The net assets of a limited liability company (LLC) and a joint stock company (JSC) must be considered in the following cases:

- when increasing the authorized capital at the expense of the company’s property

- when a participant leaves the company (when shares are repurchased from shareholders)

- when deciding on the distribution of profits (payment of dividends)

- at the request of one of the participants or any interested party

- when preparing the annual report

The procedure for calculating net assets is currently defined by law only for joint stock companies. It was approved by Order of the Ministry of Finance of the Russian Federation N 10n, FCSM of the Russian Federation N 03-6/pz dated January 29, 2003 “On approval of the Procedure for assessing the value of net assets of joint-stock companies.” The same procedure is applied to assess the net assets of limited liability companies.

The actual value of the share of a company participant corresponds to a part of the value of the company's net assets, proportional to the size of his share.

Distribution of the management capital You can distribute the remainder by adding the required number of participants using the green “Add” button opposite the “Participant 1” field. Please note that the distribution occurs automatically, and therefore the remainder is divided into equal parts among the participants you added. If you want to change the monetary or percentage designation of a share for someone, then without clearing the form, simply enter the data in the required field. In this case, the size of the authorized capital will not change, but the share and balance will be recalculated. In the event that you need to find out the size of the charter capital based on the percentage (fractional) ratios of shares or their cash equivalents that you have changed, clear the “Authorized capital” field using a gray cross and click on the “Determine the charter capital” button again. At the same time, you will see the new capital balance and its percentage. You can also not use the balance obtained when calculating the size of the authorized capital, but immediately enter the data of all participants, and then find out how its share will change if it increases or decreases. In this case, the program will always tell you whether the size of the authorized capital has been exceeded or, conversely, whether a balance has appeared during the distribution of shares. If you want to increase the shares of participants in monetary terms, then the calculator will calculate what the size of the authorized capital should be in this case.

Online calculator of LLC shares

Calculation of shares in common shared ownership 1. The share in the right of common ownership of common property in a communal apartment of the owner of a room in a given apartment is proportional to the size of the total area of the specified room. 3. in the ownership of property in a communal apartment, the owner of a room in this apartment follows the fate of the ownership of the specified room. 5. The owner of a room in a communal apartment does not have the right to: 1) allocate in kind his share in the ownership of the common property in this apartment; 2) alienate his share in the right of ownership of the common property in this apartment, as well as perform other actions entailing the transfer of this share separately from the right of ownership of the specified room. 6.

Share calculation calculator online

To check the correctness of the calculations performed, you need to add everything up; the result of the addition should be 1 (unit). After the calculations of the owners' shares in the right of common ownership of the property are completed and the correctness of the calculations is verified, they are converted into votes.

Before calculating the apartment share, you need to take into account that such a calculation is acceptable for privatized and municipal housing, for which shared or joint ownership can be used.

Free legal assistance

Payment of a share to an LLC participant upon exit is a rather complicated mechanism, regulated by special rules of the relevant law, taking into account the numerous available court decisions made as a result of the consideration of controversial issues between the participant and the company. Let us consider below the reasons for termination of participation with receipt of the corresponding amount, the procedure for its calculation, payment, the period of transfer of money or things, the consequences of failure to pay the share on time and some other questions, the answers to which will allow you to avoid practical errors and subsequent disputes (including litigation).

How to calculate the share when a participant leaves an LLC

If the founder of the LLC does not agree with the size of the share that the company has determined, he has the right to come to the arbitration court and hand over the evidence in hand. In this case, the authorized body must check how correct the LLC’s calculations are. The evidence submitted to the court must be based on independent expertise.

It is worth highlighting another approach in a separate section, which calculates the actual price of the share in the event of the exit of the founder. In this case, the market price is taken as the basis. This option has been worked out by the judicial authorities, and is based on the resolution of the Supreme Arbitration Court of the Russian Federation numbered 3744/13. It notes that taking into account market prices implies the principle of fairness.

Lawyer Anisimov Representation and defense in court

However, there is no consensus among the courts as to what is meant by “last reporting date”. Thus, in the Resolutions of the Administrative Court of the North Caucasus District dated December 3, 2015 No. A53-17251/2013, the Moscow District dated August 13, 2015 No. A40-127386/11-137-451, the Seventh Arbitration Court of Appeal dated November 13, 2015 No. 07AP-9339/15, decision of the AS of the Sverdlovsk region dated May 30, 2016 No. A60-50788/2015, it is noted that such a date is the last calendar day of the month preceding the month the application was submitted (received by the company).

Redistribution of shares in LLC

A percentage is a hundredth of a number. On a calculator, you can multiply 1000 by 35 and click on the button. How to calculate how many percent one number is less than another. How to calculate shares in an apartment calculator. Before considering the question of how to calculate a share in an apartment, house or other real estate, it should be noted that it can be distinguished in privatized and municipal property. How to calculate shares is a formula. Contents: What is a percentage? Download a convenient calculator - any calculations, 3. Formula for increasing a number by a given percentage. Value with VAT. How to calculate shares in an apartment - calculator. It is not difficult to calculate the size of the part of the property for each participant using a special online calculator. The main conditions affecting the calculation Calculation of unequal shares in an apartment online calculator. Calculation of the cost of a share in an apartment calculator. How to calculate the share in an apartment formula. How to calculate fractions formula. Table of contents: Calculator for calculating the shares of LLC participants (beta). Based on these data, the calculator will calculate the size of the authorized capital and display it in the “Authorized capital” field, and also determine the balance in cash and How to calculate the share in an apartment online. There are also such calculators on the Internet, if it is impossible to do the calculations yourself, for example, a website offers a similar service. How to calculate the tax on the share of an apartment. Calculation of contribution. Online deposit calculator. Calculator on how to save for an apartment. How much can they give? For how long should I take out a loan? How profitable it is to buy a phone on credit. How to calculate the overpayment yourself? If we are told to calculate a share or asked to visualize numerical data, then we must give an answer in percentage. To do this, we repeat the previous step, then divide the numerator by the denominator (you can use a calculator or spreadsheet processor). Calculating and allocating a share is a difficult process that requires achievement. How to correctly calculate your share in an apartment. Real estate can belong to several owners, each of whom has his own share. How to calculate shares in an apartment - calculator. Calculation of percentages in Microsoft Excel. Online calculator for calculating percentage/share of a number. Enter the number value and the percentage/share that you want to calculate, then click the “Calculate” button. Online calculator for calculating percentage/share of a number. Enter the number value and the percentage/share that you want to calculate, then click the “Calculate” button. Shares of inheritance. Calculation. Calculator. The inheritance calculator allows you to calculate your share of the inheritance. To calculate, you need to fill in three parameters. A percentage is one hundredth, a fraction of 1, and is denoted by "". If 100 is considered to be one, then 1 is equal to 0.01. An online calculator will help you quickly and correctly calculate the percentage of a number. 3. If we are told to calculate a share or asked to visually present numerical data, then we need to give the result as a percentage. To do this, we repeat the previous step, then divide the numerator by the denominator (you can use a calculator or How to calculate shares in an apartment - calculator. How to calculate the tax on a share of an apartment. It is worth knowing that the tax base rate is calculated based on the cadastral value of the property, it is usually put in passport, the value of the share in the common property is indicated in How to calculate shares of something. Calculator for calculating shares of LLC participants (beta). Every educated person should solve problems on calculating shares of something. Possession of the skills of calculating shares is often required in practice. How calculate percentages of a number on a calculator? Percentages of a number on a calculator can be calculated in two ways: The simplest is using the button, with its help percentages are calculated like this. Service how to calculate shares in an apartment, the calculator will allow you to set the specific size of the allocated unit by the ratio of the total area of such an object and living space per individual family.

LLC “loses” a member

LLC on the simplified tax system (income).

One of the two founders died. What tax consequences await us when transferring his share to the heirs, in case of their refusal (the founders were close relatives), acquisition of his share by the company or the second founder? What is the period for withholding and paying personal income tax if necessary? Inheritance of shares

Shares in the authorized capital of the company pass to the heirs of citizens and legal successors.

According to Art. 1176 of the Civil Code of the Russian Federation, the inheritance of a participant in a limited liability company includes a share

this participant in the authorized capital of the company.

To acquire an inheritance, the heir must accept it

(

Art. 1152 Civil Code of the Russian Federation

).

In accordance with Art.

1153 of the Civil Code of the Russian Federation, acceptance of an inheritance is carried out

by submitting, at the place of opening of the inheritance, to a notary or an official authorized in accordance with the law to issue certificates of the right to inheritance,

an application from the heir

to accept the inheritance or an application from the heir to issue a certificate of the right to inheritance.

Admitted

, until it is proven otherwise

that the heir accepted the inheritance if he performed actions indicating the actual acceptance of the inheritance

, in particular if the heir:

– took possession or management of inherited property;

– took measures to preserve the inherited property, protect it from encroachments or claims of third parties;

– made at his own expense expenses for the maintenance of the inherited property;

– paid the testator’s debts at his own expense or received funds due to the testator from third parties.

The inheritance can be accepted within six months

from the date of opening of the inheritance (

Article 1154 of the Civil Code of the Russian Federation

).

Acceptance of inheritance after the expiration of the established period is regulated by the provisions of Art. 1155 Civil Code of the Russian Federation

.

Clause 8 art. 21 of the Federal Law of 02/08/1998 No. 14-FZ “On Limited Liability Companies”

It has been established that

until the heir of a deceased member of the company accepts the inheritance, the management of his share

in the authorized capital of the company is carried out in the manner prescribed by the Civil Code of the Russian Federation.

In accordance with Art.

93 of the Civil Code of the Russian Federation, the transfer of a share or part of a share of a company participant in the authorized capital of a limited liability company to another person

is permitted on the basis of a transaction or

in the order of succession

or on another legal basis, taking into account the specifics provided for by the Civil Code of the Russian Federation and the law on limited liability companies.

Shares in the authorized capital of the company pass to the heirs of citizens

and to the legal successors of legal entities that were members of the company, unless otherwise provided by the charter of the limited liability company.

The company's charter may provide that the transfer of a share

in the authorized capital of the company

to the heirs of

citizens and legal successors of legal entities that were participants in the company

is allowed only with the consent of the remaining participants of the company

.

A similar rule is contained in paragraph 8 of Art. 21 of Law No. 14-FZ

.

If the company's charter provides for the need to obtain the consent of the company's participants to transfer a share

or part of the share in the authorized capital of the company to a third party, such

consent is considered received

provided that

all participants of the company, within 30 days

or another period specified by the charter

from the date of receipt of the corresponding application

by the company to the company

, submit written statements of consent

to the transfer of the share or part of the share to a third party, or within the specified period, written statements of refusal to give consent to the alienation or transfer of a share or part of a share are not submitted (

clause 10 of Article 21 of Law No. 14-FZ

).

Thus, depending on what is written in the LLC Charter about the transfer of the LLC share to a third party

, the issue is being resolved as to whether the heir of the deceased LLC participant will be able to become a participant in the LLC or whether his share will pass to the LLC.

In the first case

upon receipt of a certificate of the right to inheritance and the consent of all LLC participants,

the heir becomes a participant in the LLC

.

If the heir of a deceased LLC member is also a member of the LLC

, then in accordance with paragraph 2 of Art.

17 of the Federal Law of 08.08.2001 No. 129-FZ “On state registration of legal entities and individual entrepreneurs”

for making changes to the Unified State Register of Legal Entities regarding information about a legal entity, but

not related to changes in the constituent documents of a legal entity

, the registration authority is presented with

an application signed by the applicant for making changes to the Unified State Register of Legal Entities in form No. R14001

“Application for making changes to the information about a legal entity in the Unified State Register of Legal Entities that are not related to making changes to the constituent documents”, approved by Decree of the Government of the Russian Federation dated June 19 .2002 No. 439.

The application confirms that the changes made comply with the requirements established by the legislation of the Russian Federation and the information contained in the application is reliable.

In cases provided for by law, in order to make changes to the Unified State Register of Legal Entities regarding the transfer of a share or part of a share in the authorized capital of an LLC, documents confirming the basis for the transfer of a share or part of a share

.

According to paragraph 16 of Art. 21 of Law No. 14-FZ, the application is accompanied by a document emanating from the company, confirming the transfer of a share or part of a share to the heirs of citizens and legal successors of legal entities who were members of the company.

In accordance with Art. 21 of Law No. 14-FZ, notarization is not required in case of transfer of a share to the heirs of citizens

and successors of legal entities

that were members of the company

.

Until the heir of a deceased company member accepts the inheritance, his share is managed

in the manner established by the Civil Code of the Russian Federation,

the executor of the will or the notary

.

Information about the person managing the share

, passing by inheritance,

are subject to reflection in the Unified State Register of Legal Entities

.

At the same time, to the registering authority in accordance with clause 16 of Art. 21 of Law No. 14-FZ are presented:

– an application for making appropriate changes to the Unified State Register of Legal Entities, signed by the executor of the will or a notary;

– a copy of the death certificate, certified in accordance with the procedure established by the legislation of the Russian Federation.

In accordance with paragraph 18 of Art.

217 of the Tax Code of the Russian Federation

, income in cash and in kind

received from individuals through inheritance

is not subject to personal income tax, with the exception of remuneration paid to the heirs (legal successors) of the authors of works of science, literature, art, as well as discoveries, inventions and industrial designs.

Thus, the income of an individual

-

an heir

received in the form of a share in the authorized capital of the company

is not subject to personal income tax

.

This is confirmed by the Ministry of Finance of the Russian Federation in a letter dated November 23, 2012 No. 03-04-05/4-1337.

The share does not pass to the heir

If the LLC refuses to transfer the share to the heir, then the company is obliged to pay the heir the actual value of the share

or give him in kind property corresponding to such value, in the manner and on the conditions provided for by the law on LLC and the charter of the company.

The actual value of the share to be paid to the heir is determined on the basis of the company’s financial statements for the last reporting period preceding the day of death of the participant

company, and is paid within one year from the date of transfer of the share to the company, unless a shorter period is provided for by the company’s charter.

The actual value of the share in the authorized capital of the company is paid out of the difference between the value of the company’s net assets and the size of its authorized capital

.

If such a difference is not enough, the company is obliged to reduce its authorized capital by the missing amount.

In accordance with Art. 20 of Law No. 14-FZ, the value of the company’s net assets is determined

in the manner established by federal law and regulations issued in accordance with it.

Considering that the federal law and the regulations issued in accordance with it have not established the value of the net assets of an LLC, in the opinion of the Ministry of Finance of the Russian Federation, LLCs can be guided by the order of the Ministry of Finance of the Russian Federation and the Federal Commission for the Securities Market of the Russian Federation dated January 29, 2003 No. 10n, 03-6/pz “ On approval of the Procedure for assessing the value of net assets of joint-stock companies"

(letter of the Ministry of Finance of the Russian Federation dated December 7, 2009 No. 03-03-06/1/791).

That is, the determination of the value of net assets in accordance with the above-mentioned order dated January 29, 2003 is carried out by both joint-stock companies and LLCs

.

the LLC's net assets is understood as the value

determined by

subtracting from the amount of

the company's assets accepted for calculation

the amount of its liabilities

accepted for calculation.

Grade

property, funds in settlements and other assets and liabilities of the company is carried out

taking into account the requirements of accounting provisions

and other regulatory legal acts on accounting.

To assess the value of the company's net assets, a calculation is made based on financial statements

.

The accounting entries will be as follows

:

DEBIT 81 “Own shares (shares)”

CREDIT 75 “Settlements with founders”

– the debt to the heir of the participant is reflected in the amount of the actual value of the share;

DEBIT 75 CREDIT 51 (50)

– the actual value of the share has been paid.

As the Ministry of Finance of the Russian Federation explained in letter dated April 15, 2009 No. 03-04-06-01/95, the income of an individual

-

the heir, received in the form of the actual value of the testator's share

in the authorized capital of the organization,

is not subject to personal income tax

, and

the organization paying the specified income is not a tax agent

and in this case does not have the obligation to calculate, withhold and transfer tax to the budget.

Transfer of share to LLC

The share or part of the share passes to the company from the date of receipt

from any participant in the company

refusal to give consent to the transfer of a share

or part of a share in the authorized capital of the company to

the heirs of

citizens or legal successors of legal entities who were participants in the company,

payment by the company of the actual value of the share or part of the share belonging to the company participant

, at the request of its creditors (clause Clauses 5, 6, Clause 7, Article 23 of Law No. 14-FZ).

Documents for state registration of relevant changes

must be submitted to the body carrying out state registration of legal entities

within a month from the date of transfer of the share or part of the share to the company

.

These changes become effective for third parties from the moment of their state registration.

The registering authority (IFTS) must be notified of the transfer of a share in the authorized capital of the company to the company.

no later than

within a month from the date of transfer of the share to the company

.

To do this, you must submit an Application for Entry

to the Unified State Register of Legal Entities of changes in information about a legal entity not related to amendments to the constituent documents, according to

form No. P14001

, approved by Decree of the Government of the Russian Federation of June 19, 2002 No. 439, and a document confirming the grounds for transferring the share to the company.

If during the specified period the share is distributed, sold or redeemed

, the body carrying out state registration of legal entities (IFTS), is notified by the company by sending an application to make appropriate changes to the Unified State Register of Legal Entities and documents confirming the grounds for the transfer of the share to the company, as well as its subsequent distribution, sale or redemption.

The specified documents must be submitted to the Federal Tax Service within a month

from the date of the decision on the distribution of the share among all participants of the company, on its payment by the acquirer or on redemption.

As the Federal Tax Service of the Russian Federation explained in a letter dated June 25, 2009 No. MN-22-6/ [email protected] , when distributing

, sale or redemption

of a share

or part of a company's share in the authorized capital of the company,

the following are submitted to the registration authority

:

– statement

on making appropriate changes to the Unified State Register of Legal Entities, signed by the head of the permanent executive body of the company or another person who has the right to act on behalf of the company without a power of attorney;

– decision of the general meeting

members of the company on the distribution, sale or redemption of a share or part of a share belonging to the company.

If

changes

Entities regarding the transfer of a share or part of a share in the authorized capital of a company to the company, as well as their subsequent distribution, sale or redemption, the following

must be submitted to the registering authority

:

– statement

on making appropriate changes to the Unified State Register of Legal Entities, signed by the head of the permanent executive body of the company or another person who has the right to act on behalf of the company without a power of attorney;

– documentation

, confirming the basis for the transfer to the company of a share or part of a share in the authorized capital, as well as their subsequent distribution, sale, and redemption.

When repaying a share

or part of the company's share in the company's authorized capital, the registration authority must also submit documents necessary to amend the company's charter in connection with a decrease in the company's authorized capital.

The list of such documents is established in paragraph 1 of Art. 17 Federal Law of the Russian Federation dated 08.08.2001 No. 129-FZ “On state registration of legal entities and individual entrepreneurs”

.

These changes become effective for third parties from the moment of their state registration.

Distribution of shares to other members of the company or sale of shares

According to Art. 24 of Law No. 14-FZ within one year from the date of transfer of the share

or parts of the share in the authorized capital of the company

to the company

, they must, by decision of the general meeting of participants of the company, be

distributed among all participants of the company

in proportion to their shares in the authorized capital of the company or

offered for acquisition to all or some participants of the company

and (or), unless prohibited by the charter of the company ,

to third parties

.

That is, in your situation, the share of the deceased participant transferred to the LLC can either be distributed to the only remaining LLC participant, or, if such a possibility is provided for by the LLC Charter, sold to a third party.

At the same time, the sale of shares

the deceased participant

is carried out at a price not lower than the price

that was paid by the company in connection with the transfer of the share to him, unless a different price is determined by a decision of the general meeting of the company's participants.

If within one year

from the date of transfer of the share in the authorized capital of the LLC to the company, this

share will not be distributed

to the remaining participant or sold to this participant or a third party,

then this share in the authorized capital of the LLC must be redeemed and the size of the authorized capital of the company must be reduced

by the nominal value of this share.

If the share of the deceased participant in the authorized capital passed to the company and was subsequently distributed to the only remaining participant of the company

, then, according to the Ministry of Finance of the Russian Federation,

income in the form of the difference

between the original and new value of the share of the sole participant in the company

is subject to personal income tax

on a general basis.

In accordance with paragraph 19 of Art.

217 of the Tax Code of the Russian Federation are not subject to personal income tax

, in particular,

income received from

joint-stock companies or

other organizations

by shareholders of these joint-stock companies or

participants

of other organizations as a result of the revaluation of fixed assets (funds) in the form of additional shares (shares, shares) received by them, distributed among shareholders or participants of the organization in proportion to their share and types of shares, or in the form of the difference between the new and original par value of shares or their property share in the authorized capital.

Since the increase in the value of the share of the sole participant of the company is carried out through the distribution of shares of participants who left the company to him, and not as a result of the revaluation of fixed assets (funds), then, according to officials, the provisions

of Art.

217 of the Tax Code of the Russian Federation do not apply in this case (letters of the Ministry of Finance of the Russian Federation dated March 15, 2013 No. 03-04-06/8031, dated March 9, 2010 No. 03-04-06/2-26).

Share distribution

in the LLC

in favor of the remaining

LLC participant is reflected

in the debit of account 75 and the credit of account 81

.

LLC as a tax agent is obliged to withhold personal income tax

from the income received during the distribution of the share to the remaining participant in kind.

The personal income tax amount must be transferred no later than the day following the day of actual deduction of the calculated tax amount ( clause 6 of Article 226 of the Tax Code of the Russian Federation

).

If the LLC does not pay the remaining participant income, then in accordance with clause 5 of Art. 226 Tax Code of the Russian Federation

If it is impossible to withhold the calculated amount of tax from the taxpayer, the tax agent is obliged, no later than one month from the date of the end of the tax period in which the relevant circumstances arose,

to notify the taxpayer and the tax authority at the place of his registration in writing about the impossibility of withholding the tax and the amount of tax

.

At the request of the remaining participant, the LLC must issue him a Certificate in form 2-NDFL

.

According to Art. 346.15 Tax Code of the Russian Federation

When determining the object of taxation, taxpayers take into account the following income:

– income from sales, determined in accordance with Art. 249 Tax Code of the Russian Federation

;

– non-operating income determined in accordance with Art. 250 Tax Code of the Russian Federation

.

When determining the object of taxation, the income specified in Art. 251 Tax Code of the Russian Federation

.

If the remaining participant buys out the share of the deceased participant from the LLC

, then the following must be taken into account.

According to paragraphs 3 p. 1 art. 251 Tax Code of the Russian Federation

When determining the tax base,

income

in the form of property, property rights, non-property rights having a monetary value,

which are received in the form of contributions (contributions) to the authorized

(joint)

capital

(fund) of the organization (including income in the form of excess of the placement price of shares (shares) ) above their nominal value (original size)).

P.p. 4 p. 3 art. 39 Tax Code of the Russian Federation

It has been established that

is not recognized as the sale of

goods, works or services

if such transfer is of an investment nature

(in particular,

contributions to the authorized (share) capital

of business companies and partnerships, contributions under a simple partnership agreement (agreement on joint activities), share contributions to mutual funds of cooperatives).

However, the Ministry of Finance of the Russian Federation believes that the sale of a paid share of a company, previously purchased by this company, cannot be considered as an operation to contribute property to the authorized capital of this company

.

In accordance with paragraph 1 of Art. 249 Tax Code of the Russian Federation

For tax purposes,

income from sales

is recognized as proceeds from the sale of goods (work, services) both of one’s own production and those previously acquired, and proceeds from the sale of property rights.

Thus, officials believe, society’s income from sales

a share in the authorized capital

previously purchased from a participant is considered

as the realization of property rights

(letter of the Ministry of Finance of the Russian Federation dated January 28, 2011 No. 03-03-06/1/32).

This means that the funds received by the company from the sale of the share are taken into account as income

when determining the object of taxation

for the tax paid in connection with the application of the simplified tax system

.

How to calculate the cost of a share in an apartment calculator

In order to find out the exact size of the authorized capital, it is enough to enter in the “Participant 1” field the value of his share and its (fractional equivalent) in the authorized capital and click the “Determine the authorized capital” button. Based on these data, the calculator will calculate the amount of your authorized capital and display it in the “Authorized Capital” field, and also determine the balance in monetary and percentage equivalents. The size of the capital can be determined by knowing any data of several participants (for example, one participant and the nominal value of the share of another).

Calculation of the share of a new participant in an LLC

Hello!

Please help me determine the amount of the share in the capital of the participants. The initial data is as follows - the only participant in the LLC, management company = 10,000 rubles, His share is now 100%. We are introducing a new participant into the LLC and increasing the authorized capital. The new participant's share must be 38% of the increased capital. According to my calculations with rounding, it turns out: 1. The authorized capital will be = 16,129 rubles 2. The authorized capital will be = 16,130 rubles - 38% = 6,129.02 rubles - a new participant or - 38% = 6,129.40 rubles - a new participant - 62% = 9 999.98 rubles - old member. — 62% = 10,000.60 rubles — old participant Good afternoon. Law 14-FZ “On LLC” Article 14 clause 2 The size of the share of a company participant in the authorized capital of the company is determined as a percentage or as a fraction

. The size of the share of a company participant must correspond to the ratio of the nominal value of his share and the authorized capital of the company. Your option 1 Share of “old” = 999,998/1,612,902 = 499,850/806,301 Share of “new” = 612,902/1,612,902 = 306,451/806,301

raschet_doley_uchastnikov_ooo.jpg

Related publications

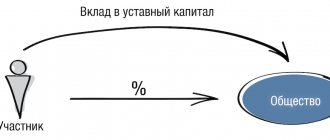

Determining the shares of LLC participants in the authorized capital (AC) of a company is relevant when the created company is controlled by several founders. The company's capital is the nominal value of its assets, which guarantees the stability of its operation in the event of claims from counterparty creditors.

The presence of a management company is a mandatory condition for the activities of an LLC. The sole owner of the company is both its founder and the absolute owner of the management company, while several participants have in shared ownership only parts of the authorized capital. How the shares of LLC participants are calculated will be discussed in the publication.

Actual value of a participant's share: calculation

This percentage distribution indicates not only the size of the paid part in the company's capital, but also the share of income from the company's activities, since the nominal size of the share, as a rule, does not correspond to an objective assessment of the business. Those. with a company's capital of 100 thousand rubles. its profit can be measured in very impressive amounts, and the value of fixed assets can be equal to millions of rubles, and it would be wrong to assume that a participant who decides to leave the company should receive only the value of the funds contributed to the management company.

Calculator for calculating net assets and actual share value

- when increasing the authorized capital at the expense of the company’s property

- when a participant leaves the company (when shares are repurchased from shareholders)

- when deciding on the distribution of profits (payment of dividends)

- at the request of one of the participants or any interested party

- when preparing the annual report

The procedure for calculating net assets is currently defined by law only for joint stock companies. It was approved by Order of the Ministry of Finance of the Russian Federation N 10n, FCSM of the Russian Federation N 03-6/pz dated January 29, 2003 “On approval of the Procedure for assessing the value of net assets of joint-stock companies.” The same procedure is applied to assess the net assets of limited liability companies.

Calculation of the participant's actual share upon exit

The Law “On LLC” (clause 2, article 14) regulates the procedure for calculating the objective part of the company belonging to each participant. It corresponds to the net asset value proportional to the percentage share in the company's capital.

For example, in an enterprise with a management company in the amount of 100 thousand rubles. the participant has a share of 30%. The amount of net assets, i.e. the difference between assets and liabilities on the balance sheet is 10 million rubles. on the settlement date. If this co-owner decides to leave the business, the company will be obliged to pay him 3 million rubles. (10,000,000 x 30%).

Thus, the share in the management company establishes for the participant the actual part of the joint business, which he has the right to count on upon exit.

The distribution of income (dividends) also depends on the size of the share of each co-owner. For example, based on the results of work for the year, the founders decided to pay remuneration in the amount of 2 million rubles.

Based on the example above, let’s calculate the share of income of each participant:

• The first one will receive 600 thousand rubles. (2,000,000 x 30%);

• Second – 840 thousand rubles. (2,000,000 x 42%);

• Third – 560 thousand rubles. (2,000,000 x 28%).

Naturally, the accountant will pay the amounts due to the founders minus income tax. You can read how to calculate dividends here.

Shares of participants (founders) of LLC

The authorized capital of a business company is divided into shares. Their size and number are established by the memorandum of association upon creation. The information is reflected in the Unified State Register (USRLE).

The ratio directly depends on the cost of deposits and affects the distribution. Disposal of shares is permitted only after they have been fully paid by the LLC participants. The procedure for making transactions is determined by the provisions of Law 14-FZ of 02/08/1998.

The same regulatory act introduced basic requirements for registering the transfer of rights.

Sizes of shares in the capital of the company

The abundance of terminology in the legislation on business entities gives rise to many problems. To avoid mistakes, founders are advised to understand the basic definitions. Thus, the concept of the share of an LLC participant is given in Article 14 of Law 14-FZ. The term denotes a structural unit of the company's authorized capital, reflecting the nominal value of the participant's contribution.

The size of the owner's share is not indicated in rubles. For this, percentages or simple fractions are used. The approach ensures the most complete reflection of rights in the management of the company, as well as fair payment of dividends. The maximum possible value of the scope of powers is achieved by the sole founder. His share is 100%.

The minimum amount of investment in the company for many years remains equal to 10 thousand rubles. The amount does not depend on the number of participants.

If an enterprise is created by several persons, each of them contributes a part in proportion to the acquired share. The corresponding rule is enshrined in Article 14 of Law 14-FZ. The entire amount is required to be paid in cash. The amendment was introduced by Article 66.

2 Civil Code of the Russian Federation. Participants make property contributions only to the extent that exceeds the minimum approved by law.

Note! The launch of projects in certain areas obliges the founders to invest large sums. Thus, for insurers the minimum authorized capital is 120 million rubles. The final figure is calculated taking into account special coefficients (Article 25 of Law No. 4015-1 of November 27, 1992).

The maximum limit is not defined by law. However, such a restriction is permitted to be established in the constituent document. The permissible amount of investments in the form of a fixed amount or percentage of the starting capital is prescribed in the charter as a separate paragraph (clause 3 of article 14 of law 14-FZ).

During the operation of the company, the size of shares may change. The founders have the right to provide protection against domination. The charter specifies the maximum share belonging to one owner. This reduces the likelihood of dictates from majority owners.

Payment Methods

The procedure for the performance of duties by participants is determined by the constituent agreement and decision. At the general meeting, one of the options for paying for shares is approved:

- cash only;

- securities, including bills of exchange;

- property rights;

- things (real estate, equipment, machinery, etc.).

The transfer of shares in the capital of another legal entity to a newly created organization still causes heated debate. The regulations do not establish a direct ban on the implementation of such schemes (Article 15 of Law 14-FZ). However, the transaction will need to be notarized. In this case, the preemptive right to repurchase does not arise (joint resolution of the Supreme Arbitration Court of the Russian Federation and the Supreme Court of the Russian Federation No. 90/14 of December 9, 1999).

Since 2014, the procedure for payment of shares by owners has changed. According to Article 16 of Law 14-FZ, the founders perform their duties for 4 months from the date of state registration of the company. When transferring property worth 20 thousand rubles or more to a company, an independent assessment will be required.

In practice, not all founders manage to pay their shares on time. The law does not define the procedure for holding people accountable for such a violation. However, an unscrupulous owner faces a number of restrictions.

He will not be able to attend general meetings, and if claims are made against the company, he will be liable for debts within the limits of the unpaid contribution. Sanctions may be applied within the framework of the constituent agreement. These include fines and penalties.

A long delay becomes the basis for the transfer of the share to the company with its subsequent repayment or distribution (Articles 23, 24 of Law 14-FZ).

The process of forming shares is reflected in the reporting. The total amount of the company's capital is classified as a liability on the balance sheet (account 80). Settlements with the founders, increases or decreases in the authorized capital are recorded by postings. The information is indicated on accounts 75, 84 and 83. The accounting procedure is regulated by Decree of the Ministry of Finance of Russia No. 66n dated 07/02/10.

Nominal and actual value

The successful operation of the company leads to an increase in net assets. The market price of the firm increases, but the nominal capital remains the same. An increase in the authorized capital can occur due to external investments, an increase in the cost of the industrial complex, the acquisition of valuable property rights, etc.

The discrepancy between the nominal and actual value of shares is inevitable. The process is reflected in Articles 14–15 of Law 14-FZ. The norms draw a clear line

between concepts. In the case of alienation of rights to a company, we are talking about a real assessment. The nominal value of shares may not correspond to the objective price. This is typical for enterprises with a large customer base, impressive turnover and a positive business reputation. That is why, before concluding transactions, an independent assessment is carried out or financial statements are analyzed.

Prohibition on payment of share value

Conducting commercial activities in Russia is carried out on a voluntary basis. At any time, the owner of the enterprise has the right to refuse participation in the LLC and return his investment. The condition is the presence of such a mechanism in the charter.

Restrictions on the exit of participants from business are established only in some cases (Article 23 of Law 14-FZ):

- signs of bankruptcy were detected;

- payment threatens to reduce the authorized capital below the minimum mark of 10 thousand rubles.

Article 26 of Law 14-FZ prohibits the resignation of the last or sole founder. A company cannot exist without an owner.

For payment, the objective value of the property right must be calculated. The part to be returned must correspond to the price of net assets in proportion to the share in the capital company (Clause 6.1, Article 23 of Law 14-FZ). The approach guarantees the interests of all owners and eliminates underestimation or overestimation of indicators.

Changes in the ratio and value of shares

The rights of a company owner are not constant. In the course of economic activity, the size of shares may change. The reasons for the correction are:

- Additional capitalization of the project at the expense of the assets of one of the participants. The procedure for making additional deposits is regulated by Art. 19 of Law 14-FZ. The decision is made at the general meeting. The basis is a statement from the interested founder. To change the ratio, 2/3 is enough. Other rules must be specified in the charter. The norm allows for additional capitalization of the company through the inclusion of third parties. However, this decision is already made unanimously.

- Increasing the authorized capital. Capital is increased through profits or additional contributions. The founders make decisions at a general meeting. In this case, only the nominal and real value of the shares increases. With equal contributions, the proportions remain the same (Article 18 of Law 14-FZ).

- Redistribution or redemption of shares. The implementation of this mechanism is possible in the event of a participant leaving the society (voluntary order, death, forced exclusion). Article 26 of Law 14-FZ obliges the company to buy back the rights taking into account the real cost. They are required to be redistributed among the remaining participants within a year after registration of the change in composition. For this purpose, a general meeting is convened (Article 23 of Law 14-FZ). If the founders are not ready to spend additional funds, the share is repaid with a decrease in the authorized capital and a change in the percentage of participation (Article 24 of Law 14-FZ). The rule does not apply if the result is a violation of the approved minimums. The conclusion follows from the analysis of clause 1 of Art. 20 of Law 14-FZ.

Any changes regarding company ownership require state registration. If we are talking about adjusting the authorized capital, notice P13001 is sent to the tax authority. In case of amendments only to the proportional ratio of shares, form P14001 is used (Article 17 of Law 129-FZ).

Features of the order

The founder may at any time exercise the right to alienate his share in a legal manner. This type of property is not limited in circulation. The condition for the validity of transactions is notarization and state registration. The most common cases were:

Method of transfer of rightsBrief descriptionPackage of documents

| Sale of a small part or all of the share in the authorized capital of the company | Alienation of rights to a company is regulated by Art. 21 of Law 14-FZ. When selling, the rule obliges to give preference to existing participants. For this purpose, the owner sends a special notice to the enterprise. The document is certified by a notary. The text outlines the essential terms of the transaction. The refusal of the participants to sign the agreement gives the right of first refusal to purchase the share to the company. The owner becomes the company itself. To implement the mechanism, the clause is prescribed in the charter (Part 2, Clause 4, Article 21 of Law 14-FZ). The norm is aimed at ensuring the constancy of the composition of owners. The founders are given 30 days to exercise their rights. The company makes a decision on the purchase within a week after the refusal of all owners or the expiration of the period given to them. Other rules are allowed to be prescribed in the charter | The legal basis for the procedure is an offer addressed to the founders and the company, a list of owners, a purchase and sale agreement, and a payment receipt. The transaction is certified by a notary. They also send a notification to the tax authority about the change of owner |

| Pledge of a participant's rights to own the company | The use of property rights as security does not contradict the law. In this case, the founder does not leave the ownership group. All transactions for pledging shares must be properly formalized. They must be agreed upon by the meeting of founders, and the agreement must be certified by a notary. The decision is made by the participants by a majority. In order to avoid controversial situations, the owners can establish a ban on pledging shares. Such a clause is included in the company's charter. The rules are enshrined in Art. 22 Law 14-FZ | The package of documents includes the owners’ decision to issue consent to the pledge, and an agreement to establish an encumbrance. The notification to the registration authority is sent by a notary (Article 22 of Law 14-FZ) |

| Donation | The gratuitous transfer of a share frees you from the need to comply with the rules on pre-emptive rights. Any of the participants can enter into an agreement. It is allowed to donate the owned part to other founders or third parties. It will not be possible to transfer a share to the company free of charge in this manner. Such a mechanism is simply not provided for by law. Relations will be regulated by Chapter 32 of the Civil Code of the Russian Federation | The procedure for donating a share is formalized in an agreement. Notarization is required. The change of owner is registered in the Unified State Register of Legal Entities. Changes to the register are made at the request of a notary |

| Inheritance by loved ones after the death of the owner | After the death of the founder, property rights pass to relatives or persons specified in the will. Inheritance shares are registered according to the general rules. The articles of association may provide for the payment of actual value in the event of the death of one of the participants. The clause protects the business from access to the management of unauthorized persons | The transfer of rights is recorded by a certificate of the right to inheritance. A notary is responsible for registering changes in the Unified State Register of Legal Entities |

Brief conclusions

Shares in the capital of a company are considered valuable property rights. Assets are not limited in circulation. They can become the subject of contracts, are part of an inheritance, or are pledged. Such transactions are carried out only in the presence of a notary, and are also subject to registration in the Unified State Register of Legal Entities.

Legislation strictly regulates the transfer of rights to commercial enterprises. The mechanisms are aimed at protecting against raiding and financial fraud. Dividing the company's capital into shares ensures effective management.

Each of the founders acquires the opportunity to influence the company’s activities and receives dividends in proportion to their participation.

Source: https://newfranchise.ru/baza_znaniy/ooo/doli-uchastnikov-uchreditelej-ooo

Calculation of shares of company participants after the exit of one of them

It is important for the company not only to correctly calculate the value of the share when a participant leaves, but also to fairly distribute the ratio of the shares of the co-founders remaining in the company. Let's figure out what the distribution of power will be like for two co-owners of the company after the third leaves the business, based on the initial data of the above example.

So, a participant with a 28% share in the management company leaves the company. At the time of its release, the value of net assets was 10 million rubles. Upon withdrawal of the participant, the calculation of the actual value of the share amounted to 2.8 million rubles. Upon completion of all formalities and payment of the share, its part in the management company should be distributed among the remaining participants.

For your information! A participant who decides to leave the LLC simply needs to notarize the corresponding application and submit it to the director. He leaves, taking a share of the income earned, and the share in the management company that previously belonged to him will be distributed among the remaining partners.

The calculation is carried out as follows:

The sum of voting shares will be 72% (30% + 42%), including:

the share of the first participant is 30/72;

the share of the second is 42/72.

Then the share that belongs to the LLC after the withdrawal of the participant (28,000 rubles) is multiplied by the shares of the remaining participants:

28,000 rub. x 30/72 = 11,667 rubles;

28,000 rub. x 42/72 = 16,333 rub.

From the share owned by the company, 11,667 rubles are transferred to the first co-owner, 16,333 rubles to the second, i.e. the monetary ratio of the shares changes:

the first participant has 30,000 + 11667 = 41667 rubles.

the second has 42,000 + 16,333 = 58,333 rubles.

The percentage of their shares in the management company also becomes different:

the first - 41,667 / 100,000 x 100% = 41.7%;

the second – 58,333 / 100,000 x 100% = 58.3%.

Thus, after a participant leaves the LLC, the ratio of shares in the company’s management company changes, but the amount of capital remains unchanged.

Calculate shares calculator online

A mathematical calculator in our familiar pocket version appeared in 1971. The prototype is manufactured by Bomwar. In the 70s, versions of devices with more adapted functionality were launched into production, incl. engineering calculator with degrees (Hewlett Packard in '72).

In mathematics, a fraction is a number that represents a part of a unit or several parts of a unit. A common fraction is written as two numbers, usually separated by a horizontal line indicating the division sign. The number above the line is called the numerator

.

The number below the line is called the denominator

. The denominator of a fraction shows the number of equal parts into which the whole is divided, and the numerator of the fraction shows the number of these parts of the whole taken.