The information is provided by all organizations, regardless of whether they have employees, as well as individual entrepreneurs who had employees in 2021. Individual entrepreneurs who are not employers do not submit the form.

The information form was approved more than 10 years ago, by order of the Federal Tax Service of the Russian Federation No. MM-3-25 / [email protected] dated March 29, 2007.

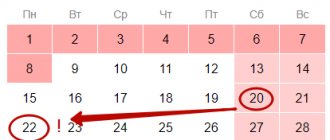

The deadline for submitting the form is no later than January 20, in 2021 the deadline is January 22, since January 20 is a day off.

The fine for failure to provide information about the number is 200 rubles. (clause 1 of article 126 of the Tax Code of the Russian Federation). In addition, an official of the organization may be held accountable under Article 15.6 of the Code of Administrative Offenses.

The average number of employees is determined taking into account the procedure for filling out the statistical form P-4.

RSV in 2021: new form and filling out rules

The rules for calculating the number from 2021 are established by Rosstat order No. 711 dated November 27, 2019. From January 15, 2021, it will be replaced by instructions from Rosstat order No. 412 dated July 24, 2020.

In general, the calculation formula looks like this:

Average year = (Average 1 + Average 2 + … + Average 12) / 12,

where: Average year is the average headcount for the year;

Average number 1, 2, etc. - the average number for the corresponding months of the year (January, February, ..., December).

For more information about the calculation procedure, read the article “How to calculate the average number of employees?” .

The information is certified by the signature of the entrepreneur or the head of the company, but can also be signed by a representative of the taxpayer. In the latter case, it is necessary to indicate a document confirming the authority of the representative (for example, it may be a power of attorney), and a copy of it must be submitted along with the ERSV.

NOTE! The power of attorney of the representative of the individual entrepreneur must be notarized (Article 29 of the Tax Code of the Russian Federation).

The completed ERSV form can be submitted in person or through a representative to the Federal Tax Service, or sent by mail with a list of attachments, provided that the average number of employees of the company does not exceed 10 people. If this indicator is higher, the report will be accepted only in electronic format.

The form is submitted to the inspectorate at the place of registration of the company or at the place of residence of the individual entrepreneur. Organizations with separate divisions report the number of all employees at the place of registration of the head office.

The tax office accepts reports with legible data entered in black ink. Forms filled out with other color variations will not be considered. Write information in cells and rows as legibly as possible. Tax professionals should not feel like graphologists.

If you are an advanced computer user, feel free to fill out the form using editing software. Tax officials accept printed forms filled out in 18 Courier New font.

When all fields of the form are completed, it must be signed manually. Only under this condition will the inspector accept your annual report for consideration. You do not have to appear in person at the tax office to submit a document. Send it by mail as a valuable letter of notification, of course taking into account the postmark date.

Useful advice! Experienced businessmen who do not like to stand idle in the crowded corridors of the tax office are advised to put an inventory of the enclosed documents in an envelope, certified with a post office stamp. The tax inspector will once again make sure that all documents are in place.

The indicator is calculated in two stages:

- For each calendar month.

- For the year as a whole.

Using an individual entrepreneur as an example, the calculation looks like this:

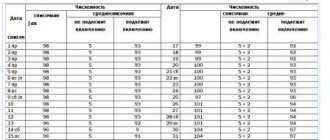

In January 2021, the individual entrepreneur had 6 employees. 4 of them worked 20 working days in accordance with the standard. One employee was on vacation and only worked 12 days, and one employee was sick and only worked 3 days.

The average number of individual entrepreneur employees for January 2021 is:

(4 × 20) + (1 × 12) + (1 × 3) = 95 / 22 = 4,31

The result obtained for each month is not rounded.

To determine the annual indicator, it is necessary to sum up the average for each month and divide by 12. The final total is rounded to a whole number according to the usual rule: values less than 0.5 are discarded, values of 0.5 or more are taken as one.

Example:

4.31 + 5 + 4.35 + 5.2 + 4.13 + 4.0 + 5.0 + 6.0 + 4.25 + 4.45 + 5.2 + 3.8 = 55.69 / 12 = 4.64 = 5 people

Thus, our entrepreneur has an average annual headcount of 5 employees. This is the information for 2020 that should be included in the report.

A report on the average number of employees for the previous calendar year had to be submitted to the Federal Tax Service:

- organizations (it does not matter whether they use the labor of employees in their activities, on the basis of Letter of the Ministry of Finance of Russia dated 02/04/2014 N 03-02-07/1/4390);

- Individual entrepreneur (only if the entrepreneur hires one or more employees on the basis of an employment contract).

These entrepreneurs were required to submit a report for 2021 no later than January 20, 2021.

The following are required to submit a report on the average number of employees for 2021 in 2021:

- newly created legal entities;

- reorganized organizations.

At the same time, newly created enterprises must submit the document within a time frame that differs from individual entrepreneurs and organizations. These categories must submit a report no later than the 20th day of the month following the month of their creation (reorganization). This provision is contained in paragraph 3 of Article 80 of the Tax Code. The document indicates data on the average number of employees for the month of creation (reorganization) of the enterprise.

Thus, if the date of creation of the organization is April 17, 2021, then the report on the average number of employees had to be submitted no later than May 20 of the same year.

Paragraph 6 of clause 3 of Article 80 of the Tax Code of the Russian Federation states that individual entrepreneurs may not submit a report on the average number of employees if they did not hire hired personnel in the reporting period. Accordingly, there is no zero form of report on the average headcount.

Individual entrepreneurs who have completed the state registration procedure this year may not submit a report on the average number of employees.

Everyone else had to submit a report to the tax office without fail.

However, Federal Law No. 5-FZ dated January 28, 2020 (hereinafter referred to as Law No. 5-FZ) amended the mentioned paragraph. 6 clause 3 art. 80 Tax Code of the Russian Federation. Thus, information on the average number of individuals from 01/01/2021 must be provided as part of the calculation of insurance premiums. There is no need to fill out or submit an independent report on the average number of employees starting in 2021. But it is necessary to calculate and report on the average headcount in the DAM calculation.

The title page of the DAM reporting has been supplemented with a new field “Average headcount (persons)”.

- TIN;

- checkpoint;

- Full name (for organizations);

- Full name (in full) and TIN (for individual entrepreneurs).

- January 1, 2021 – to provide information for the 2020 calendar year;

- The 1st day of the month following the month of creation (reorganization) - for the organization.

You can submit information on the average number of employees as part of the DAM report to the Federal Tax Service in 2021 in the following ways:

- In person (by visiting the Federal Tax Service).

- Through a representative.

- On paper.

- In electronic form (with enhanced digital signature).

- By Russian post (with a description of the attachment).

If there are more than 100 employees, then the report must be submitted exclusively in electronic form; if there are fewer, then submission on paper is allowed.

Methods for submitting information

This form can be submitted both in paper and electronic form; there are several ways to submit it:

- You can submit the completed report on paper personally to the inspector, or through an authorized representative with a power of attorney. The form must be drawn up in two copies, one will remain with the Federal Tax Service, and the second with a mark of receipt will be returned back to the business entity;

- Sending by mail in an envelope using a registered letter;

- Via the Internet, using EDI services. In this case, the file itself must be signed with a qualified signature.

Attention: in some regions, when submitting a report on paper, you also need to provide a file on a flash drive or other media. Before visiting a government agency, it is recommended to call and clarify this need.

Form and example of filling out the average number of employees according to the KND form 1110018

Average number of individual entrepreneur employees for January 2020 = (15 people x 17 days + 16 people x 14 days) / 31 = (255 + 224) / 31 = 15.45

This indicator does not need to be rounded and the average number of employees for all other months of the year is calculated similarly and divided by 12:

15.45 + 6 + 4.35 + 4.65 + 5.1 + 5.3 + 3.7 + 4.25 + 4.75 + 3.8 + 4.25 + 5.0 = 66.6 / 12 = 5.55 = 6 people.

That is, for 2021, the average number of individual entrepreneurs was 6 people. This indicator must be included in the report.

- Deadlines for payment of insurance premiums in 2021

- Changes to the simplified tax system in 2021

- KBC insurance premiums for individual entrepreneurs for themselves in 2021

- Changes to PSN in 2021

- Individual entrepreneur reporting on the simplified tax system in 2021

- Limit value of the base for calculating insurance premiums in 2018

The average payroll is calculated according to the rules provided for by Rosstat Directives No. 428 of 2013. This document indicates the categories of employees who must be included in the calculation, as well as those employees who are not subject to reflection in the report. All discussions are conducted in relation to entering information into the report in the event that the organization has only one founder who performs functions without concluding an employment contract and does not receive a salary. If we turn to the Directions, we can conclude that this founder does not need to be taken into account when drawing up the report. The average headcount applies exclusively to those employees who have an employment relationship. This is a rather important feature and differs from the reporting submitted to funds.

It will also be important that the period that the employee worked under the employment contract does not matter at all. The report on the average payroll must include all employees, regardless of whether they work temporarily or permanently, or perform their labor functions only during the season. Those employees who work part-time or part-time are also taken into account. The average list indicator is determined on average by adding the total number of employees according to the list for each month of the reporting year, after which the resulting value is divided by 12. The total value is rounded to the nearest whole indicator.

Information on the average number of employees is submitted on the established form (KND form 1110018). The document consists of one sheet, which displays the following information:

- TIN/KPP of the organization;

- name of the Federal Tax Service to which the report is submitted (tax code);

- full name of the organization;

- average salary indicator;

- manager's signature.

If the report is submitted by an authorized person, then the details of the power of attorney must also be indicated.

Important! The difference between the report on the average list of new LLCs and existing ones is only in the date.

Who submits information

The average headcount is a specially calculated element that reflects the average number of employees working in a business entity in a particular time period.

This value is required to be calculated by every business entity that has hired employees. The time period for calculation, depending on the need, can be chosen in any way - month, quarter, half-year, year, etc.

But even when calculating different time periods, the technology for obtaining the indicator does not change.

In 2014, a relaxation was made for entrepreneurs - they now do not have to document information about the average number of employees if they carry out the work independently, without hiring third-party workers.

Attention: one of the important areas of application of the obtained element is the division of business entities into groups based on the number of employees involved.

And this, in turn, will determine the possibility of using one or another tax preferential regime. Also, the payroll number is used to determine the average salary for the organization. The period of storage of the report in the archive of a business entity is 5 years.

Report on the average number of employees: form and example of completion

To calculate the average headcount for the year, sum up the average headcount indicators for each month, after which the resulting amount is divided by 12 (the number of months in a year). Now let’s figure out how the average payroll indicator is calculated for each month. To calculate it, you need to add up the total number of employees working in a month, and then divide the resulting value by the number of days in the month of calculation.

Information on the average headcount for the previous calendar year is submitted to the tax authority before January 20. If this day falls on a weekend, then the deadline for submitting the report is postponed to the next working day.

If organizations registered in 2021, they must report twice for this year. The first time in the month following the month of registration (also before the 20th), and the second time - after the end of the year - before January 20. If the company has undergone reorganization, the same rule applies to them.

Let's look at an example:

Example 1. LLC "Company" registered as a legal entity in August 2021. The LLC must submit information for the first time by September 20, 2021, as of September 1, 2018. And the second time, information must be submitted at the end of the year, before January 20, 2021, as of January 1, 2021.

Example 2: Organization LLC was registered in January 2021. For 2021, information will also need to be provided twice. The first time is until February 20, 2021, as of February 1. The second time - in 2021, together with other organizations until January 20. That is, in January 2021, Organization LLC does not submit information.

Penalties for failure to submit or untimely submission of information are provided for by the Tax Code of the Russian Federation and the Code of Administrative Offenses of the Russian Federation. The fines are as follows:

- 200 rubles – for organizations

- 300 – 500 rubles – for officials.

As a rule, the Federal Tax Service imposes a fine only on the organization. A manager can be fined only by court decision. Thus, in order for the Federal Tax Service to collect a fine from the manager, it will have to go to court. Payment of the fine does not exempt the company from submitting the report.

Question: Does the tax office have the right to block the account of a company or entrepreneur in case of late submission of a report on the average number of employees.

Answer: This penalty applies only to tax returns, or demands for payment of taxes, penalties and fines. As for information about the average number of employees, the tax office does not have the right to block the current account for late submission.

Question: Who is included in the average headcount?

Answer: When calculating the average payroll, the following employees must be taken into account:

- who are on a business trip or on sick leave;

- works remotely;

- is on vacation (annual, additional);

- who have a day off on the settlement day;

- is on leave;

- with absenteeism.

The following should not be taken into account: external part-time workers, employees working under a civil contract, employees who are on maternity leave (or in connection with adoption), employees who are on maternity leave.

Information on the average number of employees in 2021

In order to calculate the NFR for a year, in cases where the year has been fully worked out, you need to sum up the NFR for each month, and divide the resulting amount by the number of months in the year, i.e. at 12.

At enterprise N, changes in personnel during the year were insignificant. In the January-March period, the number of employees was 25, in the April-May period - 23, and in the June-December period - 40 people.

The average and payroll numbers are two different values that can only sometimes coincide.

The payroll includes all workers, even those who worked for one season or one day. It coincides with the daily report card and reflects the amount of time spent at work by each employee on the list.

At the first stage, a quantitative calculation of currently valid employment contracts is made. However, some employees are not included in the calculation.

The average value of a weekend or holiday is assumed to be equal to the average value of the day preceding it.

Let the organization employ 50 people from February 1 to 10, 40 from January 10 to 19, and 35 from March 8 to 17. This happened because some of the employees went on vacation at their own expense.

Then the total number (CN) for each of these months will be equal to:

- January= 10*40=400 people;

- February = 10*50=500 people;

- March=35*10=350 people

The subtlety of calculating the CFR for workers on a reduced schedule is that working days spent on vacation or illness are included in working hours in the amount in which they last went to work.

To calculate this indicator you need:

- Calculate the time worked per month by workers on a reduced schedule.

- Multiply the length of a working day by the number of working days in a month.

- Divide the first by the second.

Let's assume that there are 4 people in the company who work at half rate from Monday to Friday:

- January=4*16=64 hours;

- February = 4*19=76 hours;

- March=22*4=88 hours.

Thus, in total, each of these people will work 76*4=304 hours in February, 64*4=256 hours in January, and 88*4=352 hours in March.

This stage is carried out in one action: the sum of the number of workers from the list is divided by the number of days in a particular month.

- In January, SC=40*10=400 people;

- In February, SC=50*10=500 people;

- In March, SC=35*10=350 people.

Then:

- January NFR = 400/31 = 13 (12.9 rounded to 13);

- February NFR=500/28=18 (17.85 rounded to 18);

- March NFR = 350/31 = 12 (11.29 rounded to 12).

To calculate this indicator, you need to take the sum of hours at a partial monthly rate, the amount of time worked per month with an 8-hour working day and the number of days in the month.

For an eight-hour working day the following is true:

- January – 2 people (256/(8 *16);

- February – 2 people (304/(8*19);

- March – 2 people (352/(8*22);

Where 8 is the number of hours in a full working day, 256,304,352 is the total operating time for the month.

A report on the average number of employees (ASH) must be submitted by all organizations and individual entrepreneurs (regardless of the chosen taxation system) that had employees in the calendar year.

Newly created organizations (not individual entrepreneurs) need to submit the CHR report twice: once after creation, and the second time at the end of the year.

Individual entrepreneurs without employees, starting from January 1, 2014, do not need

.

Note!

2020 was the last year in which a CHR report had to be filed. From 2021, it is abolished by law dated January 28, 2021 No. 5-FZ. Information on the number of employees will be transmitted to the Federal Tax Service as part of the calculation of insurance premiums.

Information on the average payroll number is submitted by:

Based on the results of the calendar year, no later than January 20.

For 2021, the SChR information must be submitted by January 20, 2020

.

Fine

for violation of the deadline, the SCR is

200 rubles

.

They may also additionally fine the chief accountant or the head of the organization in the amount of 300

to

500

rubles. There is no penalty for providing incorrect information.

note

that even after paying the fine, a report on the average number of employees will have to be submitted in any case.

Employees working under an employment contract part-time (including those who did not come to work due to illness or business travel) are taken into account in proportion to the time worked

.

This is done according to the following formula:

Ch2 = Total / Trd / Drab

Total

– the total number of man-hours worked by these employees in the reporting month.

Trd

– length of the working day, based on the length of the working week established in the organization. For example, with a 40-hour five-day work week, this figure will be 8 hours, with a 36-hour week - 7.2 hours, and with a 24-hour week - 4.8 hours.

Drab

– the number of working days according to the calendar in the reporting month.

The result does not need to be rounded

.

Example

. The employee worked part-time (4 hours) for 22 working days per month, while the working day in the organization is 8 hours. The average number in this case will be equal to:

0,5

(88 / 8 / 22).

To calculate the average number of employees, it is necessary to add up the headcount indicators ( Ch1

and

Ch2

) for all months of the year and divide the result by

12

months.

If the result is a non-integer number, it must be rounded

(discard less than 0.5, and round 0.5 or more to the whole unit).

The average headcount indicator is involved in the calculation of some taxes, and the method of reporting to the tax authorities also depends on it.

So, for example, individual entrepreneurs and organizations with more than 100 people in a calendar year cannot use the simplified tax system and UTII.

For individual entrepreneurs with a patent, the average number of employees for all types of activities should not exceed 15 people.

There are other situations in which the exact number of employees may be of interest to tax authorities.

The form by which information on the number of personnel of an organization is submitted is form No. MM-3 25/, approved by order of the Federal Tax Service of the Russian Federation dated March 29, 2007. Information is submitted to the Federal Tax Service where the organization or individual entrepreneur is registered. If the organization has separate divisions, then they should not report separately. Information is submitted to the tax office by the parent organization for all employees, including separate divisions.

Information can be submitted both in paper and electronic form. On paper, information is submitted personally to the Federal Tax Service or sent by mail. Only those organizations whose staff does not exceed 200 people can submit information in this way. For those organizations with more than 200 people, they are required to submit information only in electronic form.

Penalties for failure to submit or untimely submission of information are provided for by the Tax Code of the Russian Federation of the Code of Administrative Offenses of the Russian Federation:

- 200 rubles – for organization

- 300 – 500 rubles – per manager.

The Federal Tax Service usually imposes a fine only on the organization. A manager can only be fined by a court decision, that is, in order for the Federal Tax Service to be able to collect a fine from the manager, it will have to go to court.

Payment of the fine does not exempt organizations from submitting information. The organization is obliged to provide information regardless of payment of the fine.

In addition to fines for late submission of reports, the tax office has the right to block the account of a company or individual entrepreneur. But the requirement applies only to tax returns, or requirements for payment of taxes, penalties or fines. As for information about the average number of employees, the Federal Tax Service does not have the right to block the current account for late submission.

Who is included in the average headcount?

The following employees are required to be taken into account when calculating the average salary:

- who are on a business trip;

- who are on sick leave;

- who works remotely;

- who is on vacation (annual or additional);

- employees who have a day off on the day of payment;

- employees on leave;

- workers who have absenteeism.

The following list contains those persons who should not be taken into account when calculating the average salary:

- external part-time workers;

- working under a civil contract;

- employees who are on maternity leave (or due to adoption);

- workers who are on maternity leave.

Where are reports submitted?

The law states that a company must submit a report on average headcount to the Federal Tax Service located at its location. If a company has branches or separate divisions, all information is compiled into a single report, which is submitted by the parent company.

Individual entrepreneurs who have employees must send a report to the address of their registration or actual residence.

Attention: if an individual entrepreneur is registered in one subject and conducts activities in another, he must still submit a headcount report to the Federal Tax Service at his registered address.

Formula and example of calculating the average number of employees in 2021

Declarations on transport and land taxes replaced by notifications from the tax authorities about the calculated amount of tax (clauses 17 and 26 of Article 1 of Law No. 63-FZ of April 15, 2019, Order of the Federal Tax Service of September 4, 2019 No. ММВ-7-21/440 ).

So far, there are more questions than answers: how the tax authority will keep records of objects, what reconciliation acts are provided for such settlement accruals, how interdepartmental exchange will be implemented. At the moment, the Federal Tax Service has not given any additional explanations; we can only wait for the implementation of this project.

By the way, no one exempted the organization from paying advance payments. And companies must calculate these advance payments independently. Needless to say, the calculated tax amounts may not agree with the amounts from the notifications, and these discrepancies will have to be justified.

Data on the number of employees will be included in the calculation of insurance premiums (DAM) from January 1, 2021 (Clause 2, Article 1 of Law No. 5-FZ dated January 28, 2020).

As you know, starting from 2021, UTII will cease to exist. And along with the abolition of the taxation regime, the filing of a declaration is also canceled. The last time UTII payers will have to report by January 20, 2021 is for the fourth quarter of 2021.

In accordance with the order of the Federal Tax Service dated 08/19/2020 No. ED-7-3/, changes were made to the VAT declaration that take into account amendments to Chapter 21 of the Tax Code of the Russian Federation introduced by Federal Laws dated 03/26/2020 No. 68-FZ, dated 06/08/2020 No. 172 -FZ.

Thus, new transaction codes have been added to the procedure for filling out a VAT return:

1010831 – transfer, free of charge, of property intended for use in preventing and preventing the spread, as well as diagnosis and treatment of coronavirus, to state authorities and management and (or) local governments, state and municipal institutions, state and municipal unitary enterprises;

1011450 – transfer of real estate objects free of charge to the state treasury of the Russian Federation;

1011451 – transfer of property free of charge into the ownership of the Russian Federation for the purposes of organizing and (or) conducting scientific research in Antarctica;

1011208 – sales of municipal solid waste management services provided by regional municipal solid waste management operators;

1011446 – sales of services provided during international air transportation directly at international airports of the Russian Federation, according to the list approved by the Government of the Russian Federation, etc.

The updated procedure for filling out the declaration will apply in the first quarter of 2021.

The KND declaration form 1152026 approved by Order No. ED-7-21 of the Federal Tax Service of Russia dated July 28, 2020 has been updated. Changes were made in connection with the provision of support measures due to the spread of COVID-19, namely the postponement of the payment of property tax (advance payments thereon) ) during 2021

What changed:

- New tax benefit codes have been added for those exempt from paying tax for the second quarter of 2021;

- in section 1, a new field “Taxpayer Attribute”: put “1” - if the organization has the right to pay tax later according to the decree of the Government of the Russian Federation; “2” – if according to regional acts; “3” – other legal entities;

- added a sign for calculating the amount of tax by a person who has entered into an agreement on the protection and promotion of capital investments in sections 1, 2 and 3, a new field “SZPK Sign” (Order of the Federal Tax Service of the Russian Federation dated July 28, 2020 No. ED-7-21/).

The deadline for submitting the declaration is no later than March 30, 2021.