According to the Tax Code of the Russian Federation, individuals receiving income in Russia are required to pay personal income tax on the total amount of income. But they have the right to a refund of part of the tax previously paid to the budget. Payers can exercise their right by submitting a declaration for a tax deduction directly to the tax authority at their place of residence in person or through their representative, sending by mail with a list of attachments attached, or transferring through the Unified Portal of State Services or the Internet service “Taxpayer’s Personal Account.”

Procedure for submitting income tax returns

It is necessary to report profit in 2021 in the format approved by Order of the Federal Tax Service of the Russian Federation dated October 19, 2016 No. ММВ-7-3 / [email protected] If the average number of personnel for the last year did not exceed 100 people, then the declaration can be submitted on paper (clause 3 Article 80 of the Tax Code of the Russian Federation).

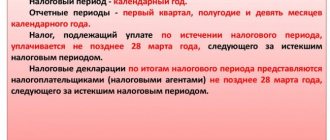

The annual declaration is submitted by March 28 of the year following the reporting year, so you must report for 2021 by March 28, 2018 (Clause 4 of Article 289 of the Tax Code of the Russian Federation).

For the reporting period, it is submitted no later than the 28th day of the month following this period. At the same time, the specific deadlines for submitting the declaration depend on how the advances:

1) monthly, based on actual profit: advance payments are paid, and the declaration is submitted monthly until the 28th, the reporting periods in this case will be a month, 2 months, 3 months, and so on until the end of the calendar year;

2) quarterly: advance payments are determined based on the results of the quarter, half a year, 9 months; In the current year, the deadlines for filing a declaration and paying quarterly advances are as follows:

- for the first quarter - no later than April 28, 2017;

- for half a year - no later than July 28, 2017;

- for 9 months - no later than October 30, 2017.

Major changes in 2021 that individual entrepreneurs need to know about

Individual entrepreneurs applying the simplified tax regime will have to submit a new declaration form to the regulatory authorities in 2021. This form changed in the spring of 2021 (from April 10). As a result, individual entrepreneurs must report using the new form for 2021.

Business entities conducting business as individual entrepreneurs and applying the UTII tax regime will also have to report to the fiscal authorities using a new form. In 2021, individual entrepreneurs paying a single tax on imputed income will also expect pleasant surprises. For example, individual entrepreneurs who employ hired workers will be able to deduct insurance premiums made for themselves from the single tax from January 1. According to information leaked to the media, the new UTII declaration form should appear approximately in November-December 2021. Until this time, fiscal officials plan to make final changes to the report form and present it in an updated form to business entities.

Individual entrepreneurs can read in more detail about all the upcoming changes relating to the UTII tax return in the bill entitled “On amendments to the order of the Federal Tax Service of Russia dated July 4, 2014 No. ММВ-7-3 / [email protected] On approval of the tax return form for the unified tax on imputed income for certain types of activities, the procedure for filling it out, as well as the format for submitting a tax return for the unified tax on imputed income for certain types of activities in electronic form.”

How to pay advance payments and income taxes

The Tax Code of the Russian Federation provides for 3 methods of paying advances:

1) based on the results of the first quarter, half a year and 9 months, plus monthly advance payments within each quarter (the method is common to all organizations);

2) based on the results of the first quarter, half a year and 9 months without paying monthly advance payments (clause 3 of Article 286 of the Tax Code of the Russian Federation): it is used by those companies whose sales income over the previous four quarters did not exceed an average of 15 million rubles for each quarter (60 million rubles per year), as well as budgetary, autonomous institutions, non-profit organizations that do not have income from sales;

3) at the end of each month, based on the actual profit received, the Federal Tax Service must be informed about its application before December 31 of the year preceding the tax period in which the transition to such an advance payment system takes place.

Letter of the Ministry of Finance of the Russian Federation dated March 3, 2017 No. 03-03-07/12170

Editor's note:

reporting for 9 months, determines whether monthly advance payments must be made for October, November and December. The calculation includes the amount of income from sales (excluding VAT and excise taxes) for the fourth quarter of the previous year and the first, second, and third quarters of the current tax period. If the indicator exceeds the specified limit, then the organization pays monthly advances.

The deadline for paying income tax for the year is the same for everyone - until March 28 of the next year (clause 1 of Article 287 of the Tax Code of the Russian Federation, clause 4 of Article 289 of the Tax Code of the Russian Federation): the tax for 2017 is paid no later than 03/28/2018.

How are the deadlines for submitting 3-NDFL related to the deadlines for paying taxes?

What are the deadlines for filing a 3-NDFL declaration?

If you need to calculate and pay personal income tax for the next tax period (year), submit the 3-NDFL declaration after its end - before April 30 of the next year (clause 1 of Article 229 of the Tax Code of the Russian Federation). If April 30 falls on a weekend, then the deadline for filing the 3-NDFL declaration is shifted to the working day following this weekend (Clause 7, Article 6.1 of the Tax Code of the Russian Federation). Taking into account these rules, the deadline for submitting 3-NDFL in 2021 falls on 04/30/2021, because it's a working day. This deadline for submitting 3-NDFL is valid for:

- individual entrepreneurs, private practitioners;

Step-by-step instructions for filling out 3-NDFL by an entrepreneur were prepared by ConsultantPlus experts. Get free demo access to K+ and go to the Ready Solution to find out all the details of this procedure.

- foreign citizens working in the Russian Federation under a patent;

- citizens who received income:

- from tax agents who did not withhold tax upon payment;

- entrepreneurial activity;

- rental of property;

- sale of property owned for up to 3 years, securities, shares in the authorized capital;

- donations;

- remuneration of copyright heirs.

NOTE! The declaration for 2021 must be submitted using the new form from the order of the Federal Tax Service dated August 28, 2020 No. ED-7-11/ [email protected] You can download the form by clicking on the picture below. And in this article you will find detailed explanations about filling out the report and a sample.

How to report if there are separate divisions

As a general rule, a “profitable” declaration is submitted by the organization to the Federal Tax Service at the location of its location and at the location of each separate division (clause 1 of Article 289 of the Tax Code of the Russian Federation).

At the location of the organization, a declaration is submitted, drawn up for the organization as a whole with the distribution of profits among separate divisions (SU). That is, in addition to those declaration sheets that are common to all taxpayers, Appendix No. 5 to sheet 02 of the declaration is filled out in an amount corresponding to the number of existing OPs (including those closed in the current tax period).

If the organization’s divisions are located on the territory of one subject of the Russian Federation, you can decide to pay tax (advance payments) for this group of enterprises through one of them (clause 2 of Article 289 of the Tax Code of the Russian Federation).

Organizations that pay tax (advance payments) for a group of EP through the responsible division submit declarations to the tax authorities at the place of registration of the organization (head office) and at the place of registration of the responsible OP.

If the organization itself (head office) and its subsidiaries are located in the same region, then profits do not need to be distributed to each of them. An organization has the right to pay tax for its OP.

If the parent company pays income tax for its divisions, it has the right to submit a declaration to the Federal Tax Service only at its location.

However, if a company decides to change the tax payment procedure or adjusts the number of structural divisions on the territory of the subject, or other changes occur that affect the tax payment procedure, then this should be reported to the inspectorate.

Letter of the Ministry of Finance of the Russian Federation dated July 3, 2017 No. 03-03-06/1/41778

Editor's note:

A different procedure for filing declarations is also provided for the largest taxpayers. They submit all declarations, including those regarding OP, to the inspectorate, where they are registered as the largest taxpayers (clause 3 of article 80, clause 1 of article 289 of the Tax Code of the Russian Federation).

In this case, information about the income tax attributable to the OP is reflected in Appendix No. 5 to sheet 02 of the tax return, that is, the procedure for filling out the declaration does not change.

Deadline for filing 3-NDFL upon termination of activity

Upon termination of activity for 3-NDFL, the deadline for submission is determined depending on which category of individuals the taxpayer belongs to. According to the standards contained in paragraph 3 of Art. 229 of the Tax Code of the Russian Federation, it is established as follows:

- within 5 days after the end of the month when this activity was terminated - this is the filing deadline for individual entrepreneurs and private practitioners under 3-NDFL;

Attention! The day of termination of activity is considered to be the date of making the corresponding entry in the Unified State Register of Individual Entrepreneurs, and not the date of filing the application for deregistration (letter of the Federal Tax Service of Russia dated January 13, 2016 No. BS-4-11 / [email protected] ).

- no later than a month before leaving the Russian Federation - this is how 3-NDFL determines the filing deadline for foreign citizens.

What to consider when filling out your income tax return

All companies paying income tax submit a “profitable” declaration at the end of each reporting period and year, which includes:

- title page;

- subsection 1.1 section. 1;

- sheet 02;

- Appendix No. 1 to sheet 02;

- Appendix No. 2 to sheet 02.

In addition, you will have to fill out, in particular:

- subsection 1.2 section. 1 – when paying monthly advance payments within quarters;

- subsection 1.3 section. 1 (with payment type “1”), sheet 03 (with attribute “A”) - when paying dividends to other organizations;

- Appendix No. 3 to sheet 02 - including when selling depreciable property;

- Appendix No. 1 to the declaration - including if there are expenses for voluntary health insurance and employee training.

Line 290 of sheet 02 of the declaration is filled out by organizations paying quarterly advance payments plus monthly advance payments within each quarter.

There they show the total amount of monthly advances due in the next quarter. In this line in the declaration:

- for the first quarter: the indicator of line 180 of sheet 02 of the same declaration is indicated;

- for the half-year: the difference between lines 180 of sheet 02 of the declaration for the half-year and the first quarter, which is greater than 0, is entered, in other cases (less than or equal to 0) a dash is entered;

- for 9 months: the difference between lines 180 of sheet 02 of the declaration for 9 months and half a year is shown, if it is more than 0, in other cases - a dash;

- for the year: put a dash.

Table: “Example of filling out line 290 of sheet 02 of the income tax return”

| Reporting period | Indicator page 180 sheet 02 (rub.) | Indicator page 290 sheet 02 (rub.) |

| For the first quarter | 2 100 000 | 2 100 000 |

| For half a year | 3 800 000 | 1 700 000 |

| In 9 months | Loss received | — |

An organization that pays monthly advance payments during the quarter, in its “profitable” declaration for 9 months, indicates the amount of monthly advances payable in the first quarter of the next year. They must be shown in lines 320-340 of sheet 02 of the declaration. These indicators are equal to the indicators reflected on lines 290-310 of sheet 02 (amounts of monthly advances payable in the fourth quarter of the current year). Thus, a company that received a loss for 9 months of the current year does not pay monthly advance payments during the first quarter of the next year. Non-operating expenses under clause 1 of Art. 265 of the Tax Code of the Russian Federation are reflected on line 200 of Appendix No. 2 to sheet 02. Separately deciphered, including:

- on line 201 - interest on loans and credits issued on securities, including bills of exchange (letter of the Ministry of Finance of the Russian Federation dated April 28, 2016 No. 03-03-06/1/24684);

- on line 204 – expenses for liquidation of OS (other expenses according to clause 8, clause 1, article 265 of the Tax Code of the Russian Federation);

- on line 205 - sanctions under the contract, compensation for damage.

Losses equated to non-operating expenses (clause 2 of Article 265 of the Tax Code of the Russian Federation) are reflected on line 300 of Appendix No. 2 to sheet 02. This will include losses from previous tax periods identified in the current reporting (tax) period, losses from downtime for internal production reasons , losses from natural disasters and other losses received in the reporting (tax) period.

The amount of loss received at the end of the year is reflected in the declaration for the current year:

- on line 060 of sheet 02;

- according to line 160 of Appendix No. 4 to sheet 02.

Please submit your 3rd personal income tax return for 2021 by 12/31/2020

Declarations on transport and land taxes replaced by notifications from the tax authorities about the calculated amount of tax (clauses 17 and 26 of Article 1 of Law No. 63-FZ of April 15, 2019, Order of the Federal Tax Service of September 4, 2019 No. ММВ-7-21/440 ).

So far, there are more questions than answers: how the tax authority will keep records of objects, what reconciliation acts are provided for such settlement accruals, how interdepartmental exchange will be implemented. At the moment, the Federal Tax Service has not given any additional explanations; we can only wait for the implementation of this project.

By the way, no one exempted the organization from paying advance payments. And companies must calculate these advance payments independently. Needless to say, the calculated tax amounts may not agree with the amounts from the notifications, and these discrepancies will have to be justified.

Information on the average number of employees. Data on the number of employees will be included in the calculation of insurance premiums (DAM) from January 1, 2021 (clause 2 of Article 1 of Law No. 5-FZ dated January 28, 2020).

Declaration on UTII . As you know, starting from 2021, UTII will cease to exist. And along with the abolition of the taxation regime, the filing of a declaration is also canceled. The last time UTII payers will have to report by January 20, 2021 is for the fourth quarter of 2021.

Calculation of insurance premiums (DAM)

Federal Law No. 5-FZ dated January 28, 2020 introduced Art. 80 of the Tax Code of the Russian Federation, amendments allowing the submission of information on the average number of employees as part of the DAM (applies to LLCs and individual entrepreneurs with hired employees). To do this, a special field will appear on the title page of the form (Fig. 1).

Combined calculation of 6-NDFL and 2-NDFL certificate

Information on the income of an individual (2-NDFL) is submitted as part of the 6-NDFL calculation.

Data on an individual’s income must be reflected in Appendix 1 to the new 6-NDFL calculation. The application is completed only in the annual report 6-NDFL. Quarterly reports are submitted as before; no one has canceled them. The calculation excludes data on the date of actual receipt of income and tax withholding, but includes fields for the date and amount of refundable personal income tax, excess tax withheld, as well as for information for past periods (Fig. 3).

We are waiting for updated statistical reporting forms regarding wages and employees who rent out LLCs and individual entrepreneurs (Rosstat Order No. 412 dated July 24, 2020).

Already in the first quarter of 2021, it is necessary to submit to Rosstat (quarterly):

In addition to the new barcodes:

- In Section 1, a subsection has appeared for individual entrepreneurs, where BCC, OKTMO, advance payments and tax are indicated;

- A calculation has been added to Appendix 3, where entrepreneurs calculate the advance based on income, professional and standard tax deductions based on the results of the first quarter, half a year, and 9 months;

- In Appendix 4 to Section 2, where non-taxable income is reflected, a new line has appeared. This line indicates financial assistance from the educational organization to students, cadets, etc.;

- An appendix has been added to section 1. This is an application for a refund or offset of the overpayment.

The declaration can be submitted:

- in electronic form;

- on paper (in person or by mail).

The deadline for citizens who are required to submit a declaration (entrepreneurs, property sellers, apartment landlords, etc.) is no later than April 30

the year following the reporting year.

If the declaration is submitted for the purpose of returning tax withheld by the employer, then it can be submitted within three years. For example, in 2021 you can submit returns for 2021, 2021 and 2018.

The legislation establishes that the 3-NDFL tax return must be submitted in the general manner by an individual before April 30. This rule applies to individual entrepreneurs registered with the Federal Tax Service. If such a day falls on a weekend or holiday, the final deadline for submitting the report is postponed to the next nearest business day.

In 2021, individuals and individual entrepreneurs will have to report for 2021 by April 30, 2021 inclusive.

Violation of this deadline is possible only for individuals whose tax agents have calculated and filed taxes for them, and the citizens themselves submit a form to receive deductions.

Attention! If an entrepreneur applying the general taxation system (OSNO) closes an individual entrepreneur and is removed from tax registration, then he must fill out the 3-NDFL form within five working days from the date of deregistration.

Declaration 3-NDFL for 2021, as in previous periods, must be sent to the tax authorities located at the place of permanent residence of the individual, that is, according to registration.

To determine exactly which tax office you need to report to, you can use the service on the website of this authority. In the appropriate fields, the individual must enter his address from the directory, and the site will tell him which institution he should contact.

However, persons who file 3rd personal income tax are not required to submit the 3rd personal income tax report at their address.

How to carry forward losses from previous years

This must be done according to the new rules.

From January 1, 2017 (to December 31, 2020), the procedure for reducing the tax base for losses of previous years has been changed:

- a restriction on such reduction has been introduced: the tax base can be reduced by no more than 50 percent (the restriction does not apply to tax bases to which certain reduced tax rates apply);

- The restriction on the transfer period has been removed (previously it was possible to transfer only within 10 years);

- The new procedure applies to losses received for tax periods starting from January 1, 2007.

Taking into account the innovations, the following line indicators must be filled in the declaration:

1) 110 sheets 02 and 010, 040–130, 150 of Appendix No. 4 thereto: in particular, the amount on line 150 (the amount of loss that reduces the base) cannot be more than 50 percent of the amount on line 140 (tax base);

2) 080 sheet 05;

3) 460, 470, 500, 510 sheet 06: the sum of lines 470 and 510 (the amount of recognized loss) must be less than or equal to 50 percent of the amount on lines 450 and 490 (tax base from investments).

In the tax return for the profit tax of a foreign organization (form approved by Order of the Ministry of Taxes of the Russian Federation dated January 5, 2004 No. BG-3-23/1), the amount of losses that reduce the tax base for the current period is indicated on line F (code 300) of section 5, taking into account application of new provisions.

Letter of the Federal Tax Service of the Russian Federation dated January 09, 2017 No. SD-4-3/ [email protected] “On changing the procedure for accounting for losses of past tax periods”

Editor's note:

The updated procedure for transferring losses is relevant for calculating the tax base for the first quarter of 2021.

When a loss is carried forward by its amount, the profit of the reporting (tax) period is reduced, reflected on line 100 of sheet 02 of the declaration and on line 140 of Appendix No. 4 to sheet 02 of the declaration, which is filled out only in the declaration for the first quarter of the year to which the loss is carried forward, and for this year.

Results

The deadline for submitting Form 3-NDFL for declaring income is set for April 30, following the reporting year. If the deadline falls on a weekend or non-working date, it is shifted to the next closest working day. But for reporting for 2021, this rule does not apply and you must report no later than 04/30/2021, because it's a working day. For late submission of a tax return, the taxpayer will face a fine of at least 1,000 rubles.

When declaring tax for deduction, a specific deadline for filing 3-NDFL is not established by law. But the tax can be returned only for the last 3 years preceding the year of filing the declaration.

Sources:

- Tax Code of the Russian Federation

- Order of the Federal Tax Service dated October 7, 2019 No. ММВ-7-11/ [email protected]

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

How to show insurance premiums in your income tax return

The organization independently determines and establishes the list of direct expenses in its accounting policies. In Appendix No. 2 to sheet 02 of the income tax return, line:

- 041 – only contributions to compulsory health insurance, compulsory medical insurance, VNIiM are reflected from the salaries of administrative and managerial personnel;

- 010 – insurance premiums from the salaries of production workers.

Indirect costs are costs associated with the production and sale of products (works, services), which can be included in expenses in the period in which they are incurred. All costs that are not classified as direct expenses in the accounting policy and are not non-operating expenses are recognized as indirect (letter of the Ministry of Finance of the Russian Federation dated March 13, 2017 No. 03-03-06/1/13785).

In the income tax return, the total amount of indirect expenses is indicated on line 040 of Appendix No. 2 to sheet 02 (clause 7.1 of the Procedure for filling out the income tax return). Such expenses are partially deciphered according to lines 041-055 of Appendix No. 2 to sheet 02.

Line 041 reflects taxes (advance payments for them), fees and insurance premiums taken into account in other expenses (clause 1, clause 1, article 264 of the Tax Code of the Russian Federation, clause 7.1 of the Procedure for filling out the declaration, letter of the Federal Tax Service of the Russian Federation dated 04/11/2017 No. SD -4-3/ [email protected] ). This:

- transport tax;

- property tax (based on both book value and cadastral value);

- land tax;

- restored VAT, which according to the Tax Code is taken into account in other expenses (for example, tax restored when receiving an exemption from VAT under Article 145 of the Tax Code of the Russian Federation (clauses 2, 6, clause 3, Article 170 of the Tax Code of the Russian Federation);

- state duty;

- contributions to compulsory public health insurance;

- compulsory medical insurance contributions;

- contributions to VNiM.

When filling out line 041 of the declaration for the reporting (tax) period, the organization indicates in it the amount of all taxes (advance payments thereon), fees and insurance premiums accrued during this period on an accrual basis, regardless of the date of their payment to the budget (letters from the Ministry of Finance of the Russian Federation dated September 12, 2016 No. 03-03-06/2/53182, dated 09.21.2015 No. 03-03-06/53920).

Please note that line 041 of Appendix No. 2 to sheet 02 of the income tax return is not reflected:

1) taxes (advance payments thereon) and other obligatory payments that cannot be taken into account in tax expenses:

- income tax;

- UTII;

- VAT presented to the buyer (purchaser) of goods (works, services);

- payments for emissions of pollutants in excess of standards;

- trade fee;

2) contributions for injuries.

The amounts of insurance premiums are included when generating the indicator for the specified line, starting with the tax return for the first reporting period of 2021. When drawing up a declaration for 2021, they are not included in this indicator (letter of the Federal Tax Service of the Russian Federation dated 04/11/2017 No. SD-4-3 / [email protected] ).

The entire amount indicated on line 041 is then included in line 040 of Appendix No. 2 to sheet 02 of the declaration (that is, in the total amount of indirect expenses).

Direct costs are costs associated with the production of products (works, services), which can be included in expenses only during the period of sale of products (works, services) (clause 2 of Article 318 of the Tax Code of the Russian Federation).

The organization determines and consolidates the list of direct expenses in its accounting policies independently (letter of the Ministry of Finance of the Russian Federation dated March 13, 2017 No. 03-03-06/1/13785).

According to the recommendations of the Ministry of Finance of the Russian Federation and the Federal Tax Service of the Russian Federation, direct expenses include all costs that form the cost of products (works, services) in accounting (letter of the Ministry of Finance of the Russian Federation dated May 14, 2012 No. 03-03-06/1/247, Federal Tax Service of the Russian Federation dated February 24. 2011 No. KE-4-3/ [email protected] ).

Thus, the composition of direct costs in the production of products (works, services) includes at least the following types of costs (clause 1 of Article 318 of the Tax Code of the Russian Federation):

- raw materials and materials that form the basis of products;

- wages of employees directly involved in production, as well as mandatory insurance contributions accrued on it;

- depreciation accrued on fixed assets directly used in the production of products (works, services).

When producing products (works, services), the total amount of direct expenses that are taken into account for profit tax purposes in the reporting (tax) period is reflected in the income tax return on line 010 of Appendix No. 2 to sheet 02 on an accrual basis from the beginning of the year (clause 2.1, 7.1 Procedure for filling out the declaration).

When reporting all expenses on line 010, the organization must keep in mind that it will have to provide all documentation as evidence of the need for the types of expenses incurred.

Thus, according to the income tax return line:

- 041 – only contributions to compulsory health insurance, compulsory medical insurance, VNIiM are reflected from the salaries of administrative and managerial personnel;

- 010 – insurance premiums from the salaries of production workers.

The indicators of lines 010, 020 and 040 of Appendix No. 2 to Sheet 02 are included in the indicator of Line 130 of Appendix No. 2 to Sheet 02, which reflects the expenses recognized by the organization for profit tax purposes. The value of line 130 of Appendix No. 2 to sheet 02 is transferred to line 030 of sheet 02 of the tax return (clause 5.2 of the Procedure for filling out the income tax return).

How to show symmetrical adjustments in the declaration

When reflecting symmetrical adjustments in Sheet 08 of the declaration (provided that the code “2” or “3” is indicated in the “Type of adjustment” attribute):

- in column 3 “Attribute” the number “0” is entered if the adjustments made led to a decrease in sales income (line 010 of Sheet 08)/non-operating income (line 020 of Sheet 08);

- in column 3 “Attribute” the number “1” is entered if the adjustments made led to an increase in expenses that reduce the amount of sales income (line 030 of Sheet 08)/non-operating expenses (line 040).

In this case, in Sheet 08 you do not need to enter “0” or “1” in column 3 “Sign” on line 050. On this line you should indicate the total amount of the adjustment without taking into account the sign.

Letter of the Federal Tax Service of the Russian Federation dated October 24, 2017 No. SD-4-3/ [email protected]

How to adjust profits if a transaction is invalid

In 2015, the bank made a real estate sale transaction, which the court later declared invalid. Due to the recognition of the transaction as invalid in accordance with clause 2 of Art. 167 of the Civil Code of the Russian Federation, the bank was obliged to reimburse the buyer for everything he paid. Consequently, the bank lost profit from the transaction.

The bank submitted an update on its profits for 2015. Since Article 81 of the Tax Code gives the right to submit adjusted reports if errors were made in the declaration, which led to an overpayment of tax to the budget.

According to the Federal Tax Service of the Russian Federation, in this case the bank acted lawfully.

Letter of the Federal Tax Service of the Russian Federation dated November 28, 2017 No. SD-4-3/ [email protected]

How to include separate income and expenses in the “profitable” base

The Ministry of Finance of the Russian Federation has published a number of letters explaining the tax accounting procedure for certain income and expenses.

Work records

When purchasing work books, their cost is taken into account in tax and accounting expenses (letter of the Federal Tax Service of the Russian Federation dated June 23, 2015 No. GD-4-3 / [email protected] ).

Income not taken into account when determining the tax base is defined in Art. 251 Tax Code of the Russian Federation. The list of such income is exhaustive. The fee charged to the employee for the provision of work books or inserts is not mentioned in this article. This means that the indicated income is subject to income tax in the generally established manner (letter of the Ministry of Finance of the Russian Federation dated May 19, 2017 No. 03-03-06/1/30818). The amount received from the employee to reimburse the cost of the work book must be taken into account for tax purposes in non-operating income (letter of the Ministry of Finance of the Russian Federation dated May 19, 2017 No. 03-03-06/1/30818).

Salary

The list of labor costs is unlimited

To be recognized for profit tax purposes, expenses must be economically justified, documented, and incurred for activities aimed at generating income. Expenses that do not meet these requirements are not taken into account.

According to Art. 255 of the Tax Code of the Russian Federation, labor costs include any accruals to employees provided for by the legislation of the Russian Federation, labor and (or) collective agreements.

The list of labor costs is open. These, according to paragraph 25 of this article, also include other types of expenses in favor of the employee, provided that they are provided for by the labor and (or) collective agreement.

Therefore, any types of labor costs incurred on the basis of local regulations of the organization can be recognized, subject to compliance with the criteria specified in paragraph 1 of Art. 252 of the Tax Code of the Russian Federation, and provided that such expenses are not specified in Art. 270 of the Tax Code of the Russian Federation (letter of the Ministry of Finance of the Russian Federation dated May 19, 2017 No. 03-03-06/1/30842).

Awards

Bonuses for production results are included in labor costs (clause 2 of Article 255 of the Tax Code of the Russian Federation).

At the same time, as follows from Art. 129 of the Labor Code of the Russian Federation, incentive payments are elements of the remuneration system in an organization, which are established by collective agreements, agreements, and local regulations of the company.

The employer has the right to encourage employees who conscientiously perform their job duties: express gratitude, give a bonus, award a valuable gift, a certificate of honor, nominate them for the title of the best in the profession (Article 191 of the Labor Code of the Russian Federation). Other types of employee incentives for work are determined by a collective agreement or internal labor regulations, as well as charters and discipline regulations.

However, for accounting for such expenses, the restrictions established by Art. 270 Tax Code of the Russian Federation. Thus, remunerations paid to management or employees and not specified in employment contracts, as well as bonuses paid from the company’s net profit, are not taken into account when determining the profit base.

Therefore, bonuses to employees can be taken into account in expenses if the procedure, amount and conditions of payment are provided for by the local regulations of the organization, and are not specified in Art. 270 of the Tax Code of the Russian Federation (letter of the Ministry of Finance of the Russian Federation dated April 17, 2017 No. 03-03-06/2/22717).

Bonuses paid on holidays are not recognized as expenses, since they are not related to the production results of employees (letters of the Ministry of Finance of the Russian Federation dated 07/09/2014 No. 03-03-06/1/33167, dated 04/24/2013 No. 03-03-06/ 1/14283, dated 03/15/2013 No. 03-03-10/7999).

Sport

For income tax purposes, expenses that are economically justified and documented are taken into account. An exception is the expenses listed in Art. 270 Tax Code of the Russian Federation.

If events aimed at developing physical culture and sports in work collectives are carried out outside working hours and are not related to the production activities of employees, these expenses are not taken into account in the tax base (letter of the Ministry of Finance of the Russian Federation dated July 17, 2017 No. 03-03-06/1 /45234).

Foreign taxes

Any expenses are recognized as expenses if they are justified, documented and incurred for activities aimed at generating income.

Article 264 of the Tax Code of the Russian Federation establishes an open list of other expenses. It expressly states only taxes and fees assessed in accordance with Russian legislation. But it is possible to take into account other costs associated with production and sales.

In addition, the list of expenses not taken into account for profit tax purposes is closed and does not include taxes paid on the territory of a foreign state.

Thus, taxes and fees paid in another country can be written off among other expenses in accordance with paragraphs. 49 clause 1 art. 264 of the Tax Code of the Russian Federation (letter of the Ministry of Finance of the Russian Federation dated February 10, 2017 No. 03-03-06/1/7449).

This does not take into account foreign taxes, for which the Tax Code of the Russian Federation directly provides for the procedure for eliminating double taxation by offsetting them when paying the corresponding tax in Russia. For example, this procedure is defined in relation to income tax and property tax of organizations (Articles 311 and 386.1 of the Tax Code of the Russian Federation).

What is the penalty for being late in reporting and paying taxes?

For failure to submit (late filing) a “profitable” declaration, the following sanctions are established:

1) for late submission of annual reporting, a fine is imposed in the amount of 5 percent of the amount of tax not paid on time, subject to payment under this declaration, for each full or partial month that has passed from the day established for submitting the declaration until the day on which it was submitted presented. In this case, there cannot be a fine (clause 1 of Article 119 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of the Russian Federation dated August 14, 2015 No. 03-02-08/47033):

- more than 30 percent of the unpaid tax amount due on a late declaration;

- less than 1,000 rubles (the same fine will be for late submission of a “zero” declaration).

2) for being late with a declaration for the reporting period (Q1, half-year, 9 months or one month, two months, etc.) you will be fined 200 rubles for each declaration not submitted on time (clause 1 of Article 126 of the Tax Code of the Russian Federation, letter of the Federal Tax Service of the Russian Federation dated August 22, 2014 No. SA-4-7/16692);

3) a company official may be fined in the amount of 300 to 500 rubles (Article 15.5 of the Code of Administrative Offenses of the Russian Federation).

As a general rule, the official is the head of the organization, but it can also be another employee (for example, a chief accountant), who, by virtue of an employment contract or internal regulation, is responsible for submitting tax reports to the Federal Tax Service;

If you are late with your annual declaration within 10 days, your company account may also be blocked. However, such a measure does not apply if the advance payment is submitted late (Determination of the Armed Forces of the Russian Federation dated March 27, 2017 No. 305-KG16-16245, letter of the Federal Tax Service of the Russian Federation dated April 17, 2017 No. SA-4-7 / [email protected] ). Therefore, the Federal Tax Service does not have the right to block an account if the deadline for submitting reports for 9 months is violated.

Penalties are charged for missed deadlines for payment of advance payments and income tax.

If non-payment of tax occurred due to an error that led to an underestimation of the tax base for profits, then in this case the organization faces a fine in the amount of 20 percent of the amount of arrears (clause 1 of Article 122 of the Tax Code of the Russian Federation):

To avoid this fine, you need to submit a “clarification”, but before that you need to pay the arrears and penalties (clause 4 of Article 81 of the Tax Code of the Russian Federation, letters of the Ministry of Finance of the Russian Federation dated September 13, 2016 No. 03-02-07/1/53498, Federal Tax Service of the Russian Federation dated 11/14/2016 No. ED-4-15/ [email protected] ).

Deadline for filing 3-NDFL for tax deductions

If you need to receive social or property tax deductions not at work, but through the Federal Tax Service, fill out 3-NDFL and submit it at the end of the calendar year. When is the 3-NDFL declaration submitted in this case? The deadline until April 30 does not apply. That is, you can submit a return just to receive a deduction at any time throughout the year. In this situation, there is no need to focus on the deadline for submitting the 3-NDFL declaration.

The statute of limitations for filing a 3-NDFL declaration when applying for tax deductions is not established by law. But only 3 years are allotted for filing an application for a tax refund, counted from the moment this payment is made (clause 7 of Article 78 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated November 17, 2011 No. 03-02-08/118).

Please note that if you declare in 3-NDFL both income subject to declaration and the right to tax deductions, then you are required to submit such a declaration no later than April 30.

For example, when selling property owned for less than 5 (and in certain situations - 3) years, you need to report before April 30 of the year following the year of sale (clause 1 of Article 229 of the Tax Code of the Russian Federation). Therefore, if you decide to reduce the income from the sale of housing by expenses associated with its acquisition, and at the same time apply to it the deduction provided for the purchase of housing, then the declaration must be submitted no later than April 30.

How to fill out the 3-NDFL declaration when selling and buying apartments during the year? The answer to this question is in ConsultantPlus. To do everything correctly, get trial access to the system and go to the material. It's free.

Read more about the impact of the period of ownership of property on the taxation of income from its sale in the material “Sale of real estate below cadastral value - tax consequences.”

How to submit a “clarification”

An updated declaration must be submitted in two cases:

- if the company discovered an error in a previously submitted declaration that led to incomplete payment of tax - when expenses were overstated or income was understated (clause 1 of Article 81 of the Tax Code of the Russian Federation, letter of the Federal Tax Service dated November 14, 2016 No. ED-4-15 / [email protected] ) ;

- upon receiving from the Federal Tax Service a request to provide explanations on the declaration or make corrections to it (clause 3 of Article 88 of the Tax Code of the Russian Federation). If, in the opinion of the company, the declaration is filled out correctly, then instead of “clarification” it is necessary to provide explanations.

An error that led to an overpayment of tax can be corrected in the declaration for the current period.

The “update” is submitted in the same form as the initial declaration. It must be submitted to the Federal Tax Service with which the organization is registered on the day the “clarification” is submitted.

In the updated declaration, all sheets, sections and appendices that were filled out in the primary declaration are filled out, even if there were no errors in them (letter of the Federal Tax Service of the Russian Federation dated June 25, 2015 No. GD-4-3 / [email protected] ).

An updated declaration at the request of the inspectorate when errors are identified during the “camera room” must be submitted to the Federal Tax Service within 5 working days from the date of receipt of the request. If you fail to meet this deadline and do not submit an explanation, the organization will be fined 5 thousand rubles under clause 1 of Art. 129.1 Tax Code of the Russian Federation. For a repeated violation within a calendar year, the fine will be 20 thousand rubles (Clause 1 of Article 129.1 of the Tax Code of the Russian Federation).

The Tax Code of the Russian Federation has not established any other deadlines for filing a “clarification”. However, it's better to hurry up. After all, if the tax payable is underestimated and the inspection is the first to discover this fact, then the company will be fined (20 percent of the amount of arrears, clause 1 of Article 122 of the Tax Code of the Russian Federation).

When last year's mistakes can be corrected in the current period

By virtue of paragraph 1 of Art. 54 of the Tax Code of the Russian Federation, errors or distortions in the calculation of the tax base for past periods discovered in the current period can be corrected during the period of their discovery in two cases:

- if the period of the error is unknown;

- if the error resulted in overpayment of tax.

Thus, this norm is applied when there are distortions in the base for the previous period, for example, when expenses are understated when receiving (discovering) last year’s “primary” from a counterparty in the current period.

However, you will still have to adjust the period of the error if a loss was incurred in the reporting period.

The financiers also recalled the norm of clause 7 of Art. 78 of the Tax Code of the Russian Federation: an application for offset (refund) of the amount of overpaid tax, including due to recalculation of the tax base, can be submitted within 3 years from the date of payment of the specified amount.

Letter of the Ministry of Finance of the Russian Federation dated 08/04/2017 No. 03-03-06/2/50113

Editor's note:

The tax payment day is considered the day of presentation to the bank of a payment order for its payment from an account in which there is enough money for payment (clause 1, clause 3, article 45 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of the Russian Federation dated June 27, 2016 No. 03-03-06/1 /37152).

Registration procedure

The declaration for property deduction must be completed accordingly. It is necessary not only to correctly fill out the 3-NDFL form itself, but also to prepare other documents (originals and copies), the presence of which is a prerequisite for receiving a deduction (2-NDFL certificate, documents confirming the fact of acquisition of property, an application for a refund of overpaid tax and etc)

These documents are needed to fill out the declaration, since the indicator values are taken from them. It’s easier and faster to enter the necessary data using special free programs located on the official website of the Federal Tax Service. The program itself will determine which sheets and lines need to be filled in and check that they are filled out correctly. You can take the necessary sheets from the Federal Tax Service and fill out the declaration manually.

When completing the declaration, you must ensure that the form you are using is up to date. Form 3-NDFL, approved in 2014, changes periodically. Thus, form 3-NDFL for income received in 2017 differs from form 3-NDFL for income for 2021, and this must be taken into account when filling it out in order to avoid refusal to accept documents.

Other reasons for refusal to accept a declaration may be:

- lack of documents confirming the payer’s identity

- lack of documents confirming the authority of the representative;

- filing documents with the wrong tax authority.

So, in order to receive a property deduction, you must submit a correctly completed declaration with supporting documents attached:

- copies of the real estate purchase agreement;

- payment documents confirming the fact of payment of funds;

- copies of the loan agreement and a certificate from the bank about the amount of interest paid on the loan;

- certificates in form 2-NDFL, etc.

In some cases, other documents, such as a marriage certificate, may be required when purchasing jointly owned property. Documents for declaration (except for income certificates) are submitted once upon the first application for deduction.

To receive a property deduction, all taxpayers need to know how to fill out a declaration.