Often, employees of individual entrepreneurs and organizations go on business trips outside their place of work. This type of travel is called business travel. The Labor Code of the Russian Federation (Article 168) contains a definition of the concept of “travel expenses” and a list of guarantees in the event that an employee is sent on a business trip.

Thus, the company guarantees the employee not only the preservation of his job and average salary, but also reimbursement of expenses incurred on a business trip. In our article we will look at what types of travel expenses exist in 2020, how to calculate and document them, and many other issues related to this topic. At the same time, daily travel expenses in 2021 will be considered in more detail.

Procedure for paying daily allowances to employees

Daily allowances are reimbursed to the employee for each day while he is on a business trip. Weekends and non-working holidays, as well as days on the road, including forced stops along the way, are also paid. For example, an employee went on a business trip on Sunday and returned the following week on Saturday. Per diems for Saturday and Sunday are paid.

Daily allowances for one-day business trips within Russia are not paid (but the employer has the right to provide compensation in the local regulations of the organization in lieu of daily allowances for such trips). Read more about daily allowances for one-day business trips later in this article.

What documents do I need to have with me to pay for a work trip?

As soon as the business trip is over, the employee is obliged to provide his management with all the receipts, which clearly show the process of spending government funds. If company representatives publish official confirmation of all expenses invested in the trip, the amount of money spent will be reimbursed in full. It is advisable to keep all checks or receipts for payment of funds in order to avoid additional questions in the future about the exact location of their spending.

After a business trip, the employee must have with him round-trip tickets that clearly indicate the cost of travel, a receipt for the price of travel accommodation, receipts for all daily expenses, as well as a receipt for the vehicles needed to get to the destination. In the event that an employee goes beyond the established daily travel limit or makes personal expenses, management is not obliged to pay such expenses.

Daily allowance in 2021 in Russia and abroad

The company has the right to decide for itself how much to pay employees per business trip day (Article 168 of the Labor Code of the Russian Federation). The amount of daily allowance for business trips must be fixed in the internal documents of the organization, for example, in the Regulations on Business Travel .

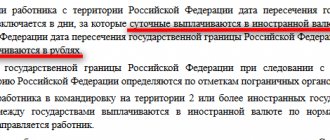

Accountants know about 700 and 2,500 rubles - if the daily allowance does not exceed these amounts, then you will not have to pay personal income tax on these amounts. Therefore, for convenience, some companies introduce daily allowance amounts of 700 and 2,500 rubles, so as not to withhold personal income tax from these amounts. But this does not mean at all that an organization can set the daily allowance for employees at 700 and 2500 rubles and not a ruble more or less. You can, for example, set a daily allowance of at least 4,000 rubles for each day of a business trip in Russia, but then you will have to withhold personal income tax from 3,300 rubles (4,000 rubles – 700 rubles = 3,300 rubles)

Please note that the organization determines the amount of daily allowance independently, fixing its amount in the local regulations of the organization, for example, in the Regulations on Business Travel. There are maximum amounts of daily allowance that are not subject to personal income tax (paragraph 12, paragraph 3, article 217 of the Tax Code of the Russian Federation). In particular, the daily allowance in Russia is 700 rubles, abroad - 2500 rubles. That is, if an organization sets daily allowances in Russia in the amount of 1000 rubles, then from 300 rubles (1000 - 700) the employer should withhold personal income tax

| As a general rule, daily allowances paid to an employee are not subject to personal income tax if their amount does not exceed: 700 rubles — for each day of a business trip in Russia; 2,500 rubles - for each day when traveling abroad. Conclusion: as such, there is no daily allowance limit for commercial organizations. There are only amounts that are not subject to personal income tax (700 and 2500 rubles). So how much per diem should you pay? — decide for your organization yourself (fix the decision in internal documents). |

If the advance is issued in rubles

In situations where an organization does not have a foreign currency account, it can issue an advance in rubles to an employee going on a business trip. The employee independently purchases currency at the relevant branch of the bank (exchange office), whose cashier is obliged to issue this person a document confirming the transaction with cash foreign currency and checks.

In this case, all currency conversion operations carried out through exchange offices (the corresponding divisions of banks) should be considered only as transactions of individuals. When purchasing cash currency (this fact must be documented), the seconded employee will spend a specific amount of rubles to purchase a specific amount of currency on behalf of an individual. Then, on the territory of a foreign state, he will spend a certain amount of currency on housing, telephone conversations and other expenses in the interests of the organization, which will be confirmed by primary documents on the expenses.

In this regard, the question arises: at what rate should an employee’s expenses incurred on a foreign business trip be reflected in accounting and tax accounting:

- on the date of approval of the advance report;

- on the date of payment of accountable amounts;

- on the date the employee exchanged rubles received for foreign currency?

The regulatory authorities gave their explanations on this matter (see letters from the Ministry of Finance of Russia dated March 31, 2011 No. 03-03-06/1/193 and the Federal Tax Service of Russia dated March 21, 2011 No. KE-4-3/4408).

Their essence boils down to the following: the organization’s expenses should be determined based on the amount of currency spent by the employee according to the primary documents at the exchange rate, which is determined by the certificate of purchase of foreign currency by the specified person. At the same time, by virtue of paragraphs. 5 paragraph 7 art. 272 of the Tax Code of the Russian Federation, the date of travel expenses is the date of approval of the advance report.

Thus, according to officials, the organization will compensate the employee for the amount of his actual expenses, that is, the amount at the rate indicated in the documents confirming the purchase of currency, taking into account the sale of the unspent balance in currency (we believe that for accounting purposes it should be reflected in expenses exactly this amount). And for the purposes of calculating income tax, currency conversion into rubles will be made at the rate valid on the date of approval of the advance report.

Example 3

The organization sent its employee on a business trip abroad from January 27 to January 31, 2015.

On January 27, 2015, an advance in the amount of 76,000 rubles was issued to the employee from the cash register.

On the same day, he purchased 1,000 euros at an exchange office at the rate of 75 rubles/euro.

On a business trip, the employee spent 990 euros, which is confirmed by relevant documents.

Upon returning from a business trip, he exchanged the balance of the advance in the amount of 10 euros at an exchange office at the rate of 80 rubles/euro.

The purchase and sale of foreign currency is confirmed by a bank certificate.

On February 2, the employee submitted an advance report in the amount of 990 euros (which was approved on the same day), and returned the balance in rubles to the cashier.

The exchange rate of the Central Bank of the Russian Federation as of 02/02/2015 corresponds to 78.1105 rubles/euro.

A posted employee spent 75,000 rubles on the purchase of foreign currency. (1,000 euros x 75 rubles/euro), received from the sale of the balance of the advance payment of 800 rubles. (10 euros x 80 rubles/euro).

In total, the employee actually spent 74,200 rubles in rubles. (75,000 - 800). In accounting, this amount should be reflected as expenses.

The employee should return 1,800 rubles to the organization’s cash desk. (76,000 - 74,200).

For the purposes of calculating income tax, travel expenses will be calculated at the exchange rate in effect on the date of approval of the advance report and will amount to RUB 77,329.4. (990 euros x 78.1105 rubles/euro).

The constant difference is equal to RUB 3,129.4. (77,329.4 - 74,200). The permanent tax asset (PTA) will be 625.88 rubles. (RUB 3,129.4 x 20%).

The following entries will be made in the organization's accounting:

How to calculate business trip days for which you need to pay daily allowance

How to determine the number of days for which daily allowance must be paid? For example, if an employee goes on a business trip in a personal and company car, then you can count the days using a memo. The employee must submit such a note when he returns from a business trip, along with documents confirming the use of transport to travel to the place of business trip and back (waybill (for example, in form No. 3), invoices, receipts, cash receipts, other documents confirming the route transport). In other cases, determine the number of days for which daily allowance must be paid using travel documents:

Departure day and arrival day must be paid

As for the payment of daily allowances for the day of departure and day of arrival, they must certainly be paid regardless of what time the employee departed (arrived). This is explained as follows.

Day of departure on a business trip

The day of departure for a business trip is the day of departure of the vehicle that will take the employee to the place of business trip from the locality where his place of work is located. Even if a plane or train departs at 23:59, this day is considered the departure day. Therefore, the daily allowance for that day must be paid in full.

Day of return from a business trip

The day of arrival from a business trip is the day of arrival of the transport that the employee used to return from a business trip. It is important to understand that per diem must be paid for the day of arrival from a business trip, no matter what time it occurs. Thus, the daily allowance must be paid even if the vehicle arrived in the locality where the employer is located at 00:01.

Alimony from daily allowances paid to an employee is not withheld. The fact is that daily allowances relate to compensation payments related to business trips (Article 168 of the Labor Code of the Russian Federation, subparagraph “a”, paragraph 8, part 1, article 101 of the Federal Law of October 2, 2007 No. 229-FZ, subparagraph “p” "Clause 2 of the List, approved by Decree of the Government of the Russian Federation dated July 18, 1996 No. 841). Moreover, the amount of daily allowance does not matter (for more details, see “Alimony cannot be withheld from daily allowance”)

One day business trip

By law, there is no minimum travel period established. A trip on behalf of the employer can be a one-day trip. We arrange such a trip as a multi-day business trip (we issue an order, put the appropriate mark on the time sheet: “K” or “06”).

Afterwards the employee reports for the trip. The employer reimburses him for expenses, for example, travel expenses, as well as other agreed amounts. Is there a daily allowance? By law, daily allowances are not paid for “mini-trips” around Russia. Leaving an employee completely without money, even on a one-day business trip, is not the best idea, even if it is legal. How can you get out of the situation?

Payment of travel expenses to public sector employees

Today, there are two options for paying expenses to public sector employees:

- Paid before departure of the trip. In this case, the preliminary amount that is given to the employee is determined. Thus, the employee is already provided with funds. This is exactly how everything should be done according to the law. The main problem is that you need to report on the first day, sometimes this is not very convenient.

- Payment is made based on the documents provided regarding the costs incurred. An employee goes on a business trip with his own money. If this is a long business trip, then this option is not entirely suitable for the employee, since you need to have a good budget with you.

Travel expenses are the costs of an employee while on a business trip on behalf of the employer far from his place of residence. In turn, there are several types of travel expenses.

At the end of the business trip, it is important to provide supporting documents on the basis of which the payment of daily allowance and other expenses incurred is made. Daily allowance payment rates are regulated within the company based on existing regulations.

Watch the video in which a specialist explains how to calculate travel allowances:

Payments for one-day business trips instead of daily allowances

The employer, at its own decision, can pay the employee a certain amount instead of daily allowance.

| Conclusion: daily allowance for one-day business trips in 2016: abroad - in the amount of 50% of the daily allowance for business trips abroadinstalled in your company's local documents; in Russia - in general, they are not paid, but you can set the payment to the employee yourself. |

How are payments calculated?

Each company sets its own daily payment standards. To do this, management has to rely on the laws of the Russian Federation. Depending on the financial condition of the company, the amount of payments annually may change slightly for the better. Typically, such amounts are prescribed in a memo or order of the enterprise itself. At the same time, depending on the region of the future business trip or the status of the employee, a differentiated approach may be used when calculating payments. Daily allowances in 2021, as in all previous periods, must be taken into account in the expenses of the institution itself. If someone notices an increase in such payments, management can always be interested in such a fact. In this case, the employee must have at hand all the expenses incurred during the trip. True, the current legislation does not specify anywhere regarding the need for documentary evidence of funds spent during a business trip.

Personal income tax on daily allowances for one-day business trips

Previously, the situation with the taxation of daily allowances and reimbursement of other expenses for one-day business trips was controversial. Today we can say with confidence that the situation has stabilized and the general trend is as follows: payments for one-day business trips are not subject to personal income tax. However, the positions of different departments differ:

Opinion of the Ministry of Finance of the Russian Federation: compensation for documented expenses associated with a one-day business trip (for example, food expenses) may not be subject to personal income tax in full. If there is nothing to support such expenses, then they are exempt from tax up to 700 rubles. for domestic Russian business trips and 2500 rubles. during a one-day business trip abroad (letter of the Ministry of Finance of Russia dated March 1, 2013 No. 03-04-07/6189).

Opinion of the Supreme Arbitration Court of the Russian Federation: money paid to an employee (called daily allowance) is not such by virtue of the definition contained in labor legislation, however, based on its focus and economic content, it can be recognized as reimbursement of other expenses associated with a business trip, made with the permission or knowledge of the employer , and therefore are not income (economic benefit) of an employee subject to personal income tax (Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated September 11, 2012 No. 4357/12).

If the advance is issued in foreign currency

According to clause 10 of the Regulations, when an employee is sent on a business trip, he is given a cash advance to pay for travel expenses and rental accommodation and additional costs associated with living outside his place of permanent residence (daily allowance). In this case, the advance can be issued in cash, both in rubles and in foreign currency.

By virtue of clause 16 of the Regulations, payment and (or) reimbursement of employee expenses in foreign currency related to a business trip outside the territory of the Russian Federation, including payment of an advance in foreign currency, as well as repayment of unspent advance in foreign currency issued to an employee in connection with a business trip, are carried out in in accordance with Federal Law No. 173-FZ.

In paragraph 1 of Art. 9 of this law, on the one hand, states the general rule prohibiting currency transactions between residents, and on the other, exceptions to this rule are provided. In particular, it is permitted to carry out transactions in foreign currency when paying and (or) reimbursement of expenses of an individual associated with a business trip outside the territory of the Russian Federation, as well as transactions when repaying an unspent advance issued in connection with a business trip (clause 9, clause 1 of the said articles).

As follows from clause 2.1 of the Directive of the Central Bank of the Russian Federation No. 2054-U, the issuance of cash foreign currency to a legal entity is carried out from its bank foreign currency account on the basis of a letter for its receipt.

When transactions are carried out in foreign currency in accounting, they are reflected in the currency of payments and in rubles (clause 4, 20 PBU 3/2006 “Accounting for assets and liabilities, the value of which is expressed in foreign currency”). Conversion of foreign currency at the organization's cash desk is carried out at the rate of the Central Bank of the Russian Federation in effect on the date of the transaction (clauses 5 - 7 of PBU 3/2006).

It happens that the receipt of money at the organization's cash desk from a foreign currency account and its withdrawal from the cash register as an advance to a posted worker occur on different days. At the same time, the exchange rate of foreign currency against the ruble changes. In this case, exchange rate differences arise. These differences also occur when returning part of the unspent advance amount in foreign currency, if the exchange rate on the date of return is different from the rate on the date of issue of the advance.

In accounting, exchange rate differences are reflected as part of other income (clause 7 of PBU 9/99 “Income of the organization”) or other expenses (clause 11 of PBU 10/99 “Expenses of the organization”), in tax accounting – as part of non-operating income (clause 11, Article 250, paragraph 7, paragraph 4, Article 271 of the Tax Code of the Russian Federation) or non-operating expenses (paragraph 5, paragraph 1, Article 265, paragraph 6, paragraph 7, Article 272 of the Tax Code of the Russian Federation).

On what date is the foreign currency exchange rate to the ruble taken for the purpose of accepting expenses in accounting and tax accounting?

According to clause 3 of PBU 3/2006, the date of a transaction in foreign currency is the day the organization has the right, in accordance with the legislation of the Russian Federation or an agreement, to accept for accounting the assets and liabilities that are the result of this transaction.

For the organization's expenses in foreign currency related to business trips outside the territory of the Russian Federation, this date will be the day of approval of the advance report (appendix to PBU 3/2006).

Expenses expressed in foreign currency are recalculated for tax purposes into rubles at the official rate established by the Central Bank of the Russian Federation on the date of their recognition (clause 10 of Article 272 of the Tax Code of the Russian Federation). For business trip expenses, this is the date of approval of the advance report (clause 5, clause 7, article 272 of the Tax Code of the Russian Federation).

Thus, when recognizing expenses for foreign business trips in foreign currency as expenses, there are no differences between accounting and tax accounting.

Example 2

The organization sent its employee on a business trip abroad from January 27 to January 31, 2015.

On January 27, 2015, an amount of 1,000 euros was withdrawn from the foreign currency account. On the same day, the money was given to the employee on account.

The employee returned from a business trip on January 31, and on February 2 he submitted an advance report in the amount of 990 euros and handed over unspent currency in the amount of 10 euros.

The euro to ruble exchange rate established by the Central Bank of the Russian Federation was:

– 01/27/2015 – 73.5633 rubles/euro;

– 02.02.2015 – 78.1105 rubles/euro.

The following entries will be made in the organization's accounting:

| Debit | Credit | Amount, rub. | |

| 27.01.2015 | |||

| Currency funds were received from the bank for issue on account (1,000 euros x 73.5633 rubles/euro) | 50-v* | 52 | 73 563,3 |

| Currency was issued to a posted worker for reporting (1,000 euros x 73.5633 rubles/euro) | 71 | 50-1 | 73 563,3 |

| 02.02.2015 | |||

| The amount of travel expenses is reflected (990 euros x 78.1105 rubles/euro) | 26 | 71 | 77 329,4 |

| The unspent advance amount was returned to the cash desk by the accountable person (10 euros x 78.1105 rubles/euro) | 50-1 | 71 | 781,1 |

| The positive exchange rate difference from currency translation is reflected (1,000 euros x (78.1105 - 73.5633) rubles/euro) | 71 | 91-1 | 4 547,2 |

* To account 50 “Cash desk” a sub-account “Cash desk in foreign currency” is opened. In this case, analytics is carried out for each currency used.

The tax accounting of the organization will reflect:

- other expenses associated with production and sales – 77,329.4 rubles;

- non-operating income – 4,547.2 rubles.

Report on daily allowance for a business trip

Upon returning from a business trip, the employee must submit to the employer within three working days:

- an advance report on the amounts spent in connection with the business trip;

- final payment for the cash advance issued to him before leaving for a business trip for travel expenses (clause 26 of the Business Travel Regulations No. 749).

| Important: as part of the advance document, the employee is not required to report either daily allowances within Russia, or daily allowances outside the Russian Federation, or for one-day or any other business trips. There are no supporting documents for daily allowance. The employer pays a daily allowance of x rubles, the employee spends it at his own discretion. |

Filling out a time sheet

In this document, the employer undertakes to indicate the working days worked by the employee during the business trip. Such days must be indicated in the timesheet, either with the code “K” or “06”.

It happens that an employee was forced to work on weekends or holidays. In this case, the document must be marked with the code “РВ” or “03”, if this has all been agreed upon with the authorities. If not, then management has the right not to note anything on the timesheet and not to pay for the hours worked by the employee on a day off.

Many people do not take into account, as working time, the time an employee spends on the road, for example, driving on a day off. Unfortunately, entrepreneurs really don't have to take this time into account. But in all fairness, of course, it is better to mark such time as “RV” or “03”.