Letters from the Federal Tax Service to help fill out the DAM in 2020

When filling out the DAM in 2021, the following explanations from the Federal Tax Service will help:

| Letter from the Federal Tax Service | How it will help |

| Letter dated 06/09/2020 No. BS-4-11/ [email protected] | Explains the procedure for filling out appendices 1 and 2 to Section 1 of the DAM by companies from industries affected by coronavirus that apply reduced insurance premium rates |

| Letter dated 04/02/2020 No. BS-4-11/ [email protected] | Clarifies how to fill out the DAM in a situation where, on the date of submission of the updated calculation, personal data (SNILS, last name, first name, patronymic) have changed |

| Explain the procedure for using tariff codes and category codes of the insured person when filling out calculations for insurance premiums by SMP subjects (before making appropriate changes to Appendices No. 5 and 7 to the Procedure for filling out DAM) |

| They explain how to fill out the DAM when several insurance premium rates are applied in the reporting period, including how many annexes to Section 1 of the DAM need to be filled out by payers of contributions ─ SMP subjects |

| Letter dated August 12, 2020 No. SD-4-3/ [email protected] | Explains the right of insurance premium payers to apply reduced tariffs under Law No. 102-FZ dated April 1, 2020, subject to the inclusion of information about them in the register of SMEs, regardless of the type of activity they carry out |

Conditions for filling out reports

RSV-1 reporting is required to be submitted to the Tax Inspectorate by all legal entities and individuals who use hired labor in their work and are payers of insurance premiums. The form and reporting procedure for RSV-1 were approved by Order of the Federal Tax Service of 2021 No. ММВ-7-11/ [email protected]

Lawyer's opinion Dmitry Ivanov Legal support center Ask a lawyer a question

This article talks about typical ways to resolve the issue, but each case is unique. If you want to find out how to solve your particular problem, call:

Or on the website. It's fast and free!

Part of the benefits for temporary disability on sick leave is paid by the employer from his own funds, the other part is compensated by the Social Insurance Fund.

If the amount of accrued benefits turns out to be less than the amount of benefits paid, then the employer has the right to receive compensation to his current account. In this case, the receipt of such compensation must be reflected in the RSV-1 reporting form.

Thus, the conditions for filling out RSV-1 reporting are as follows: the employer has the status of a legal entity or individual entrepreneur, he employs employees under an employment contract, or he engages persons for certain operations under a civil contract, he is a payer of insurance premiums.

Requirements for filling out the DAM for 9 months of 2020

They are indicated in the Procedure for filling out this report, approved. By order of the Federal Tax Service dated September 18, 2019 No. ММВ-7-11/ [email protected] :

- Calculation pages are numbered in continuous order, starting with the title page.

- Information in the RSV is entered in capital block letters from left to right.

- When filling out the calculation manually, use black, purple or blue ink.

- When filling out the RSV, the Courier New font with a height of 16-18 is installed on the computer.

- Correcting errors using putty and other corrective means is unacceptable.

- If you are creating the RSV on paper, print each sheet on a separate page.

- The printed report is not held together, not even with paper clips. It is recommended to submit it for verification in a separate file.

- In fields where there are no quantitative or total indicators, indicate “0”; in the remaining empty lines and cells, enter a dash. But if the report is filled out using a program, dashes may not be placed in empty cells.

How to submit the RSV - on paper or electronically?

There are several ways to submit the DAM for 9 months of 2021:

- On paper - if the number of employees is no more than 10 people.

If during the reporting period you paid income to a maximum of 10 employees, the calculation can be submitted both on paper and electronically.

- In electronic form - if the number of employees is 11 people. and more.

If from January to September 2021 income was paid to more than 10 employees, the DAM is submitted exclusively in the form of an electronic document signed with an electronic signature. It is sent to the Federal Tax Service via telecommunication channels (TCC) through electronic document management operators.

Who submits the payment, when and on what form?

Absolutely all employers are required to submit calculations of insurance premiums:

- Companies, their branches and separate divisions (if these separate divisions independently calculate and pay contributions) “surrender” to the Federal Tax Service at the place of registration or business (clause 7 of Article 431 of the Tax Code of the Russian Federation).

- Individual entrepreneurs and self-employed people - to the inspectorate at the place of registration (registration).

If there were no accruals during the reporting period, you are required to submit a zero calculation by filling out the required sections and applications. This will allow tax authorities to distinguish those organizations that did not have accruals from those that forgot to submit calculations (for entrepreneurs, such an obligation is not established by law).

The deadline for submitting the DAM is set by the Tax Code of the Russian Federation on the 30th day of the month following the reporting quarter. Based on the results of 9 months of 2018, you must report no later than October 30. This is a working Tuesday, and therefore there will be no rescheduling.

If the DAM is submitted 10 days later than the established deadline, the tax authorities have the right to block the current account (clause 3.2 of Article 76 of the Tax Code of the Russian Federation). The same trouble threatens the policyholder who submitted the calculation on time, but with erroneous information: the tax authorities will not accept the report, and it will be considered not submitted.

The RSV form did not change in the 3rd quarter. The calculation is still submitted in the form approved. By order of the Federal Tax Service of October 10, 2016 N ММВ-7/11/551. Let's look at how to fill it out correctly.

Composition of the DAM for 9 months of 2020

The RSV, submitted based on the results of 9 months of 2021, consists of 3 sections and 11 appendices to them. But you don't need to fill them all out. Required to be included in the calculation:

- title page;

- Section 1 “Summary of the obligations of the payer of insurance premiums”;

- subsection 1.1 of Appendix No. 1 to Section 1 “Calculation of contributions for compulsory pension insurance”;

- subsection 1.2 of Appendix No. 1 to Section 1 “Calculation of contributions for compulsory health insurance”;

- Appendix No. 2 to Section 1 “Calculation of the amounts of insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity to Section 1”;

- Section 3 “Personalized information about insured persons.”

The procedure for filling out the DAM sheets is as follows: title page, Section 3 (for each employee), appendices to Section 1, Section 1.

The remaining sheets of the RSV are filled out if necessary:

| RSV section or application | Who fills it out and in what case? |

| Section 2 and Appendix 1 to Section 2 | Included in the DAM by heads of peasant farms |

| Included in the DAM when payers apply the appropriate insurance premium rates |

| Appendices 3 and 4 to Section 1 | Included in the DAM when payers incur expenses for the payment of insurance coverage for compulsory social insurance in case of VNiM |

Unified form RSV-1 PFR in 2021: form and sample filling

- 1 – assessment of contributions occurred on the basis of desk audit reports, and prosecution occurred in this quarter;

- 2 – assessment of contributions occurred on the basis of on-site inspection reports, and prosecution occurred in this quarter;

- 3 – the employer independently identified errors and calculated the amount of contributions.

- Section 5. This section is completed only by those insurers who pay certain amounts to students working in student groups. Such payments do not require additional contributions to the Pension Fund, but certain conditions must be met: In this case, all clarifications must be accompanied by documents for personalized accounting. All documents subject to clarifications should be submitted taking into account the rules that were in force during the period in which the errors were made in the report.

- First section. This section contains information about insurance payments paid and payments that still need to be paid. Here we should highlight contributions to the Pension Fund that were accrued and paid for 2010-2013. This information is indicated in columns 4 and 5 - information on insurance and savings, respectively. And contributions to the fund from the beginning of 2014 are shown in column 3 (there is no division into the insurance and savings part). Other contributions are reflected in columns 6, 7 and 8 (for example, those for which additional tariffs apply). As for the information for 2010-2013, the first section has lines, each of which has its own purpose. So, line 100 reflects the debt until 2014. Column 3 contains data on debt or overpayment of contributions to the Pension Fund as of 2015. In the 120th line - payments that were accrued later, in 140 - fully paid contributions and in the 150th line - unpaid contributions for 2010-2013.

- Second section. Data on accrued payments and insurance deposits is displayed here. The section has three subsections that display data about additional tariffs and calculations for them. All employers enter information into subsection 2.1, but 2.2 and 2.3 are filled out only if the employee for whom the contribution was paid works in hazardous or heavy work, respectively. If insurance premiums in the period for which the report is provided were calculated at several tariffs, this section must be completed according to the number of tariffs that were applied. Information in paragraphs 2.2 and 2.3 is provided only by companies whose benefits are 6 or 4%, respectively. In general, the following factors influence the size of such benefits:

Filling out the title page

The procedure for filling out the title page of the RSV

| Line | What do they indicate? |

| TIN | TIN in accordance with the tax registration certificate. Since the TIN of legal entities is 2 digits shorter than the TIN of entrepreneurs, put dashes in the remaining cells |

| checkpoint |

|

| Correction number | If you are submitting the calculation for the first time in 2021, put “0 – -”. If you are making an adjustment, put “1- -”, “2- – ”, etc. (depending on what adjustment to the account you are submitting) |

| Settlement (reporting) period (code) | Code of the period for which the report is submitted. For RSV for 9 months we enter the code “33”. If the calculation is submitted based on the results of 9 months, but in connection with reorganization (liquidation), when deregistering an individual entrepreneur or the head of a peasant farm - code “85”. The codes for the remaining periods are indicated in Appendix No. 3 to the Filling Out Procedure (they are presented in the table below) |

| Calendar year | The year of the period for which you submit the calculation is 2020 |

| Submitted to the tax authority (code) | Code of the Federal Tax Service to which you submit the payment |

| By location (code) |

These codes are given in Appendix No. 4 to the Filling Procedure |

| “Name of organization, OP...” |

|

| Activity code (OKVED) | Employer's main activity code |

| Contact phone number | Enter in the following format: “8 space code space number.” For example: "8 917 2002010" |

| The calculation has been completed | The total number of sheets that make up the RSV. Blank pages are not included in the calculation. |

| With supporting documents attached | Fill out only if any documents are attached to the DAM: for example, a power of attorney for a representative. In other cases, dashes are placed in this line |

| Reliability and completeness... |

|

| Full name |

|

| Title of the document... | The name and details of the document on the basis of which the representative acts. For example: “Power of Attorney No. 1 dated 10/08/2020” |

A power of attorney to sign accounting and statistical reporting does not give the authorized person the right to sign the DAM. Calculation of contributions relates to tax reporting, and as a separate type of reporting must be registered in a power of attorney (Letter of the Federal Tax Service dated November 18, 2019 No. BS-4-11 / [email protected] ).

Filling out Section 3

To be completed in relation to all employees who received payments under employment and civil law contracts in the reporting period of 2021.

Procedure for filling out Section 3 of the DAM

| Line | What do they indicate? |

| 010 | Sign of cancellation of information about the insured person (indicate “1” when canceling previously submitted information about this insured person, as well as when adjusting data on lines 020-060). When filling out the RSV for the first time, this field is not filled in |

| 020-070 | Employee information: TIN, SNILS, full name, date of birth |

| 080 | Code of the country of which the employee is a citizen. For the Russian Federation - code “643”. The list of codes for other countries is given in the All-Russian Classifier of Countries of the World (OKSM). If the employee does not have citizenship, indicate the code of the country that issued him the identity document |

| 090 |

|

| 100 | Identity document code:

* See below for a complete list of codes |

| 110 | Employee's passport details. The number sign is not placed (the number is separated from the series by a space) |

| 120 | Numbers of three months of the last quarter: 1, 2, 3 |

| 130 | Insured person category code. It can be clarified in Appendix No. 7 to the Filling Out Procedure (for example, “NR” denotes persons who are covered by compulsory pension insurance, including those who are employed in a workplace with special (difficult and harmful) working conditions, for whom insurance premiums are paid according to the main tariff) |

| 140 | Monthly payment amount to employee |

| 150 | The base for contributions to compulsory pension insurance is within the limit (RUB 1,292,000 in 2020) |

| 160 | Amount of payments under the GPC agreement (if any) |

| 170 | The amount of contributions from a base not exceeding the limit of RUB 1,292,000. (for OPS) |

Block 3.2.2 is filled out only if in the reporting period of 2021 payments were made that were subject to contributions to compulsory pension insurance at an additional tariff.

If the details “TIN of an individual” in Section 3 are left blank (crossed out), tax authorities must accept such a DAM (Letter of the Federal Tax Service dated 06/04/2020 No. BS-3-11 / [email protected] ). A similar situation may arise if the employee does not have a TIN or the employer is not sure of the correctness of the available information. Let us also remind you that you can clarify the employee’s TIN using the online service on the Federal Tax Service website.

How to check the report

Before sending to the Federal Tax Service, check the RSV with form 6-NDFL. Tax officials will do the same during a desk audit. And if the values do not agree, they will ask for explanations about the reasons for the discrepancies.

For self-control, check the amount of income, excluding dividends, in 6-NDFL with the indicators on page 050 of subsection 1.1 to section 1 of the DAM form. According to the explanations of the tax authorities, the base subject to personal income tax must exceed or be equal to the base subject to insurance contributions. The formula that tax authorities rely on is given in the control ratios (CR) approved. by letter of the Federal Tax Service dated December 29, 2017 No. GD-4-11/27043

If the COPs do not agree, tax authorities may decide that the base in 6-NDFL is underestimated and the tax has not been paid in full.

But there are situations when income tax and contributions are recognized in different reporting periods, for example, if the payment is carryover.

Let's explain with an example.

The employee was paid vacation pay on Monday, October 1, and accrued on Friday, September 28. The amount of vacation pay should be included in page 050 of subsection 1.1 of section 1 of the DAM form for 9 months of 2018 (clause 1 of article 424 of the Tax Code of the Russian Federation).

In turn, the date of receipt of income in the form of vacation pay for the purpose of calculating personal income tax is the day of payment (clause 1, clause 1, article 223 of the Tax Code of the Russian Federation). Since the tax was withheld already in the 4th quarter, the amount of vacation pay will fall into the annual 6-personal income tax.

If you have a similar situation and the tax authorities ask for clarification, write a letter that there is no error, since the payment for contributions was recognized in the 3rd quarter, and for personal income tax - in the 4th.

A similar situation arises with the payment of holiday, annual and quarterly bonuses. Contributions are calculated on the day the premium is calculated, and the date of payment does not matter (letter of the Ministry of Finance dated June 20, 2017 No. 03-15-06/38515).

But for personal income tax, the date of withholding tax on bonuses (except for monthly ones) is the day of payment to the employee (letter of the Federal Tax Service dated October 6, 2017 No. GD-4-11/20217). Therefore, if a bonus is assigned in the 3rd quarter and paid in the 4th, then it will appear in the reports in different periods.

The situation is different with the monthly bonus. It is recognized as income for personal income tax on the last day of the month (clause 2 of article 223 of the Tax Code of the Russian Federation). Therefore, even if it was paid in the 4th quarter, it should be recorded in the RSV and 6-NDFL for 9 months.

Payments to “physicists” under the GPC agreement are also recognized as transferable. For contributions, the date of accrual of remuneration is important, and for personal income tax - the day of payment. They may fall on different reporting periods and, therefore, be reflected in different reports.

The difference may also arise due to different approaches to calculating personal income tax and contributions.

For example:

| Type of income | Personal income tax | Contributions |

| Cash gifts | Personal income tax is calculated on amounts exceeding 4 thousand rubles. (Clause 28, Article 217 of the Tax Code of the Russian Federation) | Gifts for the purposes of calculating insurance premiums are not considered income, regardless of the amount, and are not reflected in the DAM (letter of the Ministry of Finance dated January 20, 2017 No. 03-15-06/2437) |

| Compensation for delayed wages | Not subject to personal income tax (clause 3 of article 217 of the Tax Code of the Russian Federation) | It’s safer to charge contributions: officials insist on this (letter from the Ministry of Finance dated March 21, 2017 No. 03-15-06/16239) |

If the tax authorities ask questions, in an explanatory letter write down a list of payments from which contributions and income tax were calculated differently. To exclude possible claims, we recommend providing a detailed justification with references to letters from officials and norms of the Tax Code of the Russian Federation.

We fill out subsection 1.1 of Appendix No. 1

Rules for filling out subsection 1.1 of Appendix No. 1 of the RSV

| Line | What do they indicate? |

| 001 | Contribution payer tariff code. You can find it in Appendix No. 5 to the Filling Out Procedure. |

| 010 | From left to right - the total number of insured employees, regardless of whether they received income in the reporting period:

|

| 020 | From left to right - the number of employees who were paid income subject to compulsory pension contributions:

|

| 021 | If during the reporting quarter the employee's income exceeded the maximum base for contributions, show their number in the columns of this line. In 2021, the maximum base for contributions to compulsory pension insurance is RUB 1,292,000. |

| 030 | The amount of payments to employees subject to contributions to compulsory pension insurance:

This line does not include payments that are not subject to insurance premiums: dividends, material benefits, payments under lease agreements or upon the sale of property (Letter of the Federal Tax Service dated 08.08.2017 No. GD-4-11 / [email protected] , Letter of the Ministry of Health and Social Development dated 19.05 .2010 No. 1239-19). |

| 040 | If any payments during the year were not subject to contributions to compulsory pension insurance, they are reflected in the columns of this line in the same order as we reflected contributions on page 030 |

| 045 | This line shows the amounts:

|

| 050 | Contribution base for 9 months and July-September 2021. It is calculated using the formula: page 030 - page 040 - page 045 |

| 051 | Contribution base exceeding the maximum limit |

| 060 | The amount of calculated insurance premiums, calculated according to the formula: line 050 x tariff. Page 060 = page 061 + page 062 |

| 061 | The amount of insurance premiums calculated for 9 months of 2021 from a base not exceeding the limit of RUB 1,292,000. Calculated using the formula: (050 - 051) x tariff |

| 062 | The amount of contributions calculated from a base exceeding the limit. Calculated using the formula: line 051 x per tariff |

How to pass 4-FSS on direct payments

They planned to update Form 4-FSS in 2021, and even prepared a new report form. But it was not accepted in the first quarter and most likely will not be accepted until the end of 2021. Therefore, we report according to the old form, approved by order of the Social Insurance Fund dated September 26, 2016 No. 381.

How to fill out 4-FSS according to the new rules

Previously, in Table 3 we described the costs of insurance against industrial accidents and occupational diseases. Now it is not relevant, you don’t have to fill it out.

Another place to reflect expenses is line 15 of Table 2. Now you don’t need to fill it out either, just enter zeros or dashes.

Compensation for injury benefits and other expenses received from the Social Insurance Fund for periods before January 1, 2021 are reflected in line 6 of Table 2.

Since the credit system does not work, in 4-FSS we immediately show contributions payable. In Table 2, accrued contributions are indicated in line 2, paid - in line 16. Indicate arrears of contributions at the end of the first quarter in line 19. Debt for the Social Insurance Fund at the end of the period can now only appear if you have overpaid contributions.

Prepare and pass 4-FSS for free via the Internet

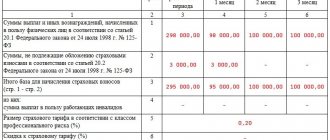

Filling example . The organization pays contributions for injuries at a minimum rate of 0.2%. For January, February and March, employees were awarded 400 rubles. As of January 1, 2021, the policyholder had a debt of 264.30 rubles.

Table 2 of the 4-FSS calculation will be filled out as follows:

Sample 4-FSS for the 1st quarter of 2021 on direct payments. table 2

What benefits should be reflected in 4-FSS

As in the RSV, only sick leave for the first three days of illness of employees and additional days off to care for disabled children will need to be included in 4-FSS. Sick leave from the fourth day, maternity and child benefits are paid by the FSS - there is no need to show them in the report.

Sick leave for the first three days of illness should be reflected in the total amount of payments in line 1 of Table 1. Since they are not subject to contributions, they will also be included in line 2 of Table 1.

Payment of additional days off to parents of disabled children falls into lines 1 and 3 of Table 1, as it forms the basis for calculating contributions. Funeral benefits do not fall into 4-FSS.

We fill out subsection 1.2 of Appendix No. 1

Subsection 1.2 includes data on compulsory medical insurance contributions. Fill it out in the same order as subsection 1.1. Since there is no maximum base for health insurance contributions, it is easier to fill out than the previous one.

If you still have questions about filling out the RSV, you can find answers to them in ConsultantPlus.

Full and free access to the system for 2 days.