Taxation of individual entrepreneurs in 2021 is the procedure for interaction between an entrepreneur and the tax service. The tax burden on his business depends on the tax system under which an entrepreneur operates.

You need to think about what taxation to choose for an individual entrepreneur at the business planning stage, before you submit documents to the tax office for business registration. It is advisable to first choose a taxation system, prepare (if necessary) an application for transition to the desired regime, and only then open an individual entrepreneur.

Free tax consultation

What should an individual entrepreneur pay for?

Article 430 of the Tax Code of the Russian Federation establishes that entrepreneurs must list for themselves:

- insurance contributions for compulsory pension insurance (OPI);

- insurance premiums for compulsory health insurance (CHI).

That is, individual entrepreneurs provide themselves with a pension and annual medical care at their own expense. But in order to receive sick leave or maternity leave, you need to register with the Social Insurance Fund and also transfer contributions to your social insurance. But these contributions are voluntary, so not all individual entrepreneurs pay them.

Additional payments and taxes for individual entrepreneurs

Today, there are some types of business activities that require the payment of additional taxes. These activities include the following:

- water tax (for the use of water bodies);

- mineral extraction tax;

- tax on the production (sale) of excisable goods.

Individual entrepreneurs who have licenses (special permits), in addition to paying taxes, must make payments for the use of subsoil, pay fees for the use of objects of aquatic biological resources and objects of wildlife.

How much should an individual entrepreneur pay for himself?

Contributions for yourself are a known amount in advance, and it is also specified in the Tax Code. In 2021, you need to transfer 26,545 rubles to your pension insurance, and 5,840 rubles to medical insurance. Only 32,385 rubles, and this is the amount for a full year of activity of the individual entrepreneur.

If you have had the status of an individual entrepreneur for less than a year, the amount of mandatory contributions will be less - only for certain months and days. In such cases, it is convenient to calculate insurance premiums for individual entrepreneurs using our calculator.

For example, an entrepreneur was registered back in 2021, and on October 10, 2021 he was deregistered with the Federal Tax Service. The income received for this period was small - 280,000 rubles. We indicate the dates in the appropriate fields and receive the amount of contributions that this individual entrepreneur had to pay for less than a full year of activity.

You need to pay:

- contributions to compulsory pension insurance - 20,622.33 rubles;

- contributions for compulsory health insurance - 4,536.99 rubles.

Total 25,159.32 rubles.

But in addition to the mandatory amounts indicated above, entrepreneurs who have received an annual income of over 300,000 rubles must make an additional contribution. It goes only to pension insurance and amounts to 1% of income over 300,000 rubles.

Here is an example of calculating contributions we made using a calculator. The period of business activity remained the same, but income increased to 1.78 million rubles.

We get what we need to pay:

- contributions to compulsory pension insurance - 20,622.33 rubles;

- additional contributions for compulsory pension insurance - 14,800.00 rubles;

- contributions for compulsory health insurance - 4,536.99 rubles.

Total 39,959.32 rubles. The amount is increased by just 1% from income over 300,000 rubles per year, based on (1,780,000 – 300,000) * 1%) = 14,800 rubles.

The additional contribution to pension insurance has an upper limit. The maximum amount in 2021 is 185,815 rubles, and taking into account the mandatory contribution of 26,545 rubles, the transfer limit for individual entrepreneur pension insurance is 212,360 rubles.

Which tax system to choose for individual entrepreneurs

It is the right of the taxpayer to legally pay the minimum possible amount of taxes. To use it, you need to take into account a number of criteria.

OSNO can be used in any activity. For the simplified tax system, the spectrum narrows - you cannot produce excisable goods, except for grapes and wine materials, or engage in banking and insurance activities - the full list can be found in Art. 346.12 Tax Code of the Russian Federation.

Patent taxation for individual entrepreneurs: the types of activities of this special regime are limited to trade and services (see Article 346.43 of the Tax Code of the Russian Federation). Another drawback is that for each type of activity you need to take out a separate patent, and if you decide to move your business to another constituent entity of the Russian Federation, the patent there will be invalid.

The Unified Agricultural Tax can be applied specifically by agricultural producers, and not by manufacturing industries. At the same time, agricultural production should be the main activity of the entrepreneur and generate more than 70% of income.

NAP is a new tax regime that has been in effect in all regions of the Russian Federation since 2021. Here the lowest tax rate on income is from 4%, in addition, in this regime you do not have to pay contributions for pension insurance of individual entrepreneurs. However, there are a lot of restrictions here, the main ones being the annual income limit of 2.4 million rubles, the ban on hiring workers and the ability to engage only in certain types of activities.

In all special tax regimes, except for the Unified Agricultural Tax, there is no need to pay VAT, except for the tax when importing goods into the Russian Federation. On the one hand, this is a plus for an entrepreneur: VAT is one of the most difficult taxes to calculate and pay. On the other hand, large customers will not work with an entrepreneur who does not include VAT in the purchase price, which is to some extent a limitation for business expansion.

In 2021, a zero rate continues to apply for some entrepreneurs, the so-called tax holiday. Taxation of individual entrepreneurs on the simplified tax system and special tax system can be carried out at a zero rate for two years if the following conditions are met:

- the entrepreneur registered for the first time after the adoption of the relevant regional law;

- will work in the industrial, social or scientific sphere.

However, activities within the tax holiday do not exempt a businessman from paying insurance premiums for himself and his employees to extra-budgetary funds.

You do not have to be limited to one tax regime for all types of activities - the law allows you to combine taxation systems. For example, you have a large food production facility and a chain of stores in the region. Then production can work on OSNO (since it is important for wholesale buyers to charge VAT in the purchase price for reimbursement), and retail trade in stores - on PSN. But there are exceptions, for example, you cannot combine OSNO with simplified tax system.

So, how to find out the taxation system for individual entrepreneurs with a minimum tax burden? It is impossible to give a definite answer - you need to take into account not only the specifics of the future business, but also changes in legislation and benefits established at the federal and regional levels.

We are ready to help you with these calculations and offer a free consultation on individual entrepreneur taxation: 1C:BO specialists will conduct a comprehensive analysis of data on the region of work of the future businessman and types of activities and offer the most favorable tax regime.

What are fixed contributions

As you can see, the Tax Code deals with insurance premiums. Where did the concept of “fixed individual entrepreneur contributions” come from then? What are these payments?

In fact, fixed contributions and insurance premiums of individual entrepreneurs for themselves are one and the same thing. It’s just that this formulation began to be used after in one of its letters (dated October 6, 2015 No. 03-11-09/57011), the Ministry of Finance prohibited taking into account an additional contribution to reduce the tax on the simplified tax system.

Supposedly fixed, i.e. Only the amounts of mandatory contributions are predetermined, because they are the same for all individual entrepreneurs. But an additional contribution of 1% of income over 300,000 rubles, according to officials, “... cannot be considered a fixed amount of the insurance premium, since it is a variable value and depends on the amount of income of the insurance premium payer.” After this letter, mandatory contributions for oneself began to be called fixed payments for individual entrepreneurs.

But after two months the department changed its point of view. In letter dated December 7, 2015 No. 03-11-09/71357 it is recognized that since the additional contribution has a minimum and maximum allowable amount, it is also fixed and mandatory. This means that it corresponds to the wording of Article 346.32 of the Tax Code of the Russian Federation, which allows you to reduce the single tax on the simplified tax system at the expense of paid mandatory contributions.

Get a free tax consultation

Tax categories for individual entrepreneurs

Please note that all tax payments of individual entrepreneurs can be divided into categories. There are four of them:

- fixed payments by individual entrepreneurs for compulsory medical and pension insurance (“for oneself”);

- taxes and payments for compulsory types of insurance (deductions from employee salaries);

- taxes provided for by the taxation system applied by the individual entrepreneur;

- taxes and payments that are additional (depending on the type of business activity).

Basis for calculating insurance premiums

Let us remind you that the mandatory contribution amount of 32,385 rubles (26,545 rubles for pension insurance and 5,840 rubles for medical insurance) is paid by all entrepreneurs. On any taxation system, with any income or loss, whether conducting or not conducting a real business. As soon as you have received the status of an individual entrepreneur, contributions begin to accrue to you, with the exception of some grace periods, which we will discuss below.

As for the additional contribution, the annual income that the entrepreneur receives is taken into account. Unfortunately, the procedure for calculating the base for paying this contribution established in the Tax Code can hardly be called fair.

The fact is that 430 of the Tax Code of the Russian Federation defines different procedures for accounting for income received by an entrepreneur, which depends on the chosen tax regime:

- for a simplified taxation system - sales and non-sales income excluding expenses;

- for the general taxation system - income received, reduced by business deductions;

- for the unified agricultural tax – sales and non-sales income excluding expenses;

- for a single tax on imputed income - imputed income calculated using the UTII formula;

- for the patent taxation system, the potential annual income specified in the law or local administration decree.

What is the result? Individual entrepreneurs on the simplified tax system Income minus expenses and unified agricultural tax have the largest base for calculating contributions - all income received excluding expenses. But these tax regimes are characterized by a high share of costs in revenue.

For example, a simplified wholesaler receives a sales income of 130 million rubles, but taking into account the costs of purchasing goods (let’s assume 110 million rubles), his real income is only 20 million rubles. Moreover, he must be charged a single tax on 20 million rubles, and an additional insurance premium on 130 million rubles. Agricultural tax payers find themselves in a similar situation.

This approach to calculating the base for an additional contribution has already been recognized by courts many times as unfair. And in private, payers of the simplified tax system Income minus expenses and the unified agricultural tax may well challenge in court the assessment of an additional contribution on all income without taking into account expenses. But if we talk about the general case, the Ministry of Finance and the Federal Tax Service categorically do not accept this option.

Once upon a time, payers of the general system also found themselves in the same situation - they also did not have their income reduced for business deductions. But after the Constitutional Court of the Russian Federation intervened in this story, the necessary changes were made to the Tax Code.

And a few words about UTII and PSN. In these regimes, the tax is calculated based not on the actual income received, but on the one calculated in advance by the state. It often turns out that the real income of entrepreneurs is greater than the established one, so the additional contribution is small.

Prepare a simplified taxation system declaration online

Individual entrepreneur taxes on OSN

The general taxation system is not used very often by individual entrepreneurs. The use of OSN requires the payment of the following taxes by individual entrepreneurs:

- Personal income tax or personal income tax (which is paid on all income of an individual entrepreneur);

- VAT or value added tax;

- property tax (which the individual entrepreneur uses for business purposes);

- land tax.

Being on the General Taxation System (GTS), the individual entrepreneur pays VAT and personal income tax “for himself”.

Thus, while on the OSN, an individual entrepreneur pays at least two taxes.

When an individual entrepreneur may not pay contributions for himself

The general rule for paying insurance premiums is that they must be paid as long as an individual has the status of an individual entrepreneur. There are no payment benefits for pensioners, disabled people, large families and other similar social categories. If an individual entrepreneur works for hire in parallel with his business, this also does not relieve him of the obligation to pay contributions.

But the Tax Code still establishes several grace periods during which an individual entrepreneur has the right not to pay contributions because he does not operate for the following reasons:

- cares for a child under 1.5 years old, an elderly person over 80 years old, a disabled person of the 1st group, a disabled child;

- serves in the Russian army by conscription;

- lives outside the Russian Federation with a spouse who is an employee of a consulate or diplomatic mission;

- is with a military spouse under contract in an area where there is no opportunity for doing business.

You must notify your Federal Tax Service in advance that you are temporarily stopping paying insurance premiums for yourself by submitting an application in the prescribed form.

Individual entrepreneur taxes on PSN

This tax regime provides for the payment of a fixed tax by an individual entrepreneur. The individual entrepreneur pays the cost of the patent for the provision of services (for a certain period of time).

The cost of a patent and the list of activities that fall under the PSN are established by the authorities of the constituent entity of the Russian Federation.

Starting from 2021, entrepreneurs have the right to reduce the cost of a patent by paid fees and benefits. Individual entrepreneurs with employees have the right to deduct contributions from the cost of the patent for themselves and for their employees, but not more than 50 percent of the cost of the patent. The main thing is that employees work in those areas of activity for which you pay tax under the PSN. Individual entrepreneurs who do not use hired labor apply only contributions for themselves to the deduction (subclauses 1-3, clause 1.2, Article 346.51 of the Tax Code).

To reduce the cost of a patent, you will first have to notify the tax authorities. The Federal Tax Service has not yet approved the notification form, so it sent out the recommended notification form as an attachment to the letter dated January 26, 2021 No. SD-4-3/ [email protected]

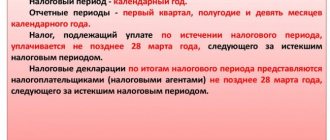

Deadlines for payment of insurance premiums

Unlike insurance premiums for employees, which are paid every month, individual entrepreneurs must pay mandatory contributions for themselves at any time until the end of the current year. That is, it is quite possible to transfer the entire amount of contributions immediately on the last day of December 2018.

But in practice, it is more convenient for those who work on the simplified tax system for income and UTII to pay contributions by dividing the annual amount into quarterly payments. Read about why this is so in the following articles:

- How an individual entrepreneur can reduce the tax on insurance premiums by 6% using the simplified tax system

- How to reduce tax through individual entrepreneur contributions to UTII in 2021

An additional contribution to pension insurance can be paid as soon as the amount of income of an individual entrepreneur in 2021 exceeds 300,000 rubles. The deadline for paying the additional contribution is July 1 of the following year. That is, the individual entrepreneur can choose when to transfer this amount - before the end of 2018 or until mid-2021.

Individual entrepreneur taxes on UTII

Since 2013, the transition to paying a single tax on imputed income (UTII) has been voluntary. The amount of this tax is determined by a special formula. To calculate the amount of UTII tax, the value of the basic profitability of an individual entrepreneur is taken, which is established by the government authority of the constituent entity of the Russian Federation. The tax calculation formula also includes coefficients that reflect the specifics of the individual entrepreneur’s work.

The single tax on imputed income is suitable for entrepreneurs who have a constant and stable income.

When applying UTII, the amount of tax payment does not depend on the actual income of the individual entrepreneur. Therefore, if the expected income is low, it is better not to apply UTII, but to use a different taxation system.

Please note that from 2021, UTII will be abolished for those entrepreneurs who sell labeled goods (furs, clothing, shoes, medicines, etc.). And starting from 2021, UTII has been cancelled. Entrepreneurs are invited to switch from UTII to PSN or simplified tax system from 01/01/2021.

Where to transfer insurance premiums

Not so long ago, mandatory payments from individual entrepreneurs were transferred to the Pension Fund, which is why they are still sometimes called contributions to the Pension Fund. But since 2017, these payments have been controlled by the Federal Tax Service, so the payment document must indicate the details of your tax office.

A sample receipt or payment order can be requested from the territorial Federal Tax Service or prepared on the Tax Service website. The BCCs for transferring individual entrepreneur contributions 2021 are as follows:

- for pension insurance – 182 1 0210 160;

- for health insurance – 182 1 0213 160.

Comments

View all Next »

Mikhail 01/20/2016 at 11:13 pm # Reply

Pensioners and mandatory payments to individual entrepreneurs

Colleagues, I will retire soon, but I want to become an individual entrepreneur. The tax regime is most likely the simplified tax system. Do I need to make a payment: Contribution to the Russian Pension Fund (PFR)?

Natalia 01/21/2016 at 08:17 # Reply

Mikhail, good afternoon. According to the current legislation of the Russian Federation, you are required to make payments to the Pension Fund and the Federal Compulsory Medical Insurance Fund as soon as you register as an individual entrepreneur, even if you are a pensioner. The legislation does not provide any tax breaks for individual entrepreneurs. Moreover, from 2021, working pensioners do not have the right to annual indexation of pensions.

Mikhail 02/03/2016 at 07:17 # Reply

Again please! Do I need to pay 1% on the amount over 300,000 rubles on UTII?

Natalia 02/05/2016 at 15:00 # Reply

Mikhail, good afternoon. When applying UTII, if the imputed income exceeds 300,000 rubles, you must pay 1% on this amount to the Pension Fund until 1.04 of the year following the reporting year. Your actual income does not matter in this case. The calculation is based on imputed income, from which 300,000 must be subtracted.

Tatyana 02/05/2016 at 15:00 # Reply

Hello. I register as an individual entrepreneur for house decoration, can I get a tax holiday?

ostapx1 02/05/2016 at 15:22 # Reply

Hello Tatiana! Regions have the right to introduce tax holidays. But only some regions took advantage of this right. Therefore, you need to study the legislation of your region in this regard.

Natalia 06/27/2016 at 01:02 pm # Reply

Tatyana, you can take advantage of tax holidays if the authorities of your region have adopted a corresponding law. The Federal Law allows the use of tax holidays, but for this there must be a decision of the local legislative assembly.

Alexander 02/21/2016 at 11:10 am # Reply

Hello, what taxes exist for private household plots and are there any concessions?

Natalia 02/21/2016 at 12:38 # Reply

Alexander, good afternoon. In Art. 2 of the Law of 07.07.2003 No. 112-FZ “On personal subsidiary plots” defines personal subsidiary plots (abbreviated as private household plots). Private household plots are a form of non-entrepreneurial activity for the production and processing of agricultural products. Those. You do not need to register as an individual entrepreneur. The Tax Code of the Russian Federation exempts from taxation the income of citizens received as a result of the sale of livestock and crop products grown in private household plots. But at the same time, the following requirements of the Tax Code of the Russian Federation must be met: 1. The total area of the land plot (plots), which (are) located (at the same time) under the right of ownership and (or) other right of individuals, does not exceed the maximum size established in in accordance with paragraph 5 of Art. 4 of Federal Law No. 112-FZ. Each region has the right to set maximum plot sizes by regulatory legal acts of local governments. 2. The taxpayer must maintain private household plots without the involvement of hired workers. Only family members can be involved in work. 3. The taxpayer must submit to the tax authority a document issued by the relevant local government body (the board of a horticultural, gardening or dacha non-profit association of citizens), confirming that the products sold were produced in his private household plot; Despite the fact that clause 4 of Article 2 of the above-mentioned Law establishes that “the sale by citizens running a private subsidiary plot of agricultural products produced and processed during the conduct of a private subsidiary plot is not an entrepreneurial activity,” it must be borne in mind that if You sell most or all of the products grown in private household plots and purchase and sale transactions are concluded constantly, and the buyers are individual entrepreneurs or organizations, then the tax authorities may consider the activity to be entrepreneurial. If you are the owner of a private household plot and registered as an individual entrepreneur, then tax inspectors almost always try to include income from the sale of agricultural products grown in the private plot in his income from business activities, on the general basis required for individual entrepreneurs.

Elena 03/04/2016 at 11:27 # Reply

I am an individual entrepreneur on the simplified tax system. I paid the mandatory payment to the Pension Fund and 6%. can I withdraw the rest of the money from the account for myself? Or do I need to pay personal income tax on this amount?

Natalia 03/04/2016 at 20:38 # Reply

Elena, good afternoon. You can safely manage the entire amount in your current account, the main thing is not to violate the deadlines for paying advance payments of the simplified tax system and contributions to the Pension Fund and the Federal Compulsory Medical Insurance Fund. Individual entrepreneurs on the simplified tax system without employees do not pay personal income tax.

Alexander 03.23.2016 at 20:26 # Reply

Good afternoon Please specify which amount of income is subject to 1% tax. Real income or imputed income i.e. settlement for individual entrepreneurs.

Natalia 03.23.2016 at 21:56 # Reply

Alexander, good afternoon. Your question, as far as I understand, refers to the additional contribution to the Pension Fund - 1%. If so, then 1% under the simplified tax system is taken from the difference between total income and 300 thousand rubles, under UTII the difference from imputed income and 300 thousand rubles is taken, under PSN the difference between potentially possible income and 300 thousand rubles is taken.

Anatoly 04/19/2016 at 09:44 # Reply

Good afternoon Are there tax benefits for individual entrepreneurs if it is registered in the name of one of the parents of a large family?

Natalia 06/27/2016 at 01:18 pm # Reply

Anatoly, good afternoon. There are no tax benefits for individual entrepreneurs if they are one of the parents of a large family. There are tax benefits for large families, whether you are an individual entrepreneur or not - personal income tax deduction, for transport tax, for property tax. At the federal level, there is not a single federal law regulating the rights and freedoms of large families; this is provided for by the regional legislation of the region where you live .

Victoria 06/09/2016 at 08:05 # Reply

If I open an individual entrepreneur, how much% will I pay monthly to the Pension Fund?

Natalia 06/27/2016 at 13:00 # Reply

Victoria, good afternoon. An individual entrepreneur without employees is required to pay fixed contributions to the Pension Fund and the Federal Compulsory Medical Insurance Fund, regardless of the amount of actual income, in an amount depending on the minimum wage. In 2021, there is a minimum wage of 6,204 rubles for the payment of fixed contributions. Therefore, during the year, until December 31, 2016, you must pay: to the Pension Fund - 6204 x 26% x 12 months = 19356-48 to the FFOMS - 6204 x 5.1% x 12 months = 3796-48 You can pay in any amount monthly or one-time at the end of the year.

Evgeniya 06/27/2016 at 12:20 # Reply

Hello, please tell me, I want to open an individual entrepreneur and rent a small room 2x3m for a shop of handmade goods. Approximately how much will this cost me? I live in the Voronezh region. Thank you.

Natalia 06/27/2016 at 01:11 pm # Reply

Evgeniya, it all depends on the taxation system you choose. The only constant amount for individual entrepreneurs without employees is fixed contributions to the Pension Fund and the Federal Compulsory Medical Insurance Fund - 23,153-33 rubles. When choosing PSN or UTII, paying taxes will not depend on your actual income; with the simplified tax system, you will pay either 6% of income or 15% of the difference between income and expenses. In the Voronezh region, each municipality has the right to independently apply tax rates, everything depends on where you will carry out your activities. For example, with a sales area of 6 sq m, in the Borisoglebsk district for 12 months the PSN will be 30,000 rubles. For UTII, you need to know the adjustment coefficient k2 for your district.

View all Next »