Accounting policy parameters for accounting purposes

Accounting and qualification of assets

| Item no. | Accounting policy element | Possible accounting methods | Legal norms |

| 1.1 | Asset accounting and qualification | Possible options:

| clause 5 FSBU 6/2020 Recommendation of the BMC dated May 29, 2019 N R-100/2019-KpR “Implementation of the rationality requirement” (Example 1) clause 4 of BMC Recommendations dated December 11, 2020 N R-122/2020-KpR “Special means of production” |

| 1.2 | Classification of assets as non-essential | It is necessary to determine the criteria for objects to be classified as assets, the value of which is insignificant for the financial statements:

| Recommendations BMC R-100/2019-KpR dated May 29, 2019 (Example 1) |

| 1.3 | Procedure for accounting for immaterial assets | Determine the method of accounting for immaterial assets | |

| 1.4 | Method of reflecting the consequences of changes in accounting policies in connection with the transition to FAS 5/2019 | Possible methods:

| clause 47 FSBU 5/2019 |

Accounting for fixed assets (PBU 6/01 continues to apply in 2021)

| Item no. | Accounting policy element | Possible accounting methods | Legal norms |

| 2.1 | Establishing a cost limit for fixed assets |

| para. 4 clause 5 PBU 6/01 |

| 2.2 | Selecting a method for determining the initial cost of fixed assets (only entities using a simplified accounting system) | Possible methods:

| clause 8.1 PBU 6/01 |

| 2.3 | Choosing a depreciation calculation method | Possible methods for calculating depreciation:

Can:

| clause 18 PBU 6/01 |

| 2.4 | Selecting a depreciation period (only entities using a simplified accounting system) | Possible periods:

| clause 19 PBU 6/01 |

| 2.5 | Implementation of the revaluation procedure | Possible options:

| clause 15 PBU 6/01 |

Accounting for intangible assets

| Item no. | Accounting policy element | Possible accounting methods | Legal norms |

| 3.1 | The procedure for recognizing expenses for the acquisition (creation) of intangible assets (only entities using a simplified accounting system) | Possible methods

| clause 3.1 PBU 14/2007 |

| 3.2 | Choosing a depreciation calculation method | Possible methods for calculating depreciation:

Can:

| clause 28 PBU 14/2007 |

| 3.3 | Implementation of the revaluation procedure | Possible options:

| clause 17 PBU 14/2007, clause 16 Letter of the Ministry of Finance dated June 29, 2016 N PZ-3/2016 |

Inventory accounting

| Item no. | Accounting policy element | Possible accounting methods | Legal norms |

| 4.1 | Application of FSBU 5/2019 “Inventories” from 01/01/2021 (only micro-enterprises using a simplified accounting system) | Possible methods:

| para. 2 clause 2 FSBU 5/2019 |

| 4.2 | The procedure for accounting for the cost of inventories for management needs | Possible methods:

| para. 3 clause 2 FSBU 5/2019 |

| 4.3 | The procedure for determining the actual cost of inventories upon acquisition (only entities using a simplified accounting system) | Possible methods:

| clause 11, 17 FSBU 5/2019 |

| 4.4 | The procedure for accounting for costs of procuring goods (GRP) to central warehouses (bases) | Possible methods:

| clause 21 FSBU 5/2019 |

| 4.5 | Product valuation (retail only) | Possible methods:

| clause 20 FSBU 5/2019 |

| 4.6 | The procedure for determining the actual cost of inventories when purchased with non-cash assets (only entities using a simplified accounting system) | Evaluation options:

| clause 14 FSBU 5/2019 |

| 4.7 | The procedure for evaluating agricultural, forestry, fishery products, goods traded on exchanges | Possible options for estimating inventories at the reporting date:

| clause 19, 34 FSBU 5/2019 |

| 4.8 | The procedure for subsequent valuation of reserves (only entities using a simplified accounting system) | Possible options for estimating inventories at the reporting date:

A reserve for impairment of inventories is created for the difference (1C KORP) | clause 28-32 FSBU 5/2019 |

| 4.9 | Method for assessing inventories upon disposal (release of raw materials into production, shipment of goods, finished products, write-off of inventories) | Possible methods:

Can:

| clause 36-38 FSBU 5/2019 |

| 4.10 | The procedure for applying inventory valuation at average cost | Possible methods:

| clause 39 FSBU 5/2019 |

Accounting for costs, work in progress and finished products

| Item no. | Accounting policy element | Possible accounting methods | Legal norms |

| 5.1 | Classification of costs into direct and indirect in the production of products, performance of work, provision of services | Determine the composition and methodology of accounting:

| clause 24 FSBU 5/2019 |

| 5.2 | Method for allocating indirect production costs | Determine how to allocate indirect production costs For example, in 1C you can determine the distribution base for such costs:

| clause 25 FSBU 5/2019 |

| 5.3 | Composition of management costs and the procedure for their accounting | Determine the composition and methodology for accounting for management costs | clause 24 FSBU 5/2019 |

| 5.4 | The procedure for accounting for costs due to improper organization of production, work, and services | Possible methods:

| clause 26 FSBU 5/2019 Recommendation of the BMC dated May 29, 2019 N R-100/2019-KpR “Implementation of the rationality requirement” |

| 5.5 | Assessment of work in progress and finished products as of the reporting date (only for mass and serial production) | Possible methods:

| clause 9, 27 FSBU 5/2019 |

| 5.6 | Accounting for semi-finished products of own production | Possible methods:

| pp. “e” clause 3 FSBU 5/2019 |

Accounting for settlements with employees and contractors

| Item no. | Accounting policy element | Possible accounting methods | Legal norms |

| 6.1 | Accounting for settlements with employees for amounts allocated for administrative, economic and other costs for the needs of the organization | Develop a way, for example:

| Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 N 94n |

| 6.2 | Accounting for tickets issued in electronic form purchased by an organization for employee business trips | Develop a way, for example:

| Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 N 94n |

Accounting for financial investments

| Item no. | Accounting policy element | Possible accounting methods | Legal norms |

| 7.1 | Recognition of expenses associated with the acquisition of securities | Possible methods (not automated in 1C):

| clause 11 PBU 19/02 |

| 7.2 | The procedure for determining the current value of debt securities for which the market value is not determined | Possible methods:

| clause 22 PBU 19/02 |

| 7.3 | A method for assessing financial investments upon disposal (by which the current market price is not determined) | Possible methods (not automated in 1C):

| clause 26-29 PBU 19/02 |

Accounting for interest on loans and credits

| Item no. | Accounting policy element | Possible accounting methods | Legal norms |

| 8.1 | Accounting for interest on loans and credits when purchasing an investment asset (only entities using a simplified accounting system) | Possible methods:

| clause 7 PBU 15/2008 |

| 8.2 | Criteria for recognizing an asset as an investment one | Determine the criteria by which an asset is recognized as an investment asset, for example:

the amount of expenses above which the fixed asset will be considered an investment asset | clause 7 PBU 15/2008 |

Accounting for income and expenses

| Item no. | Accounting policy element | Possible accounting methods | Legal norms |

| 9.1 | Classification of income and expenses | The procedure for recognizing the following income and expenses is determined:

| clause 5 PBU 9/99 clause 5 PBU 10/99 |

| 9.2 | The procedure for determining the degree of completion of work under long-term contracts as of the reporting date | Options (not automated in 1C):

by the share of expenses incurred as of the reporting date in the estimated total expenses under the contract | clause 20 PBU 2/2008 |

State aid

| Item no. | Accounting policy element | Possible accounting methods | Legal norms |

| 10.1 | The procedure for accounting for budgetary funds | The organization accepts budget funds for accounting:

| clause 5 PBU 13/2000 |

| 10.2 | Presentation of deferred income in reporting related to the receipt of budget funds to finance capital expenditures | Possible options:

| clause 21 PBU 13/2000 |

Estimated values

Accounting for income tax calculations

| Item no. | Accounting policy element | Possible accounting methods | Legal norms |

| 12.1 | Method for determining current income tax | Possible options:

| clause 22 PBU 18/02 |

Error correction

| Item no. | Accounting policy element | Possible accounting methods | Legal norms |

| 13.1 | Correction of significant errors of previous years identified after the approval of the financial financial institution (only entities using a simplified accounting system) | Possible options:

| clause 9, 14 PBU 22/2010 |

| 13.2 | The procedure for classifying an error as significant | A significant error is one that:

| clause 3 PBU 22/2010 |

Application of PBU

| Item no. | Accounting policy element | Possible accounting methods | Legal norms |

| 14.1 | PBU 12/2010 “Information by segments” (determined for all organizations) |

| PBU 12/2010 |

| 14.2 | PBU 18/02 “Accounting for corporate income tax calculations” (only entities using a simplified accounting system) |

| PBU 18/02 |

| 14.3 | PBU 2/2008 “Accounting for construction contracts” (only entities using a simplified accounting system) |

| PBU 2/2008 |

| 14.4 | PBU 8/2010 “Estimated liabilities, contingent liabilities and contingent assets” (only entities using a simplified accounting system) |

| PBU 8/2010 |

| 14.5 | PBU 11/2008 “Information about related parties” (only entities on a simplified accounting system) |

| PBU 11/2008 |

| 14.6 | PBU 16/2002 “Information on discontinued activities” (only entities using a simplified accounting system) |

| PBU 16/2002 |

| 14.7 | FSBU 25/2018 “Accounting for leases” | Apply early starting from 2021 | clause 48 FSBU 25/2018 |

Form of presentation of financial statements

| Item no. | Accounting policy element | Possible accounting methods | Legal norms |

| 15.1 | Form for presenting annual financial statements (only entities using a simplified accounting system) | Select a reporting form option:

| Order of the Ministry of Finance of the Russian Federation dated July 2, 2010 N 66n |

What changes need to be made to the accounting policy?

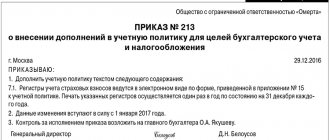

Firstly, Order No. 209n introduces new accounts into the Chart of Accounts[4]:

– 0 210 13 000 “Calculations for VAT on advances paid”;

– 0 401 10 174 “Lost income”.

These changes entail amendments to the section of the accounting policy relating to the operating chart of accounts of the autonomous institution.

Secondly, since new accounts are introduced, the procedure for their application is accordingly added. This, in turn, entails making changes to the used correspondence of accounts to reflect standard transactions in an autonomous institution.

| Contents of operation | Debit | Credit |

| Adding correspondence to VAT invoices | ||

| The amount of VAT on the transferred advance has been allocated | 0 210 13 000 | 0 210 12 000 |

| Accepted for deduction is VAT presented by the supplier in the amount allocated when transferring an advance to the supplier on account of the upcoming delivery of goods (works, services) | 0 303 04 000 | 0 210 13 000 |

| Adding correspondence to accounts for lost income | ||

| A penalty was charged against the counterparty in accordance with the terms of the government contract | 0 209 40 000 | 0 401 10 140 |

| Lost income is reflected in the form of writing off the amount of the penalty in accordance with Order of the Ministry of Finance of the Russian Federation dated April 12, 2016 No. 44n | 0 401 10 174 | 0 209 40 000 |

In addition to correspondence on new accounts, the Ministry of Finance introduces correspondence on other transactions, which Instruction No. 183n did not previously contain. Therefore, it is worth paying attention to the order in which the following transactions are reflected:

- calculations for subsidies received as part of government assignments;

- calculations for subsidies received for other purposes;

- calculations for compensation of institution expenses;

- changes in the cadastral value of land plots;

- assigning the actual cost of paid services provided to reduce the financial result of the current financial year.

Next, you need to pay attention to the adjustments to the following sections of the accounting policy:

1. The procedure for recording events after the reporting date. The Ministry of Finance, by Order No. 209n, introduced the following clarification into Instruction No. 157n: if, in order to comply with the deadlines for submitting financial statements and (or) due to the late receipt of primary accounting documents, information about an event after the reporting date is not used when preparing financial statements, information about this event and its valuation in monetary terms is disclosed in the explanatory note when submitting reports.

At the same time, according to paragraph 6 of Instruction No. 157n, the accounting entity (state (municipal) institution) in its accounting policy discloses the procedure for recognizing in accounting and disclosing events after the reporting date in the financial statements.

2. The procedure for conducting an inventory of property and liabilities. Due to the changes made to clause 20 of Instruction No. 157n, from 2021 it is mandatory to carry out an inventory:

- when establishing facts of theft or abuse, as well as damage to valuables;

- in the event of a natural disaster, fire, accident or other emergency caused by extreme conditions;

- when changing financially responsible persons (on the day of reception and transfer of cases);

- when transferring an organization’s property for rent, management, free use, as well as when purchasing or selling a complex of accounting objects (property complex);

- in other cases provided for by the legislation of the Russian Federation or other regulatory legal acts of the Russian Federation.

Let us add that similar norms are currently contained in Order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49. If the accounting policy of the AU already contained these provisions, then the adjustment should be made only in relation to the normative act (indicate on the basis of clause 20 of Instruction No. 157n).

3. Primary documents. The procedure for generating a primary accounting document is set out in clause 9 of Instruction No. 157n. According to the new provisions, if accounting is maintained by a centralized accounting department in accordance with the concluded agreement, the rules of document flow[5], the technology for processing accounting information are established in the manner prescribed by the agreement.

Download a free example of an LLC accounting policy using the simplified tax system for 2021

As the initial sample, we chose the organization’s accounting policy - sample 2021 for an LLC operating in the catering industry and using the simplified tax system “Income minus expenses” (15%). Then we analyzed the proposed example of accounting policy for changes that come into force on 01/01/2021. The resulting result can be downloaded from the link.

In the Ready-made solution from ConsultantPlus, you can familiarize yourself with a sample accounting policy for a trading organization on the OSN; production organization at OSN. And to see the procedure for drawing up an accounting policy for VAT, refer to this Ready Solution. If you do not have access to K+, sign up for a trial demo access for free.

Accounting policy for OSNO for 2021

According to Russian tax legislation, work on OSNO for the next year must be drawn up and approved before the start of the new reporting period. That is, the act for 2021 must be drawn up before December 31, 2021. The very first thing the head of the company (organization, firm) must do is issue a decree (order) of the appropriate sample, approving the direction of work for the next year.

Download a free sample Order for 2021 in doc format, available at the link:

If the company has just been created, then this document must be formulated within ninety days, and the report begins from the day when information about the newly emerged organization was recorded in the Unified State Register of Legal Entities. You can read more about this in Article No. 313 of the Tax Code of the Russian Federation.

Objectives of accounting policies

An accounting policy is a document in which an organization consolidates the chosen methods of accounting. Those that take into account the specifics of its activities.

The accounting policy requirements are specified in paragraph 6 of PBU 1/2008. Among them, for example:

- a complete reflection of all factors of economic activity, that is, all transactions without exception must be reflected in accounting;

- timely accounting of transactions, that is, they must be shown in the periods in which they were completed;

- priority of the economic content of the facts of economic activity over their legal form. For example, operations related to the acceptance and transfer of a leased property must be reflected in accounting, regardless of the date of state registration of the lease agreement (Resolution of the Federal Antimonopoly Service of the North-Western District dated February 25, 2005 No. A42-6647/03-20).

Do I need to submit my accounting policy to the tax office?

The financial statements do not include copies of orders approving accounting policies for accounting purposes (Article 14 of the Law of December 6, 2011 No. 402-FZ, clause 5 of PBU 4/99). Therefore, at the initiative of the organization, there is no need to submit them to the tax office.

Who should formulate accounting policies?

By virtue of clause 6 of Instruction No. 157n, the accounting policy adopted by an autonomous institution is approved by order or directive of the head of the state (municipal) institution.

At the same time, the current regulations do not answer the question of which of the organization’s specialists should develop accounting policies. Meanwhile, as follows from clause 5 of the draft federal standard “Accounting Policies, Estimates and Errors”, accounting policies should be formed by the chief accountant of the institution or another individual (legal) person entrusted with accounting. Let us remind you that it is the chief accountant who is responsible for maintaining accounting records and timely submission of complete and reliable financial statements. In turn, approval of accounting policies is the responsibility of the head of the institution. In the event of transfer of responsibilities for maintaining accounting records and preparing accounting (financial) statements of an institution to centralized accounting, the body exercising the functions and powers of the founder has the right to determine the accounting policy to be applied.

When companies approve accounting policies

First, let's dispel the long-standing myth that accounting policies need to be approved annually. In fact, if there are no changes, then the adopted policy must be consistently applied from year to year - Art. 8 of the Law “On Accounting” dated December 6, 2011 No. 402-FZ.

The following deadlines apply for organizations regarding the development and approval of accounting policies:

| Situation | Accounting policy | |

| for used | for NU | |

| Creation of a new organization | Within no more than 90 days from the date of registration (clause 9 of PBU 1/2008, approved by order of the Ministry of Finance of Russia dated October 6, 2008 No. 106n) | No later than the end date of the organization’s first tax period (Clause 12, Article 167 of the Tax Code of the Russian Federation) |

| Making changes to accounting policies | As a general rule, a new accounting policy is approved in the current year and applied from the beginning of the next year (clauses 10, 12 of PBU 1/2008) |

|

| Making additions to accounting policies | At the moment when the additions became necessary (clause 10 of PBU 1/2008) | In the tax period when the changes became necessary (Article 313 of the Tax Code of the Russian Federation) |

NOTE! Changing and supplementing accounting policies are two different things! The changes entail the need for a retrospective recalculation of data for the years preceding the change in order to display in accordance with them incoming accounting balances and display data from previous years in mandatory accounting, while additions are needed primarily for the correct reflection of current accounting information.

What should be used to guide the formation of accounting policies?

According to paragraph 2 of Art.

8 of the Law on Accounting, an economic entity independently forms its accounting policy in accordance with federal and industry standards. Currently, only drafts of individual federal standards have been developed (for example, “Accounting Policies, Estimates and Errors”), which, even if approved, will only be applied from 2018. In this regard, an autonomous institution, when developing an accounting policy for 2021, must first of all be guided by the Law on Accounting, instructions No. 157n, 183n[3], it is necessary to take into account the industry-specific features of the institution’s structure, as well as the powers it exercises (Letter from the Ministry of Finance of the Russian Federation dated August 17, 2016 No. 02‑07‑10/48198). At the same time, as the Ministry of Finance noted in the said letter, a state (municipal) institution can formulate an accounting policy by issuing both one normative act and a set of individual normative acts.

Standards moving forward from 2021 (point by point)

The following provisions of the proposed example enterprise policy for accounting purposes have remained unchanged from previous years and continue to be applied consistently:

- preamble and paragraphs. 1–3, since the main regulatory documents, principles and assumptions for the formation of accounting policies have not changed;

- pp. 4-6, since the applied standards for accounting for inventories in these aspects have not changed;

- pp. 7-14, since the applicable OS standards in these aspects have not changed;

- pp. 15-18, since it was decided not to change the rules set out in them regarding intangible assets;

- pp. 19, 20, because the procedure for accounting for special equipment and clothing used by the enterprise has not officially changed and is still relevant for accounting purposes;

- pp. 31–34, since the organization forms and discloses reserves for doubtful debts in the reporting for accounting purposes, and the applied procedure remains relevant;

- pp. 37–41, since the organization still does not apply some accounting provisions due to the specifics of its activities and the status of a small enterprise;

- pp. 42–44, since the current procedure for recognizing and correcting errors, as well as making changes to accounting policies remains relevant;

- pp. 46–47, 49-50, since the applied procedure and forms of document flow generally remain relevant;

- clause 51, since the special procedure for the inventory of certain accounting objects used by the organization remains relevant;

- pp. 52–62, since the organization continues to use the adopted organizational procedure in terms of signature rights, internal control, document flow and the declared ability to make changes to this accounting policy.

For a version of the document approving the accounting policy, see the article “Form of the order for approval of the accounting policy” .

When and how often to approve accounting policies

The newly created organization and those that emerged as a result of the reorganization must approve the accounting policy within 90 days from the date of state registration. This document must be applied from the moment the new organization (successor organization) is created. This procedure is established by paragraph 2 of clause 9 of PBU 1/2008. At the same time, there are no penalties for violating the deadlines for approving accounting policies.

The adopted accounting policy for 2021 can and should be applied consistently from year to year (Part 5 of Article 8 of Law No. 402-FZ of December 6, 2011). That is, there is no need to approve a new document every year.

How to make changes to accounting policies?

Please note that this procedure is strictly regulated. According to paragraph 5 of Art. 8 of the Accounting Law, accounting policies must be applied consistently from year to year. Thus, the accounting policy for accounting purposes is formed only once - when the institution is created. However, the Accounting Law allows for its change when the conditions specified in paragraph 6 of Art. 8 of this law of circumstances:

- changes in the requirements established by the legislation of the Russian Federation on accounting, federal and (or) industry standards;

- development or selection of a new method of accounting, the use of which leads to an increase in the quality of information about the object of accounting;

- a significant change in the operating conditions of an economic entity.

First of all, it is necessary to pay attention to changes in legislation regulating accounting.

Thus, by Order of the Ministry of Finance of the Russian Federation dated November 16, 2016 No. 209n (hereinafter referred to as Order No. 209n), significant adjustments were made to the organization of accounting and to the procedure for reflecting certain economic and financial transactions that are subject to application when preparing financial statements for 2021, with the exception of certain provisions that apply from 2021. Having studied the existing sections of the accounting policy, the chief accountant identifies what information is missing and what requires replacement. A significant change in the operating conditions of an economic entity may be its reorganization (merger, accession, division, spin-off, transformation). Let us recall that it is carried out by decision of the founder or body of a legal entity authorized to do so by the constituent documents (Article 57 of the Civil Code of the Russian Federation). Therefore, a reasonable decision would be to make changes to the accounting policies during the reorganization of the institution.

In order to ensure comparability of accounting (financial) statements for several years, changes in accounting policies are made from the beginning of the reporting year, unless otherwise determined by the reason for such a change (Clause 7, Article 8 of the Accounting Law).

Please note that any change in accounting policy must be formalized by a directive or order from the head of the institution.

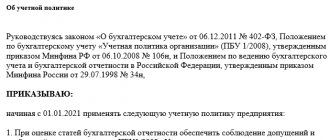

Changes that need to be taken into account if accounting for 2021 is being formed (item by item)

In the proposed example of an enterprise’s accounting policy for 2021, the following have been changed (added):

- Clause 6, 19, 21 – inventory accounting in accordance with the new FSBU 5/2019 “Inventories”.

How to apply the updated FSBU 5/2019 “Inventories” was explained in detail by ConsultantPlus experts. If you do not have access to the K+ system, get a trial online access for free.

- Paragraph 45 indicates the use of updated financial reporting forms for 2021 and the use of control ratios from the Federal Tax Service.

- Clause 48 - it includes an indication of the approval of mandatory requirements for the preparation of primary accounting documents. Let us remind you that as of June 9, 2019, the chief accountant cannot be fined for errors made in accounting due to the fault of third parties, including due to their incorrect preparation of primary documents. And from July 26, 2019, the law “On Accounting” introduced an indication of mandatory compliance with the requirements of the chief accountant (another person responsible for accounting) for the preparation of primary accounts by all employees of the organization. In this regard, it is recommended to draw up such written requirements as an appendix to the accounting policy and familiarize them with all employees involved in working with documentation, against signature.

Provisions not included in the finished document

Due to the fact that these areas of activity and accounting objects are not involved in any way in the activities of a particular enterprise, this accounting policy does not disclose the following procedures:

- recognition of revenue for work (services) with a long cycle (clause 13 of PBU 9/99, approved by Order of the Ministry of Finance of Russia dated May 6, 1999 No. 32n);

- recalculation and presentation in reporting of items denominated in foreign currency (clauses 6, 7 of PBU 3/2006, approved by order of the Ministry of Finance of Russia dated November 27, 2006 No. 154n);

- accounting for budget financing and other targeted financing (PBU 13/2000, approved by order of the Ministry of Finance of Russia dated October 16, 2000 No. 92n);

- accounting for R&D (PBU 17/02, approved by order of the Ministry of Finance of Russia dated November 19, 2002 No. 115n);

- accounting of financial investments (PBU 19/02, approved by order of the Ministry of Finance of Russia dated December 10, 2002 No. 126n).

For information on what aspects you should pay attention to if an enterprise is also developing a policy for management accounting, read the article “Accounting policies for management accounting purposes .

In what cases can accounting policies be supplemented?

Let us note that the answer to this question is not contained either in the Accounting Law or in Instruction No. 157n.

However, a mention of what is not a change in accounting policy is currently in paragraph 10 of PBU 1/2008, approved by Order of the Ministry of Finance of the Russian Federation dated October 6, 2008 No. 106n. We present this definition as reference material, since state (municipal) institutions do not use PBUs in their activities. So, according to the instructions of the Ministry of Finance presented in the said document, it is not considered a change in accounting policy to approve the method of accounting for facts of economic activity that differ in essence from facts that occurred previously, or that arose for the first time in the activities of the organization. In other words, additions to the accounting policy are made if something new appears in the activities of an autonomous institution (a new type of activity, a new type of assets, new operations, etc.), for which accounting rules are not established in it. For example, in March 2021, it is planned to open a pharmacy in the dental clinic to sell medicines and medical products. In this case, the chief accountant of the organization needs to supplement the accounting policy with methods for accounting for transactions related to retail trade (choose a method for valuing goods intended for sale (at purchase or sale prices), establish a procedure for calculating trade margins, etc.). The addition in this case can be made from the moment the institution began to engage in retail trade. Distortions in accounting in this case will not occur, since these operations did not previously take place in the activities of the institution.

Who develops accounting policies for taxation and why?

Tax legislation allows the taxpayer to choose the taxation system. In addition, to determine the tax base for some elements, different options for their application are provided. Which one to choose is up to you. The choice made must be consolidated in the accounting policy for tax purposes by order of the head of the organization (individual entrepreneur). To choose the most optimal accounting policy option for you, look at the table.

Having chosen a specific accounting policy option, it is impossible to use another taxation mechanism (determination of the Constitutional Court of the Russian Federation of May 12, 2005 No. 167-O).

There are no standard accounting policies, so draw up the order in any form. The provisions of the accounting policy can be included both in the text of the order and issued as an appendix to it.

Tax legislation does not specify who should develop accounting policies. Therefore, the head of the organization can entrust this work to any employee who is a tax specialist. As a rule, preference is given to the chief accountant.

The accounting policy is approved in advance: before the tax period, from which its provisions will be applied. Apply the developed accounting policy consistently from year to year from the moment of establishment of the organization until its liquidation. Or until changes are made to the accounting policies. There is no need to create a new accounting policy every year.