What reporting does a travel agency need to submit regarding employee income?

All travel agencies - tax agents - must submit information about the income of individuals to the tax inspectorate. That is, those who paid people income subject to personal income tax. Travel agencies submit information on income for 2014 to their inspectorates using the following forms:

- 2-NDFL (approved by order of the Federal Tax Service of Russia on November 17, 2010 No. ММВ-7-3/ [email protected] ). It must be submitted no later than April 1;

- in the form of Appendix No. 2 “Information on the income of an individual paid to him by a tax agent from transactions with securities, transactions with financial instruments of futures transactions...”). It is included in the income tax return (approved by order of the Federal Tax Service of Russia dated November 26, 2014 No. ММВ-7-3/ [email protected] ). Using this form, travel agencies report on dividends paid to their founders.

Next, we will tell you in detail how to fill out and where to submit certificates in form 2-NDFL.

Sign 1 and 2 - what is it?

In the 2-NDFL form there are fields for specifying a characteristic that can take one of four values - from 1 to 3.

Sign 3 or 4 is indicated in the case of reorganization, the reorganized company enters the required option depending on the basis for filing - to reflect data on income with withheld tax, put 3, to reflect data on income from which personal income tax is not withheld, put 4.

If there was no reorganization in the reporting year, then either characteristic 1 or 2 is selected:

- 1 - corresponds to the standard case of filing 2-NDFL at the end of the year in order to reflect income, income tax and deductions for each employee, in accordance with clause 2 of Article 230 of the Tax Code of the Russian Federation;

- 2 - corresponds to the case of reflecting data on accruals from which, for some reason, tax was not withheld during the reporting year (the grounds for non-withholding may be clause 5 of Article 226 of the Tax Code of the Russian Federation or clause 14 of Article 226.1

This is important to know: Statement on the application of the statute of limitations: sample 2021

How to fill out 2-NDFL certificates

Before you start filling out the certificates, first check the completeness and accuracy of the accounting: income received by individuals in 2014, deductions provided to them, and the application of rates.

It is also necessary to clarify the personal data of taxpayers. If they have changed (for example, the last name or identification documents have changed), appropriate changes should be made to the personal income tax registers. And only after this the accountant should start filling out the certificates. Do not forget that each certificate is issued for a specific person.

Now let’s look at an example of filling out certificates in different situations.

The travel agency did not withhold tax from an expensive gift

In December 2014, the travel agency gave the employee an anniversary gift in the amount of 8,500 rubles. However, she did not withhold personal income tax from the gift. › |

› | Gifts to an employee with a total value of up to 4,000 rubles. per year are not subject to personal income tax.

If the travel agency was unable to withhold the calculated tax from December earnings before the end of 2014, it will have to prepare a report about this to the tax office. In this case, two certificates of income of a given taxpayer with sign 2 are issued: one is sent to the inspectorate, and the second is issued to the person himself. In general, such a certificate had to be submitted to the inspectorate before February 1, 2015. It had to indicate not only information about the tax agent and the taxpayer, but also reflect the amount of the gift and the due deduction in the amount of 4,000 rubles, income and deduction codes, the amount of calculated tax and tax not withheld by the tax agent.

If the travel agency does not report on time, the certificate must still be submitted.

In this case, no later than April 1, 2015, you must submit to the inspectorate another certificate with attribute 1 for this employee. It must reflect information about the tax agent and taxpayer, all amounts of taxable income received in 2014, and deductions provided (according to the relevant codes), total amounts of income, tax base, amounts of calculated, withheld and transferred tax. The certificate with feature 1 must also reflect the amount of the gift and the amount of the deduction, as well as the amount of unwithheld tax.

2-NDFL for 2014

At the end of the year, the company must report on the withheld and paid personal income tax for each taxpayer. To do this, you need to submit certificates to the tax authorities in form No. 2-NDFL.

Employers submit 2-NDFL certificates to the Federal Tax Service twice a year. The first time - until February 1 for persons from whose income they were unable to withhold tax. The second - no later than April 1 for citizens who were paid income and withheld personal income tax. After the certificates are submitted, inspectors begin to study them. And if there are inaccuracies, tax officials may ask for clarification.

As a rule, the procedure for filling out a 2-NDFL certificate does not cause difficulties for an accountant, however, in practice there are cases that are not described in any order. We'll talk about them.

GOOD TO KNOW

The amounts of calculated, withheld and transferred tax in the 2-NDFL certificate for the year must be equal. If these indicators differ, tax authorities may ask for an explanation of the discrepancies.

Should the calculated, withheld and transferred tax amounts in Form 2-NDFL be the same?

If you are submitting 2-NDFL certificates for employees from whom tax was withheld, then ideally the indicators in lines 5.3–5.5 of Section 5 of the certificate should match. That is, the amount of tax calculated, withheld and transferred to the budget must be the same. After all, if you have calculated and withheld the tax, then in any case you must transfer it to the budget no later than the next day. Therefore, the corresponding indicators will be equal.

Difficulties arise when we either did not pay wages or did not transfer personal income tax due to our fault. In such a situation, it should be taken into account that the amounts of employee income (as well as personal income tax amounts withheld from such income) accrued (calculated and withheld) for 2014 are shown when filling out form 2-NDFL specifically for 2014, regardless of the date of actual payment of income .

Line 5.5 of form 2-NDFL indicates the amounts of personal income tax transferred to the budget from these incomes. The amount of personal income tax calculated from the taxpayer’s income in 2014 and not paid until the reporting is submitted to the tax authority is not initially reflected in the 2-NDFL certificate submitted to the tax authority for 2014; line 5.5 is not filled in. After paying this income, in our opinion, you should submit an updated 2-NDFL certificate with completed line 5.5.

GOOD TO KNOW

In the updated form of the 2-NDFL certificate, the number is the same as that of the original certificate, but the date of preparation must be indicated new.

How to show personal income tax in a certificate that cannot be withheld

It is not always possible to withhold and transfer personal income tax to the budget from employee remuneration. For example, an employee was given income in kind. But there are no cash payments from which tax could be withheld in his favor. In this case, you can postpone personal income tax payment to the next month only within the current year. It is impossible to postpone the transfer of tax to the next year or pay it at your own expense, so the Federal Tax Service must deal with the collection of underpayments.

For your part, it is important to notify both the Federal Tax Service and the employee of the impossibility of withholding tax. The notification period is until February 1 of the following year. During the same period, you must submit a 2-NDFL certificate to the inspectorate. To ensure that officials understand that they have received a message about unwithheld tax, indicate the value “2” in the name of the certificate in the “sign” field. Enter the calculated tax amount on line 5.3. Move it to line 5.7 “Amount of tax not withheld by the tax agent.” Income from which tax is not withheld is reflected in section 3 of the certificate.

If you do not inform the Federal Tax Service about the impossibility of withholding personal income tax, the tax authorities may find out about this during an on-site audit. Then they will have the right to fine you 200 rubles for each unsubmitted certificate. (Article 126 of the Tax Code of the Russian Federation). Therefore, to prevent this from happening, submit 2-NDFL certificates on time.

Two certificates in form 2-NDFL

If the salary for the previous year was paid after the deadline for submitting form 2-NDFL with sign “1”, the report will have to be submitted twice. Form 2-NDFL must be submitted for the first time no later than April 1. When filling it out in clause 5.3, you should indicate the amount of calculated personal income tax, including the amount of accrued but unpaid wages, for example, for December 2014. Since the salary has not been paid, tax cannot be withheld from it (clause 4 of Article 226 of the Tax Code of the Russian Federation).

Therefore, in paragraphs 5.3 and 5.4 of Form 2-NDFL will show different amounts. The calculated tax will be greater than the withheld tax. The amount of unwithheld personal income tax must be reflected in clause 5.7 of form 2-NDFL.

In order to avoid claims from the tax inspectorate, we recommend attaching a covering letter to the 2-NDFL form explaining the indicator in clause 5.7 of the 2-NDFL form.

Covering letter attached to certificates in form 2-NDFL with sign “1”, which the company submits before April 1, 2015

We send certificates of income of individuals for 2014 in the form of 2-NDFL in the amount of 7 pieces. We inform you that in certificates No. 1–7 in clause 5.7 the amounts of personal income tax not withheld by the tax agent are indicated.

These amounts arose due to the delay in payment of wages for December 2014.

Cosmos LLC plans to repay wage arrears for December 2014 in May 2015.

The second time after repaying wage arrears, clarifying certificates should be sent to the tax office in form 2-NDFL. In the updated report, the indicator of paragraph 5.3 will coincide with the indicators of paragraphs. 5.4 and 5.5, and the cell in clause 5.7 will become empty. When drawing up a clarifying form 2-NDFL, instead of the previously submitted one, you should indicate:

- in the field “No. ____________” – the number of the previously submitted form 2-NDFL;

- in the “from ____________” field – the new date of preparation of form 2-NDFL.

This is stated in paragraph. 8 of Section I of the Recommendations for filling out Form 2-NDFL.

We also recommend attaching a cover letter to the 2-NDFL clarification form explaining the reason for the change in the indicators. An example of it is shown below.

A covering letter attached to the clarifying certificates in form 2-NDFL, which the company submits in 2015 after issuing salaries for December 2014

We send clarifying certificates about the income of individuals for 2014 in the form of 2-NDFL in the amount of 7 pieces.

We inform you that wages for December 2014 were actually issued to employees on May 05, 2015, and therefore changes were made to section 5 of the certificates in form 2-NDFL:

- the indicator in clause 5.7 has been reset to zero;

- in clause 5.4, the indicator is increased by the amount of tax withheld from the salary for December 2014.

Certificate 2-NDFL and over-withheld tax when changing the status of an employee from non-resident to resident

When an organization employs foreign citizens or employees who often go on business trips abroad, their tax status by the end of the calendar year may change from non-resident to resident if the employee was actually in Russia for at least 183 calendar days over the next 12 consecutive months (clause 2 of Art. 207 of the Tax Code of the Russian Federation). Accordingly, on the income received by such employees, it is necessary to recalculate personal income tax at a rate of 13% instead of 30% (clauses 1, 3 of Article 224 of the Tax Code of the Russian Federation). For such cases, when an individual has acquired the status of a tax resident of the Russian Federation, Ch. 23 of the Tax Code of the Russian Federation provides for a special procedure for the return of personal income tax. In such a situation, the tax refund is made not by the tax agent-employer, but by the tax office. To do this, the taxpayer submits to the inspectorate at the end of the tax period a declaration and documents confirming his status, and the tax authority returns the tax in the manner prescribed by Art. 78 of the Tax Code of the Russian Federation (clause 1.1 of Article 231 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated October 28, 2010 No. 03-04-06/6-258). But the tax agent - the employer must:

- issue such employees with 2-NDFL certificates at the end of the year, in which in clause 5.6 “Amount of tax excessively withheld by the tax agent” you need to show the amount of excess tax withheld equal to the difference between the listed personal income tax (clause 5.5 of section 5 of the 2-NDFL certificate) and calculated tax (clause 5.3 of section 5 of certificate 2-NDFL);

- explain to such employees that they need to apply for a tax refund to the Federal Tax Service, where they are registered at their place of stay (for a foreign employee) or at their place of residence (for an employee who is a citizen of the Russian Federation).

IMPORTANT IN WORK

If the overpayment of personal income tax was offset or returned to the employee before the end of the year for which the certificates are prepared, it does not need to be reflected in the reporting. If the amounts are not credited or returned, then the overpayment is recorded on line 5.6.

Information on income in the 2-NDFL certificate from amounts paid in connection with the death of an employee to family members by inheritance

According to Art. 141 of the Labor Code of the Russian Federation, wages not received by the day of the employee’s death are issued to members of his family or to a person who was dependent on the deceased on the day of his death. This norm corresponds to Art. 1183 of the Civil Code of the Russian Federation, according to which the right to receive wages, equivalent payments and other sums of money provided to a citizen as a means of subsistence, subject to payment to the testator, but not received by him during his lifetime for any reason, belongs to those living together with the deceased members of his family, as well as his disabled dependents, regardless of whether they lived with the deceased or not.

Clauses 2, 3 art. 1183 of the Civil Code of the Russian Federation provides that in the absence of these persons or if these persons do not present demands for the payment of such amounts within four months from the date of opening of the inheritance, the corresponding amounts are included in the inheritance and are inherited on the general basis established by the Civil Code of the Russian Federation.

According to Art. 1112 of the Civil Code of the Russian Federation does not include rights and obligations that are inextricably linked with the personality of the testator, as well as rights and obligations, the transfer of which by inheritance is not permitted by the Civil Code of the Russian Federation or other laws. So, for example, the obligations of a citizen-debtor that are terminated by his death are not included in the inheritance if the fulfillment cannot be carried out without the personal participation of the debtor or the obligation is otherwise inextricably linked with the personality of the debtor (Article 418 of the Civil Code of the Russian Federation).

In accordance with paragraphs. 3 p. 3 art. 44 of the Tax Code of the Russian Federation, the obligation to pay taxes and (or) fees terminates with the death of an individual - the taxpayer or with recognition of him as dead in the manner established by the civil legislation of the Russian Federation.

In this case, the heirs are charged with the obligation to repay the debt of the deceased person or a person recognized as dead, only for property taxes and within the limits of the value of the inherited property, in the manner established by the civil legislation of the Russian Federation for the payment by heirs of the testator's debts. Based on clause 18 of Art. 217 of the Tax Code of the Russian Federation are not subject to taxation (exempt from taxation) for personal income tax, income in cash and in kind received from individuals by inheritance, with the exception of remuneration paid to the heirs (successors) of authors of works of science, literature, art, as well as discoveries and inventions and industrial designs. At the same time, the Tax Code of the Russian Federation does not establish any restrictions on the exemption from taxation of a taxpayer’s income received by inheritance, depending on the degree of relationship with the testator (letter of the Ministry of Finance of Russia dated July 26, 2010 No. 03-04-06/10-417).

Consequently, the tax agent organization does not have the obligation to withhold personal income tax from the amounts of remuneration due to the deceased employee and paid in accordance with the established procedure to members of his family or to a person who was dependent on the deceased on the day of his death, or to heirs in the manner established by Art. 1183 of the Civil Code of the Russian Federation (clause 18 of Article 217 of the Tax Code of the Russian Federation, letters of the Ministry of Finance of Russia dated 06/04/2012 No. 03-04-06/3-147, dated 02/24/2009 No. 03-02-07/1-87, letter of the Federal Tax Service of Russia dated 08/30/2013 No. BS-4-11/15797).

In other words, when the income lost by a deceased employee is paid to his heirs, personal income tax is not withheld from them, since the indicated income is included in the inheritance mass, and the amount passed on by inheritance is not subject to personal income tax. Such income (clause 18 of Article 217 of the Tax Code of the Russian Federation) of a deceased employee, from which personal income tax was not withheld, is not reflected in the 2-NDFL certificate. This is due to the fact that in this document, in addition to taxable income, only partially taxable income is reflected (for example, related to gifts, material assistance, etc.).

Desk tax audit of 2-NDFL certificates

Certificates submitted by tax agents in form 2-NDFL are neither tax returns nor calculations in the sense of Art. 80, 88 of the Tax Code of the Russian Federation, since they contain only information about income paid to individuals and the amounts of accrued and withheld tax. Therefore, they cannot be the subject of a desk tax audit.

In addition, the 2-NDFL certificate does not contain the data necessary to control the calculation and payment of personal income tax (dates of payment of income to employees, information about the amounts of tax actually transferred to the budget, etc.). Therefore, taking into account the specifics of calculation and withholding of personal income tax by a tax agent depending on the timing of payment of wages for each month (clause 6 of Article 226 of the Tax Code of the Russian Federation), the issue of the correctness of calculation, withholding, completeness of transfer and the amount of penalties can only be resolved during an on-site visit tax audit of a tax agent (resolutions of the Federal Antimonopoly Service of the Ural District dated September 13, 2010 No. Ф09-6098/10-С2, dated October 15, 2009 No. Ф09-8601/09-С3).

- Back

- Forward

The company recalculated the tax

The employee went on vacation on December 4, 2014.

Vacation pay was paid to him on December 1, 2014. However, on December 8, 2014, the employee took sick leave, remaining ill until the end of 2014. In January 2015, the employee submitted his sick leave to the accounting department. Due to the employee’s illness, the accounting department recalculated vacation pay and accrued temporary disability benefits, which the employee received already in 2015. Part of the previously accrued amounts of vacation pay and personal income tax for December 2014 was reversed. The travel agency returned the overpayment of personal income tax for December to the employee in January 2015. The date of receipt of vacation pay and sick leave benefits is determined in accordance with subparagraph 1 of paragraph 1 of Article 223 of the Tax Code of the Russian Federation as the day of payment of these incomes.

When filling out the certificate, the amount of December earnings and vacation pay (including recalculation) should be reflected both in the personal income tax register and in the certificate as part of income for December 2014. Therefore, the 2-NDFL certificate for income code 2012 (vacation pay) reflects the actual amount of vacation pay. The amount of overpaid vacation pay does not need to be shown in the 2-NDFL certificate, since it is withheld from the employee’s income.

The amount of personal income tax on December income should also be reflected in the tax register and in the income certificate for 2014. Moreover, the personal income tax amount is indicated taking into account recalculation and return of overpayment. The amount of overpaid tax is not reflected in the certificate, since it was returned to the employee.

A similar position is set out in the letter of the Federal Tax Service of Russia dated October 24, 2013 No. BS-4-11/19079O.

The employee changed jobs

A branch employee moved to work at the head office of the travel agency in October 2014.

Before the transition, the travel agency withheld tax on his earnings and transferred them to the location of the branch. The organization and its branches are located in different areas of the region. Since October 2014, the company has transferred withheld tax from employee income to the place of registration of the head office. In such a situation, two certificates with attribute 1 should be issued for the employee. One must reflect only the income received by the person for work at the head office, as well as the personal income tax paid from him. Another certificate contains the income received by the employee for work in the branch and the tax on it.

Moreover, in the first certificate in Section 1, you must indicate the INN/KPP of the organization, OKTMO code - the code of the municipality in whose territory the organization is located. The second certificate contains the TIN of the organization, the checkpoint at the place of registration of the branch, the OKTMO code - the code of the municipality in whose territory the branch of the organization is located.

Accordingly, the certificate numbers will be different.

The tax had to be recalculated due to the fact that the employee’s status changed

The employee was not a tax resident in 2014.

Therefore, at the beginning of the year, the travel agency calculated and withheld tax on his earnings at a rate of 30 percent. In July 2014, the employee acquired resident status. In this regard, the accountant recalculated the employee’s tax at a rate of 13 percent, giving him standard deductions for three children. In addition, since July 2014, the organization’s employee has received income in the form of material benefits from savings on interest for using the loan. The organization calculated and withheld tax on material benefits at a rate of 35 percent. In such a situation, one certificate must be issued for the employee, but it will have as many sections (from three to five) as the rates the travel agency applied to his income.

For example, in the third section of the certificate, it is necessary to reflect income taxed at a rate of 13 percent (by type of code), in the fourth - provided standard tax deductions (by type of code), and in the fifth section show the total amount of income, the tax base and the amount of tax (calculated , withheld and transferred) at a rate of 13 percent. › |

› | Tax deductions are provided to residents.

The heading of the third and fifth sections states the rate of 13 percent. Moreover, the same section reflects the amount of tax previously withheld at a rate of 30 percent, since it is included in the payment of tax at a rate of 13 percent.

In other sections of the certificate, you should indicate the amount of income in the form of material benefits and a tax rate of 35 percent.

Section 2

The second section indicates the final data on income and personal income tax for the reporting period:

- the total amount of income of an individual;

- the tax base;

- tax rate (usually 13%);

Note! Form 2-NDFL is filled out separately for each rate at which the taxpayer’s income was subject to personal income tax during the year.

If the tax was not withheld (signs 2 and 4), the filling details will be as follows:

- The line “Calculated tax amount” reflects the amount of accrued personal income tax;

- In the line “Amount of tax not withheld by the tax agent” - the amount of tax that was not withheld;

- In the lines “Amount of tax withheld”, “Amount of tax transferred” and “Amount of tax excessively withheld by the tax agent” there are dashes.

How to fill out the section when withholding personal income tax is shown in the example at the end of the article.

Note! There should be no empty cells in the form - they all must be filled in. If there is no indicator or it is shorter than the allotted field, dashes are placed in the empty cells. As for the absence of a total indicator, zero is indicated (example - kopecks).

Report on paper or electronically

A travel agency can submit information on Form 2-NDFL either on paper or in electronic form (clause 2 of Article 230 of the Tax Code of the Russian Federation).

In what format should your company report? Information is submitted on paper only in cases where during the year the travel agency paid income to no more than 10 people.

In other cases, information on Form 2-NDFL will have to be submitted electronically.

The date when the travel agency submitted certificates to the inspection is considered:

- the day on which they were submitted to your department of the Federal Tax Service - if you report on paper;

- the day on which the certificates were sent by post with a description of the contents - if you are sending the forms by mail;

- the day recorded in the confirmation of a specialized telecom operator or tax office - if you submit electronic reporting.

Let's look at the procedure for submitting certificates in more detail.

Responsibility for violating the deadline for submitting the 2-NDFL report in 2019

Any failure to comply with the law threatens the violator with liability. Thus, violation of the deadline for submitting 2-NDFL provides for an administrative fine, the amount of which is specified in the Tax Code of the Russian Federation (TC RF) and in the Code of Administrative Offenses of the Russian Federation (CAO) .

Since the certificate is intended for each individual employee, the fine is calculated at 200 rubles for each form not submitted or submitted in violation of the deadline.

The fine is collected from the organization or individual entrepreneur as the employer. Directly from the head of the organization to the state account for violating the deadlines for submitting 2-personal income tax comes from 300–500 rubles. There is also a fine for an inaccurate certificate, i.e. a certificate submitted with incorrect or false information. The fine in this case will be 500 rubles for each incorrect form. If the organization itself is the first to discover an error in the certificate and clarifies the information in advance, then a fine can be avoided.

However, the amount of the fine does not depend on the number of days of delay in filing reports.

When submitting reports, you should always be very careful to avoid adverse consequences. In some cases this may be a small fine, but in others it may result in criminal liability.

The travel agency submits certificates on paper

Certificates on paper must be submitted to the travel agency with the accompanying register in two copies.

On the day the certificates and accompanying registers are submitted, the inspector will check whether the following are correctly reflected in the documents:

- details of the tax agent (his name, TIN, KPP, OKTMO);

- details of the income recipient (full name, details of an identity document, address of permanent residence, date of birth);

- data on income and transferred tax amounts (month, income code, total amount of income, tax base, amount of tax that the travel agency calculated, withheld and transferred to the budget).

Based on the results of such visual control, the inspector will draw up a protocol for receiving information on the income of individuals on paper in two copies.

The inspector will give one copy of the register and the protocol to the tax agent, and he will leave the second copies with the inspectorate.

In this case, the fact that the tax agent provided correct information to the inspectorate will be confirmed by the protocol.

How to correctly fill out information about income for employees?

Form 2-NDFL is presented in several parts:

- the title part to reflect the details of the certificate and information about the tax agent;

- section 1 to reflect information about the employee;

- section 2 for income and income tax;

- section 3 for deductions;

- information about the person confirming the accuracy of the completed data.

At the top of the form there should be the TIN and KPP of the tax agent organization (if it is an individual entrepreneur, then without KPP).

- serial reference number;

- year for which submitted (2019);

- sign - 1 or 3 for reorganized companies;

- adjustment number - zero if 2-NDFL is submitted for the first time;

- tax number;

- name of the organization or individual entrepreneur acting as a tax agent;

- OKTMO;

- telephone;

- reorganized companies also indicate the form of reorganization and the TIN and KPP of the former organization.

In the section about the employee, fill in information about him:

- FULL NAME;

- status (for citizens of the Russian Federation this is 1);

- birth information;

- citizenship (643 for the Russian Federation);

- details of a passport or other identification document.

In the section on income and tax, you need to reflect data for the entire year in a generalized form for a specific employee:

- annual income accrued in favor of the employee;

- the basis for calculating the tax is the difference between income and the total amount of deductions provided;

- tax calculated from the base (13% * size of the tax base);

- tax deducted from an employee's salary;

- tax transferred to the budget;

- overpayment of personal income tax, if any;

- tax not withheld for various reasons.

The amount of deductions for calculating the tax base is calculated in the next section, where you need to show the deduction code and the corresponding amount for the year. For example, for standard benefits for children, code 126 is provided.

If in 2021 an employee applied to the Federal Tax Service to receive a tax notice to receive a property or social deduction through an employer, then you must indicate the details of the notice and the amount of the deduction provided for it.

Expert opinion

Davydov Alexander Yurievich

Civil law consultant with 20 years of practice. Author of numerous articles on legal topics

The certificate must be signed and dated. If the transfer of 2-NDFL is carried out through a representative, then you must additionally indicate his full name and details of the power of attorney.

The company provides certificates on electronic media

In this case, the travel agency sends certificates to the inspection in the form of a file (files) of the approved format.

And again, accompanying registers on paper must be attached to the files in two copies for each file. In this case, the inspector will reflect the results of monitoring the file with income certificates in the protocol for receiving information, which he will issue to you in two copies.

One copy of the register and protocol will be given to the authorized person of the tax agent or sent to you by mail, and the second copies will remain with the inspectorate.

Confirmation of the accuracy and completeness of information

The certificate can be signed by the taxpayer himself (company director, entrepreneur) or his legal successor, as well as by an authorized individual or representative of an authorized legal entity. Depending on who signs, you must indicate the code :

- 1 - the document was signed by the tax agent or legal successor himself;

- 2 - this was done by the legal representative.

In the next three lines you need to indicate the last name, first name, and patronymic of the person who signs the certificate . If the director signs the certificate and submits it to the Federal Tax Service by an accountant, then there is no need to indicate the accountant’s full name in this section.

If the 2-NDFL is signed by a proxy, the name and details of the power of attorney must be indicated in the bottom line of the first sheet.

Reporting to be done electronically

The travel agency sends electronic certificates to the inspectorate via telecommunication channels through a specialized communications operator. But this is only if the travel agency has the opportunity:

- generate certificates electronically;

- encrypt information when sending and decrypt it when receiving information using encryption tools;

- generate a qualified electronic signature when transmitting information.

If a travel agency has separate divisions, then a separate file is generated for each of them.

In this case, one file must contain information with the same combination of details: TIN and KPP, OKTMO, reporting year, attribute of the information provided. Within 10 days from the date when the travel agency sent the information to the inspection, it sends the tax agent a register and a protocol for receiving information in electronic form. › |

› | If updated certificates are submitted to the inspectorate, only the information that has been corrected must be submitted.

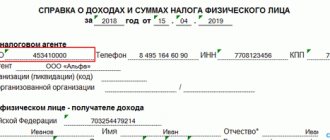

Heading

At the top of each sheet of the certificate, the tax agent’s INN and KPP are affixed, and the serial number of the page is also indicated.

At the beginning of the first sheet general information . Here is the information:

- serial number of the certificate;

- for what year is it compiled;

- sign - a digital code indicating the basis for reporting information on income: 1 - personal income tax is withheld from income;

- 2 - personal income tax could not be withheld;

- 3 - the certificate was submitted by the legal successor, personal income tax was withheld;

- 4 - the certificate was submitted by the legal successor, but personal income tax was not withheld.

- 00 - if the certificate is prepared initially;

To which tax office should information about income be submitted?

The travel agency must submit information in Form 2-NDFL to the inspectorate at its place of registration.

However, if it reports on the income of individuals working in separate divisions, the information will have to be submitted to the inspectorate at the location of each separate division. Such clarifications are given in the letter of the Ministry of Finance of Russia dated December 4, 2012 No. 03-04-06/8-341.

Important to remember

A certificate in form 2-NDFL must be filled out separately for each employee to whom the travel agency paid income.

Table. Information about Ivanov’s income and deductions for filling out 2-NDFL

| Index | Meaning |

| Monthly salary (income code 2000) | 20,000 rubles |

| Dividends in December (income code 1010) | 50,000 rubles |

| Personal income tax deduction for a child (deduction code 126) | 1,400 x 12 = 16,800 rubles |

| Total income | 20,000 x 12 + 50,000 = 290,000 rubles |

| The tax base | 290,000 - 16,800 = 273,200 rubles |

| Tax rate (salaries and dividends) | 13% |

| Accrued, withheld and transferred to the personal income tax budget | 273,200 / 100 * 13 = 35,516 rubles |

Below is how an accountant at Romashka LLC must fill out a 2-NDFL certificate for Ivan Ivanovich Ivanov (the form will become effective in 2021).

Form 2-NDFL in 2021 - how to fill it out Appendix to the 2-NDFL certificate - income and deductions by month