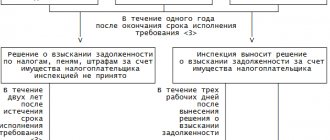

As in other cities, in Moscow and St. Petersburg, every individual who is a taxpayer is obliged to regularly transfer tax funds under the KBK code 18210601010031000110 for existing real estate.

At the moment, a taxpayer under Article 401 of the Code is an individual who has ownership rights to one of the types of real estate. Also, Article 401 of the Code states that real estate includes objects with residential status. Also on the list of objects eligible for taxation are a garage and an unfinished building. Based on the type and classification of the object itself, a certain rate is applied to the amount of tax.

KBK 18210601030131000110 transcript

PSN tax (patent)182 1 0500 110 Property tax for individuals - on properties located on the territory of municipal districts182 1 0600 110 Land tax on organizations - on sites located on the territory of municipal districts182 1 0600 110 Land tax on individuals - on sites that located on the territory of municipal districts182 1 0600 110| NAME OF TAX, FEE, PAYMENT | KBK 2021 |

| Corporate income tax (except for corporate tax), including: | |

| 182 1 0100 110 |

| 182 1 0100 110 |

| VAT | 182 1 0300 110 |

| Property tax: | |

| 182 1 0600 110 |

| 182 1 0600 110 |

| Personal income tax (individual entrepreneur “for yourself”) | 182 1 0100 110 |

| NAME OF TAX, FEE, PAYMENT | KBK 2021 |

| Personal income tax on income sourced by a tax agent | 182 1 0100 110 |

| VAT (as tax agent) | 182 1 0300 110 |

| VAT on imports from Belarus and Kazakhstan | 182 1 0400 110 |

| Income tax on dividend payments: | |

| 182 1 0100 110 |

| 182 1 0100 110 |

| Income tax on the payment of income to foreign organizations (except for dividends and interest on state and municipal securities) | 182 1 0100 110 |

| Income tax on income from state and municipal securities | 182 1 0100 110 |

| Income tax on dividends received from foreign organizations | 182 1 0100 110 |

| Transport tax | 182 1 0600 110 |

| Land tax | 182 1 06 0603х хх 1000 110 where xxx depends on the location of the land plot |

| Water tax | 182 1 0700 110 |

| Fee for negative environmental impact (NEI) | 048 1 12 010x0 01 6000 120 where x depends on the type of environmental pollution |

| MET | 182 1 07 010хх 01 1000 110 where хх depends on the type of mineral being mined |

| Corporate income tax on income in the form of profits of controlled foreign companies (CFC) | 182 1 0100 110 |

New KBK 2021

13 new BCCs have been officially approved for 2021. Nine for taxes and excise taxes, two for state duties, one for property taxes of individuals (Federal Law No. 459-FZ dated November 29, 2018, Order of the Ministry of Finance dated September 20, 2018 No. 198n). The complete list is in the table.

| Payment Description | KBK |

| Excise tax on dark marine fuel imported into Russia | 153 1 0400 110 |

| Excise tax on crude oil sent for processing | 182 1 0300 110 |

| Excise tax on dark marine fuel produced in the Russian Federation | 182 1 0300 110 |

| Excise tax on dark marine fuel imported into the Russian Federation | 182 1 0400 110 |

| Income tax on the implementation of agreements on the development of oil and gas fields located in the Far Eastern Federal District, under the terms of production sharing agreements, credited to the budgets of the constituent entities of the Russian Federation | 182 1 0100 110 |

| Tax on additional income from the extraction of hydrocarbons on subsoil plots located wholly or partially in the territories specified in subparagraph 1 of paragraph 1 of Article 333.45 of the Tax Code | 182 1 0700 110 |

| Tax on additional income from the extraction of hydrocarbons on subsoil plots located wholly or partially in the territories specified in subparagraph 2 of paragraph 1 of Article 333.45 of the Tax Code | 182 1 0700 110 |

| Tax on additional income from the extraction of hydrocarbons on subsoil plots located wholly or partially in the territories specified in subparagraph 3 of paragraph 1 of Article 333.45 of the Tax Code | 182 1 0700 110 |

| Tax on additional income from the extraction of hydrocarbons on subsoil plots located wholly or partially in the territories specified in subparagraph 4 of paragraph 1 of Article 333.45 of the Tax Code | 182 1 0700 110 |

| State duty for issuing excise stamps with a two-dimensional bar code containing the EGAIS identifier | 153 1 0800 110 |

| State duty for the issuance of federal special stamps with a two-dimensional bar code containing the EGAIS identifier | 160 1 0800 110 |

| Single tax payment of an individual | 182 1 0600 110 |

KBK 2021 - 182 1 06 06 031 03 1000 110

Tax on property not included in the unified gas supply system

| KBK | Payment Description |

| 182 1 0600 110 | payment amount (recalculations, arrears and payment arrears, including canceled ones) |

| 182 1 0600 110 | penalty on payment |

| 182 1 0600 110 | interest on payment |

| 182 1 0600 110 | amounts of monetary penalties (fines) for payment |

Tax on property included in the unified gas supply system

| KBK | Payment Description |

| 182 1 0600 110 | payment amount (recalculations, arrears and payment arrears, including canceled ones) |

| 182 1 0600 110 | penalty on payment |

| 182 1 0600 110 | interest on payment |

| 182 1 0600 110 | amounts of monetary penalties (fines) for payment |

Property tax on objects located within the boundaries of intra-city municipalities of federal cities

| KBK | Payment Description |

| 182 1 0600 110 | payment amount (recalculations, arrears and payment arrears, including canceled ones) |

| 182 1 0600 110 | penalty on payment |

| 182 1 0600 110 | interest on payment |

| 182 1 0600 110 | amounts of monetary penalties (fines) for payment |

Tax on objects located within the boundaries of urban districts

| KBK | Payment Description |

| 182 1 0600 110 | payment amount (recalculations, arrears and payment arrears, including canceled ones) |

| 182 1 0600 110 | penalty on payment |

| 182 1 0600 110 | interest on payment |

| 182 1 0600 110 | amounts of monetary penalties (fines) for payment |

Tax on objects located within the boundaries of urban districts with intracity division

| KBK | Payment Description |

| 182 1 0600 110 | payment amount (recalculations, arrears and payment arrears, including canceled ones) |

| 182 1 0600 110 | penalty on payment |

| 182 1 0600 110 | interest on payment |

| 182 1 0600 110 | amounts of monetary penalties (fines) for payment |

Tax on objects located within the boundaries of intracity districts

| KBK | Payment Description |

| 182 1 0600 110 | payment amount (recalculations, arrears and payment arrears, including canceled ones) |

| 182 1 0600 110 | penalty on payment |

| 182 1 0600 110 | interest on payment |

| 182 1 0600 110 | amounts of monetary penalties (fines) for payment |

Tax on objects located within the boundaries of municipal districts

| KBK | Payment Description |

| 182 1 0600 110 | payment amount (recalculations, arrears and payment arrears, including canceled ones) |

| 182 1 0600 110 | penalty on payment |

| 182 1 0600 110 | interest on payment |

| 182 1 0600 110 | amounts of monetary penalties (fines) for payment |

Tax on objects located within the boundaries of inter-settlement territories

| KBK | Payment Description |

| 182 1 0600 110 | payment amount (recalculations, arrears and payment arrears, including canceled ones) |

| 182 1 0600 110 | penalty on payment |

| 182 1 0600 110 | interest on payment |

| 182 1 0600 110 | amounts of monetary penalties (fines) for payment |

Tax on objects located within the boundaries of rural settlements

| KBK | Payment Description |

| 182 1 0600 110 | payment amount (recalculations, arrears and payment arrears, including canceled ones) |

| 182 1 0600 110 | penalty on payment |

| 182 1 0600 110 | interest on payment) |

| 182 1 0600 110 | amounts of monetary penalties (fines) for payment |

From 2021 there are some changes to the BCC. In particular:

- approved by the KBK for a 15% personal income tax calculated on income exceeding 5 million rubles - 182 1 0100 110;

- KBK was introduced for payment of land tax in relation to plots located within the boundaries of municipal districts, it is necessary to transfer to KBK 182 1 0600 110;

- BCC appeared to pay the tax levied in connection with the use of PSN, credited to the budgets of municipal districts - 182 1 0500 110;

- The BCC was introduced for the payment of mineral extraction tax on the extraction of other minerals, in respect of which a rental coefficient other than 1 is established for taxation, - 182 1 07 01080 01 1000 110.

BCCs for basic taxes/contributions remained unchanged.

Below you will find tables with the BCC for 2021 for basic taxes and insurance premiums.

KBK for paying taxes for organizations and individual entrepreneurs on OSN

| Name of tax, fee, payment | KBK |

| Corporate income tax (except for corporate tax), including: | |

| — to the federal budget (rate — 3%) | 182 1 0100 110 |

| — to the regional budget (rate from 12.5% to 17%) | 182 1 0100 110 |

| VAT | 182 1 0300 110 |

| Property tax: | |

| - for any property, with the exception of those included in the Unified Gas Supply System (USGS) | 182 1 0600 110 |

| - for property included in the Unified State Social System | 182 1 0600 110 |

| Personal income tax (individual entrepreneur “for yourself”) | 182 1 0100 110 |

| Name of tax, fee, payment | KBK |

| Personal income tax on income the source of which is a tax agent | 182 1 0100 110 |

| VAT (as tax agent) | 182 1 0300 110 |

| VAT on imports from Belarus and Kazakhstan | 182 1 0400 110 |

| Income tax on dividend payments: | |

| — Russian organizations | 182 1 0100 110 |

| - foreign organizations | 182 1 0100 110 |

| Income tax on the payment of income to foreign organizations (except for dividends and interest on state and municipal securities) | 182 1 0100 110 |

| Income tax on income from state and municipal securities | 182 1 0100 110 |

| Income tax on dividends received from foreign organizations | 182 1 0100 110 |

| Transport tax | 182 1 0600 110 |

| Land tax | 182 1 06 0603х хх 1000 110 where xxx depends on the location of the land plot |

| Water tax | 182 1 0700 110 |

| Payment for negative impact on the environment | 048 1 12 010x0 01 6000 120 where x depends on the type of environmental pollution |

| MET | 182 1 07 010хх 01 1000 110 where хх depends on the type of mineral being mined |

| Corporate income tax on income in the form of profits of controlled foreign companies | 182 1 0100 110 |

Our KBK table in 2020-2021 reflects information regarding insurance premium codes that are most in demand among payers.

KBK for insurance premiums for employees

| Payment type | KBK | ||

| Contributions accrued for periods before 2021, paid after 01/01/2017 | Contributions for 2017-2021 | ||

| Contributions to compulsory pension insurance | contributions | 182 1 0200 160 | 182 1 0210 160 |

| penalties | 182 1 0200 160 | 182 1 0210 160 | |

| fine | 182 1 0200 160 | 182 1 0210 160 | |

| Contributions to compulsory social insurance | contributions | 182 1 0200 160 | 182 1 0210 160 |

| penalties | 182 1 0200 160 | 182 1 0210 160 | |

| fine | 182 1 0200 160 | 182 1 0210 160 | |

| Contributions for compulsory health insurance | contributions | 182 1 0211 160 | 182 1 0213 160 |

| penalties | 182 1 0211 160 | 182 1 0213 160 | |

| fine | 182 1 0211 160 | 182 1 0213 160 | |

| Contributions for injuries | contributions | 393 1 0200 160 | |

| penalties | 393 1 0200 160 | ||

| fine | 393 1 0200 160 | ||

KBK for insurance premiums of individual entrepreneurs

| Payment type | KBK | ||

| Contributions accrued for periods before 2021, paid after 01/01/2017 | Contributions for 2017-2021 | ||

| Fixed contributions to the Pension Fund, including contributions | contributions | 182 1 0200 160 | 182 1 0210 160* *Unified BCC for the fixed part and contributions from income over 300,000 rubles. valid from 04/23/2018 |

| Contributions to the Pension Fund of the Russian Federation 1% on income over 300,000 rubles. | contributions | 182 1 0200 160 | |

| penalties | 182 1 0200 160 | 182 1 0210 160 | |

| fine | 182 1 0200 160 | 182 1 0210 160 | |

| Contributions for compulsory health insurance | contributions | 182 1 0211 160 | 182 1 0213 160 |

| penalties | 182 1 0211 160 | 182 1 0213 160 | |

| fine | 182 1 0211 160 | 182 1 0213 160 | |

You can download the KBK table for penalties and fines for contributions to compulsory pension insurance at additional tariffs here.

The BCCs for the taxes indicated in the tables below have not changed in recent years (the same for 2021 and 2021). So that you can easily and quickly find the CBC you need (among the most popular ones), we have divided them into groups:

KBK table for personal income tax for 2020-2021

| Personal income tax on employee income | 182 1 0100 110 |

| Penalties for personal income tax on employee income | 182 1 0100 110 |

| Personal income tax fine on employee income | 182 1 0100 110 |

| Personal income tax on individual entrepreneur income on OSNO | 182 1 0100 110 |

| Penalties for personal income tax on income of individual entrepreneurs on OSNO | 182 1 0100 110 |

| Personal income tax fine on income of individual entrepreneurs on OSNO | 182 1 0100 110 |

KBK income tax table

| Purpose of payment | Mandatory payment | Penalty | Fine |

| To the federal budget (except for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| To the budgets of the constituent entities of the Russian Federation (except for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| To the federal budget (for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| To the budgets of the constituent entities of the Russian Federation (for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 11 |

| When implementing production sharing agreements concluded before October 21, 2011 (before the law of December 30, 1995 No. 225-FZ came into force) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the income of foreign organizations not related to activities in Russia through a permanent representative office | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the income of Russian organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the income of foreign organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From dividends from foreign organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From interest on state and municipal securities | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the profits of controlled foreign companies | from the profits of controlled foreign companies | from the profits of controlled foreign companies | from the profits of controlled foreign companies |

KBK for VAT

Order of the Ministry of Finance of Russia dated June 8, 2020 No. 99n approved the following codes of the budget classification of the Russian Federation for 2021:

| Payment | Tax | Penalty | Fine |

| Contributions to compulsory pension insurance | 182 1 02 02010 06 1010 160 | 182 1 02 02010 06 2110 160 | 182 1 02 02010 06 3010 160 |

| Contributions to compulsory social insurance in case of temporary disability and in connection with maternity | 182 1 02 02090 07 1010 160 | 182 1 02 02090 07 2110 160 | 182 1 02 02090 07 3010 160 |

What are the BCCs in 2021: a single table (subject to changes)

Contributions for compulsory health insurance of the working population182 1 02 02101 08 1013 160182 1 02 02101 08 2013 160182 1 02 02101 08 3013 160 Contributions for injuries to the Social Insurance Fund393 1 0200 160393 1 0200 160393 1 0200 160В Pension Fund of Russia (fixed payment and payment on 1% income - single BCC)182 1 0210 160182 1 0210 160182 1 0210 160В Ф Compulsory Medical Insurance Fund182 1 0213 160182 1 0213 160182 1 0213 160 Personal income tax , the source of which is the tax agent, with the exception of income in respect of which the calculation and payment of tax are carried out in accordance with Articles 227, 227.1 and 228 of the Tax Code of the Russian Federation(Salary / Vacation pay / Dividends and other payments to employees)182 1 0100 110182 1 0100 110182 1 0100 110

Personal income tax on income the source of which is a tax agent exceeding 5 million rubles

182 1 0100 110 Personal income tax on income received by citizens registered as: – entrepreneurs; – private notaries; – other persons engaged in private practice in accordance with Article 227 of the Tax Code of the Russian Federation182 1 0100 110182 1 0100 110182 1 0100 110 Personal income tax on income received by citizens in accordance with Article 228 of the Tax Code of the Russian Federation182 1 0100 110182 1 0100 110182 1 0100 110NDFL in the form of fixed advance payments payments from income received by non-residents engaged in labor activities for hire from citizens on the basis of a patent in accordance with Article 227.1 of the Tax Code of the Russian Federation182 1 0100 110182 1 0100 110182 1 0100 110 VAT on goods (work, services) sold in Russia182 1 0300 110182 1 0300 110182 1 0300 110 VAT on goods imported into the territory of Russia (from the Republics of Belarus and Kazakhstan)182 1 0400 110182 1 0400 110182 1 0400 110 VAT on goods imported into the territory of Russia (payment administrator - Federal Customs Service of Russia)153 1 0400 110153 1 0400 110153 1 0400 110182 1 0100 110 tax 182 1 0100 110 penalties 182 1 0100 110 fine From excess wages 5,000,000 rublesPersonal income tax on a portion of the tax amount exceeding 650,000 rubles relating to the portion of the tax base exceeding 5,000,000 rubles

182 1 0100 110 tax182 1 0100 110 fines

182 1 0100 110 fine

For individual entrepreneurs and persons engaged in private practice, including notaries and lawyers (Article 227 of the Tax Code of the Russian Federation)This payment is paid by individual entrepreneurs from the income from their activities if they apply the general regime and private practitioners

182 1 0100 110 tax182 1 0100 110 fines

182 1 0100 110 fine

From an individual who pays the citizen independently, including from income from the sale of personal propertyFor example, from winnings, from the sale of an apartment, from income from rental property (all cases are in the article under Article 228 of the Tax Code)

182 1 0100 110 tax182 1 0100 110 fines

182 1 0100 110 fine

In the form of fixed advance payments from the income of foreigners working on the basis of a patent (Article 227.1 of the Tax Code of the Russian Federation) 182 1 0100 110 tax182 1 0100 110 fines

182 1 0100 110 fine

Budget classification codes affect the revenue and expenditure side of the Russian Federation budget. Firms, individual entrepreneurs and individuals use them when paying taxes, fees, fines, penalties to the budget or various funds, as well as when filling out declarations, i.e. they are faced only with the income section of the classification.

Let's turn to the code diagram regarding the algorithm for its construction. The first 3 digits of the code in section I of the KBK indicate the recipient of the payment. Next come the groups and subgroups; we will consider them using the example of the most frequently recurring taxes according to parts I–III of the figure.

To understand the decoding of KBK-2021, you need to refer to the order of the Ministry of Finance of the Russian Federation dated 06/06/2019 No. 86n as amended by the order of the Ministry of Finance dated 06/08/2020 No. 98n. It examines codes separately by component parts. This regulatory legal act is constantly updated by orders of the Ministry of Finance on new or canceled codes.

In order to familiarize yourself with the construction of the budget classification, let's look at the decoding of KBK 18210501021011000110 - what tax corresponds to it in 2021. And to see the differences in the numbers, let’s compare it with the decoding of KBK 18210501011011000110 - what tax can be paid in 2021 using this code.

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of urban settlements (payment amount (recalculations, arrears and debt for the corresponding payment, including canceled ones) | 182 1 0600 110 |

In simple words, KBK acts as a guarantor of reliable transfer of funds to the budget. That is, any kind of order for the payment of contributions, fines, etc. to the state budget must contain a correctly drawn up BCC. It is he who ensures that money is transferred without losses or errors in the right direction, therefore, the payer himself does not risk having unnecessary problems and fines.

An analogue of such a code is the usual settlement number of a company. When you are going to transfer funds to the company's account for the provision of certain services, you should note the settlement number to which payment will be made. Similarly, with the help of the KBK, you can credit certain funds to a specific “account” of the state.

Purpose

Thus, by correctly writing the BKB, the organization is able to:

- carry out various payment transactions without any errors or difficulties;

- track the history of the movement of company finances;

- simplify work for employees of government agencies;

- competently plan your own budget, as well as ensure management of the organization’s cash flows;

- Constantly monitor any debts under this category of payments.

Using a budget classification code is a guarantee that the required amount will ultimately reach the correct account, while the legal entity or private entrepreneur will not receive any penalties.

Decoding KBK 18210601030131000110 in 2021 and 2021

| Payment | KBK | |

| For periods up to 2021 | For the periods 2020-2021 | |

| KBK for insurance premiums for employees | ||

| Contributions to pension insurance at basic rates | ||

| Contributions | 182 1 0200 160 | 182 1 0210 160 |

| Penalty | 182 1 0200 160 | 182 1 0210 160 |

| Fines | 182 1 0200 160 | 182 1 0210 160 |

| Social insurance contributions | ||

| Contributions | 182 1 0200 160 | 182 1 0210 160 |

| Penalty | 182 1 0200 160 | 182 1 0210 160 |

| Fines | 182 1 0200 160 | 182 1 0210 160 |

| Health insurance premiums | ||

| Contributions | 182 1 0211 160 | 182 1 0213 160 |

| Penalty | 182 1 0211 160 | 182 1 0213 160 |

| Fines | 182 1 0211 160 | 182 1 0213 160 |

| Contributions to pension insurance at additional rates | ||

| The tariff does not depend on the results of SOUT | The tariff depends on the results of the SOUT | |

| For workers from List 1 | ||

| Contributions | 182 1 0210 160 | 182 1 0220 160 |

| Penalty | 182 1 0200 160 | |

| Fines | 182 1 0200 160 | |

| For workers from List 2 | ||

| Contributions | 182 1 0210 160 | 182 1 0220 160 |

| Penalty | 182 1 0200 160 | |

| Fines | 182 1 0200 160 | |

| Contributions for injuries | ||

| Contributions | 393 1 0200 160 | |

| Penalty | 393 1 0200 160 | |

| Fines | 393 1 0200 160 | |

| KBK for insurance premiums of individual entrepreneurs | ||

| Individual entrepreneur contributions to pension insurance | ||

| Fixed contributions (minimum wage × 26%) | 182 1 0200 160 | 182 1 0210 160 |

| Contributions from income over 300 thousand rubles. (1%) | 182 1 0200 160 | 182 1 0210 160 |

| Penalty | 182 1 0200 160 | 182 1 0210 160 |

| Fines | 182 1 0200 160 | 182 1 0210 160 |

| Fixed individual entrepreneur contributions for health insurance | ||

| Contributions | 182 1 0211 160 | 182 1 0213 160 |

| Penalty | 182 1 0211 160 | 182 1 0213 160 |

| Fines | 182 1 0211 160 | 182 1 0213 160 |

| Payment Description | KBK tax | KBK penalties | KBC fines |

| Income tax credited to the federal budget | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Profit tax credited to the budgets of constituent entities of the Russian Federation | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on bond income | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax upon implementation of production sharing agreements concluded before the entry into force of Law No. 225-FZ of December 30, 1995 and which do not provide for special tax rates for crediting the specified tax to the federal budget and the budgets of constituent entities of the Russian Federation | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on the income of foreign organizations not related to activities in Russia through a permanent establishment, with the exception of income in the form of dividends and interest on state and municipal securities | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Corporate income tax on income in the form of profits of controlled foreign companies | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on income received by Russian organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on income received by foreign organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on income received by Russian organizations in the form of dividends from foreign organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on income received in the form of interest on state and municipal securities | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Payment Description | KBK tax | KBK penalties | KBC fines |

| VAT on goods (work, services) sold in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| VAT on goods imported into Russia (from the Republics of Belarus and Kazakhstan) | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| VAT on goods imported into Russia (payment administrator - Federal Customs Service of Russia) | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| Payment Description | BCC for tax | BCC for penalties | KBC for fines | |

| Personal income tax on income the source of which is a tax agent, with the exception of income in respect of which the calculation and payment of tax are carried out in accordance with Art. 227, 227.1 and 228 Tax Code of the Russian Federation | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 | |

| Personal income tax on income received by citizens registered as: – entrepreneurs; – private notaries; – other persons engaged in private practice (Article 227 of the Tax Code of the Russian Federation) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 | |

| Personal income tax on income received by citizens in accordance with Art. 228 Tax Code of the Russian Federation | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 | |

| Personal income tax in the form of fixed advance payments on income received by non-residents employed by citizens on the basis of a patent (Article 227.1 of the Tax Code of the Russian Federation) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 | |

| Payment Description | BCC for tax | BCC for penalties | KBC for fines |

| Single tax under the simplified tax system on income | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Single tax under the simplified tax system on income (for tax periods expired before January 1, 2011) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Single tax under the simplified tax system on the difference between income and expenses (including the minimum tax credited to the budgets of the constituent entities of the Russian Federation) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Single tax under the simplified tax system on the difference between income and expenses (for tax periods expired before January 1, 2011) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Minimum tax under the simplified tax system (for tax periods expired before January 1, 2021) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Minimum tax under the simplified tax system (paid (collected) for tax periods expired before January 1, 2011) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

Contributions for compulsory health insurance

Contributions for compulsory health insurance of the working population18213 16018213 160182 10202 100Contributions for compulsory health insurance of the working population for 2021 and earlier periods18211 16018211 160182 10202 101 08 3011 160Fixed contributions of entrepreneurs for compulsory health insurance in 2021182 10202 1030 81013 160182 10202 10308 2113 160182 1020 21030 83013 160Fixed contributions of entrepreneurs for compulsory health insurance for 2016 and earlier periods182 10202 10308 1011 160182 10202 1 0308 2111 160182 10202 1030 83011 160

Changes in the BCC for 2021 - 2021 - table with explanation

| Payment Description | KBK tax | KBK penalties | KBC fines |

| UTII | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| UTII (for tax periods expired before January 1, 2011) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

Calculation of UTII is submitted and tax is paid quarterly. Conditions for using UTII:

- The average number of employees in the company does not exceed one hundred;

- the share of other companies in the company is not higher than 25%, excluding companies where 50% of employees have disabilities, consumer cooperation companies;

- companies and businessmen are not recognized as payers of the Unified Agricultural Tax;

- the company is not one of the largest taxpayers;

- the activity is not carried out under a simple partnership agreement;

- The area of the premises for trade or customer service hall for catering is no more than 150 square meters. m.

UTII is prohibited from using:

- when leasing gas stations;

- gas filling stations;

- educational, health and social welfare institutions providing public catering services.

UTII has the right to use companies providing services:

- household;

- public catering;

- road transport;

- ONE HUNDRED;

- retail;

- rental of places for trade.

ENVD can be combined with various taxation regimes: OSNO, patent, Unified Agricultural Tax, simplified taxation. The simultaneous use of taxation regimes for one type of activity is not permissible.

Tax is paid according to quarterly calculations. UTII payment dates:

- 04/25/18 - for the first quarter;

- 07/25/18 - for the 2nd quarter;

- 10.25.18 - for the third quarter;

- 01/25/19 - for the fourth quarter.

Tax is paid regardless of whether income was received and the company was operating or not. As long as the company is registered as an “imputed” taxpayer, payment is required and the filing of a zero declaration is not approved. The BCC UTII 2021 for legal entities is described further in the BCC section for transfers of UTII, penalties and sanctions for individual entrepreneurs for 2018–2019.

The deadlines for payment of imputation in 2021 will not change compared to 2018.

- I quarter — April 25, 2019;

- II quarter — July 25, 2019;

- III quarter — October 25, 2019;

- IV quarter — January 27, 2021.

If the day for payment coincides with a weekend, then the tax amount is paid to the budget on the next working day.

The BCC “imputation” for companies and entrepreneurs is the same. The tax base for tax calculation is the basic yield (BR). This is the monthly profitability taken as a basis per unit of physical indicator, calculated in rubles. When calculating tax, 2 coefficients are taken into account:

- K 1 - deflator coefficient, updated annually;

- K 2 is a reduction factor, numbers range from 0.005 to one.

Companies and entrepreneurs have the right to reduce the amount payable by 50% by the amount of insurance premiums paid for themselves and their employees.

BCC is reflected in the payment order in field No. 104. The following fields of the payment invoice are entered as follows:

- No. 105 - OKTMO of the municipality in which the company or individual entrepreneur is registered as a payer of “imputation”;

- No. 106 – “TP”;

- No. 107 - numbering of the quarter for which UTII is paid (“KV.01.2019”;

- № 108 – «0»;

- No. 109 - the date when the declaration of imputation was signed;

- No. 22 - “zero”. “UIN” – enter if the company (IP) pays tax at the request of the inspectorate.

- No. 110 - “Payment type” - do not enter.

Become an author

Become an expert

The standard budget classification code includes 20 digits divided into four blocks:

| First three digits | Administrator block that defines the payment attribute. |

| Next ten digits | Income block that determines the category designation of the payment being made. This block indicates the type of income, the type of transfer, as well as the compliance of income with the standards of the Budget Code. In addition, this block indicates the recipient's budget level. |

| 14-17 digits | A software block used to ensure separate accounting of receipts for penalties, taxes and all kinds of penalties. |

| Last three digits | A classification block indicating the type of profit received by government departments. |

Last year, budget classification codes were introduced that are used for:

- payment of income tax on income received in the form of interest on bonds of Russian organizations in rubles issued during the period from January 1, 2021 to December 31, 2021 (Order of the Ministry of Finance of Russia dated June 9, 2021 No. 87n);

- transfer of excise taxes on electronic cigarettes, nicotine-containing liquids and hookah tobacco (Order of the Ministry of Finance of Russia dated June 6, 2017 No. 84n).

- Tax - 182 1010109 00 1 1000 110

- Penalty - 182 1010109 001 2100 110

- Fines - 182 1010109 001 3000 110

New BCCs for paying excise taxes

On excise duty payments, the following codes must be indicated in field 104:

- 182 1030236 0010000 110 – excise taxes on electronic nicotine delivery systems produced on the territory of the Russian Federation;

- 182 1030237 0010000 110 – excise taxes on nicotine-containing liquids produced on the territory of the Russian Federation;

- 182 1030238 0010000 110 – excise taxes on tobacco (tobacco products) intended for consumption by heating, produced on the territory of the Russian Federation.

Budget Classification Codes (BCC) - Land Tax

It is much easier to check the BCC in advance not only in payment orders, but also when filling out calculations and declarations.

Last year, budget classification codes were introduced that are used for:

- payment of income tax on income received in the form of interest on bonds of Russian organizations in rubles issued during the period from January 1, 2021 to December 31, 2021 (Order of the Ministry of Finance of Russia dated June 9, 2021 No. 87n);

- transfer of excise taxes on electronic cigarettes, nicotine-containing liquids and hookah tobacco (Order of the Ministry of Finance of Russia dated June 6, 2017 No. 84n).

In order to familiarize yourself with the construction of the budget classification, let's look at the decoding of KBK 18210501021011000110 - what tax corresponds to it in 2021. And to see the differences in the numbers, let’s compare it with the decoding of KBK 18210501011011000110 - what tax can be paid in 2021 using this code.

Save 5,000 rubles when you subscribe to Simplified. Pay your bill with a 30% discount. Or pay by card on our website.

Errors when filling out a payment order can be divided into:

- Critical - which lead to non-transfer of payment to the budget (and as a result, the emergence of arrears for which penalties are charged). Such errors include (subclause 4, clause 4, article 45 of the Tax Code of the Russian Federation):

- indication of an incorrect UFC account;

- indication of the incorrect name of the bank in which the Federal Tax Service account is opened.

- Non-critical - which are not accompanied by non-transfer of payment to the budget, but can lead to the payment falling into the category of unknown.

When filling out a payment to the bank, the KBK land tax is indicated in field 104. The identifier contains 20 characters, divided into four blocks. Their decoding allows you to determine the purpose and subsequent distribution of the payment, to identify the payer and recipient of the tax.

- The first block consists of 3 characters (from 1st to 3rd). Indicates the payee. The combination “182” means the recipient is the Federal Tax Service (indicates a tax payment);

- The second consists of 10 characters (from 4th to 13th). Contains information about the financial classification of the payment

In July 1998, the Budget Code of the Russian Federation in Federal Law No. 145 first introduced the term “KBK”, used as a means of grouping the budget.

There are 20 digits in the KBK, they are divided into several blocks. Let's look at the example of KBK for paying tax under the simplified tax system “Income” - 182 1 0500 110.

This article talks about typical ways to resolve legal issues, but each case is individual. If you want to find out how to solve your particular problem, contact our consultant absolutely FREE!

KBK for payment of property tax for individuals

Contributions for compulsory social insurance against accidents at work and occupational diseases3937 1000 1603937 2100 1603937 3000 160 Contributions for compulsory social insurance in case of temporary disability and in connection with maternity in 20201827 1010 1601827 2110 1601827 30 10 160 Contributions to compulsory social insurance in case of temporary disability and in connection with maternity for 2021 and earlier182 1020 20 9007 1000 1601827 2100 1601827 3000 160 Contributions for compulsory health insurance of the working population18213 16018213 160182830 13 160 Contributions for compulsory health insurance of the working population for 2 021 and earlier periods 18211 16018211 16018211 160 Fixed contributions of entrepreneurs for compulsory health insurance in 2021182 10202 1030 81013 160182 10202 10308 2113 160182 1020 21030 83013 160Fixed contributions of entrepreneurs for compulsory health insurance for 2021 and earlier periods182 10202 10308 1011 160182 10202 1 0308 2111 160182 10202 1030 83011 160 Personal income tax on income the source of which is a tax agent, with the exception of income for which tax is calculated and paid in accordance with Articles 227, 227.1 and 228 of the Tax Code of the Russian Federation (KBK NDFL 2021 for employees for organizations and individual entrepreneurs)182 10102 0100 11000 110182 10102 0 1001 2100 110182 101 02 01001 3000 110NDFL s income received by citizens registered as: – entrepreneurs; – private notaries; – other persons engaged in private practice in accordance with Article 227 of the Tax Code of the Russian Federation182 10102 0200 1 1000 1101821 2100 1101821 3000 110 Personal income tax on income received by citizens in accordance with Article 228 of the Tax Code of the Russian Federation182 10102 0300 1 1000 110 1821 2100 1101821 3000 110 Personal income tax in the form of fixed advance payments payments from income received by non-residents engaged in labor activities for hire from citizens on the basis of a patent in accordance with Article 227.1 of the Tax Code of the Russian Federation182 10102 0400 1 1000 1101821 2100 1101821 3000 110Unified tax under the simplified tax system on income (KBK simplified tax system income 2021)182 1050 1 0 1101 1000 110182 10501 0 1101 2100 110182 10501 0 1101 3000 110Unified tax under the simplified tax system on income (for tax periods expired before January 1, 2011)182 10501 0120 11000 110182 10501 012 0 12100 110182 10501 0120 13000 110Types of bets

In the case of residential buildings, premises, garages and single complexes where there is even a single residential building, the tax rate is 0.1%. Business objects that do not exceed 50 meters in square footage are also subject to this rate. Despite the fact that almost all types of real estate are subject to a 0.1% rate. It can be changed, namely increased, or vice versa decreased.

387.2 of the Code contains a list of objects eligible for a tax rate of 2%; in addition, objects where the cadastral value is at least 300 million rubles are also eligible for this rate. But the rate can be significantly reduced, as exactly how this is possible is written in Article 406 of the Code.

KBK personal income tax, transport, property, decoding

Question #1: Why are these codes needed?

Since 1999, the accountant must indicate a single 20-digit code on the payment slip; this is done to detail taxes and penalties for subaccounts, statistics, and so on.

Question No. 2: What happens if you do not indicate the BCC or make a mistake?

No money will be credited for taxes or penalties, and the authority may impose additional sanctions.

Question No. 3: What to do if the wrong BCC is indicated?

Write applications to the tax or pension fund with a payment attached.

Question No. 4: The accountant sent many incorrect bills with incorrect budget classification codes...

In this case, the application must indicate a request for reconciliation of calculations, and also ask for clarification of the BCC. Sometimes the tax office refuses to reconcile, then you have to sort it out, and sometimes even go to court.

Question No. 5: What fines are provided for an accountant?

If you contact the tax office in a timely manner, there will be no penalty. But if the tax has not been paid to the address for a long time, they may come with an inspection, and the accountant will be charged from 10 to 30 thousand rubles for errors in the primary documentation, and the company will be fined for non-payment.

In this case, the principal amount of the debt goes under KBK 18210102010011000110, and the same code is used for recalculations. If the penalty has not been paid for a long time and a fine has appeared, the code 18210102010013000110 is used to pay off the debt. On the one hand, such a large number of codes causes a complete brain explosion, but on the other hand, it has become much easier to sort things out with the tax authorities. Again, it is necessary to carefully monitor the correctness of personal income tax payment.

A common mistake is to include a penalty or fine in the principal amount of the debt indicating the main BCC

. Accordingly, the debt for the tax itself will be repaid, but the debt for penalties will not. And then try to prove that the collection is illegal.

KBK is a code for the budget classification of income or expenses of the budget of the Russian Federation. In practice, business owners use only the “income version” of the KBK in their legal relations - indicating them in payment orders and thus identifying the payment that is transferred to the budget. This could be a tax, fee, contribution, duty, penalty or fine.

Budget classification codes are approved in the regulations of the main federal department that is responsible for taxes and fees - the Ministry of Finance of the Russian Federation. For 2021, the procedure for the formation and application of BCCs, their structure and principles of appointment were approved by order of the Ministry of Finance of the Russian Federation dated 06.06.2021 No. 85n. And the lists of codes related to the federal budget and extra-budgetary funds are by order of the Ministry of Finance dated November 29, 2021 No. 207n. That is, if you need to find out which tax KBK 18210301000012100110 (or any other) corresponds to in 2021, then order No. 207n dated November 29, 2021 will be the primary source.

Let's consider the main BCCs used by businessmen in 2021.

The most used in 2021 are KBK, necessary for modern Russian individual entrepreneurs and business entities dealing with payment:

- Personal income tax for hired employees (KBK 18210102010011000110);

- income tax (regional KBK - 18210101012021000110, federal - 18210101011011000110);

- simplified tax system (KBK under the “income” scheme - 18210501011011000110, under the “income minus expenses” scheme - 18210501021011000110);

- UTII (KBK 18210502010021000110);

- VAT (KBK for tax 18210301000011000110, penalties - 18210301000012100110, fines - 18210301000013000110);

- fixed contributions to mandatory pension insurance (KBK18210202140061110160);

- contributions to mandatory pension insurance for employees (KBK 18210202110061010160);

- fixed contributions for compulsory medical insurance (KBK 18210202103081013160);

- contributions to compulsory medical insurance for employees (KBK 18210202101081013160);

- contributions for compulsory insurance in case of temporary disability and in connection with maternity (KBK 18210202190071010160);

- contributions to the Social Insurance Fund for occupational injuries (KBK 39310202150071000160);

- voluntary fixed contributions to the Social Insurance Fund (KBK 39311706020076000180).

| Decoding the code | Budget classification code |

| Property tax of organizations on property not included in the Unified Gas Supply System (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) | 182 1 0600 110 (original code) 18210602010021000110 (short code) |

| Property tax of organizations on property not included in the Unified Gas Supply System (penalties on the corresponding payment) | 182 1 0600 110 (original code) 18210602010022100110 (short code) |

| Organizational property tax on property not included in the Unified Gas Supply System (interest on the corresponding payment) | 182 1 0600 110 (original code) 18210602010022200110 (short code) |

| Property tax of organizations on property not included in the Unified Gas Supply System (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0600 110 (original code) 18210602010023000110 (short code) |

| Property tax of organizations on property included in the Unified Gas Supply System (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) | 182 1 0600 110 (original code) 18210602021021000110 (short code) |

| Organizational property tax on property included in the Unified Gas Supply System (penalties on the corresponding payment) | 182 1 0600 110 (original code) 18210602021022100110 (short code) |

| Organizational property tax on property included in the Unified Gas Supply System (interest on the corresponding payment) | 182 1 0600 110 (original code) 18210602021022200110 (short code) |

| Property tax of organizations on property included in the Unified Gas Supply System (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0600 110 (original code) 18210602021023000110 (short code) |

KBK for transport tax in 2021

From 2021, the code for contributions to the compulsory pension, in categories 16 and 17, must contain the number 10. This is the structure of the code, where numbers 14 to 17 indicate the specifics of the transfer. For a contribution for an individual entrepreneur to compulsory pension insurance it is 1010, for a penalty on the same contribution - 2110, for a fine - 3010.

Deciphering the code is necessary in order to find out what information is encoded under KBK 18210601030131000110, what tax is paid by indicating this digital code in the receipt. The organizations' BCCs, which are necessary for the payment to go where it was intended, change almost every year. And the responsibility for their correct indication lies with the payer!