The concept of controlled debt is contained in the Tax Code of the Russian Federation. The corresponding article 25 of the Tax Code of the Russian Federation appeared only in 2002. This regulation is often amended, since controlled debts are not yet fully regulated by law. The latest amendment came into force in February 2021. Let's try to understand the concept.

Question: The controlled debt of an organization to a foreign organization is more than 3 times the difference between the amount of assets and the amount of liabilities of the organization at the end of the second quarter. How to take into account the maximum interest rate for calculating income tax at the end of the third quarter if the debt is repaid during the third quarter? View answer

What is controlled debt?

Almost every company resorts to loans. They are needed to create conditions for the continuation of activities. If the funds were taken from a foreign entity, they may be considered controlled debt. Controlled loans are:

- Debts to a foreign company if the latter owns at least 1/5 of the authorized capital of its debtor. In this case, the nature of ownership does not matter: direct or indirect.

- Debts to a Russian company recognized as an affiliate of a foreign entity.

- To a Russian company whose loan is secured by a credit obligation (guarantee, guarantee and other methods). It is assumed that either the foreign company or an affiliate will be responsible for securing the obligations.

- To affiliated foreign entities, if the debt exceeds the company's capital by more than three times. If the debtor is banking institutions or leasing entities, the amount of debt to capital is assumed to be 12.5 times higher.

Question: When determining the capitalization ratio, how is the amount of outstanding controlled debt to one creditor calculated: separately for each debt obligation or for the organization as a whole (clause 2 of Article 269 of the Tax Code of the Russian Federation)? View answer

A controlled debt is formed by a domestic organization to a foreign entity or a company equated to a foreign entity.

BY THE WAY! A company that can influence the activities of another legal entity is considered affiliated.

The corresponding explanation is given in Article 4 of Federal Law No. 948-1 “On Competition” as amended on July 26, 2006.

The concept of a debt obligation in modern Russian practice and the main types of debt

Debt, or promissory note, in modern Russian practice, as well as throughout the world, is understood as the amount of funds that an entity must pay as repayment of debts. In accounting, there are two main types of debt - receivables and payables.

Accounts receivable is the amount of payments that a given organization is due to receive from its counterparties as a result of economic interaction with them. For example, accounts receivable will be the amount that the buyer owes to the organization that supplied him with any goods or services. Accounts payable is the amount that the organization itself must pay to its counterparties based on the results of economic relations with them. An example is a payment that an organization has undertaken to make for the supply of raw materials to its partner.

Thus, debt is often understood as amounts that have not been paid on invoices within a certain period of time, which may have occurred due to technical reasons, for example, the duration of payment through the bank. However, in current legislation, debt obligations also include planned long-term expense items, such as various loans and credits provided to organizations by specialized financial institutions or non-financial enterprises, regardless of the procedure for their execution.

Regulatory acts

Controlled debts are regulated by Article 269 of the Tax Code of the Russian Federation “Nuances of accounting for interest on obligations.” Previously, controlled debt was considered to be loans taken from foreign entities. However, in June 2005, amendments appeared that expanded the circle of creditors. In particular, loans to affiliated legal entities are now considered controlled. In 2005, Federal Law No. 58 was also signed, concerning changes in the second part of the Tax Code.

Question: Can a Russian organization with negative (zero) equity capital take into account interest on controlled debt (clause 4 of Article 269 of the Tax Code of the Russian Federation)? View answer

Debt is not considered controlled in these cases:

- It was formed when foreign legal entities placed bonds with the subsequent extraction of dividends.

- Debt has arisen to interdependent legal entities and individuals if they are recognized as tax residents throughout the reporting period.

- The individual and legal entities to which the debtor has a debt have no outstanding loans to affiliated legal entities throughout the reporting period.

In 2021, amendments were introduced that established new rules for accounting for interest on debts.

interest on controlled debt in

income tax

Interest calculation procedure

Before making calculations, you need to study what is included in the structure of controlled debt. The latter includes interest on obligations. Their size does not exceed the total amount of charges included in the percentage. Let's look at the procedure for calculating interest:

- At the end of each reporting period, the debtor transfers the maximum possible amount of interest accrued. Accruals are the ratio of the amount of interest accrued on the debt at the end of the period to the capitalization ratio.

- The coefficient is calculated as of the last date of the tax period. To obtain it, you need to divide the total amount of debt by the amount of the authorized capital. Then you need to divide the result by 3 (for ordinary legal entities) or 12.5 (for leasing companies and banking institutions).

- The authorized capital does not include arrears of fees and debts, late payments and deferred payments.

The main rule for determining controlled debts is their calculation at the closing date of the tax period. The billing periods are 3 and 9 months, half a year.

Interest is determined by these balance lines:

- Column 300 (assets).

- Columns 690 and 590 (liabilities).

- Columns 623 and 624 (debt of tax payments).

The calculation is performed using this formula:

Spread = Sact% * CoefCap

The formula contains these values:

- Spread is the maximum amount of interest recognized as an expense and subject to a reduction in the tax base.

- Cactual % - accrued interest.

- CoefCap – capitalization ratio.

To determine the capitalization rate, this formula is used:

CoefCap = Skz / Sobcap / 3

The formula uses these values:

- Skz – the amount of controlled debt that has not been paid.

- SobCap – the amount of the debtor's fund.

If the value of the fund is zero at the end of the period, interest on debt during the reporting period will not be taken into account.

Let's consider the main stages of calculations:

- Determination of the amount of equity capital. This value is equal to the share of direct or indirect participation of a foreign company in the debtor’s capital. To determine this value, you need to multiply your own capital by the share of participation of a foreign person.

- Setting the capitalization ratio.

- Establishing the maximum amount of interest that is taken into account for taxation on the basis of paragraph 3 of Article 269 of the Tax Code of the Russian Federation. For calculations, you need to divide the actual accrued interest by the capitalization ratio determined earlier.

IMPORTANT! If the interest on obligations is greater than the maximum interest (determined at the third stage of calculations), the resulting difference is recognized as dividends, which are paid to the foreign company. The amount will be taxed at a rate of 15% based on paragraph 3 of Article 284 of the Tax Code of the Russian Federation.

Determination of the tax base

To correctly calculate controlled debt, it is worth studying Article 285 of the Tax Code. It contains information about the periods used to calculate the taxable profit base. In particular, it determines advance payments based on the amount of income.

The calculation of taxable income in each period is calculated by increasing the total amount of money spent (reflected as a percentage) for the previous period by the total amount of money spent in the current period. It should be understood that this calculation occurs discretely (that is, without adding the accrued % for the previous period).

Provided that in the current taxable period the ratio of the organization’s capital and corporate capital is subject to changes in comparison with previously obtained data, then the percentages of the previous reporting periods are not recalculated.

Features of controlled debt management

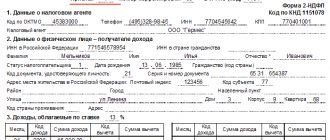

Interest on controlled liabilities is considered dividends. But the accountant must keep in mind that the accounting for these dividends differs in some nuances. In particular, for standard dividends, the 3rd sheet of the income tax return is filled out. To account for dividends from controlled debt, you need to fill out a document in KND form 1151056. When taxing, an accountant may encounter these nuances:

- The tax base is determined by the method of calculation. Payment of taxes on dividends and recognition of liabilities as controlled occurs on the final day of the reporting period. Reporting forms are completed taking into account payments transferred to foreign companies.

- Dividends from foreign entities to whom there are controlled obligations are subject to tax rates. The rate is determined on the basis of international treaties. Sometimes controlled liability provisions are used to deduct interest from the tax base. The measure under consideration is needed to prevent doubling of taxes.

- If an affiliate is distinguished by the indirect nature of its dependence on a foreign company, tax is not charged or withheld. Interest on debts is taken into account in the cost structure.

All the difficulties considered are successfully prevented. To do this, an accountant must have a good knowledge of the laws, all amendments, and also correctly interpret legal norms.

IMPORTANT! It is recommended to attach an explanation to the reports submitted to the tax authority. The document contains a list of regulations that were used in drawing up the report.

Administration

Can debt collectors sue? Restructuring of utility debts - .

The wiring assignment agreement - here are the details.

The tax charge accrued on dividends must be reflected in a timely manner in the relevant reporting in the form according to KND 1151056. Moreover, these costs do not need to be indicated in the tax return (namely in sheet No. 03), since in this case we are not talking about ordinary dividends.

Taxation of KZ interest is accompanied by the following difficulties:

- if the company's income is from 1,000,000 rubles, the tax base is formed in accordance with Chapter 25 of the Tax Code of the Russian Federation using the accrual method (this rule does not apply to enterprises with a lower level of income);

- if the liability arose in connection with indirect affiliation, it is not necessary to determine and pay the tax fee;

- If a report on accrued interest but not yet paid has been submitted to the Federal Tax Service, the government body has the legal right to reclassify this payment as a dividend or vice versa.

The CC indicator depends on three main factors - the amount of debt of the borrowing organization, the size of its own capital and the share of the foreign enterprise. If the coefficient has changed since the previous billing period, the question arises about the need to change the tax base.

Based on the innovations in the Tax Code of the Russian Federation and clarifications of the Supreme Arbitration Court, there is no need to make adjustments when determining the amount of the tax fee.