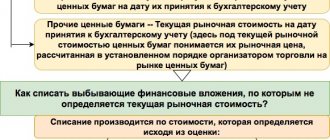

Balance sheet structure

The assets and rights belonging to the organization are presented in a grouped form on the balance sheet. In the liability, we see the sources through which this property and rights were acquired.

Schematically, assets and liabilities can be represented as follows:

For enterprises using conventional accounting and reporting methods, the balance sheet (balance sheet assets and liabilities) (table) looks like this:

For enterprises using simplified accounting and reporting methods, the balance sheet looks different:

Practical ongoing financial planning

Current financial planning is considered as an integral part of the long-term plan and represents a specification of its indicators.

Current planning consists of developing a profit and loss plan, a cash flow plan, and a planned balance sheet, since these forms of planning reflect the financial goals of the organization (enterprise). All three planning documents are based on the same initial data and must be combined with each other.

Current financial plan documents are drawn up for a period of one year. This is explained by the fact that seasonal fluctuations in market conditions generally level out over the course of a year. To ensure accuracy of the result, the planning period is divided into smaller units of measurement: half a year or quarter.

1. Profit and loss plan

It is advisable to start developing a financial plan with a profit and loss plan. Having data on the sales volume forecast, you can calculate the required amount of financial resources. This document shows the summarized results of current (economic) activities. Analysis of the ratio of income to expenses allows you to assess the reserves for increasing the equity capital of the enterprise. Another function performed by this document is the calculation of planned values for various tax payments and dividends.

The development of a profit and loss plan occurs in several stages.

At the first stage, the planned amount of depreciation is calculated, since it is part of the cost and precedes the planned profit calculations.

At the second stage, the amount of costs is determined, which can be calculated in two ways:

- traditional;

- cost planning by responsibility centers.

In the first method (traditional), based on standards, a cost system is drawn up, which includes basic costs for raw materials (in accordance with technical requirements), direct labor costs (scientifically based basic wage rates) and overhead costs.

Standard cost rates are developed based on a specific methodology. The level of accepted standards makes it possible to identify those areas of the enterprise that interfere with its effective functioning and prevent the production of competitive products. In modern conditions, the process of cost planning by responsibility centers is becoming increasingly widespread. The center of responsibility is each division of the enterprise (plant, department), the head of which is directly responsible for the costs of this division. This method allows for effective control by delegating responsibility to the level of individual departments.

Control and regulation are carried out on the basis of data on specific plans for the production of goods (works, services) in a specific center of responsibility. These planned values are called cost elements (or linear elements).

Operational control over consumption makes it possible to determine the cost of product sales as a basis for developing annual plans.

At the third stage, revenue from product sales is determined. Last year's sales revenue is taken as the starting point. This value changes in the current planning year as a result of changes in:

- cost of comparable products;

- prices for the company's products sold;

- prices for purchased materials and components;

- assessment of fixed assets and capital investments of the enterprise;

- wages (due to possible inflation).

Statistical analysis can be used to assess the impact of these factors on last year's revenue.

2. Cash flow plan

It represents the actual financing plan, which is drawn up for the year, broken down by quarter. The annual cash flow plan is broken down quarterly or monthly, since during the year the need for cash may change significantly and in any quarter (month) there may be a lack of financial resources. In addition, breaking the annual plan into short periods of time allows you to track the synchronization of cash inflows and outflows (cash flow) and eliminate cash gaps.

The need to prepare this document is due to the fact that the concepts of “income” and “expenses” used in the profit plan do not directly reflect the actual cash flow: the costs of sold products do not always relate to the same time period in which the latter was shipped to the consumer (accrual method). In addition, the profit and loss plan lacks information about the areas of activity of the enterprise.

A cash flow plan can be drawn up using two methods: direct and indirect.

The direct method is based on calculating the inflow (revenue from sales of products and other income; income from investment and financial activities) and outflow (payment of supplier bills, return of borrowed funds, etc.) of funds. In this way, balances are drawn up for three types of activity of the enterprise:

- main (current) activities;

- investment activities;

- financial activities.

After this, the final cash flow balance is calculated.

The initial element of the direct method is revenue. The indirect method is based on sequential adjustments to net profit due to changes in the assets of the enterprise. The starting element of the indirect method is profit.

When calculating the amount of cash flows using the indirect method, you can use the following scheme:

I. Cash flows from operating activities

- Net profit

- Depreciation charges (+)

- Increase (-) or decrease (+) in accounts receivable

- Increase (-) or decrease (+) in inventories and other current assets

- Increase (+) or decrease (-) in accounts payable and other current liabilities (except for bank loans)

Total: balance of current activities

II. Cash flows from investing activities

- Increase (-) of fixed assets and unfinished capital investments

- Increase (-) long-term financial investments

- Profit (+) from the sale of long-term assets

Total: balance on investment activities

III. Cash flows from financing activities

- Increase (+) of equity capital by issuing new shares

- Decrease (-) in equity due to payment of dividends and share repurchase

- Increase (+) or decrease (-) in credits, loans, bonds, bills

Total: balance for financial activities

The total change in cash must be equal to the increase (decrease) in the cash balance between two planning periods.

The advantage of the direct method is the direct calculation and coverage of the entire cash flow. However, calculations using the indirect method more fully show the relationship between cash flow and the economic activity of the enterprise as a whole; reveal the relationship between the profit and loss plan and the cash flow plan.

3. Planned balance

The final document of the financial plan is the planned balance sheet at the end of the planned year, which reflects all changes in assets and liabilities as a result of planned activities and shows the state of property and finances of enterprises.

Typically, ongoing balance sheet planning begins with asset planning.

Data on changes in material assets are taken from the long-term plan, financial assets - from the long-term financing plan. The size of inventories is determined from production, supply, and sales programs. Other items of normalized working capital are planned based on past experience and in accordance with the financial plan. The basis for planning the cost of fixed assets are investment projects.

In the liability side of the balance sheet, the change in equity capital is calculated based on the possibility of increasing (decreasing) capital at the time of drawing up the plan and changing the reserve capital formed in accordance with the law and constituent documents. The amount of required borrowed capital is obtained as the difference between the balance sheet asset and equity capital.

The balance sheet is formed on the basis of planned changes in the items of the planned balance sheet of the previous year, as well as the profit and loss plan. It is necessary to regroup the asset and liability items of the planned balance sheet based on the use of funds (left side) and their origin (right side) according to the diagram below:

| Use of funds | Sources of funds |

| I. Increase in assets 1. Investments in fixed assets, intangible assets, financial investments 2. Increase in working capital | I. Decrease in asset 1. In the area of fixed assets 2. In the area of working capital |

| II. Reducing liabilities 1. Repaying loans, borrowings 2. Reducing equity capital: distribution of profits to the consumption fund, payment of dividends, interest on bonds, losses | II. Increasing liabilities 1. Obtaining loans and borrowings 2. Issuing bonds 3. Increasing equity capital: issuing new shares, increasing reserves and funds from profits |

To organize a system for analyzing and planning cash flows at an enterprise, it is recommended to create a modern financial management system based on the development and control of the implementation of an enterprise budget system. The budget system includes the following functional budgets: wage fund budget, material costs budget, energy consumption budget, depreciation budget, other expenses budget, loan repayment budget, tax budget.

This budget system completely covers the entire base of financial calculations of the enterprise and is the basis for constructing documents: profit and loss plan, cash flow plan and planned balance sheet.

As the activities laid down in the current financial plan are implemented, the actual results of the enterprise's activities are recorded. In this case, the plan is the result of planning, while the report on actual values shows the real position of the enterprise, which is necessary for its management to make decisions.

As a result of comparing actual indicators with planned ones, financial control is carried out. When carrying it out, special attention should be paid to the following points:

- implementation of the articles of the current financial plan to identify deviations and reasons that signal an improvement or deterioration in the financial condition of the enterprise and the need for its management to respond to this;

- determining the growth rate of income and expenses over the past year to identify trends in the movement of financial resources;

- the availability of material and financial resources, the state of production assets at the beginning of the next planning year to justify their initial level.

One can also imagine a situation where it turns out that the financial plan itself was drawn up on the basis of unrealistic assumptions. In any case, the management of the enterprise must take the necessary actions: change the way the plan is implemented or revise the provisions on which the current financial planning documents are based.

Asset Analysis

For reporting, in any case, a balance sheet asset is a grouping of property by service life or turnover time. Property with a service life of more than 12 months is classified as non-current, and property with a service life of less than 12 months is classified as current.

Actually, a balance sheet asset is a grouping of economic resources according to the degree of their liquidity. Liquid assets include: money in cash or in bank accounts, financial investments for up to 12 months, property assets that can be quickly sold, bills of exchange for which payment has come due, accounts receivable with a short maturity. Illiquid ones, that is, those whose implementation will take a long time, include: fixed assets, intangible assets, long-term financial investments, etc. Grouping assets according to this principle provides visual information about whether the property is quickly sold or not. The excess of the ratio of current assets over non-current assets indicates the high liquidity of the enterprise, the ability to quickly sell its property and receive money for it, for example, to pay off obligations.

Definition

P3 Long-term liabilities are obligations for which payments must be made within a period exceeding 12 months.

Obviously, this will include all long-term liabilities (the summary of section 4).

However, some authors include here one or two items from short-term liabilities: either only deferred income, or also reserves for future expenses and payments (estimated liabilities).

Accordingly, if these items are taken out of short-term liabilities, the value of the indicator P2 Short-term liabilities will change. But you can only take out one of these indicators or not take out any articles at all.

The fact is that reserves for future expenses and payments (estimated liabilities) in any case relate to short-term liabilities. And authors who write differently are mistaken.

As for deferred income, they are received now and relate to future periods. Therefore, in fact, they have both a short-term and long-term nature.

Therefore, from the point of view of financial management, it makes sense to classify future income as long-term liabilities, and leave reserves for future expenses and payments (estimated liabilities) as short-term liabilities.

In the services, long-term liabilities include long-term liabilities and future income.

Liability Analysis

Liabilities reflect the sources of funds through which the enterprise’s property was acquired: equity capital, reserves, long-term borrowed funds and accounts payable. As can be seen from the table, sources are divided into own and borrowed. It is by the ratio of these liability indicators that one can understand with what funds, own or borrowed, the property was acquired. To do this, several coefficients are calculated:

- autonomy coefficient as the ratio of equity capital to the total amount of sources of funds of the enterprise, Ka;

- debt-to-equity ratio as the ratio of long-term and short-term debt to equity capital, Kz/s.

So, if, when calculating the indicators, we received Ka ≥ 0.5 and Kz/s ≤ 1, this means that the enterprise’s obligations can be covered with its own funds.

So, the ratio of sections and articles of reporting can give a complete picture of the economic indicators of the enterprise in numbers. In order to correctly understand the obtained figures and make management conclusions and decisions based on them, it is enough for a manager to have basic financial literacy.

Answers to frequently asked questions

Question No. 1. What does “total capital” mean? What does it include?

The total capital of an enterprise is its own capital + borrowed capital (i.e., the total amount of all capital that exists and is used in the enterprise). This is the name for the entire liability (balance sheet currency).

Question No. 2: Is the presence of long-term liabilities of an enterprise a positive or negative factor? What should you use to correctly characterize this situation?

They are definitely not a negative factor. Quite the contrary, their presence is actually beneficial for the enterprise, especially in light of inflationary processes. Naturally, provided that they are attracted and used rationally, in moderation and competently.

| Business valuation | Financial analysis according to IFRS | Financial analysis according to RAS |

| Calculation of NPV, IRR in Excel | Valuation of stocks and bonds |