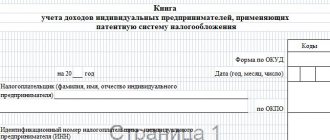

KUDIR is a book of income and expenses that must be maintained by all organizations and individual entrepreneurs using the simplified tax system (Article 346.24 of the Tax Code of the Russian Federation). There is no need to certify the book with the tax office, however, in case of any questions regarding the annual declaration, tax authorities can request the accounting book for a more thorough check. Errors in KUDIR or its absence are grounds for a fine of at least 10 thousand rubles (Article 120 of the Tax Code of the Russian Federation and Article 15.11 of the Administrative Code).

KUDIR is maintained according to the form approved by order of the Ministry of Finance of the Russian Federation dated October 22, 2012 No. 135n. KUDIR for individual entrepreneurs using the simplified tax system is the main tax accounting document. Simplified organizations, in addition to tax accounting in KUDIR, also maintain mandatory accounting. Taxpayers determine their tax base for the simplified tax on the basis of KUDIR, so if you combine several tax regimes, then you need to keep records of income and expenses under the simplified tax system separately from the other tax regime.

The general rules for registering and filling out KUDIR are as follows:

- for each tax period (that is, calendar year) - a new KUDIR;

- entries in the book are kept cumulatively in chronological order;

- KUDIR is filled out using the cash method, that is, only the actual movement of money in the cash register or in the current account is taken into account. If you have only shipped the goods to the buyer, but have not received payment, this is not yet recognized as income for the cash method of accounting. Similar rules apply for expenses;

- KUDIR is maintained on a computer, in a special accounting program or by hand;

- amounts are entered into the book in rubles and kopecks;

- The electronic KUDIR is printed at the end of the tax period;

- a printed electronic KUDIR or a handwritten paper one must be numbered, laced, sealed with the signature of the manager or the individual entrepreneur himself and a seal (if any);

- in a handwritten KUDIR, errors are corrected as follows: the incorrect entry is crossed out, the correct wording is written next to it, certified by the position, full name and signature of the person responsible, and the date the correction was made is recorded.

KUDIR consists of 4 sections plus a title page. In section I of the book, the taxpayer indicates income and expenses, in section II - expenses for the purchase of fixed assets and intangible assets, section III includes losses from previous years, by which the current tax can be reduced, section IV is devoted to expenses that reduce the amount of tax. Sections II-III should be filled out only for the simplified taxation system Income minus expenses, and section IV is intended only for the simplified taxation system Income. Let's take a closer look at how to conduct KUDIR with the simplified tax system of 15% and 6%.

The latest changes to KUDIR were approved by order of the Ministry of Finance of Russia dated December 7, 2016 No. 227n, and are effective from January 1, 2021. In 2021, the income book is filled out in accordance with this order.

Free accounting services from 1C

Filling out KUDIR under the simplified tax system Income

Since the taxpayer uses the simplified tax system for income only to take into account his own income, then in section I of KUDIR he will reflect only receipts to the current account or to the cash desk. At the same time, not any money received is taken into account as income for determining the tax base. According to Art. 346.15 of the Tax Code of the Russian Federation, the simplifier takes into account as income his revenue and non-operating income - rental of property and other income from Art. 250 Tax Code of the Russian Federation. The list of income that cannot be taken into account on the simplified tax system is given in articles 224, 251, 284 of the Tax Code of the Russian Federation.

This list is long, most of the income is very specific. Let us point out the most typical for the daily activities of most businessmen: money received from the Social Insurance Fund to reimburse the costs of child benefits and sick leave for employees, the return of advances or any overpaid amounts, the amount of loans received, or the return of a loan issued by the organization itself cannot be considered income.

Individual entrepreneurs have even more nuances when accounting for taxes on income received under the simplified system. The entrepreneur does not take into account in the KUDIR according to the simplified tax system his income as wages for hire, replenishment of the cash register of his own enterprise. The sale of property not used in business activities (for example, a car or apartment) is also not included in income when calculating the tax base.

How to conduct KUDIR with the simplified tax system of 6%? Income receipts are reflected by registering the PKO, payment order or bank statement. If revenue is deposited according to BSO, then one receipt order can be made for several forms, but provided that the forms were issued within one business day. If you need to reflect the return of money to the buyer in KUDIR, then this amount must be entered in the “income” column with a minus sign.

Another nuance of filling out KUDIR according to the simplified tax system for income is filling out section IV. Since the taxpayer can reduce the amount of tax on insurance premiums using the simplified tax system for income, the amount of these contributions should be reflected in section IV of the KUDIR. The book contains information about the payment document, the period for payment of contributions, the category of contributions and their amount. Entrepreneurs in this section indicate not only contributions for employees, but also their own pension and health insurance. Based on the results of each quarter, as well as half a year, 9 months and a calendar year, results are summed up.

How to make sure that expenses are included in the KUDiR in a timely manner for purchased goods?

- home

- About company

- Articles

- How to make sure that expenses are included in the KUDiR in a timely manner for purchased goods?

December 9, 2020

The procedure for recognizing expenses can be checked in the Taxes and reports for the organization section in the simplified tax system

—

Procedure for recognizing expenses

.

In Expenses for the purchase of goods, it is necessary to note: Receipt of goods, Payment of goods to the supplier and Sales of goods. Additionally, you can set the conditions for receiving income (payment from the buyer), that is, the data will go to KUDiR at the time of receiving payment from the buyer.

When applying the simplified tax system, always in the Accounting Policies

The organization uses the FIFO method for assessing inventories.

Checkout in the Purchases

new arrival, purchase of goods. In document movements, a posting is generated in the form of 41 accounts, since batch accounting will always have three sub-accounts: goods, warehouse and batch (receipt document). The batch is also an analytics on account 60 (settlements with suppliers), where the fact of payment is tracked in the context of the receipt document.

At the time of receipt, records of income and expenses are not generated. The formation procedure can be checked in the Book of Income and Expenses

in the

simplified tax system

.

In the Sales

—

Implementation

, go to the desired document. The implementation date must be after the receipt date. Carry out a sale, in the movements you will see that on the credit of 41 accounts, a write-off of goods by batch has been formed. But at the same time, no new entries appeared in the Book of Income and Expenses, since the goods were not paid for.

Based on the Receipt, generate a Write-off from the current account, indicating a date later than the sale. Run the count.

In the document movements, you will see analytics on receipts, closing the debt on invoice 60 to the supplier and generating expenses for part of the goods sold, since this was the last sale. Pay attention to the wording:

Check the Book of Income and Expenses; it should contain an entry for the cost of the goods.

In the case of a different sequence of documents, the wording of the KUDiR record will change.

Cancel the debit from your current account, then pay for the goods and complete the sale. In the book of income and expenses, an entry will be generated only for the cost of goods. The wording of the entry is different:

The record is generated according to the last operation for only part of the cost.

If all goods are sold, the full cost price will be displayed in the income and expenses ledger.

What mistakes can be made?

If you have in the Administration

—

Documentation

includes the possibility of writing off inventories in the absence of balances according to accounting data, that is, you can carry out sales in the absence of goods.

In this case, the amount and batch for the product will not be displayed in document movements. Accordingly, this entry will not be included in the book of income and expenses, since there is no receipt. If you create such records, then check the availability in the account, warehouse and by item.

If the product is in stock, but the record is not generated or is generated incorrectly

, then you need to check whether there is any debt to the supplier for the previous period. In this case, the debt will be closed chronologically.

If it is not possible to adjust the debt, you can indicate in the payment document that this payment pays off the debt under a specific document.

We recommend checking the Turnover Balance Sheets for account 41 to avoid errors.

In the settings for them, always fully disclose analytics for all possible subaccounts.

Check that there are no negative balances for positions and batches.

Similarly with account 60 for accounts payable.

Work with pleasure!

Example of filling out KUDIR on the simplified tax system Income 6%

Individual entrepreneur I.M. Kuznetsov bought raw materials for the production of buns for 230,000 rubles on January 11, 2016 and sold 100 buns at a price of 20 rubles per piece. The buyer returned one bun to the entrepreneur due to broken packaging. In addition, IP Kuznetsov received an advance from the buyer in the amount of 10,000 rubles. Kuznetsov has one pastry chef whose salary is 30,000 rubles. For January 2021, Kuznetsov paid insurance premiums for the employee - 9,000 rubles.

Here is what a sample of filling out KUDIR for individual entrepreneurs on the simplified tax system of 6% looks like in this example.

Filling out KUDIR under the simplified tax system Income minus expenses

Income in KUDIR is reflected in the same way, regardless of the selected simplified tax system option. But expenses are reflected in section I only under the simplified tax system: Income minus expenses. The list of expenses that can be taken into account in KUDIR is in Appendix 2 to the order of the Ministry of Finance of the Russian Federation dated October 22, 2012 No. 135n and in Art. 346.16 Tax Code of the Russian Federation. Since expenses reduce the tax base under the simplified tax system, tax authorities carefully check the company’s expenses and regularly issue letters and explanations: which expenses can be taken into account and which cannot. The general principle is that expenses can be accepted only if they are economically justified, documented and will generate income for the taxpayer.

When calculating the single tax, the payer of the simplified tax system can take into account material costs, labor costs and compulsory social insurance of employees and some other expenses. Each listed category of costs has its own characteristics, for example, costs for the purchase of goods fall into KUDIR only after they directly entered the warehouse, were paid to the supplier and sold to the buyer. Insurance premiums for employees under the simplified tax system. Income minus expenses do not reduce the calculated tax itself, but are included in the tax base as expenses in full.

Please note that personal expenses of an individual entrepreneur on the simplified tax system. Income minus expenses not directly related to making a profit cannot be entered into KUDIR.

How to configure KUDiR in 1C 8.3

Before you start creating KUDiR in 1C 8.3, you need to make a number of settings. This will avoid incorrect filling. Let's open and configure the accounting policy.

Where is the income and expense accounting book in 1C 8.3? Let's move on: Main - Settings - Accounting policies:

Then you need to select the one you need from the list of organizations and open its accounting policy:

If the object of taxation is set to Income minus expenses, then in 1C 8.3 access to the button Procedure for recognizing expenses is activated:

This function is used to select events that are needed in order to recognize expenses as reducing the tax base for a single tax:

Some events have a checkbox that cannot be unchecked. This means that an event must occur in order for an expense to be recognized. Other checkboxes can be checked or unchecked depending on the needs of the organization:

- To enter material expenses into KUDiR, you need to check the boxes: receipt of materials and payment of materials to the supplier.

According to current legislation, to account for the costs of acquiring material assets, there is no need to check the boxes Transfer of materials to production and Reducing costs for the balance of work in progress.

- To recognize and include expenses for the purchase of goods in KUDiR, the following events are necessary: receipt of goods, payment of goods to the supplier and sale of goods.

According to current legislation, expenses for payment of the cost of goods purchased for further sale are recognized as these goods are sold. Therefore, to account for these expenses, you need to check the Sales of goods checkbox.

The Receipt of income (payment from the buyer) flag can be omitted without fear of consequences, thanks to amendments to the legislation since 2011.

- To reflect incoming VAT in KUDiR, you need to check the following boxes: VAT submitted by the supplier and VAT paid to the supplier.

Also in this section there is also a checkbox Accepted expenses for goods (works, services). Each organization decides whether to install it or remove it independently. If you do not check the box, then the incoming VAT will go to KUDiR without waiting for implementation.

- For additional expenses included in the cost price, the main points are: Receipt of additional. expenses and payment to the supplier. If these 2 conditions are met, then the expenses will be reflected in the KUDiR without waiting for the inventory to be written off.

If you check the Write-off of inventories (this includes additional expenses) checkbox, the following condition will be met: additional. expenses will wait for sale and when the write-off (sale) of goods occurs, then additional expenses will be added. expenses will be in KUDiR.

- For customs payments, the following are considered mandatory: The import of goods has been formalized and Customs duties have been paid.

There is also a third checkbox: Products written off. If it is supplied, then customs payments will be included in the expenses and will appear in the KUDiR only after the goods are sold. There is a certain document (Letter of the Federal Tax Service of the Russian Federation for Moscow dated August 3, 2011 No. 16-15/0759978), which prescribes doing exactly this. Therefore, it is better to check the box to avoid tax claims.

For more details on how to set the procedure for recognizing expenses in the parameters of the Accounting Policy under the simplified tax system in 1C 8.3 Accounting 3.0, read our article. Or watch our video tutorial:

Now you need to go to KUDiR and directly configure it in 1C 8.3. KUDiR is located in the section Reports - Simplified Tax System - Book of Income and Expenses of the Simplified Tax System:

In the book form itself, click on Show settings:

To display detailed transcripts of strings, you need to check the Show transcripts checkbox:

What inaccuracies can be made when determining the costs of acquiring fixed assets for tax accounting when applying the simplified tax system “Income minus expenses”, see our video:

Example of filling out KUDIR under the simplified tax system Income minus expenses

Let's look at an example of how to fill out KUDIR for individual entrepreneurs on the simplified tax system of 15%. Data on income and expenses of individual entrepreneur I.M. Kuznetsova Let's take from the previous example. Plus, Kuznetsov paid in advance the rent for the bakery premises in January - 100,000 rubles for February-March 2021. The rent advance in KUDIR is included not on the date of transfer of money, but on the date of fulfillment of the counter-obligation, that is, the signing of an act on the provision of rental services on the last day of March 2021.

In this example, a sample of filling out KUDIR for an individual entrepreneur on the simplified tax system of 15% will look like this.

In the sample documents on our website you can download KUDIR according to the simplified tax system. If you have questions about how to fill out the KUDIR according to the simplified tax system, we recommend that you seek a free consultation from 1C:BO specialists.

How to fill out KUDiR in 1C 8.3

Now, after all the settings have been made, we will create KUDiR.

Important! Let us remind you once again that before forming KUDiR in 1C 8.3, it is necessary to close the month and restore the sequence.

On the title page of KUDiR, in addition to other information about the organization, it is necessary to ensure that the Taxable Object field is filled in.

KUDiR is divided into 4 sections:

- Income and expenses – income and expenses are recorded chronologically.

- Expenses on fixed assets and intangible assets - reflect the costs of the purchase, construction of fixed assets and intangible assets (only for enterprises that have chosen “income minus expenses”).

- Calculation of the amount of loss - losses are recorded that reduce the base for the single tax (only for enterprises that have chosen “income minus expenses”).

- Reducing the amount of tax - the insurance premiums paid “for oneself” and for employees, if any, are recorded, by the amount of which the simplified tax system tax is reduced (in the case of the simplified tax system “income”):

If the accounting policy settings are correctly completed, filling out KUDiR in 1C 8.3 will happen automatically and without any special difficulties. And the question will not arise why KUDiR is not formed in 1C 8.3.

How to avoid mistakes with the simplified tax system in 1C 8.3 and correctly reflect some types of income and expenses in KUDiR, read our article. Or watch the following video: