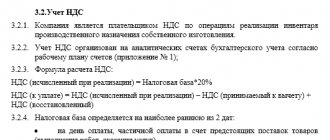

Accounting for furniture in an organization has its own characteristics. The concept of “furniture” is quite broad. Let's consider the issues of purchasing and writing off office furniture - tables, chairs, cabinets, etc., as well as accounting for furniture in the accounting records of an enterprise.

Also see:

- What applies to office equipment

- Is the computer the main tool

Receipt of equipment in 1C Accounting

To complete this operation, use the document of the same name “Receipt of Equipment”.

The list of documents is located in the “Receipt of fixed assets” section (main menu “Fixed assets and intangible assets”). You can go to the list by clicking on the “Equipment Receipt” link. In the list window, click the “Create” button. Now you can proceed to filling out the document details.

- We indicate the date and number of the primary document, the date of the document in the system. The number will be assigned automatically upon registration.

- If this information base maintains records for several organizations, select the organization. If the “Organization” field is missing in the document header, it means that records are kept for only one organization. This is a common feature for all documents.

- The selection of a counterparty can be made by TIN or by name. If it is not found in the directory, the program will offer to create it.

- If the counterparty already exists and an agreement with the “With supplier” type has been concluded with it, the agreement will be entered automatically.

Now let's move on to filling out the tabular part. On the first tab we indicate:

- Equipment that we come;

- Quantity;

- Price;

- VAT rate;

- Accounting account (usually 04/08).

Don't forget to create an invoice below.

On the “Products” tab, you can specify related products. They arrive as usual.

The “Services” tab indicates services that are not included in the cost of the equipment. For example, services related to the delivery of goods.

To reflect the services that need to be included in the cost of equipment, there is a document “Receipt of additional. expenses."

Go to the list of additional documents. expenses can also be found in the “Receipt of fixed assets” section.

The header of the document is filled out in the same way as the receipt document.

On the “Main” tab fill in:

- Name );

- Amount and rate of VAT;

- a method for allocating costs if they relate to several items of equipment.

As you can see, the amount of additional expenses increased the cost of the machine.

Requirements for depreciation groups

Each enterprise uses in its work various fixed assets that are its property and are used in the production of goods, provision of services, and performance of work. To accept them for accounting, the initial cost is determined. Accounting during use is carried out at residual value.

Regardless of the form of ownership of the company, its size and types of activities, the issue of efficient use of fixed assets is one of the paramount ones. The competitiveness of the company's products, its position in industrial production, and the financial condition of the organization depend on it. Therefore, the use of OKOF is especially important.

Office furniture accounting

Accounting for office furniture is a responsible undertaking. To carry it out, a competent approach is required. Typically, updating and purchasing new furniture is carried out in small batches. Today a company can buy a cabinet, and a month later get new chairs.

In some situations, office furniture and office equipment may also be subject to depreciation. If the object is part of the OS, the procedure is required. Determining the group to which the property belongs can help determine the depreciation period. To obtain the information of interest, you need to contact the classifier. Office furniture belongs to group 4. Its period of use ranges from 5 years 1 month to 7 years inclusive.

If an accountant turns to a classifier in order to find out the group that includes office equipment, he will not be able to solve his problem. The type of property is not included in the document. According to the established rules, if an object is not on the list, its useful life is established based on the manufacturer’s recommendations (Article 258 of the Tax Code of the Russian Federation). To do this, you need to read the documentation accompanying the purchased item.

We suggest you read: How to return furniture of proper quality

Legal requirements

According to the provisions of Article 163 of the Labor Code, the employer is obliged to provide employees with normal working conditions. These, in particular, include working conditions that meet labor protection and production safety requirements. Moreover, Article 223 of the Labor Code determines that the provision of sanitary, medical and preventive services for workers in accordance with labor protection requirements is the responsibility of the employer. In connection with this management, companies are equipped according to established standards with:

- sanitary facilities;

- premises for eating;

- premises for medical care;

- rooms for rest during working hours and psychological relief;

- sanitary posts with first aid kits stocked with a set of medicines and preparations for first aid; and also devices (devices) are installed to provide workers in hot shops and areas with carbonated salt water, etc.

The requirements for creating rooms for eating are established by sanitary standards. They are contained in paragraphs 5.48–5.51 of the Code of Rules SP 44.13330.2011 “Administrative and domestic buildings. Updated version of SNiP 2.09.04-87”, approved by order of the Ministry of Regional Development of Russia dated December 27, 2010 No. 782 (hereinafter referred to as the Rules). What requirements do the Rules impose on catering at work?

Thus, the Rules stipulate that when designing production enterprises, canteens should be provided, designed to provide all workers with general, dietary, and in some cases, therapeutic and preventive nutrition.

When there are hundreds of mines with more than 200 people per shift, it is necessary to provide a canteen that operates on semi-finished products, and when there are up to 200 people, a canteen-distributing area must be provided. When the number of workers in the largest shift is up to 30 people, a room for meals should be equipped.

In accordance with paragraph 2.52 of these Rules, the eating area must have a washbasin, a stationary boiler, an electric stove and a refrigerator. We believe that the boiler can be replaced with an electric kettle, and the electric stove with a microwave oven.

If the company employs up to 10 people per shift, then instead of a meal room, an additional space of 6 square meters should be provided in the dressing room. m with the installation of a table for eating.

Equipment decommissioning

Almost all office equipment objects are classified as means of mechanization. The service life of such items is more than 1 year. Typically, office equipment is taken into account as part of the operating system. During manipulations, the actual value of the property is taken into account.

Reflection of objects in accounting occurs on the basis of the acceptance certificate, which was drawn up in advance. The paperwork is completed using form 0504101. According to the new rules, today it is not necessary to draw up a similar act to account for office equipment. However, upon receipt of new property, the institution must draw up an order for the acceptance of material assets. The document is often used as the basis for recording office equipment in accounting.

The company must exercise control over the furniture that is on its balance sheet. All activities carried out for this purpose must be carried out in accordance with the company's accounting policies. In addition, the accountant must be familiar with the provisions of PBU 5/01 and PBU 6/01.

Features of furniture write-off depend on its value. If the price of an object is more than 40,000 rubles, and the period of use exceeds 1 year, the property is recorded on account 01. The original cost of the items is taken into account. When performing the write-off procedure, you will have to make the following entries:

- Dt 91 Kt 01 (residual value).

- Dt 02 Kt 01 (wear).

- Dt 10 Kt 99 (capitalization of material assets upon liquidation).

- Dt 91 Kt 99 (income from disposal).

- Dt 99 Kt 91 (loss on disposal).

Property included in this category can be written off as expenses at once. The result of the write-off is the execution of the corresponding act. It is compiled by a special commission, which includes officials working in the organization.

For various reasons, equipment may be written off. The reasons may be different and are indicated arbitrarily for printing the act. Completing the document does not require any special explanation.

Depreciation is charged at the end of the month through the month-closing transaction. Based on the parameters specified when accepting equipment for accounting, the program will automatically calculate the amount of depreciation. Depreciation begins to accrue from the next month after receipt.

After completing the operation, by clicking on the link marked in the figure, you can view the details.

Carrying out accounting of office equipment

Almost all office equipment objects are classified as means of mechanization. The service life of such items is more than 1 year. Typically, office equipment is taken into account as part of the operating system. During manipulations, the actual value of the property is taken into account.

Reflection of objects in accounting occurs on the basis of the acceptance certificate, which was drawn up in advance. The paperwork is completed using form 0504101. According to the new rules, today it is not necessary to draw up a similar act to account for office equipment. However, upon receipt of new property, the institution must draw up an order for the acceptance of material assets. The document is often used as the basis for recording office equipment in accounting.

Note! From the month that follows the period when office equipment is included in accounting, depreciation begins to accrue. The action is carried out until the full cost of the property is paid off or its disposal occurs.

Tax accounting of costs for the purchase of furniture

If the company is on the simplified tax system, all property worth less than 40,000 rubles. and is used for more than 1 year, refers to material costs (Article 257 of the Tax Code of the Russian Federation). The company has the right to write it off as costs under the “simplified procedure”. The basis for carrying out such manipulation is Article 346.16 of the Tax Code of the Russian Federation. However, the accountant must take into account Article 254 of the Tax Code of the Russian Federation.

Furniture and office equipment that cost less than 40,000 rubles are classified as low-value property. If the company incurred expenses for the purchase of items belonging to this category, the accountant has the right to reflect them in the “Income and Expenses Accounting Book” immediately after payment. There is no need to wait until the property is put into operation (Article 346.17 of the Tax Code of the Russian Federation).

We invite you to familiarize yourself with: Balance sheet form 1 and 2 completed by the enterprise

Attention! If a company makes contributions to the state under the simplified tax system, only reasonable costs can be taken into account. The category includes expenses necessary to carry out business activities.

Example 1. The Iskra company is on the simplified tax system and makes payments based on the income-expenses system. In January 2021, the organization decided to purchase a cabinet, the cost of which was 5,000 rubles. The company put the purchased property into operation and took it into account as a material value. An example of an entry that will need to be made in the “Account Book...” is presented below.

| № | Date and number | Content | Income | Expenses |

| 1 | Cash receipt dated January 15, 2017 No. 01234567, commissioning certificate dated January 15, 2017 No. 1 | The cost of the cabinet is reflected in the costs | – | 5000 rub. |

Fixed assets in accounting and tax accounting, main changes in 2021

- Starting from January 1, 2021, some changes were made to the Tax Code of the Russian Federation, Art. 259.3, clause 1 - expanded the list of equipment operated under the best available technologies. This equipment is depreciated with an increasing factor of two.

- A new list of equipment for accelerated depreciation was approved in accordance with Government Decree No. 622-r 04/07/2020.

The activities of a business entity involve the use of property with a long time of use in the production process. Since such accounting objects have a long time of use and a significant price, there are some features of how they are reflected both in accounting and in tax accounting. Let's take a closer look at how fixed assets are indicated in accounting and tax accounting in 2020.

We recommend reading: What is needed to build a house on a Snt site

Acceptance of equipment for registration

After registration of receipt, the equipment must be accepted for accounting.

From the same section, go to the document list form “Acceptance for accounting of fixed assets” and click the “Create” button.

Let's start filling out the document details:

- “OS event” – we indicate how we will accept the equipment for accounting, with commissioning or not. Affects generated wiring;

- “MOL” – indicates the materially responsible person to whom the equipment will be assigned;

- “Location of OS” is the division for which equipment records will be kept.

On the “Fixed Assets” tab, select an equipment card, which must first be entered into the “Fixed Assets” directory.

This directory stores all information about fixed assets. For the most part, the equipment card is filled out automatically when you post this document. It stores information about the initial and current cost of equipment, accrued depreciation, and reference information. The data is taken from the document. When a document is changed, the data in the directory also changes.

If the company pays income tax, the “Tax Accounting” tab is also filled out. As a rule, it contains the same values as in the previous tab.

It can be seen that the equipment was registered on account 01.01.

Furniture Belongs to Fixed Assets in 2020

- The purpose of the object is to use it in the production process, when performing work or providing services, for management purposes, as well as providing it for temporary use or possession for a certain period of time for a fee.

- The enterprise or organization does not intend to further resell the object.

- The object can be used for a long period (more than 12 months or an operating cycle exceeding 12 months).

- The object has the potential to bring economic benefits to the organization (enterprise) in the future.

Changes have been made to the classifier - a new OKOF will be introduced in 2021 (OK 013-2014 (SNA 2008)). Let us recall that OKOF is a classifier of fixed assets, that is, all property classified as fixed assets. In connection with these changes, the classifier of fixed assets will also change, since the first column of the classifier table contains OKOF codes.

Nuances of accounting for purchased furniture

Features of accounting for furniture and office equipment depend on the price of the property and the period of its commissioning. Before proceeding to further manipulations, it is necessary to determine which category the purchase belongs to - OS or MPZ.

We suggest you familiarize yourself with: Law on Consumer Rights Return of Furniture

The amount of funds on the basis of which an object is assigned to one or another classification differs for accounting and tax accounting. If in the first case, in order to be classified as fixed assets, an item must cost at least 40,000 rubles, then in the second situation, depreciation is carried out on property whose price exceeds 100,000 rubles.

Not all office equipment and inventory can be taken into account when writing off expenses. So, if there are no complaints about the purchased furniture, then the inclusion of some equipment in the documentation may raise questions among tax inspectors.

| Property that was purchased | Is it possible to write off expenses using the simplified tax system and OSNO? |

| Furniture objects | There will be no problems |

| Technology to make office work easier | Write-off possible |

| Air conditioners and heaters | The company works according to OSNO - there will be no problems The company works according to the simplified tax system - expenses are canceled |

| Kitchen appliances | According to OSNO - accounting for expenses is allowed According to the simplified tax system - expenses are not included in the list of permitted ones |

What applies to fixed assets in 2020

In accounting and tax accounting, the limit on the value of assets is different. From 2021, the tax accounting limit has been increased, and new amendments are expected in accounting. Read this article to see what the main limit will be for the year. intended for the manufacture of goods, provision of services or work; period of use – more than 12 months; objects are not for resale to contractors; The goal is to bring benefits to the company.

No. 03-03-06/1/66200 recalled that changes have been made to the Classification of fixed assets included in depreciation groups, which apply starting from January 1, 2021. The taxpayer has the right to increase the useful life of an asset after the date of its commissioning in if, after reconstruction, modernization or technical re-equipment of such an object, its useful life has increased.

Documents required for registration

Furniture accounting is a relatively complex process. During its implementation, it is impossible to do without filling out the appropriate documentation. To make the work of accountants easier, Goskomstat has developed standardized paper forms. They can be used to account for inventories. In addition to standardized forms, ready-made cards may be useful to an accountant. They are intended for registration of low-value property. An accountant may use the following forms:

- accounting card No. MB-2;

- disposal act No. MB-4;

- write-off act No. MB-8.