The income limit for applying the simplified tax system in 2021 is established by order of the Ministry of Economy. To apply the simplified tax system in 2021, income under the simplified tax system must be no more than 60 million rubles, which are multiplied by the deflator coefficient for 2021 (it has not yet been approved at the moment). This is the income limit for applying the simplified tax system in 2016.

Chapter 26.2 of the Tax Code of the Russian Federation contains conditions, if violated, taxpayers lose the right to use the simplified system. It says that if income under the simplified tax system exceeds the income limit, then the simplified person must switch to the general regime. The transition to the general regime occurs from the quarter in which the income limit for applying the simplified tax system in 2021 is exceeded.

How to calculate the income limit under the simplified tax system in 2021

Organizations using the simplified tax system should take into account all types of profit when calculating the income limit in 2021. Let us remind you that only if the limited value established at the legislative level of 150 million rubles is observed and not exceeded, LLCs and individual entrepreneurs can use the “simplified” tax system. All income coming to the organization, as a rule, is reflected in the KUDiR (Income and Expense Accounting Book), namely, in the “Income” column. It should be taken into account that, in contrast to determining the taxable base, in this case the total amount of income cannot be reduced by the amount of expenses.

The “Income” column reflects the entire profit of an individual entrepreneur or organization on a simplified tax system. These data can be safely used to calculate the maximum turnover under the simplified tax system in 2021, since the “simplified people” use the so-called cash method in their work when determining the profit received. This means that they only take into account funds that actually passed through the company’s cash desk or entered its r/account. Thanks to this, it becomes possible to take information from the “Income” column of KUDiR for any required reporting period: year, half-year, 1st and 3rd quarter, and it will be correct.

When calculating the individual income limit, an accountant of a company or individual entrepreneur must take into account all types of profit received since the beginning of the reporting period:

- funds received from the sale (sale) of goods, services, etc. (revenue);

- amounts not received from sales (non-sales), for example, paid rent, receipt of interest on loans, etc.;

- receivables, the reimbursement of which occurred not in monetary terms, but in some other way (for example, claims were offset);

- advance payments.

But here you should take into account possible nuances. For example, if a certain advance amount has been received at the cash desk or on the account of an organization, which after some time will be reasonably returned to the client (counterparty), then its value will not be included in the calculation of the total amount of income. At the same time, it should also be excluded from the tax base (Article 346.17 of the Tax Code of the Russian Federation).

Another case worthy of attention is when another company joins a company whose activities are based on a simplified taxation system. At the time of such affiliation, it is imperative to calculate the total amount of income of both companies in order to find out whether it exceeds the permissible limited value.

This is done because the affiliated organization ceases to conduct any activity at all, that is, it no longer exists as a separate legal entity. face. Therefore, all the profit received by it since the beginning of the year is added to the income of the company that has undergone reorganization. But this does not lead to the formation of a new legal entity; simply, the reorganized company assumes all the rights and obligations of the affiliated company (Article 50 of the Tax Code of the Russian Federation, Articles 57, 58 of the Civil Code of the Russian Federation). If at the time of merger and recalculation the total income of the reorganized company is more than 79 million 740 thousand rubles, it will have to immediately switch to the general taxation system.

Some types of profits of LLCs and individual entrepreneurs located on the simplified tax system are not included in the total amount of their income:

- amounts received from the results of activities on UTII;

- income listed in Article 251 of the Tax Code of the Russian Federation;

- dividends.

Tax rates under the simplified tax system

Under the simplified system, there are two possible ways to calculate tax:

- up to 6% of the entire amount of income

- up to 15% of income minus expenses specified in Article 346.16 of the Tax Code of the Russian Federation.

An organization can choose the object of taxation itself and change it by first submitting an application to the Federal Tax Service. In this case, the method of calculating the tax base will be changed from the beginning of the next tax period (calendar year).

Starting from 2021, the current tax rate can be regulated by regional regulations for various types of activities in the range from 1 to 6% in the first case and from 5 to 15% in the second (No. 232-FZ). For individual entrepreneurs registered in 2021, a zero rate may be applied in the first two years if the entrepreneur provides household services (for example, furniture repair, tailoring, photography studio, etc.)

An important change regarding VAT has come into force in 2021. Now presented to clients, for example, in invoices, VAT can be ignored in the amount of income. However, it should be kept in mind that VAT cannot be included in expenses.

Minimum tax rule and loss

For taxpayers who choose the tax base “income minus expenses”, the rule is that the tax paid for the year must be at least 1% of the income received. If the difference between income and expenses does not meet these requirements, then the organization is obliged to pay the minimum tax, regardless of the size of the tax base for the year. A loss received in a given year can be included in the expenses of the next year or any other year for 10 years, after which this amount will “burn out.” At the same time, the obligation to make a minimum tax payment to the budget remains.

Which bet is better?

To determine the optimal tax rate for a particular business, you need to make a forecast of income and expenses for the coming year and calculate the approximate amount of tax for the objects “income” and “income minus expenses.” It is important to consider that you can reduce the amount of income only by the amount of expenses confirmed by a cash receipt, payment order or bank account statement. You can only take into account the expenses specified in clause 1 of Article 346.16 of the Tax Code of the Russian Federation.

An effective tool for calculating tax according to the simplified tax system for small organizations is online accounting.

What to do if the maximum revenue under the simplified tax system in 2021 is exceeded?

If the total value of all company income received since the beginning of 2021 exceeds the established income limit (RUB 150 million), then it will inevitably be transferred to the general tax payment system. The transition takes place in the same quarter in which the maximum allowable limit was discovered to be exceeded. In order to do this correctly and avoid penalties, you must follow the following sequence of actions:

- Complete all settlements with the Tax Service according to the simplified tax system.

- Before the 25th day of the month in which the excess of the established income limit was recorded, it is necessary to submit a declaration according to the simplified tax system (Article No. 346.23 of the Tax Code of the Russian Federation) to the Federal Tax Service.

- From the beginning of the quarter in which an excess of the permissible value of the total amount of income was discovered, all taxes, including on property, profit, added value and others, must be calculated according to the rules of the OSN.

- All tax reporting from this moment on is carried out in accordance with the current tax payment system.

- For organizations that have been forced to switch from the simplified tax system to the special tax system, a taxation procedure identical to that applied to newly formed organizations is applied.

Revenue limit

For the purpose of applying the “simplified tax”, two income limits are used. They are needed for different purposes:

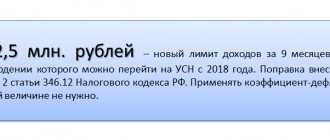

- one is used to switch to a special regime for companies that are going to use the simplified tax system starting next year. The amount is calculated for 9 months of the year in which the notice of transfer is submitted; its value is specified in clause 2 of Art. 346.12 Tax Code of the Russian Federation;

- the second controls the revenue received by the simplified entity (company or individual entrepreneur) for the tax period. Its value is calculated on an accrual basis from the first of January, the amount is determined in clause 4.1 of Art. 346.13 Tax Code of the Russian Federation.

The taxpayer must independently compare the limit values with the indicators of his business activities.

Income limit for individual entrepreneurs on a patent

For individual entrepreneurs who are on the patent system of calculations and payment of taxes (PSN), as well as for those who work under the simplified tax system, the legislation provides for a certain income limit. But, unlike the “simplified people,” the total profit of entrepreneurs on a patent should not exceed 60 million rubles. from the beginning of the year, in such cases the deflator coefficient is not applied. This value applies only to those activities for which patents were acquired. If from the beginning of the year (tax period) the total amount of all accounted income of a businessman exceeds the permissible limit, then he will have to switch to a general tax payment system. This must be done from the beginning of the tax (reporting) period for which the patent was received.

The income limit established for PSN is not subject to annual revision; it does not change or be indexed. This figure is 60 million and does not increase depending on the increase in the deflator coefficient, since it is not multiplied by it.

The deflator coefficient for PSN in 2021 still exists and is equal to 1.425. But, as mentioned above, this value does not at all affect the income limit established for the current year. Depending on it, only the size of the potential income of the individual entrepreneur on the patent changes. This suggests that in 2021 the cost of a patent will increase. The lower limit for potential income has not been determined, but there is an upper limit and amounts to 1 million rubles. To obtain an indicator relevant in 2021, this figure must be multiplied by the deflator coefficient (1.425), resulting in the maximum value of potential income - 1 million 425 thousand rubles. Depending on the region and types of activity of the entrepreneur, this value can be increased up to 10 times.

Billing periods and deadlines for submitting documents to the simplified tax system

Individual entrepreneurs and simplified organizations make advance payments by the 25th day of the month following the reporting period. Advances paid are offset against tax at the end of the year.

In total, from January to December the payer must make three advance payments corresponding to the reporting periods:

- for the first quarter - from April 1 to April 25;

- for half a year - from July 1 to July 25;

- for nine months - from October 1 to October 25.

The tax return by agents under the simplified tax system is submitted in the next calendar year by March 31 for an LLC and April 30 for an individual entrepreneur . You must also provide the tax authority with:

- book of income and expenses;

- for organizations additionally forms No. 1 and 2 (balance sheet and profit and loss statement).

At the same time, the final payment for the year should be made, taking into account previously made advance payments. In case of delay, a penalty is charged, and for non-payment a fine of up to 40% of the tax amount is imposed. Failure to comply with the deadline for filing a declaration also faces a fine of 5 to 30% of the unpaid amount for each month of delay.

Income limit for individual entrepreneurs combining simplified taxation system and PSN

What can be the maximum income of an entrepreneur when combining the simplified taxation system and the PSN in 20167? For such cases, the same income limit applies as for individual entrepreneurs and LLCs on the simplified market - 150 million rubles. But to determine the total amount of all income of a businessman, it is necessary to add up the profit received from activities on the simplified tax system and the special tax system. The resulting amount is compared with the established income limit.

Similar articles

- USN expenses accepted for taxation 2017

- Simplified tax system “income minus expenses” - accounting policy

- Rules for calculating the minimum tax under the simplified tax system

- Income limit under the simplified tax system in 2021

- Types of activities of individual entrepreneurs under the simplified taxation system

Transition to simplified tax system

To take advantage of the simplified tax treatment, the taxpayer must submit an application form 26.2_1 . This does not have to be done during the process of registering an LLC or individual entrepreneur, but it must be done within 30 calendar days from the date of registration. If you miss this deadline, you will have to submit tax reports according to the OSN system (general taxation system), that is, in a much larger volume. Existing taxpayers cannot change the tax regime in the current tax period, that is, in a given calendar year. However, they have the right to switch to the “simplified” system starting next year. To do this, you need to submit 2 copies of the notification to the tax service in the 4th quarter of the current year.

New KBK codes in 2021

Among other things, starting from 2021, the BCC for payment of contributions for employees, as well as payment of fixed contributions for individual entrepreneurs, will change.

The change in KBK codes occurs on the basis of Order of the Ministry of Finance of Russia dated 06/08/2015 No. 90n.

You can obtain the BCC values for paying contributions to the Pension Fund and the Compulsory Medical Insurance Fund in 2021 from your tax office.

Thank God, this order does not provide for any increase in payments, but simply changes the KBK itself where payments for employees and individual entrepreneur contributions are made.

simplified tax system and benefits for business

It is beneficial to use the simplified tax system for running your business, and therefore this taxation system is widespread among legal entities. It has several advantages that set it apart from other taxation methods.

Before you start using the simplified tax system, you have the right to choose one of two tax rates:

- 6%, if your activity contains income items and minimizes expenses (in this case, the entrepreneur pays only 6% of the profit amount);

- 15% if the company has both income and expenses (first the difference between the profits and expenses received for the year is calculated, and then 15% is deducted from the amount received - this is the tax payable).

These rates can be differentiated in different regions and reduced to a minimum of 1% for some types of activities.

Business owners using the simplified tax system pay only one tax instead of:

- Income tax (for founders of organizations);

- personal income tax;

- VAT (although there are exceptions. For example, if you enter into a transaction with non-residents, you are still required to pay VAT).

The simplified tax system has a rather simplified reporting system: paying a single tax makes running your business easier.

There are also the following features for companies using the simplified tax system:

- You can transfer the payment of insurance premiums, transport tax and other expenses to expenses (for the simplified tax system with a tax rate of 15%);

- The simplified tax system does not limit a company from having a representative office.

How to submit a personal income tax report in 2021

Changes await us here as well, and if you have employees whose earnings are subject to personal income tax, then the 2NDFL report is submitted by April 1 of the year following the reporting year.

Now, additional reporting has been introduced in addition to personal income tax certificates; organizations and entrepreneurs will have to submit quarterly personal income tax payments (based on law dated May 2, 2015 No. 113-FZ).

Personal income tax calculations are submitted quarterly:

- First quarter – the calculation must be sent by April 30;

- Half-year – the calculation must be sent before July 31;

- Nine months – the calculation must be submitted by October 31;

- Annual – annual calculations must be submitted together with 2NDFL reports before April 1 of the year following the reporting year.

When you employ 25 people or more, the report must be submitted electronically.

If it is less than 25, then it can be done on paper. To be honest, a small business that employs 25 or more people... is very rare. In my city I know only 3 people who fall under this criterion.

In general, small businesses simply do not face these restrictions, precisely because they are so small.

As always, in case of delay in submitting personal income tax calculations, organizations and individual entrepreneurs will face a fine of 1000 rubles. for each month that they are overdue. So, we deliver everything on time.

What is included in the concept of “single tax”

A tax payment under a simplified regime for representatives of small and medium-sized businesses replaces a number of other payments that they are required to make to the budget. The single tax according to the simplified tax system replaces for LLC:

- tax liability provided for the profit received by the company (with the exception of income from dividends on shares and proceeds from the company’s debtors);

- property tax (an exception has been introduced since 2015 - organizations are not exempt from paying tax on real estate if the tax base for it is the cadastral value);

- VAT (except for customs and other cases provided for by law).

For individual entrepreneurs, tax payments under the simplified tax system include:

- Personal income tax, when the income was received through commercial activities;

- property tax for individuals, if the property is not included in the list specified in Art. 378.2 of the Tax Code of the Russian Federation;

- VAT (exception – customs “import” VAT, tax under simple partnership and trust management agreements).

Simplified tax limit for 2021

Every year, the Russian Ministry of Economic Development publishes an administrative document in which it indicates the income threshold for entrepreneurs. The revenue limit under the simplified tax system for 2021 is 150 million rubles.

All organizations and individual entrepreneurs who operate under a simplified system for paying tax obligations are required to adhere to the threshold established by the ministry when doing business. If the company’s revenue exceeds the revenue limit under the simplified tax system for 2021, then it undertakes to switch from the special system to the general regime for paying tax obligations. This must happen from the moment the simplified tax system limit was exceeded (that is, in the same quarter).

The established limit for the “simplified tax” for 2021 must be calculated by both companies and private entrepreneurs. In this case, the object of taxation (“income” or “income minus expenses”) does not matter.

USN tax “income” or “income minus expenses” in 2016-2017: which is better?

When choosing a subtype of special mode, you need to consider several nuances:

- The object for calculating tax in the “income” format is the entire total income from business activities. In the “income minus expenses” version, the expense part is subtracted from its value, and the accrual is made, in fact, on profit.

- If the base is income, then in monetary terms the standard rate is 6%; when applying a “minus”, the rate reaches 15%.

- You can only deduct documented expenses, and also take into account the fact that not all of them can be deducted. Here you should be attentive to the question of whether the costs relate directly to the conduct of activities.

Advice : if you doubt that the fiscal authorities will agree that the expenses you have incurred are those that can be classified as proven, then it is better not to include them in the calculations. For example, you purchased new upholstered furniture for your office space and reduced your income by the amount of this purchase. If you do not agree with such a tax operation, you will be charged a fine for underpayment.

- Conditional calculations confirm the profitability of using the simplified tax system of 15% in cases where the expenditure portion is equal to or exceeds 60% of income. However, here you need to remember about the correspondence of costs, their evidence, and the like.

Important: only documents of the established form are considered as confirmation of expenses. These can be tickets, receipts, coupons, subscriptions and other strict reporting forms, the use of which requires a BSO accounting book for individual entrepreneurs, invoices, checks, TTN and the like. In addition, expenses must comply with the list of the Tax Code of the Russian Federation, or they require the fulfillment of special conditions. You should find out all these details directly from your tax office.

- On the simplified tax system of 6%, insurance premiums are fully deductible; on the simplified tax system of 15%, the amount of the deduction is no more than half of the accrued tax amount.

- For the simplified tax system of 15%, the rule of mandatory minimum tax (1% of annual income) applies. If the real income is less than the minimum, then the “minimum” is paid.

- Particular attention should be paid to the moment of operation of the selected system. She is elected by the entrepreneur once a year, and the next transition is possible only after the end of the calendar year.

Determining which subtype of special regime is best is necessary only based on the nuances of your own business. A larger (15%) figure, but a smaller income due to the deduction of expenses, may be more attractive for those who are confident in their ability to prove their expenses, and their amount will be at least 60% of the income. The simplified tax system of 6% is beneficial for those entrepreneurs who do not incur such high costs directly related to their activities.

Also, when calculating tax, you need to take into account the algorithm for calculating insurance premiums, which can be deducted from its amount:

- fixed size for individual entrepreneurs “for yourself” RUB 3,796.85. to the Federal Compulsory Medical Insurance Fund (medical insurance), RUB 19,356.48. in the Pension Fund of the Russian Federation (pension), as a result in 2016 only 23,153.33 rubles;

- from income over 300 thousand, another plus 1% in the Pension Fund;

- The maximum contribution to the Pension Fund for 2021 is set at 154,851.84 rubles, therefore, if the estimated payment for income exceeds 300 thousand is exceeded, it cannot be more than specified.

That is, if you receive an income of 20 million rubles by the end of this year, then your calculation of insurance payments will look like this:

- paid during the year and equal to 23,153.33;

- estimated additional contribution - (20,000,000 - 300,000) x 1% will be 197 thousand;

- actually payable - 154,851.84 (max amount) - 19,356.48 (PF contribution), that is, 135,495.36 rubles. Please note that if the estimated additional contribution exceeds the maximum payment amount established by law, the additional payment will always be the specified amount. The calculation is relevant only for individual entrepreneurs without employees.

Payment of 1% to the Pension Fund for income over 300,000 rubles

Please note that if an individual entrepreneur received an income of more than 300 thousand rubles during the reporting period, then an additional 1% of the excess amount is paid to the pension fund (PFR). For example, if an income of 400,000 rubles is received, then you will additionally need to pay (400,000 – 300,000) * 1% = 1,000 rubles.

Important! In a letter dated December 7, 2015 under number No. 03-11-09/71357, the Ministry of Finance explained that this payment will be equated to a mandatory fixed payment, so the simplified tax system can also be reduced by this amount. Do not confuse this amount with the minimum tax!

Types of systems in Russia

Within the framework of modern Russian legislation, there are several procedures for calculating payments to the state. They differ in the features of use - rates, bases, payment frequency.

General system (OSN)

This is a standard option, automatically assigned to all individual entrepreneurs, LLCs and other organizations, unless a corresponding application is submitted to switch to other forms of payment. OSN is the most complex mode in terms of calculations and accounting documentation. It is usually used by those firms that cannot be guided by other conditions of relations with the state (with a high number of personnel or large volumes of revenue).

Simplified scheme in the Russian Federation

The simplified taxation system in 2021 is a special form of relationship that provides the greatest benefit for a commercial entity. A significant number of activities fall under the algorithm; under the simplified tax system there is only one payment, amounting to 6% or 15%, based on certain parameters.

Imputed principle

This option involves a single payment of a fixed amount. Used in retail trade and other areas of activity. The size of the profit does not play a role here, since the fixed amount to be paid is established by law.

More about UTII

Features of the application of the three most common taxation systems can be presented in the following diagram:

Common agricultural regime

This is a special scheme designed for the activities of persons engaged in farming activities. In this mode, one value can be used to replace other payments, which simplifies paperwork.

Patent scheme

This is a special direction exclusively for individual entrepreneurs whose number of employees does not exceed 15 people. While using the regime, the entrepreneur has the right to count on purchasing patents one at a time. When making calculations, income does not play a role.

Among all payment algorithms, “simplified” is popular due to the possibilities of ease of accounting and cost minimization.

The advantages of working on a patent can be summarized as the following:

Patent scheme

Let's switch to OSNO

Legislative norms oblige those who switched to OSNO to inform the tax authorities about this within 15 days after the end of the reporting period. Once the transition has taken place, the taxpayer is required to pay all applicable taxes, just like newly registered companies.

If an organization or individual entrepreneur, when switching to OSNO, overlooked the payment of monthly payments, this is not a reason for fines from the tax authorities. As a punishment, penalties will follow in the amount of unpaid tax.

Initial data

Let’s assume that by the end of 2021 the simplified tax system with the object “income” has the following indicators:

| Period | Income on an accrual basis, rub. | Advance payment (tax), rub. | Incremental amounts that can be deducted, rub. | How much can you reduce the advance payment (tax), rub. | Advance payment (tax) to be paid additionally, rub. |

| I quarter | 300 000 | 18 000 (300 000 × 6%) | 10 500 | 9000 (10 500 ˃ 18 000/2) | 9000 (18 000 — 9000) |

| Six months | 800 000 | 48 000 (800 000 × 6%) | 18 500 | 18 500 (18 500 | 20 500 (48 000 — 18 500 — 9000) |

| 9 months | 2 000 000 | 120 000 (2 000 000 × 6%) | 50 000 | 50 000 (50 000 | 40 500 (120 000 – 50 000 – 9000 – 20 500) |

| 2016 | 3 000 000 | 180 000 (3 000 000 × 6%) | 102 000 | 90 000 (102 000˃180 000/2) | 20 000 (180 000 – 90 000 – 9000 – 20 500 – 40 500) |

The following link shows how to fill out a declaration under the simplified tax system “income” for 2016 by an accountant at Guru LLC.