The legal topic is very complex, but in this article we will try to answer the question “Access control system depreciation group 2021.” Of course, if you still have questions, you can consult with lawyers online for free directly on the website.

telephone apparatus and special devices, payphone apparatus and radiotelephones; subscriber unit of compaction equipment; equipment for multiplexing subscriber lines; Smart Service Control Node (SCP); service border router (BRAS/BNG/BSR); optoelectronic interface converter; batteries at communication facilities; uninterruptible power supplies - third group

(property with a useful life of more than 3 years up to 5 years inclusive)

OKOF-2 (as amended on 05/08/2021, taking into account changes came into force on 07/01/2021) All-Russian classifier of fixed assets OK 013-2021 (SNA 2021) came into force on January 1, 2021 to replace OKOF OK 013-94 For To convert the OKOF code to the OKOF2 code, use the OKOF to OKOF2 code converter.

320.26.30.11.190

automatic and semi-automatic telephone stations; automatic and semi-automatic intercity and international telephone stations - sixth group

(property with a useful life of over 10 years up to 15 years inclusive)

The All-Russian Classifier of Fixed Assets (OKOF), which determines the depreciation group of fixed assets, remains unchanged. From January 1, 2021, OKOF OK 013-2021 (SNS 2021), approved by Rosstandart order No. 2021-st dated December 12, 2021, is in effect. The same classifier will be in effect in 2021.

What is ACS

ACS: what is it - a common question for owners of office buildings or private areas. A control system is one of the security elements that is created on the basis of technical devices and electronic systems combined into one network. The security enhancement element runs on specially developed software (software). The ACS access control and management system also allows you to automate the recording of working hours in any organization.

Important! Thus, an access control system on the Internet or offline allows you to increase the security of the building and make the work of security and personnel easier.

Rationale

Depreciable property is property with a useful life of more than 12 months and an original cost of more than 40,000 rubles (clause 1 of Article 256 of the Tax Code of the Russian Federation). Based on paragraph 1 of Art. 258 of the Tax Code of the Russian Federation, depreciable property is distributed among depreciation groups in accordance with its useful life. The useful life is the period during which an item of fixed assets (fixed assets) serves to fulfill the goals of the taxpayer's activities. The useful life is determined by the taxpayer independently on the date of commissioning of this depreciable property in accordance with the provisions of Art. 258 of the Tax Code of the Russian Federation and taking into account the Classification of fixed assets included in depreciation groups (hereinafter referred to as the Classification), approved by Decree of the Government of the Russian Federation dated January 1, 2002 N 1. When assigning an asset to a depreciation group according to the Classification, one should be guided by the All-Russian Classifier of Fixed Assets OKOF (OK 013 -94), approved by Decree of the State Standard of Russia dated December 26, 1994 N 359. For those types of fixed assets that are not indicated in depreciation groups, the useful life is established by the taxpayer in accordance with the technical conditions or recommendations of the manufacturers (clause 6 of Article 258 of the Tax Code of the Russian Federation) . Similar clarifications are contained in letters of the Ministry of Finance of Russia dated January 25, 2021 N 03-03-06/1/21, dated November 16, 2009 N 03-03-06/1/756. If the technical passport of the manufacturer or other similar technical documentation does not indicate the useful life of the fixed asset, then, if possible, you should contact the manufacturer with a corresponding request. In the absence of any information about the useful life of the installed video surveillance system, we consider it possible to be guided by the following. An analysis of arbitration practice indicates that when resolving disputes, the subject of which was the question of whether a video surveillance system belongs to one or another depreciation group, the courts recognize the inclusion of this system in the fourth depreciation group as justified (see, for example, the decisions of the Federal Antimonopoly Service of the North-Western District dated 11.02 .2008 N A56-14866/2007; Eighteenth Arbitration Court of Appeal dated March 29, 2021 N 18AP-12884/11). Previously, there was an opinion that video surveillance systems can be classified as a group of photographic and cinematic equipment (code 14 3322000) under code 14 3322162 “Land-field surveillance, tracking, photo and cinematic recording equipment”. According to the Classification, such equipment is included in the fifth depreciation group with a useful life of 7 to 10 years. However, the resolution of the Ninth Arbitration Court of Appeal dated 01.03.2021 N 09AP-278/2021 states that the video surveillance system used to protect the premises (building) cannot be classified as equipment for field surveillance, tracking, photo and film recording. The same resolution contains a conclusion on the legality of assigning the video surveillance system to the third depreciation group. It should be recognized that in this case the taxpayer could confirm the established service life of the object with the technical conditions and recommendations of the manufacturers. Taking into account the above, we believe that the video surveillance system can be classified in the fourth depreciation group - property with a useful life of more than 5 years up to 7 years inclusive, under OKOF code 14 3230000 “Television and radio receiving equipment” or under code 14 3221137 “Video recording and playback equipment general use." In this case, the depreciation group of the fixed asset and its useful life must be approved by a local act (order or directive of the head of the organization.

More to read —> UFMS Yaroslavl Details for Paying the State Duty for Changing a Passport

Service life of CCTV camera

Reflect the property as part of fixed assets in the amount of .19 rubles. VAT in the amount of 40.81 rubles. The article of the Civil Code of the Russian Federation states that under a contract, one party, the contractor, undertakes to perform certain work on the instructions of the other party, the customer, and deliver the result to the customer, and the customer undertakes to accept the result of the work and pay for it. Unless otherwise provided by the contract, the work is performed at the expense of the contractor - from his materials, with his forces and means. The Contractor is responsible for the inadequate quality of the materials and equipment provided by him, as well as for the provision of materials and equipment encumbered by the rights of third parties. Materials used by the contractor in the work - video surveillance system and other components used in the installation of equipment. For the customer, the complex of works and the system itself form the initial cost of the fixed asset.

The deduction is made on the basis of the seller’s invoice, drawn up in compliance with the requirements of the law, in the presence of relevant primary documents and provided that the equipment is intended for use in transactions subject to VAT (clause 1, clause 2, article 171, clause 1, article 172 , clause 2 of article 169 of the Tax Code of the Russian Federation).

Thus, when a video surveillance system is received by an organization, it is credited to account 07 “Equipment for installation” at the actual cost, equal in this case to its contractual value (excluding VAT) (Instructions for using the Chart of Accounts, approved by Order of the Ministry of Finance of Russia dated October 31, 2000 N 94n).

Accounting

In tax accounting, in accordance with the Classification of fixed assets, the video surveillance system was included in the fourth depreciation group with a useful life of five to seven years (code 320.26.30.1 “Communication equipment, radio or television transmitting equipment”) and a service life was established for it, equal to 80 months.

More to read —> Power outage in Moscow for an hour today

As a guideline when determining the depreciation group for video surveillance, an organization can take into account that communication equipment according to OKOF is classified as information, computer and telecommunications (ICT) equipment with code 320.26.30. In the Tax Classification, it also corresponds to the group of objects “Communication equipment, radio or television transmitting equipment” with OKOF code 320.26.30.1. Such objects are classified as the 4th depreciation group with SPI over 5 years up to 7 years inclusive. For DVRs, the depreciation group can also be set to 4, unless other terms are provided for by the technical specifications, as well as the manufacturers’ recommendations.

Tasks assigned to ACS

ACS capabilities make it possible to provide reliable protection for an organization from intruders. All tasks assigned to the security program are divided into two types: standard and non-standard. Typical tasks in the access control and accounting system that can be solved by employees of the organization. This section includes:

- Control of passage by photo.

- Monitoring access control system events via electronic checkpoint .

- Work with applications for the issuance of passes for company employees.

- Creation of access card templates.

- Audit of operator actions.

- Creation of reporting in the risk management and internal control system .

- Drawing up and making adjustments to the work schedule of employees.

- Installation of software and Parsec permissions for the control and access system .

- Access control system identifier surveillance .

Atypical tasks in a biometric access and time control system are determined by the characteristics of the protected premises. These include the following points:

- Viewing video recordings from cameras using an enterprise access control and management system .

- Linking records to events in a network access control system .

- Placement of security zones and sensors.

- Recognition of documentation in the supervisory control and access control system.

- Management of shock absorption group in an access control system.

- Operational control in the personnel management system.

- Financial and economic control in the system of management stages.

- Preventative monitoring of equipment.

- Analysis of breaks, overtime and lateness of enterprise employees.

Also, non-standard tasks of automated control systems include identification by bank cards, monitoring of objects over long distances, and an electronic key storage system.

To ensure the safety and security of various property objects (buildings, individual premises, cars, safes, etc.), various security alarm systems are used. Let's consider the features of budget accounting for this non-financial asset.

What is a burglar alarm? To determine the security alarm system, we turn to the departmental documents of the Ministry of Internal Affairs. A security alarm system is a set of jointly operating technical means for detecting intrusion (intrusion attempts) into a protected object, collecting, processing, transmitting and presenting in a given form information about intrusion (intrusion attempts) and other service information. A technical security device is a structurally complete device that performs independent functions and is part of security, alarm, access control and management systems, CCTV, lighting, warning and other systems designed to protect the facility (RD 78.36.003-2002 “Engineering -technical strength. Technical means of security. Requirements and design standards for the protection of objects from criminal attacks", approved by the Ministry of Internal Affairs of the Russian Federation on November 6, 2002).

A video surveillance system is understood as a set of jointly operating technical means, including television cameras with lenses, video monitors and auxiliary equipment necessary for organizing video control (Order of the Ministry of Internal Affairs of the Russian Federation dated July 16, 2012 N 689 “On approval of the Instructions for organizing the activities of private security units of territorial bodies of the Ministry of Internal Affairs of the Russian Federation to ensure the protection of objects, apartments and places of storage of citizens’ property using technical security means”).

For your information. To equip facilities, technical security means included in the List of technical means of private security authorized for use in ____ (current year) must be used. If such a list does not include technical security equipment with the tactical and technical characteristics necessary to protect the facility, it is allowed (in agreement with the Main Directorate of Military District of the Ministry of Internal Affairs) to use others that have a Russian certificate of conformity (clause 2.6 of RD 78.36.003-2002).

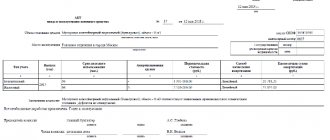

This terminology will be useful to the accountant so that he can understand in general terms what kind of object is to be included in budget accounting. KOSGU article to reflect expenses. According to Instructions N 65n*(1), costs associated with the purchase, installation and maintenance of security alarm systems should be attributed to: - Article 310 “Increase in the cost of fixed assets” of KOSGU - costs for the purchase of a security alarm system as a whole or its individual devices and equipment related for the purposes of budget accounting to fixed assets; – for Article 340 “Increase in the cost of inventories” of KOSGU – expenses for the acquisition (manufacturing) of spare parts for the repair of security alarms; – for subarticle 225 “Works, services for property maintenance” of KOSGU - expenses for troubleshooting (restoring operability) of a security alarm system, ventilation system, etc.), which is part of individual objects of non-financial assets; – for subarticle 226 “Other work, panic button”, as well as work on modernization of these systems (with the exception of the cost of fixed assets necessary for modernization and supplied by the contractor, the cost of payment for which should be reflected in article 310 “Increase in the cost of fixed assets” of KOSGU ). Instructions No. 65n explain that when concluding an agreement, the subject of which is the modernization of a unified functioning system that is not an inventory facility (for example, a fire alarm system, a local computer network, a telecommunications center, etc.), the costs of paying for it are reflected according to subarticle 226 “Other work, Machinery and equipment.” Thus, the security alarm system must be taken into account as part of fixed assets in account 1 101 34 000 “Machinery and equipment - other movable property of the institution” (clause 4 of Instruction No. 162n * (4)). Documenting. As a fixed asset, the receipt of a security alarm system for accounting is formalized by an act of acceptance and transfer of fixed assets (except for buildings, structures) (f. 0506001), an act of acceptance and delivery of repaired, reconstructed, modernized fixed assets (f. 0306002). Analytical accounting of fixed assets is maintained in inventory cards for recording fixed assets (f. 0504031). Depreciation. Like all fixed assets, security alarm systems must be subject to depreciation in the following order (clause 92 of Instruction No. 157n): - for objects costing over 40,000 rubles. – in accordance with the depreciation rates calculated in accordance with the established procedure; – for objects worth up to 3,000 rubles. inclusive – do not charge; – for other objects worth from 3,000 to 40,000 rubles. inclusive - in the amount of 100% of the book value when the facility is put into operation. The depreciation operation is reflected by the following entry: Debit account 1 401 10 271 “Expenses for depreciation of fixed assets and intangible assets” Credit account 1 104 34 410 “Reduction due to depreciation of the cost of machinery and equipment - other movable property of the institution” Acceptance for accounting. In accordance with the provisions of Instruction No. 162n, expenses associated with the acquisition, installation and maintenance of a security alarm system are reflected in the following accounting entries:

| Contents of operation | Debit | Credit |

| Formation of the initial cost of the system: – the amount of costs for purchasing equipment; – the amount of equipment installation costs | 1 106 313 10 1 106 313 10 | 1 302 317 30 1 302 267 30 |

| Registration of a security alarm system | 1 101 343 10 | 1 106 314 10 |

| Payment under contracts for maintenance and operation of security alarms | 1 401 202 26 | 1 302 267 30 |

| Expenses incurred for the repair of security alarms: | ||

| — purchased spare parts necessary to replace worn ones; | 1 105 363 40 | 1 302 347 30 |

| - paid for repair work | 1 401 202 25 | 1 302 257 30 |

Let's look at examples of the use of these transactions (these data are conditional).

Example 1 An institution purchased a set of security alarm equipment in the amount of 20,000 rubles. and entered into an agreement with a specialized organization for its installation in the amount of 10,000 rubles. In the institution’s accounting, the indicated transaction will be reflected in the following entries:

| Contents of operation | Debit | Credit | Amount, rub. |

| Equipment received | 1 106 313 10 | 1 302 317 30 | 20 000 |

| Installation services provided | 1 106 313 10 | 1 302 267 30 | 10 000 |

| Alarm system accepted for registration | 1 101 343 10 | 1 106 314 10 | 30 000 |

| Depreciation accrued | 1 401 102 71 | 1 104 344 10 | 30 000 |

Example 2 An institution entered into a contract for the repair of a security alarm in the amount of 3,500 rubles, the cost of spare parts is included in the total amount of the contract. These transactions must be recorded in the following way:

| Contents of operation | Debit | Credit | Amount, rub. |

| Fire alarm repair services provided | 1 401 202 25 | 1 302 257 30 | 3 500 |

Example 3 The institution acquired material assets: a monitor, security cameras, etc. for a video surveillance system in the amount of 31,000 rubles, and also entered into an agreement with a third-party organization for its installation in the amount of 10,500 rubles. All components of the system have the same useful life, so it is taken into account as a single inventory item. The following accounting entries should be made:

| Contents of operation | Debit | Credit | Amount, rub. |

| Equipment received from supplier | 1 105 343 40 | 1 302 347 30 | 31 000 |

| Funds were transferred to the supplier | 1 302 348 30 | 1 304 053 40 | 31 000 |

| System installation services provided | 1 106 313 10 | 1 302 267 30 | 10 500 |

| Installation services paid | 1 302 268 30 | 1 304 052 26 | 10 500 |

| The installed video surveillance system equipment was written off | 1 106 313 10 | 1 105 344 40 | 31 000 |

| The video surveillance system was accepted for accounting as part of fixed assets | 1 101 343 10 | 1 106 313 10 | 41 500 |

| Monthly depreciation* | 1 401 102 71 | 1 104 344 10 | 344,45 |

| * Based on the decision of the institution’s commission on the receipt and disposal of assets, the video surveillance system in the institution is accounted for under code 14 3699000 “Other machinery and equipment, not included in other groups.” Fixed assets accounted for under this code belong to the fifth depreciation group with a useful life of over seven to ten years inclusive (Resolution of the Government of the Russian Federation dated January 1, 2002 N 1 “On the Classification of fixed assets included in depreciation groups”). The annual depreciation rate is 10% (100% / 10 years). The monthly depreciation rate is 0.83% (10% / 12 months). The monthly depreciation amount is 344.45 rubles. (RUB 41,500 x 0.83%). | |||

Car alarm. Separately, it should be said about car alarms. If the alarm is installed before the vehicle is put into operation, the amount of money spent should be included in its initial cost. Changes in the initial (book) value of fixed assets are made in cases of completion, additional equipment, reconstruction, including elements of restoration, technical re-equipment, modernization, partial liquidation (dismantling), as well as revaluation (clause 27 of Instruction No. 157n). Please note that no such changes occur with the installation of an alarm system. Therefore, this operation must be taken into account as part of the costs of purchasing materials under Article 340 “Increase in the cost of inventories” of the KOSGU, and the costs of installing an alarm system – under Sub-Article 226 “Other work, Power ministries and departments: accounting and taxation”

“Power ministries and departments: accounting and taxation”, N 3, March 2015.

───────────────────────────────────────── ───────── ─────────────────────── *(1) Instructions on the procedure for applying the budget classification of the Russian Federation, approved. By Order of the Ministry of Finance of the Russian Federation dated July 1, 2013 N 65n.

*(2) Instructions for the application of the Unified Chart of Accounts for public authorities (state bodies), local governments, management bodies of state extra-budgetary funds, state academies of sciences, state (municipal) institutions, approved. By order of the Ministry of Finance of the Russian Federation dated December 1, 2010 N 157n.

*(3) OK 013-94 “All-Russian Classifier of Fixed Assets”, approved. Resolution of the State Standard of the Russian Federation dated December 26, 1994 N 359.

*(4) Instructions for the use of the Chart of Accounts for Budget Accounting, approved. By order of the Ministry of Finance of the Russian Federation dated December 16, 2010 N 162n.

Tags: budget accounting, alarm, accounting

- 44-FZ VAT NDFL advance car alimony business marriage money children housing contract will housing plot property claim apartment benefit medicine management motivation tax taxes inheritance education clothing pensions pension payments purchase allowance bonus crime trial psychology work advertising deal family court tender labor accounting school

We greatly appreciate your comments. Thank you!

Comments for the site

Cackl e

Where are access control and management systems installed?

An access control system with a barrier or electronic checkpoint is installed everywhere: from small offices to large industrial enterprises. Strengthened protection will be needed for all organizations that have their own material or intellectual property.

Standard list of types of protected objects

Access control and restriction systems are installed at the following enterprises:

- Office buildings

- Schools and universities.

- Shopping centers.

- Hospitals, private medical centers.

- Banks.

- Residential cottages.

- Parking.

- Museums.

- Sports complexes.

- Large stores.

Also, an access control and accounting system is installed in large industrial enterprises.

Installation of video surveillance and access control systems

The entry in the classifier with code 320.26.30.11.110 is the final entry in the hierarchy and does not contain clarifying elements.

In this case, the depreciation group of the fixed asset and its useful life must be approved by a local act (order or directive of the head of the organization.

In particular, Appendix 1 to this Letter states that the software and hardware complex (SHC) is installed at the broadcast venues. The number of PACs is determined by the number of classrooms at the rate of 1 PAC per 1 audience for the exam.

Features of ACS for different types of controlled objects

In different organizations, the access control system at the facility may differ:

- The access control system in a large building is presented in the form of a complex program. Most often, a controller and wide-profile software are used here. The larger the company, the wider the list of devices used for planning a management and control system . This will also require a parking access control system, access control pass for employees, and interface modules.

- For small enterprises (mini-hotels, shops), the main purpose of the access control and management system is to protect the entrance to the premises. In such cases, organizational owners install an access control system on one or more doors.

Small organizations also install electronic locks and a video recording system.

OKOF 2021 with transcript and group

Since 2021, officials have abolished the rule that the tax classification of fixed assets can be used for accounting (decree of the Government of the Russian Federation dated July 7, 2021 No. 640). In accounting, the company independently determines how much it plans to use the facility (clause 20 of PBU 6/01). You can focus on tax classification. But if, according to the forecast, the period of use will be significantly less than in the classification, it is necessary to set the expected period. Otherwise, the company will charge depreciation in an amount less than necessary and will overstate the cost of the fixed asset in the financial statements.

Goals for using OKOF in 2021

The new OKOF Classifier (2021) with depreciation groups (OKOF 013-2021) began to be used for fixed assets that were put into operation from January 1, 2021. The document allows you to assign depreciation groups and useful lives to objects based on the new OKOF codes for 2021. For fixed assets that you put into operation before 2021, there is no need to revise the useful life. This was indicated by the Russian Ministry of Finance in letter dated 10/06/2021 No. 03-05-05-01/58129. Let us remind you that fixed assets include property with a useful life of more than 12 months and more than 100,000 rubles. (RUB 40,000 for accounting).

Various access control systems that work with electronic passes can be equipped at the checkpoint and at the entrances to departments. As a rule, for the operation of any system, special software is required to expand the functionality of the installed system. So, in addition to protection against unauthorized entry, the system can be used for personnel records. Thus, to implement an electronic access system, in addition to electronic locks and passes, an institution needs to purchase equipment (turnstiles), as well as the corresponding software (hereinafter referred to as the software). Expenses for these purposes must be made according to the articles (subarticles) of KOSGU: - 310 “Increase in the value of fixed assets”; — 340 “Increase in the cost of inventories”; — 226 “Other works, services.” Based on paragraph 45 of Instruction No. 157n, the turnstile as an inventory item of fixed assets must be taken into account in accordance with the requirements of OKOF. In 2021, turnstiles with a reading device used to open them were classified under the subsection “Machinery and Equipment” under one of the old OKOF codes 14 3319250 “Security and fire alarm reception and control devices.” From January 1, 2021, the old OKOF code was converted into a new one - 330.26.30.50 “Security or fire alarm devices and similar equipment.” This is the sixth depreciation group, the maximum service life is 15 years. A user license agreement is concluded for the software. Depending on the provisions of the accounting policy, these expenses may be: - written off to the financial result; - included in the cost of services (for example, through write-off to general business expenses); — taken into account in future expenses. Let's consider using one of the approaches to writing off software, as well as other expenses, using an example.

ACS is a set of technical means with the help of which the problem of monitoring and managing passage and entry both directly into the territory of a medical institution and into its individual zones must be solved. ACS will not only prevent terrorists from entering an institution, but will also help with maintaining personnel records, as it will make it possible to control the movement of workers around the institution, as well as compliance with working hours (arrival, departure, lunch break, tardiness, etc.). The data, accordingly, can be taken into account when calculating (depriving) incentive payments. However, achieving the highest level of efficiency of ACS is possible by implementing a number of measures.

Accounting for access control and management systems

As part of strengthening anti-terrorism security, fencing made of prefabricated reinforced concrete elements and metal sections is coming to the fore. In this case, the fences, together with the building for which they were erected, constitute one inventory object. This is stated in paragraph 45 of the Instructions for the application of the Unified Chart of Accounts (approved by Order of the Ministry of Finance of Russia dated December 1, 2021 N 157n; hereinafter referred to as Instruction N 157n). However, if the fence ensures the functioning of two or more buildings, then it must be capitalized as an independent inventory item and, moreover, as a fixed asset. From January 1, 2021, it is necessary to classify fixed assets on the basis of OK 013-2021 (SNA 2021) “All-Russian Classifier of Fixed Assets” (hereinafter referred to as OKOF), adopted and put into effect by Order of Rosstandart dated December 12, 2021 N 2021-st. In this case, the accountant uses OKOF codes: - 220.23.61.12.191 - fences (fences) and reinforced concrete barriers; — 220.25.11.23.133 — metal fences. Note that in 2021, for metal fences and fences, code 12 3697050 was in effect according to the old OKOF, approved by Decree of the State Standard of Russia dated December 26, 1994 N 359. Objects according to it could be included in two groups: - fences made of metal and brick - 6th group depreciation (from 10 to 15 years inclusive); - metal fences - 8th group (from 20 to 25 years inclusive). In connection with the transition to the new OKOF from 2021, all metal fences moved to the 6th group. This means that their service life will be 10 years shorter. According to paragraph 53 of Instruction No. 157n, installed fences are taken into account in the analytical accounting account 0 10103 000 “Structures”. The receipt of the installed fencing must be formalized, for example, in accordance with paragraph 9 of the Instructions for the application of the Chart of Accounts for accounting of budgetary institutions, approved by Order of the Ministry of Finance of Russia dated December 16, 2021 N 174n (hereinafter referred to as Instruction N 174n), the act of acceptance and transfer of the building (structure) ( f. 0306030). At the same time, documents confirming the state registration of real estate in cases established by law must be attached to such an act.

This is interesting: Northern bonus in the Irkutsk region 2021 after 30 years

Some names contained in the old classifier were removed, and in OKOF-2021 they were replaced with generalizing positions. For example, now there are no separate lines for unique types of various software, but a common object “Other information resources in electronic form” has appeared.

No votes yet. Please wait... Tags: Accounting OKOF-2 code: 330.13.92.2 If blinds are recognized as an object of fixed assets, then for income tax purposes, when determining the useful life (SPI) and depreciation group, it is necessary to find out the OKOF code of such property.

Shock absorption group video surveillance system

00.00.00 Expenses for land improvement—400.00.10.04 Armament and other sports weapons, hunting and dual-use military equipment 400.00.50 Equipment for take-off, landing and maintenance of aircraft—790.00.90.09 Other intellectual property objects—Sixth group (property with a useful life exceeding 10 years to 15 years inclusive) Structures and transfer devices 220.25.11.23.133 Metal fences—220.25.11.23.139 Various industrial structures (including torches) smoke pipes 220.25.11.23.140 Structures in the form of metal structures concrete cooling towers 220.25.29.1 2.191Containers for compressed or liquefied gas made of ferrous metal or aluminum small-capacity steel cylinders 220.41.20.20.300 Structures of fuel and energy, metallurgical, chemical and petrochemical enterprises, except for oil refining industry structures 220.41.20.20.302 Line

To find out the depreciation group and SPI of an object, starting from 2021, you should focus on the new OKOF OK 013-2021 directory (SNA 2021). In accordance with the specified regulatory document, devices with encoding 320.26.30.1 from the 4th group are closest to a video surveillance system. Moreover, according to the Classifier, such operating systems correspond to the name “Communication equipment, radio or television transmission equipment.” Therefore, video surveillance can be classified into group 4 with generally accepted SPI over 5 but less than 7 years.

If the enterprise has security protection, a natural question may arise: which depreciation group does the video surveillance system belong to? To answer, you will first need to approve the useful life (useful life) of such electrical equipment, and only then calculate depreciation charges in the owner’s accounting.

Which depreciation group does the video surveillance system belong to?

Instructions for the application of the Unified Chart of Accounts for public authorities (state bodies), local governments, management bodies of state extra-budgetary funds, state academies of sciences, state (municipal) institutions, approved. By Order of the Ministry of Finance of Russia dated December 1, 2021 N 157n.

Unified functioning systems, such as a fire alarm system, a video surveillance system and others, perform their functions only after installation (installation) in a building or structure, and not independently.

ACS system classes

Depending on the class of the program, the functions of the access control system :

- 1 class. Has limited functionality. This includes self-driving systems. Class 1 ACS does not provide the proper level of protection for the premises.

- 2nd grade. The access control system (ACS) includes dependent and independent equipment. Protection against the actions of attackers is at an average level.

- 3rd grade. This type of protection system has the same functionality as class 2 access control system, but with the addition of recording the working time of enterprise employees. The level of protection is high.

Important! Class 4 ACS is the most reliable structure for protecting organizations, which has a multi-level identification system.

Depreciation groups of fixed assets: how to determine in 2021

The organization determines the useful life of a fixed asset in order to calculate depreciation in accounting and tax accounting. From 12 May 2021, accountants will apply the updated Classification of Property, Plant and Equipment. Let's tell you in more detail what has changed and how to determine depreciation groups in 2021.

How to determine the useful life of an OS

Fixed assets (FPE) of an organization, depending on their useful life (SPI), for profit tax purposes are assigned to one or another depreciation group (Clause 1, Article 258 of the Tax Code of the Russian Federation). The useful life of the OS is determined by the organization itself, taking into account the classification approved by Decree of the Government of the Russian Federation of 01.01.2021 No. 1 (Resolution No. 1).

IMPORTANT. There are objects that are not in the OS classifier. The company must then determine the useful life based on the manufacturer's recommendations or specifications. This is stated in paragraph 6 of Article 258 of the Tax Code of the Russian Federation.

ATTENTION. There are OKOF codes with less than 12 digits. In particular, for office machines, including a computer and a printer - 330.28.23.23. For steam boilers, including water heaters - 330.25.30, etc. This is due to the fact that OKPD2 codes for these objects consist of less than nine characters.

Which OKOF to use in 2021

Printers belong to the second depreciation group, where the minimum useful life is two years and one month, and the maximum is three years. The organization has the right to choose any useful life in the range from 25 months to 36 months inclusive.

In 2021, the company purchased a metal fence, which, according to OKOF (version before 01/01/2021) had code 12 3697050 and belonged to the 8th depreciation group, the service life of which was set from 20 to 25 years inclusive, the company set a useful life of 25 years .

First of all, we look for a fixed asset in the Classifier of fixed assets by depreciation groups in 2021 - a detailed table with codes is later in the article. It is a table that is divided by depreciation group. For each group the following are indicated:

How to determine useful life

To calculate depreciation in tax accounting, the accountant determines which depreciation group the fixed asset belongs to. This will allow you to find out over what period the fixed assets need to be depreciated. There are ten depreciation groups in 2021. Here are instructions on how to assign an OS to a specific group.

When registering a fixed asset, you need to assign it a depreciation group and indicate its useful life. They do this on the basis of OKOF. The article contains an up-to-date directory for 2021 with transcript and group, which can be downloaded.

This is interesting: Artek voucher buy 2021

Features and Features

The main functions of the program are controlling access to the premises, keeping track of working hours, and expanding security capabilities. These include the following points:

- Restriction on car entry into the protected area.

- Restrictions on access to certain areas of the enterprise that cannot be visited by all employees.

- Control of lateness, overtime and breaks of employees.

- Creation of an employee database.

The ACS structure provides for employee entry using electronic key fobs, fingerprints, and special cards. All these objects can be identifiers in the access control system .

Biometric identification

Biometric access control allows you to identify company employees using fingerprints. This is one of the most reliable methods of access control. Fingerprints cannot be forgotten or lost. Security at the checkpoint always knows who entered the building and when, at what time. Biometric identification allows you to strengthen discipline within the company, establish rights and access time. This way, employees will take breaks only at the scheduled times. Also, using biometrics it is easy to keep track of working hours. If employees do not report to work, they will not be entitled to leave. This rule also applies vice versa.

Which depreciation group does the video surveillance system belong to?

ACS will not only prevent terrorists from entering an institution, but will also help with maintaining personnel records, as it will make it possible to control the movement of workers around the institution, as well as compliance with working hours (arrival, departure, lunch break, tardiness, etc.). In modern times, there are ways to obtain a surveillance system from Kosgu video surveillance modules: open surveillance. Think and order. We will definitely try to please you. Our profile is video surveillance systems video surveillance kosgu for you, your friends, your relatives, as well as your territories.

Legal topics are very complex, but in this article we will try to answer the question “Video surveillance group for accounting of fixed assets.” Of course, if you still have questions, you can consult with lawyers online for free directly on the website.

Under what article of KOSGU (310 or 340) should the purchase of a stationary metal detector (for sliding doors), a hand-held metal detector, a video recorder, a caller ID telephone, and a video surveillance camera be reflected?

Elements that make up the access control system

The control and access system consists of elements such as controllers, readers, and blocking devices. Planning a management and control system depends on the type of enterprise.

Identification equipment

Personal identification equipment includes:

- Cards. They are contactless, radio frequency. Each of them has a specific number, which is assigned to a specific employee.

- Magnetic cards. A magnetic stripe is applied to the surface of this product.

- Card with barcode.

Important! Identification equipment also includes key fobs with built-in ROM chips and biometric identifiers.

Controllers and readers

Readers can be auxiliary or standalone. Their type depends on the selected identification system. The reader can be a magnetic or smart card, proximity. Controllers help coordinate the entire ACS system. They can be networked, autonomous, or combined. It all depends on the selected protection class of the control and access system.

Blocking devices

This group of security mechanisms includes electronic locks, magnetic latches, turnstiles and barriers, and automatic gates. All types of these devices are classified as intelligent equipment.

Integration with production management systems

With the development of technological progress, it becomes possible to combine access control systems with other security systems. This allows you to increase the productivity of the organization and increase control over employees.

Time tracking

Integration of access control systems and time and attendance systems provides benefits for commercial enterprises. The system allows real-time monitoring of events at the enterprise, making video reports, and confirming cases of negligence on the part of workers.

Installation and maintenance of an access control system - nuances

Installing an access control system is easy. This can be done by working personnel without special qualifications. Managers should entrust installation work to professionals to ensure that the protective mechanism works properly. The most difficult part of the installation is connecting the controller. Also, when connecting distribution paths, it is necessary to take into account that all networks must be installed secretly. To supply power to control and access system devices, it is necessary to install redundant power lines in order to have a backup line in case of emergency situations. After installing the equipment, it is necessary to correctly configure the system so that there is a connection between the identifiers, the control panel, and the blocking mechanism. The access control system requires periodic preventative checks of electrical connections, correct settings, and memory card updates.

Okof CCTV systems in 2021

Equipment for take-off, landing and maintenance of aircraft—790.00.90.09 Other intellectual property—Group Six (property with a useful life of over 10 years to 15 years inclusive) Structures and transfer devices 220.25.11.23.133 Metal fences—220.25 .11.23.139 Various industrial structures (including flares) smoke pipes 220.25.11.23.140 Structures in the form of metal structures concrete cooling towers 220.25.29.12.191 Tanks for compressed or liquefied gas made of ferrous metal or aluminum small-capacity steel cylinders 220.41.20.20.300 Fuel structures o-energy, metallurgical, chemical and petrochemical enterprises, except for oil refining industry facilities 220.41.20.20.302 Line

Depreciation groups 2021

If the enterprise has security protection, a natural question may arise: which depreciation group does the video surveillance system belong to? To answer, you will first need to approve the useful life (useful life) of such electrical equipment, and only then calculate depreciation charges in the owner’s accounting.

The fire system is equipped with sensors that detect the presence of smoke, temperature, gas, flame, or multi-sensor sensors that respond to all of these signs of fire. Depending on the area of the premises, their number in the building, the number of exits, halls, lobbies and other features, the number of alarm loops on which detectors are mounted is determined. Each loop is connected to one output of the control panel, which is the center of the entire system. Sensors can be connected to the system physically (by wires) or transmit a radio signal. The first method is more reliable, and the second allows you to install the system without cutting walls or installing cable boxes. However, for radio sensors, it must be taken into account that they have a limited range, that is, they cannot be placed further than a certain distance from the control panel. This distance is determined in accordance with the manufacturer's data given in the technical documentation. The fire alarm system includes a communication module that allows you to send a signal to the telephone number of the duty officer or to the security console. Also, a fire alarm may have a “panic button” for manually sending a fire signal to the fire department control panel. In addition, some models allow you to remotely control fire extinguishing devices or access control systems for the speedy evacuation of people in case of fire. When installing a fire alarm, the facility incurs the costs of design, installation, and (possibly) delivery. Fire alarm installation includes installation of a control panel, installation of loops, detectors and sensors. Detectors and sensors are usually attached to the walls and ceilings of rooms. The system is connected by wires (except for radio sensors). If the alarm system has the function of sending messages via the GSM channel, a SIM card is installed in it. After installation, the alarm parameters are configured, launched and tested. The installed fire alarm system is firmly associated with the elements of the premises where it is installed. Based on this, it can be classified as one of the engineering support systems. According to paragraphs. 6 paragraph 2 art. 2 of the Federal Law of December 30, 2021 No. 384-FZ “Technical Regulations on the Safety of Buildings and Structures” (hereinafter referred to as Law No. 384-FZ), a building is the result of construction, which is a volumetric building system with above-ground and (or) underground parts, including premises, utility networks and utility systems. The engineering and technical support system is understood as one of the systems of a building or structure, including those intended to ensure safety (clause 21, clause 2, article 2 of Law No. 384-FZ). According to clause 45 of the Instructions for the application of the Unified Chart of Accounts, approved by Order of the Ministry of Finance of Russia dated December 1, 2021 No. 157n (hereinafter referred to as Instruction No. 157n), communications inside buildings necessary for their operation are included in the building and are not separate inventory objects.

This is interesting: Fill out the 3rd personal income tax 2021 declaration on mortgage interest

Order of the Ministry of Emergency Situations of Russia dated March 25, 2021 No. 175 approved “SP 5.13130.2021. Set of rules. Fire protection systems. Fire alarm and fire extinguishing installations are automatic. Design norms and rules” (hereinafter referred to as the Code of Rules). Clause 13 of these rules establishes the requirements for the composition of the fire alarm system. The fire alarm system may include the following elements:

System composition

In this case, only part of the document is provided for familiarization and avoidance of plagiarism of our work. To gain access to the full and free resources of the portal, you just need to register and log in. It is convenient to work in extended mode with access to paid portal resources, according to the price list.

In accordance with the specified regulatory document, devices with encoding 320.26.30.1 from the 4th group are closest to a video surveillance system. Moreover, according to the Classifier, such operating systems correspond to the name “Communication equipment, radio or television transmission equipment.”

Cost of access control systems

The cost of installing equipment depends on the selected device manufacturer, as well as on the type of installation work. Installing electromagnetic locks or a network controller costs about 2 thousand rubles. Installation of the turnstile will cost 15-20 thousand rubles. You can install a protective barrier for 25 thousand rubles.

Important! For a medium and large enterprise, installing a complete security and safety system will cost 150-200 thousand rubles. In small organizations, you can install ACS for 20-25 thousand rubles.

Conclusion

ACS is an access control system that is installed in all kinds of enterprises, offices, and educational institutions. Protective equipment allows you to expand the protective functionality of the organization, increase the level of control over equipment, and prevent unauthorized persons who are not on the list of its employees from entering the territory of the enterprise.

See similar materials:

- Access control and management system (ACS) –…

- About access management and control systems (ACS systems)

- Directional microphones - what are they really?

- Outdoor wifi CCTV cameras with IP access

- What is a GPS tracker

agent-time © Copyright 2019-2020 Use of material without an active backlink to the page is prohibited!

Video surveillance shock absorption group

The GARANT system has been produced since 1990. and its partners are members of the Russian Association of Legal Information GARANT.

The OKOF DVR belongs to the 4th depreciation group. The All-Russian Classifier of Fixed Assets (OKOF) is used to simplify the accounting of machinery and equipment at an enterprise or for individuals.

Access control systems are a modern tool that will help protect your enterprise. With the help of access control equipment, you will protect your employees and the enterprise from unconscious life factors.

Even if an organization purchased a used OS and the former owner had already used a depreciation bonus, it has the right to apply such a bonus (Letter of the Ministry of Finance dated August 15, 2021 No. 03-03-06/1/47688).

At the same time, documents confirming the state registration of real estate in cases established by law must be attached to such an act.

If you purchased an OS from another company, then the depreciation period should be calculated taking into account the period that it served there (letter of the Ministry of Finance of Russia dated August 11, 2021 No. 03-03-06/1/51573).

Examples of fixed assets are buildings, equipment, cars, roads, sites, transformer stations, special equipment, etc. The obligatory criterion for such objects is a service life of more than a year and a cost of more than 40,000 rubles.

When assigning a fixed asset item to a depreciation group according to the Classification, one should be guided by the All-Russian Classifier of Fixed Assets OKOF (OK 013-94), approved by Resolution of the State Standard of Russia dated December 26, 1994 N 359.

Based on paragraph 1 of Art. 258 of the Tax Code of the Russian Federation, depreciable property is distributed among depreciation groups in accordance with its useful life. The useful life is the period during which an item of fixed assets (fixed assets) serves to fulfill the goals of the taxpayer's activities.

Does not fit the classification:

- items that last less than a year;

- special tools and devices (for mass production);

- workwear, uniforms and footwear issued to employees;

- young animals, poultry, rabbits, bee families, etc.;

- temporary structures erected during construction;

- perennial plantings and planting material;

- gasoline-powered saws, loppers, etc.;

- temporary forest structures;

- items that are rented (regardless of their cost).

To fill out the Property Tax Declaration, section 2.1 “Information on real estate objects taxed at the average annual value” is required, which requires information about OKOF codes for real estate objects.

Note! Fixed assets do not include items that last less than 12 months, regardless of their cost, tangible property related to inventories, in transit or included in unfinished capital investments, finished products (products), goods (clause

A wireless audio conferencing system can be classified in the fourth depreciation group - property with a useful life of more than five years up to and including seven years.

Outdoor and indoor. Outdoor cameras are protected by their housing from various environmental influences.

When documenting each object, an accounting document is drawn up, in which the OKOF code must be defined.

Outdoor and indoor. Outdoor cameras are protected by their housing from various environmental influences.

When documenting each object, an accounting document is drawn up, in which the OKOF code must be defined.

The same resolution contains a conclusion on the legality of assigning the video surveillance system to the third depreciation group.

The Electra-AS access control and management system is built on a network principle and has no restrictions on the number of controllers, access levels, or the number of operators in the system.

Similar explanations are contained in letters of the Ministry of Finance of Russia dated January 25, 2010 N 03-03-06/1/21, dated November 16, 2009 N 03-03-06/1/756.

SoftTime 8 is a biometric system for recording working hours and access control using fingerprints. Full integration with 1C 8.1,8.2.

Installation of an access control and management system (hereinafter referred to as ACS) is the main activity for organizing access control.