Leasing is one of the most profitable opportunities for individual entrepreneurs to develop their business. This scheme may be of interest not only to beginning individual entrepreneurs, but also to those businessmen who have been working in the market for a long time and are striving to open new directions.

Question: An organization, after buying out a leased car, sold it to an individual entrepreneur at a price higher than the redemption price, but significantly lower than the market price. What tax risks arise in this case for the organization and the individual entrepreneur regarding income tax and personal income tax? View answer

Leasing for individual entrepreneurs. Concept and main points

At its core, leasing is a cross between a loan and rental property. Leasing is quite actively used by large enterprises, but in recent years its advantages have also been appreciated by some representatives of small businesses, including individual entrepreneurs.

Question: What taxes will an individual entrepreneur (UTII) pay when selling a car (purchased under lease), if the transaction is carried out by an individual and not an individual entrepreneur? View answer

The leasing scheme is quite simple: an individual entrepreneur enters into an agreement with the lessor for the purchase of any machinery, equipment, transport, etc. property and begins to actively use this property for its own commercial purposes. At the same time, he gradually pays the full cost of the leased asset. The key word here is “gradually”: payments are spread out over time and the purchase comes into ownership only when the lessee pays its full cost.

A return leasing scheme is also used, which consists in the fact that the lessor buys the property of interest and then leases it out to the seller himself. With this form of leasing, the recipient of the property actually retains both the asset itself and the funds, which can be used for any purpose. And when the leasing period expires, the right to ownership of the property will again return to the lessee.

For what reasons will they refuse to deduct VAT on leasing transactions ?

Car leasing for legal entities and individual entrepreneurs

A leasing agreement, at its core, is a set of financial and legal conditions that appear to the lessor in connection with the acquisition of ownership of any property, which he provides for a fee to another legal entity (lessee) for temporary possession and use.

Leasing agreements are a type of rental agreement and all the basic rules and principles of leasing apply to leasing, unless the law on financial leasing expressly provides otherwise.

.

At the same time, the fundamental difference between leasing agreements and rental agreements is a mandatory condition: the lessor acquires ownership of a car specifically for the lessee and transfers it to the lessee during the implementation of this agreement.

Another difference between leasing and rent is the possibility of the lessee purchasing the leased item (car) at the end of the leasing agreement under the condition that there are no outstanding lease payments.

The price at which the leased asset is purchased at the end of the contract term is the residual value of the car, which consists of the purchase price of the leased asset minus accrued depreciation.

A condition for the purchase of the car at the end of the leasing agreement may initially be contained in the text of the leasing agreement, but there are often cases when such a condition is not included in the text of the agreement, and at the end of the leasing agreement a separate agreement for the purchase of the car is concluded.

As a rule, the redemption price is a relatively small cost, in most cases it is equal to a purely symbolic 100 rubles.

Accounting for car leasing

The lessor can transfer the car to the lessee’s balance sheet as an object of fixed assets (it is important to remember that in this case the lessor will still be the owner of the leased asset). In this case, the legal entity - the lessee has the right to attribute to its expenses the amount of accrued depreciation for the period of validity of the leasing agreement. But we must remember that the lessee only receives the right to own and use the car; he does not have the right to dispose of it (provide the car as collateral, sell or otherwise alienate the property).

From the moment the car is transferred to the lessee, the entrepreneur has the right to write off all expenses arising during the operation of the car^

- costs for fuels and lubricants,

- vehicle repairs (both current and major),

- spare parts and other consumables.

A car leasing agreement can be a good source of financing for small and medium-sized businesses, as it makes it possible not only to constantly use a new luxury car (after all, a leased car can not be purchased, but simply replaced with a new one), but also to lease a truck that is already a source of income for the entrepreneur.

Website editors

Publications on the topics: how to get a car loan, which car to choose for credit, conditions for car loans in banks for new and used cars, how to repay a car loan ahead of schedule, CASCO and MTPL insurance for a loan car. The editors of the “Car on Credit” website help you understand the issues of obtaining, repaying and servicing a car loan

Was this publication useful to you?

Bookmark it on social networks!

Total score: 7Votes: 7

Where to buy a car with minimal risk of fraud

Trade-in is a system for buying a car, when the old one is accepted as a replacement for the new one.

We recommend other useful posts on this topic:

How to rent a car in installments without a down payment and a bank

Where to buy a car with minimal risk of fraud

Why buying a car through a loan is popular

How to buy a car on credit on favorable terms

“Gray” car dealership - how to recognize unofficial car dealers

What additional options to choose for your car?

The main advantages of leasing

The advantages of leasing transactions for individual entrepreneurs are visible at first glance.

- Unlike banks and other credit institutions, leasing companies have less stringent requirements for the life of an individual entrepreneur, as well as its financial condition, income and turnover.

- To obtain a leased asset, an individual entrepreneur is not required to draw up a business plan.

- The leasing company makes the final decision on the possibility of working with a specific individual entrepreneur in a fairly short time (sometimes within one day). At the same time, the required package of documents for concluding a leasing agreement is significantly less than that required for banking organizations.

- For individual entrepreneurs, when leasing under certain taxation regimes, tax breaks and benefits are possible.

- Leasing companies do not have commissions, which are necessarily included in almost all bank loan programs.

- After concluding a leasing agreement, an individual entrepreneur does not need to immediately pay the entire cost of an expensive purchase.

- As soon as the agreement is concluded, the entrepreneur can immediately begin to use any property purchased on lease.

- Leasing companies, as a rule, give the client the right to choose the supplier of a particular product.

- The client of a leasing organization most often does not need to look for guarantors or provide collateral.

- The higher the price of the leased object, the more favorable the terms of its purchase.

- You can pay all lease payments ahead of schedule (but usually this right occurs no earlier than six months after the conclusion of the leasing agreement).

- Leasing companies, although not very willing, nevertheless almost always meet halfway in situations where a deferred payment is required.

Thus, leasing has quite a lot of advantages.

What attracts individual entrepreneurs and legal entities? 10 advantages of leasing

Experts in the field of banking and investment business cite a number of undeniable advantages of leasing:

№1 Simplicity of design

Getting a lease is much easier than taking out a regular loan from one of the Russian banks. What is this connected with? Leasing is recognized as a less risky service. Most financial institutions are considering the possibility of providing this financial instrument even for businessmen with a zero balance. The probability of approval of a loan application in such a situation tends to zero .

#2 Freedom of choice

Are a passenger car or specialized vehicles needed to solve short-term problems? Then don't invest the full price in them. As soon as the planned project is completed, the entrepreneur has the right to independently sell fixed assets and not make payments. The future fate of the property will be thought about by its owner - a leasing company or one of the organizations affiliated with the bank.

No. 3 Flexible conditions

Under some agreements, lease payments for vehicles are made from the moment the vehicle begins to generate income. Leasing companies offer a number of options - deferred payment, preferential leasing, etc. The operational form is provided without making an initial payment (but an advance may be required!). In financial leasing, the initial payment can reach 49% of the value of the property.

No. 4 A small set of documents

Each lessor individually determines the list of documentation that a private entrepreneur or organization is required to submit for consideration to obtain approval.

However, the general package consists of the following items:

- application (in the form established by the LC),

- photocopy of passport,

- Unified State Register of Legal Entities,

- TIN.

Some companies request photocopies of VAT and 3-NDFL (for businessmen using the main tax system). Entrepreneurs working under the simplified tax system (USN) must provide a tax return for 2 or more reporting periods. Before submitting copies for review, have them certified by the tax service.

Attention! If the lessor has doubts about the financial stability of an entrepreneur or LLC, he has the right to request an original certificate of transactions on the current account from the bank.

No. 5 Benefits and relaxations

There are no additional commissions for leasing programs (unlike loans and insurance contracts!). In addition, in some tax regimes there is the possibility of a VAT refund.

#6 Unlimited choice of supplier

In 9 out of 10 cases, lessors give individual entrepreneurs the right to independently choose a supplier. The only thing is that they can introduce restrictions on the property purchased (for example, you can only buy trucks whose cost exceeds 850,000 rubles ). Remember the unspoken rule - the higher the price of the object of the agreement, the more favorable the terms of its purchase.

No. 7 Early payments under the agreement

The client of a leasing company has the right to repay payments under the agreement early, BUT most lessors introduce a restriction - they grant this right no earlier than six months after the conclusion of the agreement.

No. 8 Minimum security

The acquired property serves as collateral for leasing. There is no need to additionally provide real estate as collateral or involve guarantors. However, in Russia there are several programs that provide for the absence of a down payment, but the presence of solvent guarantors.

No. 9 Simplification of tax and accounting documentation

In reporting when leasing a vehicle for an individual entrepreneur, there is an accelerated depreciation scheme and a reduction in the tax base. Additionally, rental payments paid for property are included in the businessman’s expenses.

No. 10 Taxes are not increasing

A legal entity uses a vehicle, BUT it does not have ownership rights. Consequently, the property is not listed on the company’s balance sheet, is not included in the tax base and does not lead to an increase in taxes.

Demand for leasing from individual entrepreneurs

As the experience of Russian entrepreneurship shows, despite the obvious advantages of leasing over bank credit programs, this service is not in wide enough demand among individual entrepreneurs. This is due to several reasons:

- low awareness of individual entrepreneurs about the possibility of leasing machinery, equipment and other property;

- aggressive marketing policy of banks and a small amount of advertising in the wider media from lessors;

- insufficient number of leasing companies in the country.

Disadvantages of leasing for individual entrepreneurs

Perhaps, partly the not very high popularity of leasing in the Russian Federation is also justified by the negative factors that it has. These include:

- the need to make an advance payment (minimum 10% of the purchase price);

- mandatory insurance of the leased object (the lessee insures the leased object at his own expense);

- lack of ownership of the leased asset until its cost has been fully repaid under the leasing agreement;

- the possibility of unilateral termination of the contract with the individual entrepreneur by the lessor. True, this is only possible if the individual entrepreneur does not comply with the terms of the leasing, for example, a car purchased on lease repeatedly gets into accidents, does not pass technical inspections, etc.

Advantages and disadvantages of buying a car on lease

Leasing: A rental agreement is defined as an agreement between a lessor (the owner of the property) and a lessee (the user of the property) in which the former purchases property for the latter and allows him to use it in exchange for periodic payments called rent or minimum rental payments.

Advantages

- Balanced Cash Outflow (The biggest advantage of leasing is that the cash outflow or payments associated with hiring are spread over several years, saving the burden of a large one-time cash payment; this helps the business maintain a stable cash flow profile).

- Quality Assets (When leasing an asset, ownership of the asset still remains with the lessor, while the lessee simply pays the costs; given this agreement, it becomes possible for a business to invest in good quality assets that may otherwise appear unaffordable or expensive) .

- More efficient use of capital (given that the company chooses to hire rather than invest in an asset through purchase, it frees up capital for the business to fund its other needs or simply save money).

- Improved planning (leasing costs typically remain constant over the life of the asset or lease term, or rise in line with inflation; this helps plan expenses or cash outflows when budgeting).

- Low capital costs (leasing is an ideal option for a new business, given that it means a lower initial cost and lower capital investment requirements).

- Rights to terminate the contract (at the end of the lease term, the lessee has the right to purchase the property and terminate the leasing agreement, thereby providing business flexibility).

Flaws

- Lease expenses (rental payments are treated as expenses and not as equity payments on the asset).

- Limited financial benefit (when paying money for a car, the business cannot benefit from any increase in the value of the car; a long-term lease agreement also remains a burden on the business since the contract is locked in and the costs are fixed for several years. In case the use of the asset is not satisfactory needs after a few years, rental payments become a burden).

- Debt (Even though hiring doesn't appear on a company's balance sheet, investors still view long-term leases as debt and adjust their valuation of the business to include leases).

- Limited access to other loans (given that investors view long-term leases as debt, it may be difficult for a business to access capital markets and raise additional loans or other forms of debt from the market).

- Processing and documentation (in general, concluding a lease agreement is a complex process and requires careful documentation and proper study of the subject of leasing).

- Property Maintenance (The tenant remains responsible for the maintenance and proper operation of the rental property).

What doesn’t make lessors happy?

Why is leasing not as widespread as it could be, although it occupies a serious segment of small and medium-sized businesses? This is probably due to its features for the providing party:

- the amounts of leasing agreements are rarely large, otherwise it would be more profitable to simply buy an asset, therefore they are of less interest for large businesses;

- Individual entrepreneurs often do not reflect the actual financial condition in the reporting documents, which makes leasing operations a risky undertaking for the lessor.

Features of leasing a car under the simplified tax system

The simplified taxation system (STS) exempts from payment of VAT, income and property taxes, and personal income tax for entrepreneurs. Small and medium-sized businesses use the simplified tax system.

Leasing a car for businesses on a “simplified” basis has a number of nuances.

Let's understand them.

VAT refund and expense accounting

All leasing payments that a legal entity or entrepreneur pays under the simplified tax system under a leasing agreement are subject to VAT (20%). These include:

- Repayment of the cost of the leased item (repurchase of a car);

- Leasing interest, lessor's margin, insurance costs, transport tax.

The cost of the car is subject to VAT by the supplier, i.e. a car dealer from whom the leasing company purchases vehicles for the client. Accordingly, an organization using the simplified tax system pays this tax on a general basis, as if it were buying a car at a time using its own funds.

The main thing: the lessee cannot reimburse VAT on interest under the “simplified” system, unlike organizations operating on the general taxation system (GTS).

It makes sense for an enterprise using the simplified tax system to pay for insurance and transport tax on its own, taking advantage of the VAT benefit. If you include these expenses in leasing payments, you will also need to pay accrued VAT, that is, 20% plus. With the “simplified” approach, this overpayment is considered a cost.

Another feature: payments will be recognized as expenses, whereas for organizations on the OSN, they are included in the cost price.

Conclusion: subjects of the simplified tax system overpay VAT when leasing without subsequent reimbursement.

Service availability level

For businesses using the “simplified” system, the same procedure for registering car leasing works as for large organizations using the OSN.

Before redemption, a car is the property of a leasing company, which transfers the property for financial lease. This makes car leasing more accessible than a loan - no collateral or guarantors are needed, the transaction is completed using a minimum package of documents. For leasing under express programs of Gazprombank Autoleasing, 2 documents are enough.

Car leasing allows businesses using the simplified tax system to:

- Make a purchase with an investment of 5% of the cost;

- Receive a car in 3-5 days;

- Distribute costs over a period of up to 5 years;

- Repay obligations according to an individual schedule, including regression and payments based on seasonal income.

Conclusion: leasing for small businesses using the simplified tax system is an affordable way to buy cars with a convenient distribution of expenses.

Taxes for subjects of the simplified tax system in 2021

For individual entrepreneurs and companies, the previously existing rates have been retained: 6% on income, 15% on the difference between income and expenses.

Features of leasing for individual entrepreneurs

There are two options for obtaining a leased object for the duration of the leasing agreement:

- the leased object remains on the balance sheet of the leasing company;

- the leased object is transferred to the balance of the lessor's client.

Whatever the situation, the leasing agreement must provide for one of these two possible scenarios as a separate clause. Subsequently, the holder of the lease will have to include it in the depreciation of tangible assets.

Attention! If the property acquired under lease remains on the balance sheet of the lessor organization, then its client must take into account the fact that the lessor may well include the property taxes it pays in the lessee’s monthly payments under the leasing agreement.

Important! Payments under leasing agreements are always subject to VAT.

Principles and features of work

Leasing is the rental of property with the right of subsequent purchase. Leasing is based on a credit transaction. But, unlike a regular loan, equipment purchased under lease is the property of the lessor. At the same time, the businessman has the right to independently select the necessary property and its supplier. The lessor provides information services and ensures the operation by preparing the necessary documents.

The lessee uses the equipment, makes leasing payments on time and at the end of the contract, receives ownership of the property. All costs of operation and maintenance of the leased asset are borne by the individual entrepreneur.

An individual entrepreneur can purchase various property through leasing:

- production equipment;

- real estate (except land);

- motor transport;

- special equipment.

Another interesting program is the “return” scheme. According to it, the company buys property from the businessman and, under a leasing agreement, transfers it back to the same individual entrepreneur. The business receives money for development and does not lose the opportunity to use fixed assets. After the end of the rental period, the property is again re-registered as an individual entrepreneur.

Leasing can be different

For small businesses, whose representatives are individual entrepreneurs, leasing is a very popular business operation. Demand has generated several types of leasing offers:

- express leasing;

- leasing, without assessment of financial condition;

- specialized leasing (depending on the chosen tax regime).

Express leasing

Most often chosen by individual entrepreneurs, since its conditions optimally meet the interests of small businesses. The individual entrepreneur submits a leasing application to the company, which considers it at an accelerated pace: the decision on leasing is made no longer than a day, sometimes within 1 hour. If there is no refusal, the lessor assumes obligations to finance the lease for the applicant. After voicing the decision, the individual entrepreneur must provide a package of documentation, which is not numerous, so that the leasing transaction can be formalized. The parties quickly agree on the terms of the lease and enter into an agreement.

Leasing excluding financial assessment

This leasing product offers relevant services without assessing the financial condition of the entrepreneur, or such assessment is carried out to a minimum extent. Of course, the lessor is at financial risk, but as compensation he intends to receive a larger than usual down payment - up to half the cost of the leased property, as well as a higher interest rate. Often, an additional guarantee is provided by a third party guarantee for the lessee.

Leasing for individual entrepreneurs under different tax regimes

Under different taxation systems, leasing is taken into account differently:

- If an individual entrepreneur uses a simplified tax regime with an object of income minus expenses of 15%, then he has the opportunity to reduce the tax base by the amount of leasing payments.

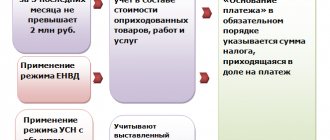

As for those individual entrepreneurs who are on the simplified tax system with an income of 6%, since their expenses are not taken into account, leasing payments do not affect the amount of tax in any way. Important! When choosing a leasing company, an individual entrepreneur should carefully consider what tax system it uses. This is important in order to eliminate unfavorable situations for “simplified” companies when the lessor works with VAT. The most interesting option: find a company that does not include VAT in its services, since it is also “simplified”. - If an individual entrepreneur uses two tax regimes simultaneously: UTII and the simplified tax system, then he is obliged to keep separate records for them.

Accordingly, leasing payments should be distributed evenly, based on the type of activity. However, the situation here is such that it is impossible to accurately attribute leasing payments to any specific type of activity, therefore expenses for this part are divided proportionally, depending on the income at the end of the quarter into UTII and simplified tax system. To avoid confusion under the two tax regimes, individual entrepreneurs should open special sub-accounts into which to enter all information relating to certain types of activities. For your information. Expenses on UTII cannot be classified as expenses that reduce the tax base on the “simplified” basis. - If an individual entrepreneur operates under the general taxation system, he can safely use leasing programs, without regard to any specifics. Leasing agreements under OSNO allow for very profitable optimization of taxation, so that individual entrepreneurs under the general tax regime can purchase property under leasing schemes on significantly more favorable terms than under any credit programs.

Attention! Whatever tax regime an individual entrepreneur uses, you need to be prepared for the fact that the lessor will require certification of the leasing agreement by a notary, which will entail additional costs in the amount of 1% of the agreement amount. In addition, in some cases it may be necessary to pay another tax, for example, transport tax when purchasing a car on lease.