VAT rate for export

There are several points of view explaining the appearance of the 0% VAT rate.

On the one hand, VAT is an indirect tax paid by the buyer. Foreign buyers are not subject to the Russian Tax Code and therefore do not have to pay Russian VAT. In this regard, the sale of Russian goods and services to foreigners should occur without tax.

On the other hand, exports are of great importance for the economic growth of the country, so the state is interested in businesses striving to develop sales not only within the country, but also abroad. To increase the interest of entrepreneurs in export operations, there are various stimulating economic instruments. One of them is the VAT rate for export transactions, equal to 0%. Against the backdrop of fairly high regular VAT rates, one of which was recently increased, the use of a zero VAT rate for exports looks very attractive.

Let us remind you what VAT rates exist in Russia in 2021:

Works and services

Based on Article 2 of the Protocol, when performing work or providing services by companies resident in member countries of the Eurasian Economic Union, the base rate of indirect taxes, the procedure for their collection and fiscal benefits are determined in accordance with the legislation of the state whose territory is recognized as the place of sale.

“When determining the place of sale for goods, as a rule, no problems arise. Controversial situations usually concern works and services that are subject to VAT taxation. This is due, first of all, to the economic interests of the EAEU member states.

The rules for determining the place of implementation of work (services) differ significantly in the national legislation of the CU member countries.

According to the general rule established by Article 148 of the Tax Code of the Russian Federation, the place of sale will be the state where the company performing work or providing services operates, unless otherwise provided by special rules listed directly in the said article of the Code.

The national tax legislation of the Republics of Belarus and Kazakhstan contains generally similar approaches to determining the place of implementation of work.

Thus, when performing work in member states of the Customs Union, conflicts related to different criteria of legal personality are possible. This state of affairs can lead to a situation of double taxation, for example, when a Russian company, without having a branch or representative office in Kazakhstan, provides services to a resident of this country. A situation of double charging of fees may also arise in the case where a Russian resident provides services to a company from Kazakhstan through a branch registered there,” comments Evgenia Eremenko, a tax law specialist at the Ural Union audit and consulting group.

Since in the case of return, for example, by a Kazakh commission agent, unsold goods are not acquired, VAT does not need to be paid when importing them into the territory of our country.

[email protected] dated May 31, 2012, taking into account the opinion of the Ministry of Finance, answered the question of an entrepreneur who was planning to purchase translation and proofreading services from a legal entity - a resident of Belarus. The officials concluded that since subparagraphs 1–4 of paragraph 1 of Article 3 of the Protocol do not specify translation and proofreading services, the territory of Belarus is recognized as the place of their provision. In this regard, these services are not subject to VAT in Russia.

Zero rate

So, the subject of our article is VAT on the export of goods.

As mentioned, the VAT rate for exports is 0. Clause 7 of Art. 164 of the Tax Code of the Russian Federation was introduced recently and allows in some situations to refuse the 0% rate:

It is logical to ask, for what purpose or for what reasons can one refuse a preferential rate? One of the reasons is this: you cannot simply take and apply a 0 VAT rate when exporting; you need to confirm it. And confirmation of the 0 VAT rate for export requires the collection of a large amount of documentation, that is, labor and time costs.

We will tell you further what is needed to confirm the zero VAT rate for export.

Confirmation of eligibility for a 0 percent rate

The procedure for confirming the zero VAT rate is described in Art.

165 Tax Code of the Russian Federation. To prove the legality of applying the zero VAT rate for exports, it is necessary to generate the following package of documents:

Instead of copies of the specified documents, paragraph 15 of Art. 165 of the Tax Code of the Russian Federation allows the submission of electronic registers indicating the registration numbers of the relevant declarations.

Electronic registers must be compiled in approved formats and sent to the tax authority via TKS through an EDI operator duly registered in the Russian Federation.

It must be borne in mind that during the audit, tax authorities may require the submission of documents from the electronic register.

The taxpayer is given 180 calendar days to collect documents.

If after 180 days the documents are not collected, the goods sold must be subject to VAT according to Russian rules (at the rates from paragraphs 2 and 3 of Article 164 of the Tax Code of the Russian Federation). If the taxpayer nevertheless collects the entire package of documents after 180 days and pays VAT under Art. 164 of the Tax Code of the Russian Federation, the right to submit documents to the tax office is retained. If the tax authorities come to the conclusion that the 0% rate has become confirmed, the previously paid VAT on exports will be returned to the taxpayer.

Clause 10 of Art. 165 of the Tax Code of the Russian Federation states that the VAT declaration and confirmation documents must be submitted to the tax office at the same time.

Fill it out correctly

According to subparagraphs “k”, “k” of paragraph 2 of the Rules for filling out an invoice, approved by Decree of the Government of the Russian Federation of December 26, 2011 No. 1137, columns 10, 10a and 11 of the documents indicate the country of origin of the goods, as well as the customs declaration number. Please note that these columns are filled in for those products whose country of origin is not Russia.

Sometimes the chain from manufacturer to seller can be very complex, which raises questions for accountants. Financiers gave an answer to them too. Thus, in Letter No. 03-07-14/88 dated September 12, 2012, the Ministry of Finance clarified the issue of issuing invoices for the sale in our country of goods manufactured in China, released for free circulation in Belarus, and then imported into Russia . Officials explained that in this case, dashes are placed in columns 10, 10a and 11 of the invoice. Why is that? Because goods imported from third countries and released for free circulation on the territory of the EAEU are recognized as goods of the union. Keep in mind: in column 10 you can still enter the name of the country or write “Eurasian Economic Union” there, and this fact will not entail a refusal to deduct VAT. In addition, it is not prohibited to indicate several countries of origin of goods (Letter of the Ministry of Finance of Russia dated May 31, 2012 No. 03-07-09/60).

Features of VAT accounting in the presence of export operations

If a company begins to export, then the question arises: what accounting features exist for this type of activity?

Let's analyze the subtleties of export in terms of VAT calculation. Let's consider the concept of export in relation to goods. When exporting services, VAT is paid in the general manner if they are provided on the territory of the Russian Federation. Services are not subject to VAT if provided outside the Russian Federation.

If an organization carries out both taxable and non-VAT-taxable transactions, then clause 4 of Art. 149 of the Tax Code of the Russian Federation requires separate accounting of such transactions, because one of the main conditions for accepting input VAT from a supplier for deduction is the condition that the purchased goods (work, service) are used for operations subject to VAT.

By analogy, we can say that when a 0% rate is applied, it becomes necessary to keep separate records of such transactions. Thus, separate accounting for VAT on exports is necessary.

Let's turn to the regulatory framework. Paragraph 3 clause 10 art. 165 of the Tax Code of the Russian Federation prescribes separate VAT accounting according to the rules established by the taxpayer himself, if he has activities taxed at a 0% rate. However, there is an exception to this rule: when exporting non-commodity goods registered after 07/01/2016, separate accounting can be omitted and VAT can be deducted in the general manner.

Deadline for determining the tax base:

Taxpayers using the simplified tax system, in accordance with paragraph 2 of Art. 346.11 of the Tax Code of the Russian Federation, must pay VAT when importing goods into the customs territory of the Russian Federation. However, nothing is said about the need to pay VAT on exports. Thus, when exporting, simplifiers do not have any VAT obligations.

Purchase returns

Another difficult question is whether to pay VAT or not if the buyer returns the goods. The answer can be found in the Letter of the Ministry of Finance dated May 29, 2012 No. 03-07-15/54.

In Letter No. 03-07-15/57 dated June 1, 2012, the Russian Ministry of Finance explained that transport and forwarding services provided for in the above subclause are subject to VAT at a rate of 0 percent. This rule applies regardless of the number of carriers involved in transporting goods and the rate of charge they apply.

The tax on goods imported within the framework of the Eurasian Economic Union is levied by the tax authorities of the country into which they are imported, at the place of registration of the companies purchasing the goods, after they have been registered. Since in the case of return, for example, by a Kazakh commission agent, unsold goods are not acquired, VAT does not need to be paid when importing them into the territory of our country.

Deduction for export transactions

A pressing question is whether an organization is entitled to deduct VAT when exporting?

The answer is yes. Input VAT for export, that is, the VAT that you paid to the seller for goods used for export, is deductible. But for this there is a certain procedure, somewhat different from the general procedure for accepting VAT for deduction. Those involved in the distribution of VAT on exports need to pay special attention to the process of VAT deduction.

The procedure for applying deductions when calculating export tax is described in paragraph 3 of Art. 172 of the Tax Code of the Russian Federation. It states that exporters of non-commodity goods can deduct input VAT in the general manner, that is, in the same way as for ordinary non-export sales. These rules were introduced on July 1, 2016. Those exporters who refused to use the preferential rate do the same.

For commodity exporters, the process of applying deductions depends on whether a package of documents confirming the zero rate has been collected or not. In addition, if VAT was accepted for deduction earlier, VAT restoration will be required when exporting this product.

Filling out a VAT return when exporting

Let's consider what data and in what sections must be entered when filling out a VAT return for export.

Declaration for export of non-commodity goods

When exporting non-commodity goods, VAT is deductible according to the same rules as for ordinary transactions.

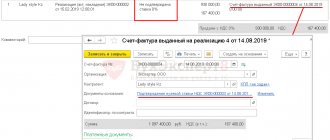

Line 120 of Section 3 must be completed. The fact that the collection of documents does not affect the period for recognition of the deduction does not exempt the taxpayer from collecting a package of documents confirming the zero rate. If this package is formed in the reporting quarter of shipment, the amount of the tax base falls into line 020 of section 4, and line 030 remains empty, otherwise a double deduction will result. Section 4 is completed in the same way during the period of receiving the full package of documents. An example of filling out a declaration regarding export, that is, filling out the specified lines, is shown below.

How to report VAT if you export raw materials

As already mentioned, when exporting raw materials the situation is different, which is why the declaration is filled out differently. For such exporters, there are special export sections 4, 5 and 6 in the declaration.

The completed sections of the declaration (they may be in different declarations for different tax periods) are presented below:

VAT refund on export

VAT refund when exporting is a frequent procedure.

This is due to the peculiarities of export operations, namely the fact that when a 0% rate is applied, the VAT charged to the buyer is zero. Provided that goods for export are purchased from VAT payers, that is, when input VAT exists, VAT refund on export becomes inevitable. The same situation as with the return of export VAT may arise for ordinary transactions carried out within the country. The procedure for refunding export VAT and regular VAT does not differ in any way. Only the package of necessary documents differs: as already mentioned, in order to receive a VAT refund when exporting from Russia, you must collect documents confirming the zero tax rate.

Differences between exports to the EAEU and other countries

Many Russian companies work with neighboring countries, so questions often arise about the specifics of paying VAT when exporting to Uzbekistan from Russia or about VAT reimbursement when exporting to Kazakhstan.

Peculiarities of trade in terms of VAT with close neighbors do exist, but not with all of them. Countries that are part of the Eurasian Economic Union (EAEU) are subject to special conditions:

So, what are the features of accounting for VAT when exporting to Belarus and other EAEU countries?

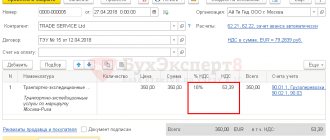

Despite the fact that VAT for exports to Kazakhstan and other EAEU states is zero, since in any case a zero tax rate is applied, an invoice must be drawn up. Indication of the zero VAT rate and the code of the type of goods according to the Commodity Nomenclature of Foreign Economic Activity is mandatory. Here is an example of filling out an invoice indicating the zero VAT rate when exporting to Belarus in 2021:

Exhibition fee

The Federal Tax Service, by letter dated April 10, 2012 No. ED-4-3/ [email protected], brought to the attention of companies clarifications from the Ministry of Finance on issues related to the procedure for paying VAT when purchasing goods previously imported into Russia for participation in exhibitions, as well as products placed in warehouses for storage for further sale. The Service concluded that in these cases the fees were paid by the Russian company purchasing the goods. The organization must submit a declaration, as well as the documents provided for in paragraph 8 of Article 2 of the Protocol, including an application for the import of products and payment of indirect fees.

The place of sale in this case is the territory of the Russian Federation, and sales operations are recognized as subject to VAT taxation: a zero tax rate is applied to them, subject to the submission of the documents provided for in paragraph 2 of Article 1 of the Protocol.

Import from EAEU countries

Let us briefly consider the process of calculating VAT when importing goods from the countries of the Customs Union. Just as when calculating VAT for exports to Belarus and other EAEU countries, the guideline is primarily not the Tax Code of the Russian Federation, but the Treaty on the Eurasian Union.

The main feature is that when importing from Kazakhstan to Russia, VAT will have to be paid in any case, unlike paying VAT when exporting to Kazakhstan. Even simplified people and those who are exempt from paying VAT.

In addition, VAT when importing goods into Russia from Kazakhstan and other EAEU member countries must be paid to your tax office within certain deadlines that differ from the deadlines for paying internal VAT.

This differs import VAT from EAEU countries from customs VAT paid when purchasing from other countries. An import VAT return is different from a regular import VAT return. It is submitted to the tax authority at the place of registration of the organization before the 20th day of the month following the month in which imported goods were accepted for registration. The same deadlines are established for payment of this tax. Subsequently, it can be taken for deduction.

***

Accounting for VAT on exports is a rather labor-intensive process. Exports can be taxed at a preferential zero rate, but for this it is necessary to submit a package of documents to the tax authorities within a certain period. If this is not done, the regular rate of VAT will need to be applied to export transactions.

Customs Union: principles of VAT collection

On December 11, 2009, in order to implement the agreement on the principles of collecting indirect taxes on the export, import of goods, performance of work and provision of services in the Customs Union of Russia, Belarus and Kazakhstan (CU), several protocols were signed. The first intergovernmental protocol regulates taxation issues for the export and import of goods sold within the Customs Union. When importing goods, indirect taxes - VAT and excise taxes - will be collected by tax authorities, with the exception of excise taxes on excisable goods, which are subject to mandatory labeling (collection will continue to be handled by customs services). When importing into the Russian Federation, taxes will be paid by the owner of the cargo. The tax base for goods imported into the territory of the Russian Federation is determined as the cost of goods, which is reflected in the agreement between the seller and the buyer. When importing goods into Russia, indirect taxes will have to be paid by all taxpayers of the Russian Federation, regardless of what taxation regime they apply. Tax rates are determined by the Tax Code of the Russian Federation, Chapters 21 and 22. Payment must be made monthly, no later than the 20th day of the month following the one in which the purchased goods were registered with the taxpayer. When importing goods, importers will have to pay tax and, accordingly, report to the tax authorities by submitting a declaration and a number of documents that confirm the actual payment. The most important document is a statement indicating payment of taxes on imported goods. Confirming the fact of paying taxes on the territory of the Russian Federation, the tax authorities affix a stamp on this application stating that the tax has been paid in full. Then the buyer of goods submits the application to his exporting counterparty in the territory of another state of the Customs Union, for which this document will be the basis for obtaining in his country the right to apply a zero rate on value added and, accordingly, exemption from excise taxes. Some goods imported into the Russian Federation are exempt from VAT. Their list is provided for in Article 150 of the Tax Code. If a taxpayer has tax or excise taxes when selling goods, works and services in Russia, he has the right not to pay VAT and excise taxes when importing goods from the territories of the CU member states. In this case, the overpayment that was created when selling goods on the territory of the Russian Federation can be offset against taxes when importing goods from countries participating in the Customs Union. For goods exported to the countries of the Customs Union, a zero VAT rate and exemption from excise taxes . To obtain confirmation of the application of the zero rate, the taxpayer must submit the relevant documents to the tax authorities. For the exporter, the main document is the application given to him by the importing counterparty (see above). If the taxpayer does not have a paper application with marks from the tax authorities, the tax authorities have the right to provide a zero rate to the exporter based on confirmation of payment of indirect taxes in the territory of the importing country, received by the tax service electronically from their colleagues from another state of the Customs Union . The deadline for submitting documents with which the taxpayer can confirm the right to apply the zero rate is 180 days from the date of shipment . Refund of input VAT when applying a zero rate occurs in the same manner and on the same conditions as provided for by the Tax Code (Articles 171 and 172 - the procedure for applying deductions when exporting goods). Reimbursement in the event that a taxpayer receives a negative difference in value added tax will be made in accordance with the provisions of Article 176 and Article 176.1 of the Tax Code of the Russian Federation, which entered into force on January 1, 2010. The second intergovernmental protocol concerns the collection of indirect taxes when performing work and providing services in the Customs Union. The main thing is to determine the place of sale of work/services when the seller and buyer are located in different states of the Customs Union. First of all, this is necessary in order to avoid double taxation in different countries. At the same time, it is important that a situation does not arise where the service is not taxed either in the territory of the seller’s country or in the territory of the buyer’s country. Almost the entire procedure for determining the place of sale of work/services, which is established by the Tax Code of the Russian Federation (Article 148), is preserved. The protocol contains small additions to Article 148. They consist in the fact that design and technological services will be taxed at the location of the buyer , and not the seller, as was previously the case. The Protocol also establishes a zero VAT rate for work/services for processing customer-supplied raw materials . This applies to those operations when one of the economic entities located on the territory of the Customs Union transfers customer-supplied raw materials to its counterparty in another country for processing. In this case, the right to apply the zero rate will be given to the enterprise that processes raw materials. Based on the report of Olga Tsibizova, head of the indirect taxes department of the Department of Tax and Customs Tariff Policy of the Ministry of Finance of the Russian Federation.