × 9) : (12 + 1)) | 1,01 (244,62 × 2,2% – 4,37) |

| Based on the results of 9 months | 318 ((840 + 810 + 780 + 750 + 0 × 6) : (9 + 1)) | 1,75 (318 × 2,2% × 1/4) | 0 | 0 |

| Based on the results of the tax period | 244,62 ((840 + 810 + 780 + 750 + 0 × 9) / (12 + 1)) | –3,24 (244,62 × 2,2% – 5,38 – 4,37 – 2,5 – 1,75) | 0 | 0 |

As can be seen from the table, if the declaration is submitted ahead of schedule, the company will pay an amount at the end of the six months that is significantly less than it would have paid as an advance payment. And after 9 months, advance payments are no longer paid, and the company does not have any overpayments. The tax benefits of this method of reporting are obvious.

The Federal Tax Service of Russia only warns about the riskiness of such a step if the company, before the end of the tax period, acquires new fixed assets that will be subject to taxation. Then she will have to retake tax calculations for earlier reporting periods (Article 81 of the Tax Code of the Russian Federation), calculating the tax base for all, even retired objects, since there are no exceptions to the calculation procedure for such situations. This means that the company will have arrears in property taxes. Along with it, an obligation to pay a penalty will arise (Article 75 of the Tax Code of the Russian Federation). In addition, for late submission of calculations, the company will be fined in the amount of 200 rubles (clause 1 of Article 126 of the Tax Code of the Russian Federation). But we note that these risks may be partly justified if the company saves significant amounts (in the event of disposal of expensive property at the beginning or middle of the year), and the acquisition of other taxable objects is planned, for example, at the end of the year.

The calculation of property tax for a tax period does not depend on the number of months in it

To determine the amount of property tax, the average annual value of the property is multiplied by the tax rate (Clause 1, Article 382 of the Tax Code of the Russian Federation). The procedure for calculating the average annual value of property for the tax period is established by Article 376 of the Tax Code of the Russian Federation. According to paragraph 2 of clause 4 of this article, the total residual value of the property is calculated on the 1st day of each month of the tax period and the last day of the tax period. The resulting amount is divided by the number of months in the tax period, increased by one. Thus, the average annual value of the property is the quotient of dividing the resulting total residual value by 13 (12 + 1).

Let's assume that the company owns a car that was put into operation in 2012. It was taken into account as part of fixed assets, which means it was subject to property tax (clause 1 of Article 374 of the Tax Code of the Russian Federation). The company sold this car to its employee and immediately bought a new car. Since the movable property was put into operation after January 1, 2014, it is no longer subject to property tax (subclause 8, clause 4, article 374 of the Tax Code of the Russian Federation). The company has no other taxable objects.

on the numbers

The residual value of the car as of January 1, February 1, March 1 and April 1, respectively, is equal to 840 thousand rubles, 810 thousand, 780 thousand and 750 thousand rubles. The car was sold on April 1, so as of May 1, the residual value is 0. The company pays corporate property tax at a rate of 2.2 percent. The amount of property tax for the year is equal to 5382 rubles ((840 thousand + 810 thousand + 780 thousand + 750 thousand + 0 × 9) : (12 + 1) × 2.2%).