Everyone has their own reasons for uncovered losses. An uncovered loss may result from:

- excess of expenses over income for financial and economic activities and non-operating operations;

- identification of significant errors from previous years in the reporting year (subclause 1, clause 9 of PBU 22/2010);

- changes in accounting policies (clause 16 of PBU 1/2008).

The loss received in accounting at the end of the year is reflected by posting to the debit of account 84, the subaccount “Uncovered loss of the current year” and the credit of account 99 “Profits and losses”.

EXAMPLE 1. HOW THE LOSS FOR THE CURRENT YEAR IS FORMED

In the reporting year, Passive LLC received revenue from sales of products (excluding VAT) in the amount of 360,000 rubles.

The cost of products sold was RUB 290,000. The amount of other expenses is 80,000 rubles. In the reporting year, Passive accrued income tax to the budget in the amount of 15,000 rubles. Passive did not create any reserves or special-purpose funds. At the end of the year, the following data will be reflected in the financial results statement: — on line 2110 “Revenue” – 360,000 rubles;— on line 2120 “Cost of sales” – (290,000 rubles); - on line 2200 “Profit (loss) from sales” - 70,000 rubles. (RUB 360,000 – RUB 290,000);— on line 2340 “Other expenses” – (RUB 80,000);— on line 2410 “Current income tax” – (RUB 15,000);— on line 2400 “Net profit (loss)” – (25,000 rubles). The owners of the company did not make decisions on repayment of the resulting loss. When reforming the balance sheet, the following entry will be made: DEBIT 84 CREDIT 99

- 25,000 rubles. – the uncovered loss of the reporting year is written off. Line 1370 of the Liability balance sheet for the reporting year will reflect a loss in the amount of 25,000 rubles. It is indicated in parentheses.

What to do if the director and founder are one person?

If the founder himself was a director of the company, then the claim for recovery of damages from the director is sent directly to the founder, but at the same time he must perform certain actions, which include:

- Causing harm to the organization by entering into transactions for one’s own personal interests, and not in the interests of the company;

- In case of concealment of information about entering into a contractual relationship, and if this action requires the approval of other persons of the company;

- Indifferent attitude towards ongoing transactions. The director does not check the reliability of the counterparty, does not find out information about the licensing of the counterparty when such information is necessary for the transaction, and also does not take other measures aimed at obtaining the necessary information about the contract being concluded;

- Negligent or criminal actions in relation to the organization’s documentation, forgery of documents, loss or theft of documents.

If the financial savings of a legal entity are sufficient to satisfy the claims of creditors, then losses are not recovered from the founders of the business. A situation that results in compensation for losses by the LLC founder may also arise if he did not file or untimely filed a bankruptcy petition. The bankruptcy of an enterprise (company) must be declared, in accordance with Articles 9 and 224 of Law 127-FZ, within one month.

Features of the founder's liability for losses

Liability for losses to society by the founder is an important point. If the LLC does not fulfill its obligations, the founder loses part of the share or all of it. But recovery of damages from the LLC founder is possible only if his direct guilt is proven.

It should be noted that, according to a court decision, the penalty can be imposed not only on the part of the authorized capital belonging to him, but also on his personal, owned property.

While recovery of losses from a company member occurs infrequently, compensation of debts from the director almost always occurs in the event of bankruptcy of an LLC. If there is insufficient funds from the authorized share to resolve issues with debtors, the court may order additional collection of debts.

If you want to get a result that will satisfy you in all respects, you should enlist the support of the best specialists. At the same time, they should have extensive experience in the field of activity you are interested in.

Ways to “fight” losses: TOP-7

If a loss is received at the end of the reporting year, the accountant should inform the manager about the need to convene an extraordinary meeting of participants (shareholders) so that they can make a decision regarding the loss received.

The loss (both previous years and the current year) can be covered by retained earnings of previous years, reserve capital (fund) and targeted contributions from the owners of the company.

If this is not enough, an uncovered loss is left on the balance sheet.

When, at the end of the financial year following the second financial year or each subsequent financial year, at the end of which the value of the company’s net assets turned out to be less than its authorized capital, the current legislation requires, and the company is obliged to make a decision to reduce the authorized capital to the value of the net assets (clause 6, Article 35 of the Federal Law of December 26, 1995 No. 208-FZ “On Joint-Stock Companies”, paragraph 4 of Article 30 of the Federal Law of February 8, 1998 No. 14-FZ “On Limited Liability Companies”). This must be done no later than six months after the end of the relevant financial year.

Another option may be a decision to voluntarily liquidate the company. The algorithm for calculating net assets was approved by Order of the Ministry of Finance of Russia dated August 28, 2014 No. 84n.

The operation of reducing the size of the authorized capital to the value of the company's net assets is a legal way to repay the resulting loss. At the same time, the indicator of retained earnings increases.

In addition, it is possible to increase the value of the net assets themselves through contributions from the founders to the property of the company.

Write-off of losses against profits of previous years

If there is a decision to repay such a loss using the profits of previous years, you need to make an internal entry to account 84:

Debit 84 subaccount “Retained earnings of the previous year” Credit 84 subaccount “Uncovered loss of the current year”

Without the owners' decision to repay the loss, there is no reason to make an internal entry to account 84.

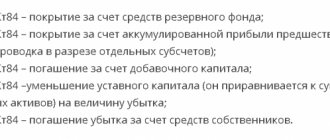

Covering losses using reserve capital

Covering the loss using reserve capital funds is reflected by posting:

DEBIT 82 CREDIT 84

— the loss of the reporting year was repaid using reserve capital funds.

EXAMPLE 2. HOW TO WRITE OFF A LOSS

AT THE ACCOUNT OF RESERVE CAPITAL As of January 1 of the reporting year, Passive LLC has reserve capital in the amount of 30,000 rubles.

and a loss in the amount of 20,000 rubles. On March 15 of the reporting year, it was decided to cover the loss using reserve capital funds. The Passive accountant must make the following entries. December 31 last year (during balance sheet reformation): DEBIT 84 CREDIT 99

- 20,000 rubles.

– reflected uncovered loss; April 15 of the reporting year: DEBIT 82 CREDIT 84

- 20,000 rubles. – the loss of the previous year was repaid at the expense of reserve capital. In the balance sheet as of the beginning of the reporting year, line 1360 “Reserve capital” will show the amount of 30,000 rubles, and line 1370 “Retained earnings (uncovered loss)” - the amount of 20,000 rub. in parentheses.

Covering losses through targeted contributions from founders

If the organization does not have sources to repay losses, then the founders of the company may decide to cover them through additional contributions.

Reflect this operation with wiring:

DEBIT 75 CREDIT 84

— the loss of the reporting year was repaid at the expense of the founders’ funds.

EXAMPLE 3. COVERING LOSSES AT THE ACCOUNT OF TARGETED CONTRIBUTIONS OF THE FOUNDERS

As of January 1 of the reporting year, the uncovered loss of Passive LLC amounted to 50,000 rubles.

The founders decided to allocate additional funds to cover the resulting loss. The funds were deposited into the company's cash desk and into its current account. The Passive accountant must make the following entries: DEBIT 50 (51) CREDIT 75

- 50,000 rubles.

– funds were received from the founders to cover the loss; DEBIT 75 CREDIT 84

- 50,000 rub. – funds were allocated to repay the losses due to the founders’ contributions.

Reduction of authorized capital

The decision to reduce the authorized capital is made at the general meeting of shareholders, which is its exclusive competence (subclause 7, clause 1, clause 2, article 48 of the Law on Joint Stock Companies).

The issue of reducing the authorized capital is within the competence of the general meeting of participants of the limited liability company (subclause 2, clause 2, article 33 of the LLC Law).

In a joint stock company, the reduction of the authorized capital is carried out by reducing the par value of the shares (without paying cash to shareholders or transferring issue-grade securities to them) (Clause 1, Article 29 of the Law on Joint Stock Companies). The total number of outstanding shares does not change.

In an LLC, the reduction of the authorized capital is carried out by reducing the nominal value of the shares of all participants in the company in the authorized capital of the company. At the same time, the size of the shares of all participants in the company does not change (Clause 1, Article 20 of the LLC Law).

The decision to reduce the authorized capital to the net asset value must be made no later than six months after the end of the relevant financial year. After making such a decision, the company must, within three working days, report this to the body that carries out state registration of legal entities - the tax inspectorate (Article 30 of the Law on Joint Stock Companies, paragraph 3 of Article 20 of the Law on LLCs).

In addition, the company is obliged to publish a notice of the decision twice (once a month) in the media, where data on state registration of legal entities is published (the dates of publication of these messages are indicated in the application for state registration of changes made to the constituent documents).

Then you need to submit a package of documents to the tax office. It includes, in particular:

- application for state registration of changes made to the constituent documents (form R13001, approved by Order of the Federal Tax Service of Russia dated January 25, 2012 No. ММВ-7-6/ [email protected] );

- decision of the meeting of owners (participants, shareholders) to reduce the authorized capital;

- changes made to the constituent documents, or constituent documents in a new edition in two copies;

- document confirming payment of the state duty (according to subparagraph 3, paragraph 1, article 333.33 of the Tax Code of the Russian Federation, its amount is 800 rubles).

The registration authority is obliged to carry out state registration of changes in the authorized capital of the company within five working days from the date of submission of documents.

The date of reduction of the authorized capital will be considered the day of making changes to the Unified State Register of Legal Entities. In the accounting registers, the decrease in the authorized capital should be reflected by posting on this date:

DEBIT 80 “Authorized capital” CREDIT 84 “Retained earnings from previous years”

As a result, society acquires a more stable financial position.

Let us also dwell on the fact that when registering a decrease in the authorized capital, the company incurs certain expenses. This:

- payment of state duty;

- payment for publications in the media;

- notarization of documents if necessary, etc.

All these expenses in accounting are classified as other expenses and are accrued by postings:

DEBIT 91-2 “Other expenses” CREDIT 68 Subaccount “state duty”

— a state fee has been charged for registering a decrease in the authorized capital;

DEBIT 91-2 “Other expenses” CREDIT 76 “Settlements with various debtors and creditors”

— costs associated with registering a decrease in the authorized capital are reflected.

EXAMPLE 4. REDUCTION OF AUTHORIZED CAPITAL TO THE VALUE OF NET ASSETS

At the end of the reporting year, the uncovered loss of Passive LLC amounted to 200,000 rubles.

The value of net assets as of December 31 of the reporting year amounted to 70,000 rubles. The authorized capital of the company is 300,000 rubles. An extraordinary meeting of the company's participants decided to reduce the authorized capital by 230,000 rubles. (from 300,000 rubles to a net asset value of 70,000 rubles) by reducing the nominal value of the shares of all participants. Registration of changes in the charter was made on May 15 of the following year. On this date, the accountant made the following entry: DEBIT 80 “Authorized capital” CREDIT 84 “Retained earnings of previous years”

- 230,000 rubles. – the authorized capital was reduced. As a result, the resulting loss was completely covered, and an indicator of retained earnings in the amount of 30,000 rubles was formed in the accounting. (RUB 230,000 – RUB 200,000).

As for tax accounting, all other expenses associated with registering a decrease in the authorized capital are taken into account when taxing profits as part of other non-operating expenses on the basis of subparagraph 49 of paragraph 1 of Article 265 of the Tax Code of the Russian Federation. Amounts by which a decrease in the company's authorized capital occurred in the reporting (tax) period, in accordance with the Tax Code, are not taken into account when determining the tax base for income tax (subclause 17, clause 1, article 251 of the Tax Code of the Russian Federation).

This means that on the date of reflection in the accounting records of a decrease in the authorized capital in the organization’s accounting, a permanent difference and a corresponding permanent tax liability arise (clauses 4, 7 of the Accounting Regulations “Accounting for calculations of corporate income tax” PBU 18/02, approved by order of the Ministry of Finance of the Russian Federation dated November 19, 2002 No. 114n), if the organization applies PBU 18/02.

This operation is reflected by the posting:

DEBIT 99 “Profits and losses” CREDIT 68 “Income tax calculations”

— a permanent tax liability has been accrued for the amount of the reduction in the authorized capital.

EXAMPLE 5. CALCULATION OF PNO WHEN THE AUTHORIZED CAPITAL IS REDUCED TO THE VALUE OF NET ASSETS

Let's use the data from the previous example.

The company applies the general taxation system and applies PBU 18/02. On the date of registration of the decrease in the authorized capital and simultaneously with the reflection of this operation in the accounts, the accountant made the following entry: DEBIT “Profits and losses” CREDIT 68 “Calculations for income tax”

- 46,000 rubles . (RUB 230,000 × 20%) – a permanent tax liability has been accrued when the authorized capital is reduced. In the income statement, this value will be reflected on line 2421.

We also note that the company has the right to reduce its authorized capital on a voluntary basis, without waiting for conditions to arise for a mandatory reduction of the authorized capital or the use of an alternative option in the form of liquidation of the company.

Investments in property

The charter of a limited liability company may provide for the obligation of its participants to make contributions to the property of the company (Clause 1, Article 27 of Federal Law No. 14-FZ of 02/08/1998).

For joint stock companies, this opportunity is provided by amendments made to Federal Law No. 208-FZ dated December 26, 1995 by Federal Law No. 339-FZ dated July 3, 2016. The contribution is formalized by an agreement between the company and the shareholder.

Contributions to property do not change the size and nominal value of the shares of company participants or shareholders in its authorized capital. The purpose of such investments is to finance and support the activities of the society.

The Ministry of Finance of Russia in its Recommendations for auditors on conducting an audit of the annual financial statements of organizations for 2021 (attachment to the letter of the Ministry of Finance of Russia dated December 28, 2016 No. 07-04-09/78875) explains that such deposits are reflected separately - on account 83 “Additional capital” .

Please note: there is no direct opportunity to use additional capital generated from participants’ contributions to directly repay losses.

However, additional capital is one of the components of equity capital. Therefore, investments in property will prevent the formation of negative net assets. EXAMPLE 6. FORMATION OF ADDITIONAL CAPITAL THROUGH CONTRIBUTIONS TO PROPERTY

The Charter of Passive LLC provides that its participants are obliged to make contributions to the property of the company.

At the end of the year preceding the reporting year, “Passive” received a loss in the amount of 120,000 rubles. The general meeting of participants made a decision to make contributions to the property in this amount (subclause 13, clause 2, article 33 of the Federal Law of 02/08/1998 No. 14-FZ). The Liability accountant will make entries: DEBIT 75 CREDIT 83

- 120,000 rubles .

– a decision was made on the amount of contributions to the property; DEBIT 51 CREDIT 75

- 120,000 rub. – participants made deposits in cash. This operation will increase the amount of additional capital on line 1350 of the balance sheet in the reporting year by 120,000 rubles.