What does the FSS check?

There are several main points that exist in the activities of almost any company that may be of interest to the Social Insurance Fund:

- Calculation and payment of contributions (correctness of calculation, whether payment is timely);

- The procedure for spending money that the policyholder has accrued for insured events such as maternity leave, sick leave or parental leave;

- Vouchers;

- The procedure for spending money transferred when an employee receives an injury.

Thus, inspectors from the Social Insurance Fund ensure that the transferred insurance payments are justified, and that the contributions are calculated correctly and transferred on time.

For additional control of reports sent to the FSS, companies can check them using a special FSS check. It checks whether the employer has filled out the calculation correctly, determined the base, as well as the amount of accruals and payments. This check is carried out based on control ratios and is performed free of charge.

What checks does the FSS conduct?

There are several types of FSS checks (Law No. 255-FZ):

- Desk - during such an audit, payments for insurance coverage are reconciled based on claims for compensation, or information from the tax office;

- Unscheduled on-site visit - carried out if social insurance has received a complaint from an insured person, suggesting that the insurance coverage was accrued incorrectly to him;

- Scheduled on-site audit - such an audit is carried out together with the tax office in order to determine the correctness of payments for insurance coverage;

- A check necessary to determine the correctness of the calculations, as well as the timeliness and completeness of payment of contributions due until 2021.

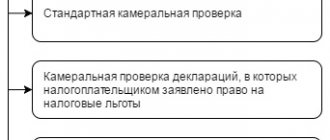

The main goal of all inspection activities is to monitor companies’ compliance with Russian legislation. A desk audit is carried out upon receipt of each report from the company. If, as a result of the “camera camera”, violations are identified or a decision is made, the FSS will send an inspection report to the person being inspected. If the camera meeting is successful, then no reports are sent to the companies.

Important! You can find out about upcoming scheduled inspections of the FSS on their official website for the regional office.

What can the FSS check?

First of all, the territorial body of the Social Insurance Fund is usually interested in justifying the costs of paying out insurance coverage (hereinafter referred to as SB), and secondly, in the correctness of calculation of insurance premiums and compliance with the deadline for their transfer.

Therefore, to the question of what documents to prepare for the FSS inspection in 2017, the answer is:

- documents confirming expenses for CO;

- documents related to the calculation and transfer of contributions.

This conclusion is confirmed, among other things, by the provisions of Articles 26.14, 26.16 F. Law No. 125-FZ.

The specific list of documents depends directly on the situation. These may include, but are not limited to:

- source documents;

- payroll statements;

- contracts;

- acts confirming the facts of injury, etc.

What does the FSS check during an on-site inspection in 2021?

As noted above, an on-site inspection can be either scheduled or unscheduled. To check whether contribution payers comply with legal requirements, the Social Insurance Fund draws up a plan for the year. Reasons for scheduled inspections include requests for funds for payment of benefits, complaints from employees, as well as processes of liquidation and reorganization of the company.

Important! The main thing that interests inspectors from the Social Insurance Fund is how the transferred amounts are spent, the procedure for calculating and paying contributions in the case of sick leave or maternity benefits.

Checking sick leave

Sick leave certificates are checked by FSS employees with special care, since they are the only confirmation that the employee needs to be paid benefits. The sheets are checked both during desk and on-site inspections. What exactly does the FSS check on sick leave:

- Does the sick leave form comply with State Standards and is it not a fake?

- Availability of the doctor's seal and signature on the sick leave (they must be clear and legible);

- Correct filling (all information about both the employee and the organization must be clearly filled out). If there are errors on the sick leave, they must be certified in the required manner.

Important! The FSS checks not only whether the employer filled out the sick leave correctly, but also how the medical institution filled it out. Errors in the employee's full name or employer's name are not allowed.

Appealing the pension fund inspection report

The policyholder has the right to object to the inspection report within 15 days from the date of receipt.

In addition, a complaint against the inspection report can be filed with a higher authority of the pension fund and/or in court. In this case, you can simultaneously appeal to a higher authority and to the court.

When appealing, it is necessary to point out the violations committed by the inspectors during the inspection, and also indicate that certain conclusions of the inspectors are not unreasonable, and therefore ask to declare the act invalid. Most often, decisions to prosecute are challenged, however, one should not forget about challenging the inspection report.

HEALTHY:

What documents will the FSS require during inspection?

The first thing that FSS employees check is the reports 4-FSS and 4a-FSS. The organization must store these reports for at least 5 years, since future benefits are calculated on the basis of previous periods.

In addition, the inspector may request other documents. Initially, documents are requested orally, and if they are not immediately provided, then a written request is sent, which the person being inspected is obliged to fulfill within 10 days. If suddenly the company being inspected does not meet the 10-day deadline, it has the right to ask for an extension. To do this, a letter is sent to the FSS indicating the request for an extension of the period, as well as the justification for its extension. In response, the FSS will send a decision in which the deadline may be extended or refuse to extend it.

General procedure for desk audit

The desk audit will begin from the day when the policyholder submitted a calculation to the Pension Fund of the Russian Federation in the RSV-1 Pension Fund form. Such an inspection may last three months from this date (Part 2 of Article 34 of the Law of July 24, 2009 No. 212-FZ).

When conducting a desk audit, fund employees are guided by Article 34 of the Law of July 24, 2009 No. 212-FZ and the Methodological Recommendations approved by the order of the Pension Fund Board of July 31, 2014 No. 323r.

A desk audit is carried out on the territory of the fund. Therefore, in addition to the calculation itself, fund employees can only use documents they already have during the inspection. Eg:

- calculations of insurance premiums presented earlier;

- documents that the policyholder submitted with the initial calculations - if we are talking about a desk audit of the updated calculation;

- extracts from accounting or tax registers;

- other documents received from the policyholder in the manner established by the Law of July 24, 2009 No. 212-FZ.

Fund employees have the right to request additional documents only if they identify any errors or contradictions in the submitted reports. In this case, they may require the organization to correct these nonconformities. And also has the right to request written or oral explanations.

Inspectors must inform the payer about any errors (inconsistencies) identified. At the same time, they will send a request to make corrections to the calculation. This requirement must be fulfilled within five working days. The period is counted from the day following the day when the organization received the demand via TKS or in person. If the request arrived by mail, then it is considered received on the sixth day from the date of dispatch, which is indicated in the stamp. Along with explanations, you can additionally submit documents to the fund that confirm the accuracy of the data. For example, extracts from accounting registers.

Such rules are established in parts 3–4 of Article 34 of the Law of July 24, 2009 No. 212-FZ.

In addition, during a desk audit, Pension Fund employees can call the payer of contributions to the territorial office of the fund to give oral explanations (clause 3, part 1, article 29 of the Law of July 24, 2009 No. 212-FZ). The call is issued in writing.

Situation: is it possible not to comply with the requirement of the Pension Fund of the Russian Federation to provide written explanations if this document does not indicate specific errors and (or) contradictions identified during a desk audit?

Yes, you can.

The Pension Fund of the Russian Federation has the right to demand written explanations from the organization only if there are errors and contradictions in the reporting. In this case, inspectors are obliged to inform the organization about specific identified inaccuracies and at the same time may require written explanations for them. This is stated in Part 3 of Article 34 of the Law of July 24, 2009 No. 212-FZ.

When there are no errors or contradictions, fund employees have no reason to demand an explanation from the policyholder. And if they nevertheless requested such without indicating specific errors and (or) contradictions, then this requirement may not be fulfilled. It is considered illegal.

Advice: It is still worth responding to the illegal request of the Pension Fund. Write that Pension Fund employees can demand clarification only if there are errors and contradictions in the calculation (Part 3 of Article 34 of Law No. 212-FZ of July 24, 2009). And since the received request does not say anything about errors, the request looks unreasonable and the organization cannot fulfill it.

On-site inspection results

Based on the results of the on-site inspection, the FSS draws up a report. Initially, before the inspection report, on the last day of the inspection, the inspector from the Social Insurance Fund draws up a certificate indicating the subject of the inspection, as well as the timing of the inspection.

Important! The report on the results of the inspection is drawn up within 2 months after the issuance of such a certificate. After drawing up the report, it is transferred to the audited company within 5 days.

The act is signed by both the inspector from the Social Insurance Fund and a representative of the company being inspected. If the company does not agree with the contents of the act, then it can present its objections before signing it (Read also the article ⇒ Inventory of wage calculations in 2021 + postings).

Controlled period

An on-site inspection may cover a period not exceeding three calendar years preceding the calendar year in which the decision to conduct the audit was made. But now only 2010 can be checked. After all, it was from January 1, 2010 that the funds were given the authority to monitor the correctness of calculation, completeness and timely payment of insurance premiums in accordance with Law N 212-FZ. On-site inspections of the payment of unified social tax and pension contributions for previous periods are carried out by tax inspectorates. The corresponding clarifications are given in the joint Letter of the Federal Tax Service of Russia N MMV-22-2/ [email protected] and the Pension Fund of the Russian Federation N AD-30-24/9291 dated August 31, 2010. As part of on-site inspections of the correctness of payment of the unified social tax, tax inspectorates are authorized to identify including errors related to the payment of pension contributions. But tax inspectors do not have the right to hold businessmen accountable for identified violations regarding the payment of pension contributions. Having discovered arrears for the period before January 1, 2010, the inspector must transfer the information to the territorial office of the Pension Fund where the merchant is registered. In turn, the fund will make a decision to hold the inspected person liable for non-payment of pension contributions. This joint Letter instructs tax inspectors to send pensioners reports of desk audits, extracts from reports of on-site audits, documents confirming arrears of pension contributions, and other necessary materials. All this information is transmitted no later than two business days following the day the tax audit report is signed. Note that the inspection must inform the businessman that within 15 days the businessman can submit his objections to the on-site inspection report to the Pension Fund. If the individual entrepreneur forwarded such objections to the inspection, the inspectors will forward them to the Pension Fund.

Employer's liability

Fines that can be imposed by the FSS are provided for in Law No. 125-FZ and the Code of Administrative Offenses of the Russian Federation. For delay in providing calculation of contributions, a fine will be charged in the amount of 5% of insurance premiums for the last three months in the billing period. In this case, both the maximum and minimum limits must be observed - respectively, no more than 30% of the specified amount, but not less than 1000 rubles.

Let's consider the administrative liability for the employer in case of violation of the requirements of the legislation of the Russian Federation regarding the provision of certain documents:

| Violation | Fine, rubles |

| For violation of the deadline for providing information to the Social Insurance Fund on opening/closing a bank account | 1000 – 2000 |

| For late submission of calculations for social insurance and occupational diseases | 300 – 500 |

| Refusal to provide or untimely provision of information requested during the inspection, as well as provision of information incompletely or with errors | 300 – 500 |

How to prepare for on-site inspections from the Social Insurance Fund and the Pension Fund of Russia?

Joint inspections of the Pension Fund of the Russian Federation and the Social Insurance Fund are a mandatory event regulated by federal law dated July 24, 2009 No. 212-FZ “On insurance contributions to the Pension Fund of the Russian Federation...”. Often such inspections come as a surprise to enterprises. The Expert service from SKB Kontur will help you avoid a “surprise” from the Social Insurance Fund and Pension Fund.

The expert assesses the likelihood of inspections based on reporting on insurance premiums and points out those aspects of the company’s activities that may attract the attention of the Pension Fund and the Social Insurance Fund. In addition, by assessing the likelihood of an inspection with the help of an Expert, the company’s accountant will be able to put in order the documents that inspectors may request during the inspection.

What documents may the inspector require?

The list of documents that inspectors may require is contained in the methodological recommendations of the FSS and the Pension Fund of Russia. According to Federal Law No. 212, the requested documents are provided in the form of copies certified by the head of the organization being inspected. However, notarized copies will not be accepted. You should also pay attention to the fact that inspectors have the right to request the same document an unlimited number of times.

The list of documents that inspectors may request during an inspection is extensive:

- Constituent documents. Based on them, inspectors will establish the name, legal and actual address of the company and the type of its activities. In addition, the constituent documents indicate the procedure for paying dividends, which are not subject to insurance contributions.

- Accounting and tax registers. These documents will allow inspectors to establish the procedure for maintaining the accounting policy of the enterprise and the presence or absence of “salary schemes” aimed at avoiding the calculation of insurance premiums.

- Calculations of accrued and paid insurance premiums. They are verified with primary accounting and tax accounting documents.

- Books of accounting of income and expenses and business transactions for the audited period. It is known that organizations operating under a simplified taxation scheme are payers of insurance premiums for compulsory insurance, so ledgers will confirm the accrual and payment of remuneration to employees who have entered into employment or civil law contracts with an employer company that uses the simplified tax system.

Organizations that are awaiting an on-site inspection from the Pension Fund of Russia or the Social Insurance Fund should pay attention to the fact that inspectors often request documents that they do not have the right to demand. In addition, inspection specialists may ask to see documents that, in principle, are not maintained by the organization. For example, a list of persons working on the basis of civil contracts. The organization is not obliged to keep records of these persons and provide it during inspections. There is no punishment or fine for the absence of such documents - after all, the amount of contributions to the Social Insurance Fund and the Pension Fund is not calculated on their basis.

In addition to constituent documents, accounting and tax registers, calculations of accrued insurance premiums and books of income and expenses, the inspector has the right to request:

- Accounting statements for the audited period. On its basis, information about the enterprise’s debts to extra-budgetary funds, which is indicated in the balance sheet and reports to the funds, is compared.

- Employment contracts are necessary for inspectors to verify the date of hire of employees, as well as their salaries, allowances and bonuses. This information allows you to determine the completeness and timeliness of the transfer of insurance premiums to the funds.

- Civil agreements (contracts) with individuals. In such contracts, in addition to the amounts of remuneration, the subject of the contract is studied: does it relate to contracts for the provision of services (performance of work) or to the transfer of property rights, for example, a lease agreement.

Please note that inspectors will try to reclassify a civil contract into a labor contract. This is possible if the subject of the contract is spelled out incorrectly: the contract was concluded not for the performance of a specific service, but for the performance of functions. At the same time, payments made under civil contracts are not subject to insurance contributions payable to the Social Insurance Fund (subclause 2 of clause 3 of Article 9 of Federal Law No. 212).

Inspectors may also be interested in:

- Banking and cash documents : bank statements, instructions, orders, cash book, cashier's journal, cashier's reports, etc. In these documents, fund specialists will look for methods of avoiding official salaries.

- Primary accounting documents confirming the facts of the enterprise's economic activities. The purpose of checking these documents is to determine the completeness of the report for advances issued and to calculate contributions for the difference.

- Personnel documents : work books and documents on personnel accounting and movement. Work books are necessary to compare the dates of hiring, dismissal, transfer, promotion indicated in them with the dates entered in other personnel documents. Primary HR records are required to verify the dates of hiring, dismissal, payment of bonuses and salaries.

- Documents for payments related to insurance coverage : certificates of incapacity for work, orders for employment, time sheets, pay slips for salary payments, application and order for maternity leave.

Responsibility for failure to provide documents.

Federal Law No. 212 provides for the obligation of insurance premium payers, during the audit, to provide fund specialists with documents that confirm the correctness of calculation and completeness of payment of all amounts. Data can be provided both in printed form and on electronic media. The period for providing the requested documents is 10 working days. According to Article 48 of Federal Law No. 212, late submission of documents or refusal to submit them entails a fine of 200 rubles for each unsubmitted document.

Organizations that are awaiting inspections by the Pension Fund of Russia and the Social Insurance Fund should carefully review the documents to see if they correspond to each other: whether the indicated amounts and timing of transfers to extra-budgetary funds coincide.

The Expert service will help you avoid hasty preparation of documents during on-site inspections: timely assess the likelihood of a visit from the Pension Fund of the Russian Federation and the Social Insurance Fund and put the organization’s documents in order. An expert will tell you what you should pay attention to. You can purchase the service on the purchase page.