You need to report on insurance premiums in 2021 to the Federal Tax Service, and not to extra-budgetary funds. Tax authorities have developed a new calculation form that replaces the previous 4-FSS and RSV-1 calculations; it must be applied starting with reporting for the 1st quarter of 2021. The form and instructions for filling out the calculation were approved by Order of the Federal Tax Service dated October 10, 2016 No. ММВ-7-11/551. In addition, new BCCs are now used to pay insurance premiums.

Read more about the new form, as well as the procedure for filling it out with an example, in this article.

The procedure for submitting the calculation of insurance premiums in 2021

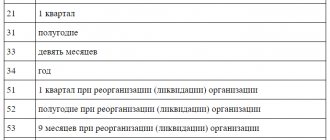

Organizations and individual entrepreneurs with employees must submit a new single calculation to the Federal Tax Service on a quarterly basis. The last day for submitting calculations is the 30th day of the month following the reporting period (clause 7 of Article 431 of the Tax Code of the Russian Federation). The first report on the new form must be submitted no later than May 2, 2021, due to the postponement of dates due to the May holidays.

With an average number of more than 25 people, a single calculation must be submitted only in electronic form; others can submit it on paper. Please note that the due date for premium calculations from 2021 onwards is now the same for all policyholders, regardless of how they submit the calculation.

Important: the calculation is considered not submitted if the total pension contributions for each employee do not coincide with the total amount of Pension Fund contributions. After receiving notification of this from the Federal Tax Service, the policyholder has 5 days to eliminate the error, otherwise a fine cannot be avoided.

Reasons for the changes?

“Raschet” asked Pavel Kurlat, partner of the First Legal Network, to answer the question: why does the state need changes in the procedure for collecting and monitoring insurance premiums? Is the main goal to increase fundraising?

“This change has been discussed for a long time. It is expected that the adoption of new amendments to legislation will reduce the administrative burden on business by reducing the number of regulatory bodies, reducing unnecessary bureaucracy and optimizing reporting. How this will look in practice, only time will tell.

note

Taking into account how poorly our interdepartmental exchange of information is, at the beginning of 2021, there will most likely be problems in the relationship between funds, tax authorities and payers in the transfer of data on the amount of insurance premiums, their payment and all related mutual settlements.

I believe that the change in the procedure for collecting insurance premiums in 2017 serves several purposes. But first things first. I think that the reform is dictated by the need to increase the state’s collection of funds for social insurance. Apparently, funds are not able to cope with such a task on their own. In general, it should be noted that despite the reform, the amount of taxes paid will not change. As employers paid insurance premiums, so they will pay – both LLCs and individual entrepreneurs. Only now almost all payments will be made to the Federal Tax Service at the place of registration of the business.”

Read also “How to pay insurance premiums correctly and report in 2017”

How to fill out the Calculation of insurance premiums in 2021

The calculation consists of a title page and three sections. In turn, sections 1 and 2 include applications: in section 1 there are 10 of them, in section 2 there is only one application. All policyholders are required to submit the following parts of the Calculation:

- Title page,

- Section 1, containing summary data on insurance premiums payable to the budget,

- Subsection 1.1 of Appendix No. 1 of Section 1 – calculation of pension contributions,

- Subsection 1.2 of Appendix No. 1 of Section 1 – calculation of compulsory medical insurance contributions,

- Appendix No. 2 of Section 1 – calculation of social insurance contributions in case of temporary disability and in connection with maternity,

- Section 3 – personalized information about insured persons.

The remaining subsections and annexes are presented if there is data to fill them out.

The calculation is completed in rubles and kopecks. In unfilled cells, dashes are added. All words in the Calculation lines are written in capital letters. The detailed line-by-line procedure for filling out the Calculation was approved by order of the Federal Tax Service of the Russian Federation dated October 10, 2016 No. ММВ-7-11/551.

Let's look at how to calculate insurance premiums in 2021 using the following example.

In the 1st quarter of 2021, Alpha LLC accrued insurance premiums from payments to 1 employee, who is also the manager. The organization works on the simplified tax system and applies the basic tariff of insurance premiums.

Contributory payments to Mikhailov I.P. amounted to 30,000 rubles monthly. In January-March, insurance premiums were charged for each month:

Pension Fund (22%) - 6600.00 rubles each, compulsory medical insurance (5.1%) - 1530.00 rubles each, social insurance (2.9%) - 870.00 rubles each.

The total amount of payments to Alpha LLC for the 1st quarter: 90,000 rubles.

The total amount of contributions of Alpha LLC for the 1st quarter: Pension Fund (22%) - 19,800.00 rubles, compulsory medical insurance (5.1%) - 4590.00 rubles, social insurance (2.9%) - 2610.00 rubles.

It will be more convenient to fill out the sections for calculating insurance premiums in 2021, the example of which we are considering, in the following sequence:

- First, fill in the personalized information in section 3 . This section is completed for all insured persons and includes information for the last 3 months. In our case, the information is filled in for one employee, but if there are more insured persons, then the amount of information in the Calculation must correspond to their number.

- The next step is to fill out subsection 1.1 of appendix 1 of section 1 on pension contributions: we summarize and transfer here the accounting data from section 3. Remember that all indicators of personalized information in total must coincide with the indicators of subsection 1.1. Our example is simplified and there is only one employee, so we simply transfer his indicators from section 3.

- Next, fill out subsection 1.2 of Appendix 1 of Section 1 on contributions to compulsory medical insurance. Indicators of insurance premiums for health insurance are reflected only in this section of the Calculation.

- Social insurance premiums are calculated in Appendix 2 of Section 1 . If there were social insurance expenses (sick leave, benefits) during the billing period, then this should be reflected in Appendix 3 to Section 1, which means line 070 of Appendix 2 of Section 1 should be filled in. In our example, there were no such expenses, so Appendix 3 is not fill it out.

- Having filled out the sections for each type of contribution, we fill out the summary section 1 . The amount of insurance premiums payable to the budget is indicated here. Please note that the BCC indicated on lines 020, 040, 060, 080 and 100 have not yet been approved for 2021, so in our example the codes for 2021 are indicated, in which the first 3 digits are replaced by 182, which means payment to the Federal Tax Service.

- In conclusion, we number all completed Calculation sheets and indicate their number in a special line on the Title Page. Under each section we will put the signature of the head and the date.

RSV for the 3rd quarter of 2021: sample filling

A large number of policyholders fill out insurance premium calculations using various accounting programs or online services. In this case, the calculation is generated automatically based on the data that the policyholder enters into the program. However, it is necessary to understand a number of basic principles of calculation formation in order to eliminate possible errors.

Below is a sample RSV with explanations of the features of filling out the most common sections.

You can download a sample of filling out a calculation of insurance premiums for the first quarter of 2021 or download a form for calculating insurance premiums for the 3rd quarter of 2021 in Excel using the links provided at the end of the article.

Change of department

The process of transferring taxpayer cases from the Pension Fund of the Russian Federation and the Social Insurance Fund to the tax authorities’ databases began in October 2021, but has not yet been completed.

“In this regard, I believe there is a possibility that taxpayers will be faced with insufficient data from the Federal Tax Service regarding the availability of submitted reports and the amounts of previously paid insurance premiums,” says Yulia Rybalko, “In order to avoid further proceedings on this issue not only with extra-budgetary funds, but and with fiscal authorities, I recommend that companies make a reconciliation with extra-budgetary funds by the end of 2021. Since reporting will be provided directly to tax authorities in 2021, the rules established by fiscal legislation will apply to them when conducting audits. In turn, the Social Insurance Fund will retain the obligation to carry out checks regarding compulsory insurance costs.

In this regard, companies should take into account that the same tax period can be checked twice - both by the Service and by the Social Insurance Fund. The Pension Fund of Russia will retain the obligation to verify only in relation to personalized accounting, i.e. verification will remain only in relation to the information that companies indicate monthly in the SZV-M form.

To date, the mechanism for inspections by the Federal Tax Service has been developed and well established. As practice shows, it does not fail, and therefore the number of detected inconsistencies, inaccuracies, and errors in reports provided by taxpayers will be significantly higher than it was during audits by extra-budgetary funds.

Read also “Federal Tax Inspections: a new approach”

To be fair, it is worth noting that over the past couple of years, extra-budgetary funds have begun to master the methods of their tax colleagues when conducting audits, however, starting from 2017, insurance premium audits will reach a new level and will be carried out more often and more strictly.”

Possible problems

Studying the text of the law gives the impression that funds and the tax office will be forced to exchange a large amount of information with each other. However, given how poorly our interdepartmental exchange of information is, at the beginning of 2021, there will most likely arise possible problems in the relationship between funds, tax authorities and payers in the transfer of data on the amount of contributions, their payment and all related mutual settlements. In this regard, it can be predicted that the workload on the courts will increase in connection with taxpayers challenging the actions of the tax service. “It seems to me that some confusion in payments at the beginning of the year is inevitable. Not all entrepreneurs in our country follow changes in legislation so closely. Much will depend on the actions of the funds themselves and the tax service, which need to be given more complete advice on the procedure for paying insurance premiums,” sums up Pavel Kurlat.

Conceptual approach

“Another thing is that the tax service has much more opportunities and practical experience in how to most effectively collect debts,” continues Pavel Kurlat. “I think in this case the total number of collected fees will only increase. In addition, this corresponds to the conceptual approach to reforming the financial management system in our state. In the recent past, several supervisory authorities in the field of control were liquidated with the transfer of functions to the mega-regulator - the Central Bank of the Russian Federation. The situation is the same here - the transfer of several similar functions from several entities to a single “tax agent”. This, ultimately, should provide greater opportunities for the government to mobilely accumulate and operate public finances, simplifying the procedure and guaranteeing higher efficiency in the collection of taxes and mandatory payments. Moreover, there is an obvious tendency towards tightening tax discipline for all categories of payers in the context of a shrinking tax field.”

Read also: “Mistakes by tax agents”

What awaits entrepreneurs

At the request of “Raschet”, Yulia Rybalko, a leading specialist in legal payroll calculations, told us what to expect for companies and entrepreneurs after the adopted changes, how the inspection procedure will change and how much the amounts of additional charges can increase?

“As for the procedure for checking accruals, the reports provided for the year 2021 inclusive will be checked by extra-budgetary funds for the correctness and correctness of the calculations. Starting from the results of the first quarter of 2021, the reporting will be checked by the tax authorities.

In my assessment, companies should expect an increase in desk audits from the Social Insurance Fund related to reimbursement of employer expenses paid for sick leave. The increase in inspections will be due to the fact that tax authorities will transmit information on declared expenses in quarterly reports to the territorial body of the Social Insurance Fund. I believe that insurance costs will be checked through desk or even on-site audits.”

Read also “Desk and field tax audits”