Starting from 2021, UTII has been abolished; this regime can no longer be used. There is a profitable alternative for individual entrepreneurs - the patent taxation system. For LLCs, the simplified tax system remains - we also wrote a lot about this system in the reference book.

This article remains for history only.

To work for UTII, submit an application to the tax office. Not all types of businesses can be transferred to this taxation system - read the UTII article about this: who can apply and how much to pay.

The deadline for submitting an application for UTII is 5 working days from the start of the activity that you are transferring to this taxation system.

Retail

52.21. Retail trade in vegetables and fruits 52.22. Retail trade in meat products, canned meat, meat 52.23. Retail trade in seafood, fish 52.24. Retail trade in bakery products, bread, confectionery 52.25. Retail trade of alcohol and other beverages 52.26. Retail trade in tobacco 52.27.11. Retail trade in milk and milk products 52.27.12. Retail trade in eggs 52.27.2. Retail trade in oils and fats 52.27.3. Retail trade of cereals, canned vegetables, sugar, salt, tea, pasta 52.33. Retail trade in cosmetics and perfumes 50.30. Trade in automobile spare parts 50.40.2. Retail trade in spare parts for motorcycles 50.50. Retail trade in oils 52.41. Retail trade of textile and haberdashery goods 52.44.4. Retail trade of fabrics and tulle 52.42. Retail trade in clothing 52.43. Retail trade of footwear and leather goods 52.44. Retail trade of furniture and household goods 52.48.1. Retail trade of office furniture and office equipment 52.48.11. Retail trade of office furniture 52.48.31. Retail trade in household chemicals, synthetic detergents, wallpaper 52.48.32. Retail trade in flowers, seeds, fertilizers 52.48.33. Retail trade of pets and food 52.46. Retail trade in hardware, paint and varnish materials and glazing materials 52.48.12. Retail trade of office machines and equipment 52.48.13. Retail trade in computers, software and peripheral devices 52.45.4. Retail trade in technical media 52.44.6. Retail trade of household appliances 52.45. Retail trade in household electrical goods, video-audio equipment, television equipment 52.48.14. Retail trade in cameras and other precision devices 52.48.15. Retail trade in telecommunication equipment 52.47.1. Retail trade in books 52.47.2. Retail trade of printed materials 52.47.3. Retail trade in notebooks and stationery 52.46.5. Retail trade of sanitary equipment

Features of “imputation”

According to the Tax Code of the Russian Federation, the types of activities for UTII for 2021 are listed in paragraph 2 of Article 346.26 of the Tax Code of the Russian Federation. Moreover, this norm provides a complete list of types of activities with UTII. There cannot be others. Moreover, this list is gradually being reduced every year. And from 2021 there will be no more types of activities falling under UTII. Because this special regime will be cancelled. For more information, see “When will UTII be cancelled: from 2021 or later?”

It must be said that the Tax Code of the Russian Federation does not separate the types of activities on UTII for an LLC in 2021 and the types of activities on UTII for individual entrepreneurs in 2021. The law provides a general list.

Please note that no types of activities in Moscow are subject to UTII in 2021. In the capital, this special regime has not been in effect for a long time. It is partly replaced by a trading fee.

Prohibited activities

Let's now touch on the issue of restrictions for UTII payers:

- Only certain categories of persons can pay tax (the list of professions is presented above). It is prohibited to engage in other types of work;

- the total staff should be no more than 100 people;

- the maximum amount of authorized capital owned by other persons should be no more than 25%;

- It should also be remembered that this regime is prohibited from being used in a number of territories of the constituent entities of the Russian Federation. Today, “imputation” is not applied only in Moscow, but over time, many other cities and municipalities may abandon this tax (it is expected that by 2021 it will be completely abolished in all constituent entities of the Russian Federation).

New form of declaration for UTII

In 2021, legal entities and individual entrepreneurs on UTII will submit tax returns using a new form. Federal Tax Service amendments to the UTII declaration form and the procedure for filling it out by order No. ММВ-7-3/574 dated 10/19/2016. For the first time, an updated declaration must be submitted for the 1st quarter of 2017 (no later than April 20). See “Deadline for submitting the UTII declaration in 2021: table.”

New declaration on UTII: amendments

Changes in the UTII declaration from 2021 apply to individual entrepreneurs with employees. In the new “imputed” declaration, it will be necessary to show differently the calculation of the amount of single tax payable. Not only contributions for employees, but also fixed contributions “for yourself” will need to be deducted from the tax. That is, the change in the declaration is associated with amendments to the legislation. Also in the new version of the UTII declaration from 2021 there are the following changes:

- in Section 3 of Appendix No. 1, the field barcodes have changed;

- in table 4.14 of Appendix No. 2, the name of the element “The amount of insurance contributions paid by an individual entrepreneur to the Pension Fund of the Russian Federation and the Federal Compulsory Medical Insurance Fund in a fixed amount” changed to the wording “The amount of insurance contributions paid by an individual entrepreneur in a fixed amount for compulsory pension insurance and for compulsory health insurance";

- in Appendix No. 3, the names of the lines and the calculation procedure have been changed (items have been added regarding insurance payments for individual entrepreneurs who do not make payments and other remuneration to individuals).

Not all household services

It must be said that such types of “imputed” activities as household services represent a very large set of occupations and business activities. Therefore, local authorities for this category of services usually specify what types of activities UTII applies to. It can be:

- list of groups of household services;

- list of subgroups;

- certain types of services;

- individual household services.

Also see “Increasing the adjustment coefficient K1 for UTII from 2021.”

UTII: code of type of entrepreneurial activity

The business activity code for UTII-2, UTII-4 (for entrepreneurs) and UTII-1, UTII-3 (for organizations) should be indicated in accordance with the appendix to the procedure for filling out a tax return for the single tax on imputed income for certain types of activities (Order Federal Tax Service of Russia dated December 11, 2012 No. ММВ-7-6/). Appendix 5 to this order contains UTII codes for each type of activity defined in clause 3 of Art. 346.29 Tax Code of the Russian Federation.

Increased deduction for individual entrepreneurs for insurance premiums “for themselves”

From January 1, 2021, individual entrepreneurs can include insurance premiums paid for themselves in the deduction. Moreover, without a limit of 50% (subclause 1, clause 2, article 346.32 of the Tax Code of the Russian Federation, as amended on January 1, 2017). Before 2021 (for example, in 2016), there was a situation where an individual entrepreneur had the right to reduce the single tax (UTII) by insurance premiums for his employees, but could not deduct insurance premiums “for himself.” For more information about the innovation, see “Insurance premiums of individual entrepreneurs for UTII in 2021: what has changed.”

In 2021, individual entrepreneurs without employees have the right to reduce the amount of UTII by the amount of insurance contributions paid for themselves in a fixed amount to the Pension Fund and the Compulsory Medical Insurance Fund without a limit of 50%.

Who benefits from using UTII?

UTII is suitable for people who receive large profits from their commercial activities. The fact is that “imputation” is a fixed tax, so its size is not affected by the final volume of profit, the cost of goods and other parameters. However, this is also the main disadvantage: if a person was at a loss in the previous period, he still must pay a fixed payment to the treasury.

If an entrepreneur constantly suffers losses, then he can switch to another regime (for example, to the simplified tax system), where other indicators are used as a basis (for example, in the case of the simplified tax system, the entrepreneur’s income is used).

You should also remember that tax must be paid approximately every 25 days, so it is suitable for people who have free time to file and pay.

Transition to UTII-2018

If an individual entrepreneur or organization in 2021 carries out the permitted activities, meeting all the requirements of Art. 346.26 of the Tax Code of the Russian Federation, and in the region where this activity is carried out, the “imputed” regime is officially applied, then you can switch to it:

- from January 1, 2021, if work on this type of activity in 2017 is carried out using the simplified tax system (Article 346.13 of the Tax Code of the Russian Federation);

- on any day of the current year, if this is a new line of business for the company or individual entrepreneur (the application is submitted to the Federal Tax Service within 5 working days from the date of its start);

- also, on any day you can switch to “imputation” from OSNO (letter of the Federal Tax Service of the Russian Federation dated November 11, 2013 No. ED-4-3/20133).

The procedure for switching to UTII is established by Article 346.28 of the Tax Code of the Russian Federation.

List of activities under UTII for 2018

We can name 14 types of activities falling under UTII in 2018. This:

1. Household services.

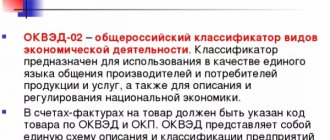

To identify household services as types of activity on UTII in 2021, use their codes from the All-Russian Classifier:

- types of economic activity (OKVED);

- products (OKP).

2. Treatment and prevention for animals.

3. Repair, maintenance and washing of vehicles.

4. Renting out parking spaces, including for the purpose of storing cars (except for impound lots).

5. Transportation of people and cargo by no more than 20 vehicles.

6. Retail trade through shops and pavilions with a sales area of up to 150 sq. m. m for each object.

7. Retail trade through:

- stationary facilities without trading floors;

- mobile objects.

8. Catering with a service hall up to 150 sq. m for each object.

9. Catering without a service hall.

10. Street advertising through special structures.

11.Advertising on vehicles.

12. Temporary accommodation and residence services with a total area of the relevant premises up to 500 square meters. m;

13. Renting:

- retail spaces in a stationary retail chain without sales floors;

- objects of non-stationary trade;

- catering facilities without a service hall.

14. Leasing of land plots for the placement of a stationary and non-stationary retail chain, as well as public catering.

These are the types of entrepreneurial activities for UTII in 2018. Compared to 2017, this list has not changed. There were no global changes in tax law.

We have listed all possible types of activities on UTII in 2018. However, it is not enough to know what types of activities UTII falls under. It is also important that a local law be adopted that gives the go-ahead for the introduction of “imputation” for one or more of the listed occupations.

What's next?

- Number and print each page on a separate sheet.

- Secure the application sheets with a paper clip. There is no need to staple, sign or notarize in advance.

- Take the application to the tax office at the address of your business. For activities from the list above that do not have an exact address, submit an application to the tax office at the registration of an individual entrepreneur or at the legal address of an LLC.

- Sign the application in front of the inspector who accepts it.

- 5 working days after submitting the application, the tax office must issue a notice of application of UTII or a refusal. But inspectors do not always comply with this formality. Call ahead and make sure you are registered.

- Register in Elba to pay tax and submit a UTII report.

If you want to learn more about UTII, read our article: Reporting on UTII.

Physical parameters

To use the UTII system, it is not enough to have a code for the type of activity included in the list. In addition to the State List, it is necessary that the business entity comply with the established physical parameters. Their accounting is regulated by the Tax Code. The following factors determine compliance:

- Application to a specific business area.

- Number of employees, including the owner.

- Number of equipment used, including vehicles.

- Area of territory or premises.

The above physical indicators are a prerequisite and are reflected in the tax return.

Let's give an example. The individual entrepreneur decided to open a snack bar with a hall for serving customers. In this case, the tax calculation will depend on the square meters of the premises, and the amount of UTII will be based on 1000 rubles per month. If an individual entrepreneur opens a catering facility without a service hall, for example a cheburek restaurant, then the tax will depend on the number of hired employees. And the size of UTII will become higher and reach 4,500 rubles per month. The code for the type of such activity corresponds to 12.