Who must submit the 6-NDFL report and when?

The 6-NDFL report is submitted every quarter and at the end of the year, all firms and individual entrepreneurs with employees are tax agents. The report reflects information about personal income tax accrued and withheld from salaries.

If the salary has not been accrued, there is no obligation to withhold income tax and submit a report. Send the tax office a letter stating that you are not a tax agent, so that they do not expect a report from you and do not block your current account for being late.

The deadlines for submitting 6-NDFL for the year are established by clause 2 of Art. 230 Tax Code of the Russian Federation. Submit calculations for the 1st quarter, half a year and 9 months no later than the last day of the month following the reporting period. Annual calculation - until March 1 of the year following the reporting year.

- For 2021 - until March 1, 2021;

- For the 1st quarter of 2021 - until April 30, 2021;

- For the first half of 2021 - until August 2, 2021;

- For 9 months 2021 - until November 1, 2021;

- For 2021 - until March 1, 2022.

Form 6-NDFL is submitted to the tax office at the place of registration. This can be done electronically via the Internet. Only tax agents whose number of employees during the tax period did not exceed 10 people have the right to submit a paper version.

New deadlines for reporting and paying taxes: postponement to 2020 due to coronavirus

The government has approved deferments for tax payments and reporting due to the coronavirus epidemic. Resolution No. 409 dated 04/02/2020 was published on Monday, April 6.

Please note that postponing the submission of the declaration does not automatically mean postponing the tax payment, even if the payment deadline is tied to the deadline for submitting the report. This is directly stated in the resolution.

What was extended according to reports

- The deadline for submitting all tax and accounting reports, the due date of which falls on March-May for three months. Except VAT.

- VAT reporting for the 1st quarter until May 15.

- The deadline for submitting insurance premium payments is May 15.

Deadlines for submitting reports have been postponed for all organizations and individual entrepreneurs, regardless of the type of activity, lists and registers of SMEs.

And for citizens too (3-NDFL).

New reporting deadlines in 2021

The Ministry of Finance explained for whom the deadline for submitting accounting reports is June 30. Therefore, the deadline is May 6.

| Reporting type | Last day for submitting the report |

| Accounting statements for 2021 | 12 May |

| Income tax for 2021 | June 29 |

| Income tax for the 1st quarter of 2021 | July 28th |

| Income tax for March 2021 (if paid monthly) | July 28th |

| Income tax for April 2021 (if paid monthly) | August 28 |

| Income tax for May 2021 (if paid monthly) | September 28 |

| Property tax for 2021 | 30 June |

| VAT for the 1st quarter of 2021 | May 15 |

| Calculation of insurance premiums for the 1st quarter of 2021 | May 15 |

| 6-NDFL for the 1st quarter of 2021 | July 30 |

| STS for 2021 (organizations) | 30 June |

| STS for 2021 (IP) | July 30 |

| UTII for the 1st quarter of 2021 | July 20 |

| 3-NDFL | July 30 |

| 4-FSS | May 15 |

Postponement of tax payment deadlines

Tax deferrals will not be provided to all organizations and individual entrepreneurs, but only to those included in the register of small and medium-sized businesses and engaged in activities included in the government’s list (the most affected industries). Read more about the transfer in the article New deadlines for taxes and reporting. The government approved deferments, but not for everyone.

Organizations specified in paragraph 2 of the Presidential Decree that are required to work on non-working days are highlighted in a separate column. According to the Federal Tax Service, they were required to submit reports within the usual deadlines, because these organizations have working days. This means, by this logic, they are obliged to pay taxes also within the usual time limits.

| Taxes/fees | Organizations and individual entrepreneurs - SMEs from the list of affected industries | Those working on non-working days according to the Presidential Decree and not included in the list of affected industries | Other organizations and individual entrepreneurs |

| 1 | 2 | 3 | 4 |

| Income tax for 2021 | September 28 | 30th of March | 12 May |

| Income tax for the 1st quarter of 2021 | 28 of October | April 28 | 12 May |

| Income tax for March 2021 (if paid monthly) | 28 of October | April 28 | 12 May |

| Income tax for April 2021 (if paid monthly) | September 28 | May 28 | May 28 |

| Income tax for May 2021 (if paid monthly) | 28 of October | June 29 | June 29 |

| Property tax for 2021 | 12 May | 30th of March | 12 May |

| Property tax for the 1st quarter of 2021 | October 30 | April 30 | 12 May |

| Property tax for the 2nd quarter of 2021 | December 30th | July 30 | July 30 |

| Transport and land taxes for the 1st quarter of 2021 | October 30 | Within the time limits established by regional and local laws | Within the time limits established by regional and local laws |

| Transport and land taxes for the 2nd quarter of 2021 | December 30th | Within the time limits established by regional and local laws | Within the time limits established by regional and local laws |

| VAT for the 1st quarter of 2021 |

|

|

|

| Insurance premiums for March 2021, including for industrial injuries | October 15 | April 15 | 12 May |

| Insurance premiums for April 2021, including for industrial injuries | November 16 | May 15 | May 15 |

| Insurance premiums for May 2021, including for work-related injuries | December 15 | June 15 | June 15 |

| Insurance premiums for June 2021, including for work-related injuries | November 16 | July 15 | July 15 |

| Insurance premiums for July 2021, including for industrial injuries | December 15 | August 17 | August 17 |

| STS for 2021 (organizations) | September 30th | March 31 | 12 May |

| STS for 2021 (IP) | October 31 | April 30 | 12 May |

| simplified tax system for the 1st quarter of 2021 | October 26 | April 27 | 12 May |

| simplified tax system for the 2nd quarter of 2021 | November 25 | July 27 | July 27 |

| Unified agricultural tax for 2021 | September 30th | March 31 | 12 May |

| Unified agricultural tax for the 1st half of 2021 | November 25 | July 27 | July 27 |

| UTII for the 1st quarter of 2021 | October 26 | April 27 | 12 May |

| UTII for the 2nd quarter of 2021 | November 25 | July 27 | July 27 |

| PSN for payment dates falling in the 2nd quarter of 2021 | postponement by 4 months | no transfer | no transfer |

| Personal income tax for 2021 (individual entrepreneurs, notaries, lawyers) | October 15 | July 15 | July 15 |

| Insurance premiums for individual entrepreneurs in the amount of 1% on income over 300 thousand rubles | Nov. 1 | July 1 | July 1 |

___________

Report 6-NDFL for 2021

In 2021, the version of form 6-NDFL, approved by Order of the Federal Tax Service dated January 17, 2018 No. MMV-7-11/18, is in effect. Starting from the first quarter of 2021, Form 6-NDFL will change; we will describe how to fill out the new calculation below.

Report form 6-NDFL for 2021 consists of:

- title page;

- section No. 1 with generalized indicators;

- section No. 2 with the dates and amounts of income actually received and personal income tax that needs to be withheld.

Filling out the title page

Enter the tax identification number and checkpoint of the organization submitting the report. If the report is submitted by a branch, then you need to enter the branch checkpoint. Entrepreneurs, lawyers, and notaries enter only the TIN.

In the line “Reporting period (code)” enter the code:

- 1st quarter 2021 - 21;

- 2 quarters (6 months) of 2021 - 31;

- 3 quarters (9 months) of 2021 - 33;

- 12 months - 34.

The tax period in this case is the reporting year “2020”.

In the “Adjustment number” field, enter “000” - if this is the first report, “001” - if this is a report after clarification, “002” - the second clarification, etc.;

“By location (code)”: code of the tax authority at the place of registration of the business. The first two digits indicate the region code, the second two indicate the code of your Federal Tax Service.

Code by location (accounting) in accordance with Appendix 2 to the filling procedure: write 120 for individual entrepreneurs, 214 for organizations, 220 for separate divisions.

We indicate the abbreviated name of your organization (if it has one) and its legal form. If you are an individual entrepreneur, you must provide your full name. Enter the OKTMO code (municipal body) in whose territory your company was registered.

Important! All lines on the title and other pages are filled in with either values or dashes. You cannot indicate negative amounts in 6-NDFL.

Filling out section No. 1

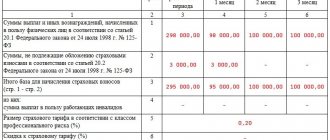

The data in this section is filled in with a cumulative total from the beginning of the year and is taken from each 6-NDFL certificate. For each bet, you need to calculate a separate cumulative total and fill out a separate section 1.

- 010: first enter the tax rate (13%). If several tax rates were used during the reporting period, you need to compile the same number of copies of the first section. Please indicate each bet in field 010;

- 020: we enter all taxable income of employees in increasing amounts from the beginning of the year. When filling out, we focus on the date of receipt of income for personal income tax purposes, and not on the accrual date. In line 020, do not include completely non-taxable income and income of employees that are below the taxable limit, for example, financial assistance in the amount of 2,000 rubles. Dividends paid must be reflected in line 025.

- 030: we record standard, property, social, professional and investment tax deductions, if they are due to employees, on an accrual basis from the beginning of the year. Immediately indicate other amounts that reduce the tax base under Art. 217 of the Tax Code of the Russian Federation, if income is exempt from tax within the standard.

- 040: this paragraph contains the calculated personal income tax. 040 = 010 × (020 – 030). On line 045, highlight the personal income tax accrued on dividends since the beginning of the year.

- 050: enter the amount of fixed advances paid to foreign employees. If you don’t have them, write 0. This amount cannot be more than the amount of the calculated tax.

- 060: we record the number of employees who have received income since the beginning of the reporting year. It is necessary to indicate the real number of income recipients, and not just those with whom an employment contract has been concluded. If one person gets a job with you twice in a year or receives income at different rates, he appears as one income recipient.

- 070: write the total amount of taxes that were withheld for 2020. Note that lines 070 and 040 may not be the same. This may not be a mistake: it’s just that sometimes taxes can be accrued earlier than they are withheld from employees.

- 080: we pay all non-withheld personal income tax amounts for the year.

- 090: returned tax that was over-withheld or recalculated at the end of the tax period. It doesn't matter when the tax was withheld.

Filling out section No. 2

This section contains information for the latest period: time of payment of income to employees, transfer of personal income tax. Transfer dates are indicated in chronological order. Let's look at the lines in this section individually:

- 100: we write the day when employees actually received income. If there were several transfers for one employee that day, they must be summed up. The transfer date depends on the type of payment to the employee. If this is a salary, then it will become the employee’s income on the last day of the month of its transfer. That is, you can indicate, for example, May 31, but the person will receive their salary in June. In this case, vacation pay and sick pay will become income on the day the employee receives them. The day of payment of financial assistance is also the day of receipt/transfer of income.

- 110: write the day, month and year when the tax was withheld. Personal income tax for an employee from vacation pay, wages, sick leave, financial assistance (from the taxable part), remuneration for work and services, as well as other payments in favor of the employee must be withheld on the day the income is transferred.

- 120: in this line we write the date of transfer of personal income tax to the state budget. As a rule, this is the day that follows the payment day. But, for example, for sick leave and vacation pay - the last day of the month in which the money was paid.

- 130: we write income before personal income tax was withheld, received on the date indicated in line 100.

- 140: indicate the personal income tax required for withholding, take the date from each line 110.

If different types of income were received on the same date, for which the transfer deadlines differ, then lines 100-140 are filled in for each transfer deadline separately.

If the tax base has been reduced by the amount of tax deductions, then the tax must be reflected taking into account the deductions. The personal income tax amount on line 140 must be equal to the amount paid to the budget.

New form of calculation of 6-NDFL in 2021

As of the report for the 1st quarter of 2021, a new form 6-NDFL, approved by order of the Federal Tax Service dated October 15, 2020 No. ED-7-11/753, is in effect. The report has undergone major changes in both structure and content. It now includes:

- Title page;

- Section 1 “Data on tax agent obligations”;

- Section 2 “Calculation of calculated, withheld and transferred personal income tax amounts”;

- Appendix 1 “Certificate of income and tax amounts of an individual” is an analogue of the former 2-NDFL.

The title page contains mostly technical edits. And sections 1 and 2 in the new form, in fact, have been swapped: now section 1 reflects information about the amounts and timing of personal income tax transfers, and section 2 contains generalized information. Another very important change is the inclusion of a 2-NDFL certificate in the calculation. It is no longer necessary to submit it separately, but as part of the calculation it is filled out once a year. There are also changes to the certificate form. Let's look at the procedure for filling out a new report.

Filling out the title page

The title page and the procedure for filling it out are almost the same as the title page from the previous form. Only the names of some fields have changed:

| Was | It became |

| Submission period (code) | Reporting period (code) |

| Tax period (year) | Calendar year |

| Reorganization (liquidation) form (code) | Form of reorganization (liquidation) (code)/Deprivation of powers (closing) of a separate division (code) |

| TIN/KPP of the reorganized organization | TIN/KPP of a reorganized organization/TIN/KPP of a deprived (closed) separate division |

Also, to deprive authorities or close a separate unit, a special code was introduced - “9”.

Filling out Section No. 1

In the first section, we indicate the timing of tax transfers and the amount of tax withheld for the last three months. For example, in a six-month calculation this would be April, May and June. Let's look at it line by line.

- 010: indicate the BCC for tax. You can view the KBK for personal income tax in the Kontur.Accounting directory.

- 020: the amount of tax that was withheld over the last three months, generalized for all employees.

- 021: date no later than which the withheld tax must be transferred to the budget.

- 022: the generalized amount of withheld tax that must be paid to the budget on the date specified in field 021.

Note! The tax amount in field 020 must be equal to the sum of the values of all fields 022. And there must be exactly the same number of fields 022 as fields 021. Similar rules apply for the returned personal income tax from fields 030–032.

- 030: we indicate the generalized amount of personal income tax that was returned to employees over the last three months in accordance with Art. 231 Tax Code of the Russian Federation.

- 031: indicate the return date.

- 032: indicate the refund amount on each date from field 031.

As you can see, now you do not need to indicate the date of actual receipt of income, the date of withholding and the amount of income actually received. Often it is in these fields that confusion has arisen that will finally stop.

Filling out section No. 2

The second section summarizes the amounts of accrued income, calculated and withheld taxes for all individuals. Data are provided from the beginning of the tax period on an accrual basis. For each personal income tax rate, a separate section 2 is filled out. Let’s look at the order of filling out the fields:

- 100: enter the tax rate. If you withhold personal income tax at different rates, then each of them will need its own section 2.

- 105: KBK for personal income tax. You can find out KBK in the Kontur.Accounting directory.

- 110: income generalized for all individuals, accrued from the beginning of the year. In field 111 we indicate data on dividends, in field 112 - on employment contracts, and in field 113 - on GPC agreements for the provision of services or performance of work. The sum of lines 111–113 should be equal to line 110.

- 120: indicate the number of individuals who received taxable income in the reporting period. Indicate all income recipients, and not just those with whom you entered into an employment or civil contract. If one person quits and gets a job again, he is counted as one person. The same applies to individuals who receive income taxed at different rates.

- 130: we indicate the cumulative total of deductions for all individuals from January 1.

- 140: we indicate the generalized calculated tax from the beginning of the year, and in line 141 we additionally highlight the tax on dividends.

- 150: enter the generalized amount of fixed advances, which reduce the amount of calculated tax from line 140.

- 160: we calculate the total amount of tax withheld since the beginning of the year.

- 170: reflect taxes not withheld.

- 180: reflect taxes withheld excessively,

- 190: the total amount of tax returned to taxpayers in accordance with Art. 231 Tax Code of the Russian Federation.

Of the new fields - 112, 113 and 190. Everything else has remained virtually unchanged compared to Section 1 of the 6-NDFL form, which was in force in 2020.

We fill out Appendix No. 1 “Certificate of income and tax amounts of an individual”

We fill out the certificate only when making calculations for a full year. The first time this must be done is by March 2022. The certificate includes information about the income of individuals in the past year, the amount of personal income tax accrued, withheld and paid to the budget, as well as about unwithheld taxes.

The help includes 4 sections:

- Section 1 “Data about the individual - recipient of income.” In it, indicate the TIN, full name, date of birth and passport details of the income recipient. In the “Taxpayer status” field, indicate the appropriate code: “1” - for residents of the Russian Federation, “2” - for non-residents, “3” - for highly qualified non-resident specialists, etc.

- Section 2 “Total amounts of income and tax based on the results of the tax period.” Fill out as many sections 2 as the rates applied to the income received by an individual. Enter the tax rate, total income without deductions, calculated, withheld and transferred tax amount. If part of the tax was withheld excessively, enter it in the appropriate line.

- Section 3 “Standard, social and property tax deductions.” Provide information about the deductions you provide as a tax agent and about notifications issued by the tax office. Enter all deduction codes and corresponding amounts. Next, enter information about tax notices.

- Section 4 “The amount of income from which tax is not withheld and the amount of tax not withheld.” Here we indicate the amount of income from which tax was not withheld, and the amount of calculated tax at the appropriate rate.

In the appendix to the certificate we indicate information about income accrued and actually received by an individual in cash and in kind, as well as in the form of material benefits, and deductions. Separate them by month.

If the calculation needs to be adjusted, the updated form can be submitted without attachments with certificates. If you need to change the information in the certificates, you need to submit the entire calculation.

Fines for 6-NDFL

Late fees. According to clause 1.2 of Art. 126 of the Tax Code of the Russian Federation, for each month (full/partial) of delay, the tax agent (NA) must pay 1,000 rubles, regardless of the period of the year. The delay begins from the day when the agent was supposed to submit tax calculations. For example, you are 2 months and 3 days late in filing 6-NDFL. Your fine = 3 × 1,000 = 3,000 rubles.

The tax office usually does not wait for the results of a desk audit and imposes a fine within 10 working days from the date the delay began. In addition to fines, the tax office can “freeze” bank accounts and financial transactions of the debtor.

Penalties for errors. If you submit a report on time, but with errors, for each “damaged” report you are entitled to a fine of 500 rubles. However, if the tax inspectors see an error, but you manage to submit a correct report, you will not be fined. Since 2017, you can also be forgiven for mistakes in some cases: for example, if you did not underestimate the tax, did not create adverse consequences for the budget, or did not violate the rights of individuals.

Not only the entire organization, but also responsible employees - the manager, the accountant - can be held accountable. Officials face a fine of 300 to 500 rubles.

Easily prepare and submit 6-NDFL online using the online service Kontur.Accounting. The declaration is generated automatically based on accounting and is checked before sending. Get rid of routine, submit reports and benefit from the support of our service experts. For the first two weeks, new users work in the service for free. For new LLCs, the gift is 3 free months of work and reporting.

Changes in document content

Starting from the 2021 calendar year, reporting acts for 2021 are submitted according to a modified format. The exact list of changes to 6-NDFL, deadlines for 2018 can be found on the Federal Tax Service website. The updated version of the form is presented:

- title - a sheet without numbering;

- barcode with the numeric value 15202024;

- changed sequence of filling out reports.

Now tax agents can provide forms in person, send them by e-mail or via TKS through an operator on duty.