In what cases are entries made for Debit 90 and Credit 90, 68, 43, 99, 20

According to the chart of accounts (approved by order of the Ministry of Finance of Russia dated October 31, 2000 No. 94n), account 90 is needed to generate information about the company’s income and expenses for its main type of activity, as well as to determine the financial result of its business operations. For analytical purposes, subaccounts are opened to account 90 to record revenue (90.1), cost (90.2), VAT, excise taxes and export duties (90.3, 90.4 and 90.5, respectively), and financial results (90.9).

Accounting for subaccounts of account 90 must be kept cumulatively throughout the year. Every month, the accountant compares sales revenue with cost, VAT (if necessary, excise taxes and export duties) and writes off the final financial result to account 99. At the same time, there is no balance on account 90 as of the reporting date. At the end of the year, all subaccounts of account 90 (except 90.9) will be closed with internal postings Dt 90 Kt 90 , and subaccount 90.9, in turn, will be closed on account 99.

Postings

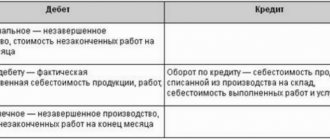

By debit account 23

| Operations | Credit |

| depreciation of fixed assets and intangible assets used in the issue is reflected | Kt 02, 05 |

| materials and finished products were transferred to the VP workshops | Kt 10, 43 |

| reflects the work performed and services for the needs of the VP by involved organizations | Kt 60, 76 |

| salary and deductions from it for VP employees | Kt 70, 69 |

On loan account 23

| Operations | Debit |

| materials manufactured in VP workshops are accepted for accounting | Dt 10 |

| VP costs are included in ODA and general business expenses | Dt 25, 26 |

| the cost of production of VP sold externally was written off | Dt 90 |

| the production of VP is reflected at actual costs | Dt 40, 43 |

How is the financial result determined on account 90

To do this, accounting entries are made such as Dt 90 Kt 20, Dt 90 Kt 43 , Dt 90 Kt 41, Dt 90 Kt 68, Dt 90 Kt 90, Dt 99 Kt 90, Dt 90 Kt 99, Dt 99 Kt 90. Let's consider Learn more about the logic of posting Dt 90 Kt 90 and other accounting operations to determine the financial result using an example.

Example

Sdoba LLC operates at OSN. In December 2015, it purchased raw materials in the amount of RUB 1,180,000. with VAT for the production of confectionery products.

The following entries were made in accounting:

- Dt 10 Kt 60 - 1,000,000 rub. (raw materials for the production of buns have arrived at the warehouse);

- Dt 19 Kt 60 - 180,000 rub. (VAT on purchased raw materials);

- Dt 68 Kt 19 - 180,000 rub. (VAT on raw materials is accepted for deduction);

- Dt 20 Kt 10 - 1,000,000 rub. (raw materials transferred to production).

The confectioners made 20,000 buns from the received raw materials and transferred them to the finished goods warehouse. You can account for manufactured products in different ways. Sdoba LLC does this without using account 40, arriving ready-made bakery products at actual cost directly to account 43.

For other ways to account for finished products, read the article “How finished products are reflected in the balance sheet.”

Dt 43 Kt 20 - 20,000 buns were accepted into the warehouse at an actual cost of 50 rubles. a piece.

Next, an order was received from a buyer for 5,000 buns at a price of 65 rubles. a piece. After the products are shipped, the accountant will make the following entries in the accounting records:

- Debit 90 Credit 43 - in the amount of 5,000 × 50 rubles. = 250,000 rub. (sold buns are written off from the warehouse at actual cost).

- Dt 62 Kt 90.1 - in the amount of 5,000 × 65 rubles. = 325,000 rub. (sales revenue includes VAT).

The accountant will record the amount of VAT on buns sold by writing: Debit 90 Credit 68 - 49,576.27 rubles.

Next, at the end of December, the accountant must determine the financial results of the company.

Debit turnover on the account is 90 - 250,000 rubles. (cost of buns) + 49,576.27 rub. (VAT), and a total of 299,576.27 rubles.

Credit turnover on the account is 90 - 325,000 rubles. (proceeds from the sale of buns).

At the end of December, the accountant of Sdoba LLC will close each of the subaccounts of account 90 with entries Dt 90 Kt 90 to 90.9.

Since the amount of credit turnover is greater than debit turnover, the company made a profit. In this case, the accountant uses the accounting entry: Debit 90 Credit 99 - 50,423.73 rubles. (profit was recorded at the end of the month).

If Sdoba LLC ended the month with losses, the accountant would make an entry in the accounting: Dt 99 Kt 90.9.

Closing the annual turnover on account 90 will be carried out by postings Dt 90 Kt 90 to the corresponding subaccounts:

- Dt 90.1 Kt 90.9 - RUB 325,000;

- Dt 90.9 Kt 90.2 - RUB 250,000;

- Dt 90.9 Kt 90.3 — 49,576.27 rub.

If a company opens its own subaccounts to account 90, then by posting Dt 90 Kt 90 it will have to close both the subaccounts provided for by law and its own.

Since the vast majority of companies conduct accounting using computer programs, the program automatically posts Dt 90 Kt 90 when performing the “Month Closing” operation.

Account 90 “Sales”

]]>]]>

The moment of implementation of a transaction for the sale of goods and services is associated with the need to simultaneously show the amount of revenue and the cost of production. Account 90 “Sales” was created to record the facts of sales of goods from services and derive basic values of profitability or unprofitability of business activities.

Characteristics of account 90 “Sales”

To systematize information about the level of profitability and the size of the cost part when carrying out ordinary activities, the enterprise uses account 90 in the accounting department. It is classified as a matching type of account and is characterized by the absence of a closing balance. In relation to the sections of the balance sheet, account 90 is active or passive, depending on the turnover of a specific subaccount; in the Chart of Accounts it is listed as active-passive.

Account 90 “Sales” reflects the total amount of revenue with the formed cost of:

- all types of finished products;

- work with services for various purposes;

- purchased products to form a complete set of manufactured products;

- account 90 in accounting is also necessary to reflect work related to construction and installation;

- product groups;

- transportation services;

- loading and unloading operations;

- sch. 90 is used in cases of leasing one’s property;

- transfer of rights to patented inventions on a paid basis.

The debit of account 90 “Sales” reflects the formed set of expenses for the production of a specific product in the form of cost. When reflecting this loan transaction, accounts 41, 43, 44, 20 may be involved in the correspondence. Account credit 90 shows the total amount of revenue received during the reporting period. Debit turnovers pass through account 62.

For enterprises specializing in the production of agricultural products, the cost price is reflected according to planned values. The difference between the planned indicators and the calculated actual data based on the results of the annual calculation is recorded as a separate debit amount. 90 account is not reflected in the balance sheet, since it is subject to reset upon closing at the end of the reporting period.

The 90 counting scheme looks like this:

| Debit 90 | Credit 90 |

| Expenses in the form of product costs including VAT, including sales costs | Income part in the form of proceeds from sales, including VAT |

| Total expenses | Total income |

| The balance indicates a loss | The balance shows profit |

Analytical accounting for account 90

Analytics is carried out on sub-accounts, which are closed at the end of the month and their balances are transferred to the profit and loss account. The score card 90 can have the following turns:

- 90.1 in relation to revenue;

- 90.2, showing the cost of production with operating expenses;

- 90.3 for VAT amounts;

- 90.4, intended for accounting for excise taxes;

- 90.5, allocated for export duties;

- account 90 “Sales” for summing up its subaccounts has a subaccount 90.9.

Amounts accumulated during the month on accounts 90.1 – 90.4 are subject to write-off to 90.9. Next, account 90 is reset by posting with account 99. For the purposes of analytical accounting, a separate reflection of each type of commodity item is typical.

Account 90 in accounting: postings

Subaccounts 90.3-90.5 are not used in practice by all enterprises. Their presence is determined by the taxation system of the organization and the specifics of the chosen area of economic activity. Typical transactions for account 90 are presented in two blocks - debiting and crediting the sales account.

Postings to account 90 when reflecting revenue:

- D76 – K90.1 from organizations considered other debtors and creditors;

- D50 (55, 51, 52) – K90.1 upon receipt of proceeds from the sale transaction into the accounts of the selling company;

- D79 - K90.1 - in this case, correspondence from account 90 shows the amount of income from subsidiaries and branch divisions;

- D98 - K90.1 when attributing part of the proceeds to deferred income in the case of making advance payments.

Additional postings to account 90 “Sales”:

- D90.2 – K43, 41, 40 when writing off goods or categories of finished products at discount prices;

- account 90 in accounting, when reflecting trade margins, forms a posting between D90.2 and K42;

- D90.3 – K68 at the time of issuing VAT on products sold.

Results

Posting Dt 90 Kt 90 means closing the internal subaccounts of account 90 in accordance with the financial result obtained.

For more information about what a company’s financial results are, read the article “Accounting and analysis of financial results.”

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

How to close account 20 - postings

Before writing off the amounts accumulated on the register, it is necessary to distribute and reset the associated costs:

- Auxiliary production (account 23);

- General production expenses (account 25);

- Defects in production (account 28).

If an organization produces one type of product, then, prior to the closure of the 20th account, the collected costs are fully allocated to work in progress. If products are produced in an assortment or several types of work are performed, then costs are included in the cost proportionally according to the accepted method:

- Regarding revenue;

- Comparison of planned prices;

- Simultaneously according to two indicators.

Example

The company built a garage and hangar for customers in January. Planned prices are 50,000 and 100,000 rubles. respectively. General production expenses (salaries, depreciation, transport, etc.) amounted to 30,000 rubles, materials - 25,000 and 70,000, respectively.

How to close account 20 - postings:

| Debit | Credit | Sum | Operation |

| 10 000 | Costs related to garage | ||

| 20 000 | Hangar related costs | ||

| 5 000 | Damaged metal when welding a garage door | ||

| 25 000 | Materials written off within a month | ||

| 70 000 |

After calculating the full cost of the objects, the accountant will close account 20, the postings of which are based on the implementation method:

| Debit | Credit | Sum |

| 40 000 | The cost of the garage is reflected | |

| 90 000 | The cost of the hangar is reflected |

With the direct and intermediate methods, registers are adjusted from which the cost of objects at the time of sale was previously written off at planned prices. An example of how to close account 20 – correction postings:

| Debit | Credit | Sum | Operation |

| Direct option | |||

| Reversal – 10,000 | Garage | ||

| -10 000 | Hangar | ||

| -20 000 | Corrected the cost of work performed | ||

| Intermediate option | |||

| 150 000 | Planned cost of objects | ||

| 130 000 | Actual amount | ||

| -20 000 | Implementation adjustments | ||

With automatic accounting, the necessary account assignments are made by the program. You need to know how to close account 20 and make manual entries to resolve unforeseen situations.

Regular operations written by programmers are based on standard accounting rules and software features. Before ending the month, you need to make sure that the settings are correct, otherwise the 20th account will not be closed. If you don’t have time to find out and eliminate the causes, you can use an alternative option - independently carry out regulations upon completion of the production process.

Postings for closing account 20 are manually organized through the “Operations” menu. But it is advisable to set up the program for automatic processing, since in the future errors may occur when re-posting documents. The accounting algorithm uses cost accumulation registers, rather than numbers from costing accounts.

Accounting account 20 is the active calculation account “Main production”. Using simple examples for dummies, let's look at typical transactions for account 20 in accounting, as well as what transactions are used to close account 20.

Closing an account

Closing is carried out at the end of the reporting month or upon the end of the production period or cycle. Often the 20 account has no balance, that is, it is reset to zero. If a debit balance has formed for “Main Production”, then it will reflect the value of work in progress as of a specific date. This balance is carried forward to the beginning of the next reporting period. Closing account 20 can be carried out for certain types of goods, works or services produced, and for other analytical registers the balance will be reflected in the form of work in progress.

Closing can be done in one of the following ways:

- straight;

- intermediate;

- direct sales of released products.

The closing methodology and cost allocation basis are prescribed in the accounting policy and cannot be changed or canceled during the reporting period.

Here is a brief instruction on how to close a 20 account using the direct method. During the reporting period or production cycle, there is no accurate information about the price of the product. Production results are reflected at deemed cost. You can take into account prices at planned cost, but accounting at actual cost during the reporting period is not allowed. After its completion, the accountant will already know the amount of the actual cost, after which the appropriate adjustment will be made to close the 20th account.

Account 20 in accounting

Manufacturing enterprises use account 20 to record production costs, namely the costs of creating new products (services, works). In addition to costs, account 20 also reflects the material value of work in progress:

Determination of production costs

Production costs include direct costs attributable to the production of specific products, services provided or work of the main activity.

The following types of direct costs can be distinguished:

- Expenses for the purchase of raw materials for production and materials for the provision of works and services;

- Remuneration of production workers;

- Depreciation and repair of production fixed assets;

- Losses from marriage;

- Modernization, introduction of new technologies;

- Other costs of the production process.

Important! At the end of the reporting period or where there is no more detailed division (for example, auxiliary production and others), account 20 also displays:

- Expenses of auxiliary and service production;

- Indirect costs for the management and maintenance of main production.

Definition of work in progress (WIP)

Work in progress includes:

- Material assets that are in production or processing, as well as accepted for production, but not yet participating in the production process;

- Unshipped released products to storage warehouses.

To determine the amounts of work in progress, first describe all of the above material assets at the end of the reporting period, and then establish their valuation.

Account 20 Main production

Main properties of account 20 “Main production”:

- Only the valuation is taken into account;

- It is active and does not have a negative balance at the end of the period, but may have a positive balance, which is a cost indicator of work in progress;

- In addition to synthetic accounting, analytical accounting is also carried out in the context of types of products, costs (estimates) and by divisions of the organization.

Primary documents for accounting of production costs: