Form 6-NDFL for the 4th quarter of 2021 was approved by order issued by the Federal Tax Service on October 14, 2015 under No. ММВ-7-11/ [email protected] taking into account changes dated January 17, 2018. The document is divided into 3 blocks:

- information about the tax agent - enterprise, individual entrepreneur submitting the report (data is entered on the title page);

- Section 1 is devoted to cumulative indicators for the period from the beginning of the year (in this case, for the year), accruals for the last reporting month are also included in it, payment for which will be made in the next reporting interval;

- section 2, reflecting data for each month of the last quarter.

The reporting form provides for the reflection of the dates of accrual and payment of income. Wages are calculated on the last day of each month (for the purposes of reporting, it does not matter whether it is a day off or a work day), and it is issued upon the fact on the same day or the next month (Clause 2 of Article 223 of the Tax Code of the Russian Federation). The employer can pay personal income tax on the day of payment of wages to the staff or on the next working day (clause 6 of Article 226 of the Tax Code of the Russian Federation).

We rent out 6-NFDL for the 4th quarter of 2021

In form 6-NDFL, companies and individual entrepreneurs indicate the income paid to individuals during the year on an accrual basis.

The procedure for filling out 6-NDFL provides for the reflection of three dates and the corresponding amounts:

- the date when the income was accrued - the final day of the month;

- the date when the income was paid is established by the employer taking into account Art. 223 Tax Code of the Russian Federation;

- the date when the tax was withheld from the income - the day following the payment (clause 6 of Article 226 of the Tax Code of the Russian Federation).

The specificity of 6-NDFL for the 4th quarter of 2021 lies in the reflection of the payment of earnings for December.

If an individual received earnings in December 2021 on the 29th, then December accruals are indicated in the first section of 6-NDFL for the year, but will not be included in the second section of the report. This is due to the fact that the tax payment date is the first working day in January, that is, the next reporting period. Therefore, income for December goes into the second section of 6-NDFL, presented in 2021 for the 1st quarter.

If income is paid on December 28, 2021, the tax is transferred until December 29, so information about the payment is indicated in both sections of 6-NDFL for 2021.

Payment of December assessments in 2021, in January, in form 6-NDFL for 2021 will be reflected only in the form of accrued tax, the withheld tax will appear in the first tax report for 2021, and in the annual 6-NDFL in line 070 of section 1 and 2 section will not be indicated.

For 2021, the deadline for filing 6-NDFL is April 1, 2021. For the current 6-NDFL report form for 2021, see the Federal Tax Service website.

6-NDFL is submitted to the tax service based on the results of the reporting quarter 4 times a year within the deadline prescribed in the Tax Code of the Russian Federation.

dekabr.jpg

Option two

How to file 6-NDFL (4th quarter), if the payment of December income was made in January of the following year:

- the title page and section 2 will be identical to the version from the previous example;

- when filling out section 1, data on the December earnings of hired personnel will be included in lines 020 and 040 (accrued income and tax), but will not be reflected in column 070, since the payment was made in the next reporting interval, which means that the December tax is not in fact withheld in 2021.

Payment of December salaries in January 2021 assumes that the December breakdown will be included in the report for the 1st quarter of 2019 in section 2 in the following form:

- line 100 – 12/31/2018;

- line 110 – 01/09/2019 (date of salary payment);

- line 120 – 01/10/2019 (deadline for repayment of obligations to the budget).

All deadlines for filing 6-NDFL for 2021

According to Art. 230 of the Tax Code of the Russian Federation, the deadline for filing 6-NDFL is the last day in the month following the reporting quarter. Taking into account weekends and holidays, these dates in 2021 fall on the following days:

- April 1 - annual 6-personal income tax for 2021;

- April 30 — report on the 1st quarter;

- July 31—half-year report;

- October 31 – 9 month report.

Report 6-NDFL via the Internet

Kontur.Extern will help you fill out the form, check for errors and submit it to the tax office.

Send a request

Procedure for filling out the report

The rules for filling out 6-NDFL are prescribed in the Order of the Federal Tax Service dated October 14, 2015 No. ММВ-7-11/ [email protected] According to that order, the report form is divided into two sections.

The first section includes lines 010 to 090, which indicate:

- 010 — tax rate;

- 020 - income accrued to individuals during the year on an accrual basis;

- 025 - income in the form of dividends accrued to individuals during the year on an accrual basis;

- 030 - tax deductions that reduce taxable income during the year;

- 040 - tax accrued on the income of individuals during the year on an accrual basis;

- 045 - tax accrued on the income of individuals in the form of dividends during the year on an accrual basis;

- 050 - advance payments that reduce accrued tax during the year;

- 060 - number of individuals whose income is subject to personal income tax;

- 070 - tax withheld from individuals during the year on an accrual basis;

- 080 - tax that was not withheld from individuals during the year, also on an accrual basis;

- 090 - tax, which, according to Art. 231 of the Tax Code of the Russian Federation, the tax agent returned it to taxpayers.

In the second section, the information is indicated not on an accrual basis, but for a specific reporting period. In the second section, lines 100 - 150 are indicated for completion:

- 100 - the date when the income entered in line 130 was received;

- 110 - the date when tax was withheld from income on line 130;

- 120 – final day for tax transfer;

- 130 - the amount of income on line 100 as of the specified date;

- 150 - the amount of tax withheld as of the date on line 110.

Note that line 130 indicates income in full, excluding deductions and taxes. Reflecting income minus deductions and taxes entails a fine of 500 rubles. for submitting false information.

How to fill out the calculation for 2021?

Report 6-NDFL is filled out generally for all employees of the organization in respect of whom the organization or individual entrepreneur acts as a tax agent for personal income tax.

The data is provided on the basis of tax registers on a cumulative basis from the beginning of the year - for three, six, nine and twelve months.

Based on the results of 2021, Form 6-NDFL must be submitted to the Federal Tax Service by March 1, 2021 inclusive. In the calculation, information for the calendar year should be provided in the first section, as well as data for the last 4th quarter (October, November, December) in the second section.

Composition of form 6-NDFL:

- title page;

- section 1;

- section 2.

The procedure for filling out this report can be found here.

General filling requirements:

- mandatory absence of errors and corrections;

- the presence of a page number on each completed sheet;

- the presence of a signature and date on each completed page;

- one-sided document printing;

- the organization and separate divisions submit settlements at their location;

- Individual entrepreneurs are rented out at their place of residence.

Title page

The first page of the 6-NDFL calculation is the title page, which contains general information about the tax agent submitting the report.

You need to fill in the following fields:

- TIN/KPP - the details of the tax agent are written down at the top of the page, for individual entrepreneurs only the TIN;

- correction number - 00 for the first submission, for clarification and change - correction number, starting from 01;

- submission period - 34 for submission per calendar year;

- tax period - year 2020;

- tax authority - code of the Federal Tax Service branch where the calculation is submitted;

- by location - code from Appendix 2 to the Procedure for filling out 6-NDFL - 214 for organizations submitting payments at their location; 120 - at the place of residence of the individual entrepreneur;

- tax agent - full name of the legal entity or full name of the entrepreneur;

- form of reorganization, liquidation, TIN/KPP of the reorganized organization - filled out only when carrying out the specified activities;

- OKTMO - code of the territorial location of the tax agent;

- telephone - contact number;

- reliability - the report can be signed by the director (the individual entrepreneur himself), in this case, put 1, signature of the director (or individual entrepreneur), date; a representative can sign, in this case the number 2 is entered, the full name of the authorized person, details of the power of attorney and the signature of the representative are written.

An example of filling out the title page of 6-NDFL for the 4th quarter of 2021:

Section 1

The first section of Form 6-NDFL provides summarized data for all employees for the calendar year (from January to December 2020).

Line by line filling:

- 010 - tax rate, in relation to the salaries of residents of the Russian Federation it is 13%;

- 020 - taxable income accrued for the year for all employees, the accrual date of which fell within the period from 01.01.2020 to 31.12.2020 (before tax, excluding dividends);

- 025 - accrued dividends, if the tax agent accrued them to one of the employees in 2021;

- 030 - deductions provided to employees for the calendar year 2020 (standard, social, property);

- 040 - calculated tax on income from line 020, taking into account deductions = line 010 * (line 020 - line 030);

- 045 - tax calculated on dividends from line 025 = line 010 * line 025;

- 050 - the field is filled in in relation to foreign employees on a patent - indicates the amount of advances for 2021 paid by such employees on their own;

- 060 - the number of employees in respect of whom the organization (or individual entrepreneur) acted as a tax agent;

- 070 - actual tax withheld (it is important to remember that personal income tax is withheld when paying income to an employee);

- 080 - tax not withheld for 2021 due to various reasons;

- 090 - refunded tax for 2021 in accordance with clause 231 of the Tax Code of the Russian Federation.

Income from January 2021 and 2020

Lines 040 and 070 - the first indicates the calculated personal income tax, the second the withheld. Indicators may differ due to different calculation and deduction dates.

When filling out the calculation for 2021, the payroll tax for December 2021 is calculated in December 2021, and is usually withheld already in January 2021 when paying salaries, which means that this personal income tax is not included in line 040 and is included in line 070.

Similarly, the tax for December 2021 is calculated in December, and is withheld in January 2021 when paying salaries to employees. This means that this tax will be included in line 040 and will not be included in line 070.

Conclusion: when filling out 6-NDFL for 2021, line 040 will include personal income tax calculated from income accrued from January to December 2021, line 070 will include personal income tax withheld from income paid from January to December 2020.

An example of filling out section 1 6-NDFL for 2020:

Section 2

The second section of 6-NDFL, filled out for 2021, reflects data for the 4th quarter (for October, November, December 2020).

It is important to indicate correctly here:

- date of actual receipt of income - for wages and monthly bonuses - the last day of the month; for one-time, annual, quarterly bonuses, vacation pay, sick leave, financial assistance, dividends, payments under GPC agreements - the day of actual issue to the employee;

- tax withholding date - the day when income is actually issued to employees;

- tax payment date - coincides with the day of withholding or the next day.

In this way, income in the form of wages and monthly bonuses, for which there is a single date of actual receipt, is separately grouped, and all other payments are grouped separately.

Salary for September 2020

Here it is important to pay attention to wages for September 2020 - despite the fact that the date of actual receipt for it falls on September 30, 2020 (that is, does not fall into the 4th quarter), it still needs to be included in the calculation for the year as the first line, since the tax on it will already be withheld and paid in the 4th quarter.

Salary for December 2020

As for the salary for December 2021, the date of its actual receipt is December 31, 2020 (that is, included in the 4th quarter), but the tax will be withheld and transferred in January 2021, which means this income does not need to be included in the calculation for the year.

For the 4th quarter of 2021, section 2 of form 6-NDFL is filled out as follows:

How to reflect alimony in 6-NDFL

Alimony is one of the types of deductions that raise questions when filling out 6-NDFL.

The issue of correctly reflecting alimony in form 6-NDFL concerns lines 020 and 130. According to the rules for filling out the report, line 020 records the income accrued to an individual in full from the beginning of the year, and line 130 records the taxpayer’s income for the reporting period without tax withholding or deductions provided.

Article 210 of the Tax Code of the Russian Federation establishes that alimony does not reduce the income tax base. The tax is withheld from the individual's full income, and after the tax is withheld, the amount of alimony is determined, and the employee receives the payment minus personal income tax and alimony.

Thus, in fact, alimony does not affect the income accrued to an individual, and therefore is not reflected in 6-NDFL.

Example of filling out form 6-NDFL

Form 6-NDFL includes two sheets: a title page and a sheet with income and tax indicators, divided into two sections. We'll tell you how to fill out 6-personal income tax line by line below.

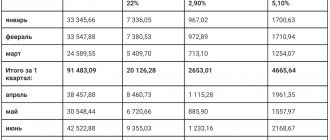

Example. 7 employees who received monthly salaries during the 4th quarter of 2018 in the total amount of 245 thousand rubles, including the salary of M.S. Konyukhova - 37 thousand rubles, of which child support is withheld - 25%. Application for deduction of M.S. Konyukhov did not write. In December 2021, employees of Zolottse LLC received their salaries on the 29th.

Before reflecting the listed transactions in the annual form 6-NDFL, we will fill out the title page, which contains mandatory information about the company.

Let's fill out section 1 of the report:

020 - income accrued to individuals for the full year 2021 - 2,940 thousand rubles. Salaries are accrued on the last day of the month, therefore December accruals are also taken into account in this indicator;

025 - dividends were not accrued in the tax period, so we put a dash in the line;

030 - M.S. Konyukhov did not write an application for a child deduction; other employees were also not provided with tax deductions, therefore, in line 030 6-NDFL, as well as in the annual certificate 2-NDFL under code 126 for M.S. Konyukhov, dashes are added;

040 - income tax calculated for 2021, taking into account wages for December - 382.2 thousand rubles;

045 - dividends were not accrued, which means there is nothing to withhold tax from, put a dash;

050 - no advance payment was made - dash;

060 - the number of individuals to whom Zolottse LLC accrued income during the year - 7 people;

070 - tax amount withheld for the year. Tax on December wages is included in this figure because the income was paid in December;

080 - the tax agent withheld the tax in full, put a dash;

090 - the company did not return tax during the tax period - dash.

A completed sample of the first section of 6-NDFL is presented below.

Next, we will consider the procedure for filling out section 2 of the form.

The amounts indicated here are only for the reporting period, in our case - for the last quarter of 2021. The December salary was issued on the last working day of the month, and the payment of income tax falls on 01/09/2019. Therefore, December accruals in the second section of 6-NDFL based on the results of 2021 will not be reflected, but will appear in the first personal income tax report in 2021. Since for September - November 2021 the amounts of accruals were equal, the same amounts will be reflected in lines 130 - 140.

In 2021, in the last reporting period, M.S. Konyukhov was kept in alimony payments. However, such deductions do not reduce the personal income tax base, so the second section of the first 6-personal income tax in 2021 will reflect the entire amount accrued to employees for December 2018:

You must submit 6-NDFL for the year by 04/01/2019. Companies with up to 25 employees, like Zolotse LLC, are allowed to submit a report in paper form.

New form of Calculation 6-NDFL in 2021

Publication date: 01/13/2021 10:48

The Federal Tax Service of Russia for the Republic of Adygea (hereinafter referred to as the Office) brings to the attention of taxpayers who are tax agents in connection with payments of income to individuals that by Order of the Federal Tax Service of Russia dated October 15, 2020 No. ED-7-11/ [email protected] a new form for calculating amounts has been approved personal income tax calculated and withheld by the tax agent, Form 6-NDFL, the procedure for filling it out and submitting it, as well as the format for presenting the Calculation.

Attention! The 6-NDFL calculation for 2021 will be submitted using the old form, and for reporting for the first quarter of 2021, you need to submit the 6-NDFL calculation using the new form.

When submitting the annual Calculation 6-NDFL for 2021, you will need to submit a certificate of income and tax amounts of an individual (now it is 2-NDFL). In the appendix to the order approved by the Federal Tax Service, there is also a form of income certificate that is issued to employees.

The new 6-NDFL calculation consists of:

- from the title page;

— Section 1 “Data on the obligations of the tax agent”;

— Section 2 “Calculation of calculated, withheld and transferred personal income tax amounts”;

— Appendix No. 1 “Certificate of income and tax amounts of an individual.”

The names of the fields on the title page have been changed:

— “Reporting period (code)” - instead of “Presentation period (code)”;

- “Calendar year” - instead of “Tax period (year)”.

In the field that reflects the code of the reorganization or liquidation form, you will need to indicate the code for deprivation of authority or closure of a separate division. For this case the code is set to 9.

The Department draws the attention of taxpayers that in the new Calculation 6-NDFL, sections 1 and have swapped places: in section 1 it will be necessary to reflect information about the timing of personal income tax transfers and the amount of tax, and in section 2 - generalized information. We ask taxpayers to be careful when filling out the Calculation, since there are often cases when, instead of the number of individuals who received income, the amount of accrued income is indicated, which leads to distortion of the information specified in the report and may lead to penalties.

The innovations include the following:

— in both sections you need to reflect the BCC (field 010 of section 1 and field 105 of section 2);

— in general indicators it is necessary to indicate the amount of income accrued under employment contracts (field 112) and under the GPA (field 113), as well as the amount of tax withheld in excess (field 180);

- in section 1 they reflect only the deadline for transferring the tax and its amount (fields 021 and 022), but the date of actual receipt of income, the date of tax withholding and the amount of income actually received is not necessary;

— separate fields in section 1 are provided to reflect personal income tax amounts returned in the last 3 months of the reporting period, broken down by return date.

In conclusion, we remind you of the deadlines for submitting Calculation 6-NDFL:

03/01/2021 – deadline for submitting the annual Calculation 6-NDFL for 2020. (submitted using the old form);

04/30/2021 - deadline for submitting Calculation 6-NDFL for the 1st quarter of 2021. (submitted in a new form);

07/30/2021 - deadline for submitting Calculation 6-NDFL for the 1st half of 2021;

01.11.2021 - deadline for submitting Calculation 6-NDFL for 9 months of 2021.

(30.10 – day off); 03/01/2022 - deadline for submitting Calculation 6-NDFL for 2021. (submitted together with Appendix No. 1 “Certificate of income and tax amounts of an individual”).