Dividends are part of the profit of a commercial organization that is distributed among its participants. If the LLC participant is an individual, then he must pay income tax on dividends on income received from the business. In general, the personal income tax rate on dividends in 2016 is 13%, and two years ago it was 9%.

Read more: Dividends in 6-NDFL 2021: example of filling

Let's remind you of the duties of a tax agent when transferring dividends.

The organization paying dividends becomes a tax agent, that is, it is obliged to withhold tax on dividends and transfer it to the budget. If it is impossible to withhold tax (if paid in kind), the agent is obliged to inform the tax office about the source of income of its recipient. The tax payment date is no later than the date of transfer of dividends. Responsibility for failure to fulfill this obligation is described in Article 123 of the Tax Code of the Russian Federation - a fine of 20% of the amount to be withheld. There are also penalties accrued for each day of delay in payment.

It is worth recalling that after changes were made in 2015 to Article 76 of the Tax Code of the Russian Federation (which regulates the procedure for blocking bank accounts at the initiative of the tax inspectorate), failure to submit calculations for payment of tax on dividends became an indisputable basis for blocking the account of a tax agent. Actually, a similar focus existed before, but arbitration practice, as a rule, protected tax agents: after all, formally they did not submit a declaration, but only a calculation. The right of the tax authorities was thus called into question. But after the changes in the Tax Code, I repeat, this issue no longer causes discrepancies.

Now about the issue of withholding the unpaid tax itself. Regarding fines and penalties, the courts agree with the tax authorities: the agent must pay them because he did not fulfill his duties. And regarding the amount of tax, the court’s position is as follows: the agent is not a taxpayer, and he cannot pay the tax at his own expense. Therefore, tax officials were asked to go to the taxpayer himself (that is, the recipient of the dividend) and withhold the tax there.

But in any case, penalties will be accrued to the agent until the recipient of the dividend repays the debt to the budget. This is the nuance.

By the way, the absence of the obligation to pay the tax itself does not apply to the situation when income is paid to a foreign legal entity. In the case where the taxpayer is not under the control of our tax authorities, then the responsibility for transferring the tax to the budget of the Russian Federation lies with the agent. This circumstance is stipulated in the resolution of the Plenum of the Supreme Arbitration Court dated July 30, 2013 No. 57. By the way, it contains conclusions about the impossibility of blocking the agent’s account, but, I repeat, they were made even before the changes to Article 76 of the Tax Code of the Russian Federation.

If the participants are foreigners

To avoid double taxation, it is necessary to find out in advance which agreement is in force between countries. The seventh article of the Tax Code of the Russian Federation will tell about the priorities for the Russian side.

To take advantage of the privileges, management must prepare documents that would confirm the fact of carrying out activities in the territory of another state.

When paying dividends by individual founders, the latter must confirm payment of tax to the treasury of another country.

Otherwise, the citizenship of the founder will not affect the amount of tax. The declaration for this tax must be completed the day after the profit is received.

But this rule does not apply to organizations that operate under a simplified system. In such situations, income tax is included in the base when calculated according to the usual scheme, and is indicated in the usual declaration.

back to menu ↑

How to correctly calculate the amount of tax to be paid on dividends?

Clause 3 of Article 284 of the Tax Code of the Russian Federation talks about three tax rates on dividends. Zero rate, 13% and 15%. In the latter situation, with foreigners, the rate must correspond to the intergovernmental agreement. And if a reduced rate is provided there, then it is necessary to apply it. The agent’s task is to obtain confirmation from the recipient of the income that he, as a foreign legal entity, falls under the jurisdiction of this intergovernmental agreement. Tax authorities will primarily pay attention to this.

When we talk about Russian recipients (with a rate of 13%), we need to look at the conditions for excluding part of the income from the tax base (Article 275 of the Tax Code of the Russian Federation). The essence of the exception is that the amount of dividends you pay to the parent organization is reduced by the amount of dividends you received from the subsidiary. So as not to tax them twice. There may be a situation where the subsidiary is more profitable than you, meaning your dividends are less than those you received. In this case, the object of taxation does not arise.

The calculation situation becomes more complicated when the recipients of dividends, among others, are entities that do not pay income tax. These are the same foreigners (including individuals), Russian individuals, and municipalities or constituent entities of the Russian Federation that own shares in the organization.

Article 275 of the Tax Code of the Russian Federation precisely proposes the so-called mechanism for the specific weight of dividends paid to each of the participants, using a special formula that takes into account the difference between dividends received and dividends payable. You distribute, and having already determined the tax base for each participant, apply the appropriate rate to it. This is precisely what sheet 03 form is aimed at (the same calculation of tax on dividends) in today’s income tax return. It is quite rich because it takes into account all amounts of dividends (including those intended for income tax evaders).

But there is a nuance here. After all, making a decision to pay dividends is one thing, and another is their actual payment, which, due to a lack of funds, can be carried out in stages - first to one participant, then to another. And if you paid dividends only partially in the first quarter, then sheet 03 is filled out in relation to the decision itself (and this is stated in the instructions for filling out the declaration). That is, this is a calculation of the tax base. And then you determine the dividends that were actually paid in a given reporting period. They determine the amount of tax that must be paid. And this information goes to section 1.3. And sheet 03 is basically duplicated each time, but lines 110 and 120 change. And the data from line 120 of sheet 03 of this quarter is transferred to section 1.3.

Features of calculation and payments

Paragraph 1 46 of Article 46 of the Tax Code of the Russian Federation will help to avoid annoying mistakes and misunderstandings during calculations.

According to the law, dividends are any profit received by an individual or organization. It can only be used after deducting income tax.

Dividends also include interest income received from shares. What income does not fall into this category?

- Payments that are contributions from organizations.

- Valuable documents belonging to companies. They are considered the personal property of each individual participant.

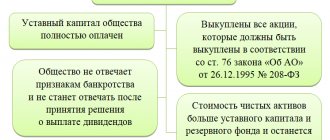

- The money that participants receive when they are declared bankrupt[/anchor]. If these amounts do not exceed the contribution made by members or shareholders.

back to menu ↑

Personal income tax in 2021

Line 070 of the 6-NDFL report: cumulative or not?

Form 6-NDFL has become familiar to organizations and individual entrepreneurs when filing tax reports, but difficulties in filling out this form still arise. And one of the common questions: how to fill out line 070 in 6-NDFL - on an accrual basis or not? The answer to this is given in the order of the Federal Tax...

What is included in line 070 of form 6-NDFL

Tax reporting form 6-NDFL is still new for enterprises and organizations. And filling it out often raises questions that require clarification from inspectors. Let's take a closer look at line 070 6-NDFL: what is included there and what information the accountant needs to fill it out. This line is located in the first section of the reporting form.…

Online tax certificate 2-NDFL: how to get it

Probably more than half of all employed citizens sooner or later faced the need to obtain documentation of their income. This function is performed by the 2-NDFL certificate, which contains all the information about the taxpayer for the period specified in it. With the development of information technology, people are increasingly interested in the question of how...

Financial assistance not subject to taxation

Employers can provide financial assistance to their employees for various reasons. For example, a certain amount is paid at the birth of a child or in connection with tragic events - the death of a family member, emergency incidents. There are several types of payments, and almost all of them relate to tax-free financial assistance...

Income declaration form for individuals for 2021

In 2021, many individuals need to submit a report on their income for the past year to their tax office. In this material, we have collected the most important things about filling out and submitting the personal income tax return for 2021. We'll tell you which form to use for this with the option...

Income declaration form 2021: download

At the end of 2021, many individuals need to fill out and submit an income tax return in 2021. We will tell you which form to use for this with the opportunity to download its most current version for free directly from this article. Who is submitting in 2021 The task is to download the income statement...

Transfer of personal income tax in 2021: payment details

In order to correctly comply with payment discipline for income tax, you need to know the exact details for transferring personal income tax in 2018. This consultation will help you avoid making mistakes when filling out the relevant payment order. What to follow In order to pay personal income tax for an employee, it’s almost impossible to get the details somewhere in one place (source)...

What is the personal income tax on lottery winnings?

How much is personal income tax on winnings? The 2018 declaration campaign for income for 2021 is nearing its end. The last day to submit the declaration is May 3, 2021. This means that individuals who were lucky enough to get rich last year urgently need to submit a report on this and then pay personal income tax...

How to pay personal income tax from non-resident foreigners in 2021

The actual status of a tax resident allows you to understand at what rate income tax should be paid. As a general rule, individuals and legal entities permanently stationed in Russia make significantly fewer deductions than foreign citizens. Let's look at what the personal income tax rate is for non-residents in 2021, how to comply...

Deadline for submission of 3-NDFL declaration for individual entrepreneurs and individuals for 2021

The deadline for submitting 3-NDFL for 2021 depends on several circumstances. Let's consider who this obligation applies to and what determines the deadline for filing the 3-NDFL declaration for 2021 in 2018. Also see “New Form 3-NDFL in 2021”. Who is required to submit a 3-NDFL declaration From the title...

Features of companies operating on the simplified tax system

To pay dividends, the founders need to determine what net profit the LLC receives. Calculations are made based on data from accounting reports.

But the legislation says that companies using the simplified tax system are exempt from such reporting. They only need to report on intangible assets and fixed assets. How to solve the problem in this case?

There are several options.

- Accounting. This helps with determining net income and paying dividends.

- Restoring accounting records if they were missing before.

- When accounting reporting is carried out after a complete inventory of all property has been carried out.

The information indicated in the balance sheet is confirmed by the inventory and its results. This procedure is formalized with primary documents.

To fill out the balance correctly, you need to take an inventory of:

- The amount of funds, not only in the cash registers, but also for the current account.

- Assets and liabilities in the company.

- Amounts of debt on loans and borrowings.

- Financial investments for different periods.

- Manufacturing processes that have not been completed.

- Debts on credit and debit.

- The number of fixed assets, intangible assets.

The charter of the LLC company reflects the indicators by which the additional authorized capital is calculated.

When the asset and liability indicators on the balance sheet are calculated, a difference appears, which reflects the result of the company’s activities. Profit is shown as a positive difference, and loss as a negative difference.

The calculation of net assets in the company for the founders is carried out according to the balance sheet.

back to menu ↑