What's new

Adjustments to the form of the book of income and expenses from 2021 were made by orders of the Ministry of Finance of Russia dated December 7, 2021 No. 227n. Let's look at them in detail. Let us remind you that it was adopted by order of the Ministry of Finance dated October 22, 2012 No. 135n.

Order of the Ministry of Finance of the Russian Federation dated December 7, 2016 No. 227n was officially published on December 30, 2021. The updated ledger for accounting income and expenses must be used from January 1, 2021. That is, from the beginning of the tax period according to the simplified tax system.

Trade fee

Based on paragraph 8 of Article 346.21 of the Tax Code of the Russian Federation, “simplifiers”, even with the object “income”, have the opportunity to reduce their tax through deductions from the trade tax where it is valid (so far only in Moscow).

For these purposes, they keep a book of income and expenses. Since 2017, a separate 5th section has been introduced. It looks like this:

As you can see, all payments for the trade fee are given in chronological order.

Note that before the appearance of this section, the book form did not imply a reflection of the trading fee at all. Accountants had to keep in mind the imputed tax amounts and reduce the simplified tax by them even before entering it into the book. Now such a need has disappeared.

Seal

Since 2021, the Ministry of Finance has directly indicated that the book does not need to be certified with a seal if a company or individual entrepreneur on the simplified tax system prefers to abandon its own stamp.

Let us remind you that such an opportunity appeared for business companies on April 7, 2015 thanks to the Federal Law of April 6, 2015 No. 82-FZ.

Let us note that previously the accounting department had to print out the entire electronic book of income and expenses on the simplified tax system at the end of the year and affix the company’s stamp and signatures on it. For the period 2021 and 2017, this will also have to be done, but without the obligatory company stamp.

Profit of controlled foreign companies

From 2021, only the income of the simplifier himself should appear in the book in question. Let us recall that they are shown in the fourth column of the 1st section.

In the rules for filling out the book, the Ministry of Finance clarified that the profits of foreign companies controlled by the domestic simplifier in the book of income and expenses under the simplified tax system since 2017 .

The catch was that a completely different tax is paid on the profits of CFCs - on profits, and the register in question is kept only for the purposes of the simplified tax system. Meanwhile, the rule that CFC profits do not need to be included in the book has not been recorded anywhere.

IP "Revenue" without staff

The updated rules for filling out the book of income and expenses since 2017 have significantly simplified the corresponding obligation for businessmen without employees who use the “income” object and pay insurance premiums only for themselves.

From January 1, 2021, Article 430 of the Tax Code comes into force. And under the name “insurance premiums in a fixed amount” she combined:

- contributions based on minimum wage

- contributions in the amount of 1% of income over 300,000 rubles

This suggests that businessmen using the simplified tax system will be able to easily list in the book all their deductions for compulsory insurance: both from the minimum wage and 1 percent of income above the specified level.

Note that until 2021, controllers often took hostility to reducing the tax on the simplified tax system due to one-percent contributions. Hence, problems arose with filling out the book of income and expenses.

General procedure for accounting for income under the simplified tax system

The procedure for accounting for income under the simplified tax system, regulated by Art. 346.15 and 346.17 of the Tax Code of the Russian Federation , is fundamentally different from accounting for income under other tax regimes.

The basic rules for accounting for income during “simplification” are as follows:

- the procedure for accounting for income does not depend on the applied taxation object, that is, it is the same for both the “income” object and the “income minus expenses” object;

- income is taken into account, determined in the manner established by paragraphs 1 and 2 of Art. 248 Tax Code of the Russian Federation . Income includes income from the sale of goods (work, services) and property rights ( Article 249 of the Tax Code of the Russian Federation ) and non-operating income ( Article 250 of the Tax Code of the Russian Federation ). At the same time, the amounts of taxes presented in accordance with the Tax Code of the Russian Federation by the taxpayer to the buyer (purchaser) of goods (work, services, property rights) are excluded from income - we are talking about VAT billed by the “simplified”;

- Income specified in Art. is not taken into account. 251 of the Tax Code of the Russian Federation , as well as the income of an organization subject to corporate income tax at the tax rates provided for in clauses 1.6 , 3 and 4 of Art. 284 of the Tax Code of the Russian Federation , in the manner established by Ch. 25 of the Tax Code of the Russian Federation , and the income of an individual entrepreneur, subject to personal income tax at the tax rates provided for in paragraphs 2 , 4 and 5 of Art. 224 of the Tax Code of the Russian Federation , in the manner established by Ch. 23 Tax Code of the Russian Federation ;

- the cash method of accounting for income is applied, that is, the date of receipt of income is the day of receipt of funds in bank accounts or at the cash desk, receipt of other property (work, services) or property rights, as well as repayment of debt to the taxpayer in another way;

- A special procedure for accounting for income has been established:

– in the form of payments received to promote self-employment of unemployed citizens and stimulate the creation of additional jobs by unemployed citizens who have opened their own businesses,

– in the form of subsidies received in accordance with Federal Law No. 209-FZ dated July 24, 2007 “On the development of small and medium-sized businesses in the Russian Federation” (hereinafter referred to as Federal Law No. 209-FZ );

– in the form of financial support received from the budgets of the budget system of the Russian Federation under a certificate for attracting labor resources to the constituent entities of the Russian Federation;

- income is determined on the basis of primary documents and other documents confirming the income received by the taxpayer, and tax accounting documents.

Application of KUDiR

KUDiR - stands for a book of income and expenses under a simplified taxation system. Everyone who uses the simplified procedure is required to keep a book of income and expenses. In the book of income and expenses, organizations and individual entrepreneurs using the simplified tax system must reflect business transactions completed in the reporting (tax) period.

For each new tax period (year), you need to create a new accounting book (clause 1.4 of the Procedure approved by order of the Ministry of Finance of Russia dated October 22, 2012 No. 135n). The book of income and expenses is compiled in a single copy. Starting from 2021, you need to open a new book using a new form.

Composition of the new form: sections of the book

Starting from 2021, you need to use a new form of income and expense accounting book. Changes to KUDiR from 2021 were made by order of the Ministry of Finance dated December 7, 2016 No. 227n.

The book of income and expenses, used since 2021, consists of a title page and five sections:

- Section I “Income and Expenses”

- Section II “Calculation of expenses for the acquisition (construction, production) of fixed assets and for the acquisition (creation by the taxpayer himself) of intangible assets taken into account when calculating the tax base for the tax for the reporting (tax) period”

- Section III “Calculation of the amount of loss that reduces the tax base for the tax paid in connection with the application of the simplified taxation system for the tax period”

- Section IV “Expenses provided for in paragraph 3.1 of Article 346.21 of the Tax Code of the Russian Federation, reducing the amount of tax paid in connection with the application of the simplified taxation system (advance tax payments) for the reporting (tax) period”

- Section V “The amount of the trade fee that reduces the amount of tax paid in connection with the application of the simplified taxation system (advance tax payments) calculated for the object of taxation from the type of business activity in respect of which the trade fee is established for the 20__ reporting (tax) period”

as amended by order of the Ministry of Finance dated December 7, 2016 No. 227n (including a new form of the income and expenses accounting book).

General rules for maintaining KUDiR

The general rules that must be followed when registering KUDiR include the need to:

- keep a separate book for each tax period, including one for which there is no data to fill out;

- enter only information relevant to tax calculations;

- maintain the chronology of records;

- provide links to the details of specific primary documents that served as the basis for each of the entries;

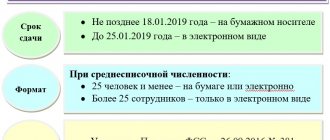

- prepare a paper copy of the book, regardless of which of the possible methods it was maintained (electronically or on paper);

- sew the book, number its pages, certify it with the signature of the head of the legal entity or individual entrepreneur and a seal, if used.

Read about the nuances of filling out KUDiR here.

When comes into force: controversial point

Changes to the form of the book according to the simplified tax system were made by order of the Ministry of Finance of Russia dated December 7, 2016 No. 227n. This Order comes into force after one month from the date of its official publication (published on December 30, 2016), but not earlier than the 1st day of the next tax period according to the simplified tax system. That is, from January 1, 2021. Some experts think so. However, we have a different opinion. Let me explain.

The calendar month after the publication of the said document is December 2021. This month ended December 31, 2021. The next day, January 2021 arrived. The changes come into force no earlier than the 1st day of the next tax period according to the simplified tax system. The tax period according to the simplified tax system is a calendar year. This means the new form of the book applies from January 1, 2021, and not from January 1, 2021.

Order of the Ministry of Finance of Russia dated December 7, 2016 No. 227n states that it comes into force precisely after the expiration of a month. And the month of publication is December 2021.

Rules for filling out KUDiR under the simplified tax system

KUDiR is always filled out in a single copy. When a new tax period (TP), namely the year, begins, a new Book is opened. This document can be maintained in paper form, as well as electronically.

If the Book was kept by the taxpayer in paper form, then before the moment of making relevant entries in it, it is necessary to:

- Create a title page

- Don't forget about stapling and page numbering

- The last page of the Book, which is completely numbered and bound, is filled with information regarding the pages contained in it

- Get certification directly from the head of the company/organization/individual entrepreneur

- Apply the seal of the company/organization

When maintaining this document in electronic form, at the end of each reporting/tax period it will need to be printed, in other words, transferred to paper.

Upon completion of the NP, perform the following manipulations:

- Print the document in its entirety

- Stitch it well, remembering to number the pages and indicate their total number on the last page of the Book.

- Have the certification signed by the head of the organization/company/individual entrepreneur

- Securing the signature with the appropriate seal

Here it is imperative to pay attention to the fact that certification of the Book by the tax office is no longer necessary, since it is not provided for by the Procedure.

What are the fines for KUDiR under the simplified tax system?

If the Book was not kept or the indicators were incorrectly reflected in it, violators will face liability based on Article No. 120 of the Tax Code of the Russian Federation. The fine in this case can vary from 10 thousand rubles. up to 30 thousand rubles

If it so happens that certain violations that were committed led to a decrease in the tax base, then the fine will be 20% of the amount of tax that was not paid, but not less than 40 thousand rubles.

KUDiR in electronic version

Today, there is an excellent opportunity to maintain a Book on the simplified tax system in electronic form (for example, in Excel). Alternatively, you can also use an online service that can be found on the Internet. This development is very convenient in that all Book data is stored not in accessible form, but in encrypted form. If necessary, you can log into the service using your password and login and print the document.

KUDiR sections

The book consists of four sections:

- Section No. 1: “Income and Expenses”

- Section No. 2: reflection of Expenses for the creation / acquisition of fixed assets, intangible assets

- Section No. 3: filled out by those who received any losses based on the results of previous tax periods

- Section No. 4: filled in only with “simplified” ones, distinguished by the “Income” object. This reflects insurance premiums paid by employees for benefits due to temporary disability, as well as payments based on a voluntary personal insurance agreement

Section No. 1 is supplemented with Help.

When filling out the first section, you must provide the following information:

- Column 1 – entering the serial number of the transaction that is being registered

- Column 2 – designation of the date, number of the primary document, which is the basis for receiving Income / registration of Expenses

- Column No. 3 – indicates the content of the operation that is being registered

- Column No. 4 – enter the amount of Income, which is taken into account during the calculation of the single tax

- Column No. 5 – enter the amount of Expenses, which is taken into account during the calculation of the single tax (necessary for those who pay tax on the difference between D/R). Those companies/organizations that use the “Income” object, based on the general rule, do not enter data regarding Expenses into the Book. However, since 2013, an exception to the above rule has been introduced. For simplified people who have an “Income” object, according to the new rules, it is necessary to reflect the amounts spent on subsidies (those that were allocated by companies / firms from the budget for certain purposes). Clause 2.5 of the Procedure provides for two types of such financing: the state is allowed to partially reimburse the Costs of creating additional jobs, and the budget can also allocate funds for the development of small/medium businesses

In other cases, based on the general rules, organizations / firms / individual entrepreneurs that pay a single tax on income must fill out exclusively the first section and only that part of it that concerns income.

Making corrections to KUDiR

Certain changes may be made to this document, but they must be supported by an appropriate basis for this. To carry out this operation, the organization must have strong arguments that can confirm the legality of the changes made (for example, primary documents, accounting statements, etc.). If the Book is maintained in paper form, then to correct the error you will need:

- Carefully cross out the mistake you made.

- Enter the correct value of the indicator next to it

- Add the change with the date of the manipulations performed

- Corrections must be certified by the signature of the head of the organization/company and sealed with the appropriate seal

The rules for adjusting KUDiR, which is maintained electronically, have not been officially established. However, in practice it looks like this: if this document was maintained electronically on a computer, you will need to delete incorrect values and enter others (correct ones).

Correct reflection of income in KUDiR

It is known that under the simplified tax system one should take into account income from sales, as well as non-operating income (their composition should be determined based on Articles No. 249, No. 250 of the Tax Code of the Russian Federation). Thus, only these amounts should be entered in column No. 4 of Section No. 1 of KUDiR.

This document does not require reflection of the revenues listed in Article No. 251 of the Tax Code of the Russian Federation. Also, if an organization / company is engaged in combining UTII and simplified tax system, then it should not show income from the activities that were transferred to pay UTII.

Income that was received in kind must be accounted for based on market prices. Thus, the market value of the property is entered in column No. 4, Section No. 1 of the Book. In this case, supporting documents will be considered acts of acceptance/transfer of property, accounting certificates in which calculations of the market value of the property were made.

Reflection of income in kind in KUDiR (example)

Liven LLC applies the simplified tax system and has the object “Income minus expenses.” The organization provides furniture repair and sale services.

The company entered into an exchange agreement, according to which it is obliged to ship a batch of tables for a total cost of 14.8 thousand rubles, in return for this, arrange for the receipt of materials (screws / screws / nails / nuts, etc.). Both parties transferred the property on January 16, 2017. The company’s accountant determined that the market value of the materials that were received was equal to the amount of 7,540 rubles. Since the property was recognized as unequal, the party transferring the materials transferred the difference in money on January 19, 2017. The income received should be reflected in the tax accounting of Liven LLC.

Thus, LLC “Liven” on January 16, 2017 must record in column 4 of section No. 1 KUDiR the market value of materials that were received within the specified time frame (RUB 7,540), and on January 19, 2017 – the amount of funds received from counterparty (that is, 14.8 thousand rubles - 7540 rubles).

Income that was received during the offset of mutual claims must be reflected in the KUDiR by the date of signing the act regarding the offset of mutual claims. According to Article No. 410 of the Civil Code of the Russian Federation, at the moment the buyer signs the act, his obligation is extinguished directly to the seller. Thus, the date of repayment of the obligation is the date of receipt of the corresponding income (Article No. 346.17, paragraph 1 of the Tax Code of the Russian Federation). The act of offsetting mutual claims is the basis for making certain entries in the KUDiR.

| No. | Date and number of the primary document | Contents of operation | Income taken into account when calculating the tax base | Expenses taken into account when calculating the tax base |

| 1 | 2 | 3 | 4 | 5 |

| … | … | … | … | … |

| 69 | Property acceptance and transfer certificate No. 13 dated 01/16/2017, accounting certificate No. 38 dated 01/16/2017 | The market value of materials is reflected in income | 7540 | — |

| 70 | Bank statement No. 41 dated January 19, 2017 | The amount transferred under the exchange agreement is reflected in income | 7260 | — |

| … | … | … | … | … |

Correct reflection of expenses in KUDiR

In column 5 of section No. 1 of KUDiR, “simplified” residents with the object “Income minus expenses” should enter the expenses that are listed in article No. 346.16, paragraph 1 of the Tax Code of the Russian Federation.

Reflection in KUDiR personal income tax in kind (example)

Liven LLC uses the simplified tax system and has the “D-R” facility. On 02/05/2017, the organization paid the second part of the salary to employees for January 2021 in the amount of 430.9 thousand rubles. The wages were paid from cash proceeds. On 02/06/2017, personal income tax withheld from employee income was transferred in the amount of 110,552 thousand rubles. The listed operations should be correctly reflected in the KUDiR.

The company/organization has every right on 02/05/2017 to take into account in the item of labor costs the amount of wages that were issued, without personal income tax (that is, 430.9 thousand rubles), and on 02/06/2017 - personal income tax, which was withheld and transferred to the budget (that is, 110,552 thousand rubles).

Since wages and personal income tax were transferred on different days, they must be reflected in separate entries in KUDiR.

| No. | Date and number of the primary document | Contents of operation | Income taken into account when calculating the tax base | Expenses taken into account when calculating the tax base |

| 1 | 2 | 3 | 4 | 5 |

| … | … | … | … | … |

| 123 | Payroll No. 7 dated 02/05/2017 | The paid salary is taken into account in expenses | — | 430 900 |

| 124 | Payment order No. 389 dated 02/06/2017 | Included in personal income tax expenses | — | 110 552 |

| … | … | … | … | … |

When reflecting in the KUDiR expenses for writing off the cost of certain goods, in addition to the payment order / cash receipt, which confirms payment for the corresponding goods, you should reflect the details of the accounting certificate justifying the date of writing off the cost of a particular product as an expense item. This rule is confirmed by Article No. 346.17, paragraph 2 of the Tax Code of the Russian Federation.

Reflection in KUDiR of the cost of goods sold (example)

LLC "Liven" applies the simplified tax system, has the object "Income minus expenses", and sells children's toys. On 03/06/2017, the store purchased construction sets (30 pieces) at a cost of 800 rubles. excluding VAT / piece. The selling price of one set is set at 1,400 rubles.

On March 13, 2017, 5 sets of this toy were sold. Cash for the goods sold was received from the buyer on March 16, 2017.

The previously mentioned transactions should be reflected in tax accounting. Thus, the purchase price of goods sold should be written off as an expense item after payment has been made to the supplier and sales to the buyer. For this reason, on March 13, 2017, the company has the right to include 4 thousand rubles in the expense item. (800 rub. x 5 pieces).

On March 16, 2017, income should be reflected in the amount of 7 thousand rubles. (1400 RUR x 5 pieces).

| No. | Date and number of the primary document | Contents of operation | Income taken into account when calculating the tax base | Expenses taken into account when calculating the tax base |

| 1 | 2 | 3 | 4 | 5 |

| … | … | … | … | … |

| 92 | Payment order No. 38 dated 03/06/2017, accounting certificate No. 15 dated 03/13/2017 | The purchase price of sold constructors is reflected in expenses | — | 4000 |

| 93 | Bank statement No. 118 dated March 16, 2017 | Revenue from the sale of constructors is included in income | 7000 | — |

| … | … | … | … | … |

When making an entry in KUDiR regarding normalized expenses, in addition to the payment order, you should also indicate the details of the bank certificate, since on its basis the amount that relates to expenses was calculated.

The cost of materials / raw materials of companies and organizations working on the simplified tax system have the opportunity to be taken into account in the expense item immediately after they have been capitalized and paid. Thus, waiting for goods/raw materials to be released into production becomes unnecessary. The above explanations are supported by letter No. 03-11-11/284 of the Ministry of Finance of the Russian Federation dated October 27, 2010.

Correctly filling out section No. 3 of KUDiR according to the simplified tax system

Completing section No. 3 KUDiR is required only if the following conditions are simultaneously met:

- Object of taxation – “Income that is reduced by expenses”

- Presence of losses in the reporting year / previous years

So, if one or another, “Income minus expenses,” but there were no losses, you do not need to fill out this section.

To begin with, experts recommend understanding why section No. 3 of KUDiR is provided for. Since companies/organizations working on the simplified tax system and having the object “Income minus expenses” should, at the end of the year, reduce the tax base under the simplified tax system by the amount of past losses that were received during the application of this special regime. Here you should immediately pay attention to the fact that this is not a right, but an obligation. If a reduction in the current year’s income by the amount of last year’s losses is unprofitable for someone, then the reduction in the tax base can not be reduced, but the losses can be carried forward to future periods (any loss can be written off within ten years).

For clarification, experts remind that losses include the amount of excess expenses that were taken into account directly over the amount of income received for the same period. And since writing off last year’s losses to reduce the current tax base under the simplified tax system is possible only based on the results of the year, section No. 3 of KUDiR should also be filled out only based on the results of the year. How to do this correctly?

Line 010 indicates the total amount of losses that were transferred from previous periods.

This amount is distributed in detail in lines 020-110, namely by year of occurrence.

Line 120 records the value of the tax base for the tax under the simplified tax system, the period is the current reporting year.

Line 130 indicates the amount of losses by which the organization/firm will reduce the current tax base. By the way, the indicator in this line must be less than the indicator recorded in line 010.

For reference, line 140 records the amount of losses for the current period. This amount can be determined by paying attention to line 041 of the certificate to section No. 1 of KUDiR. Companies/organizations can use this amount to reduce their tax base for the next year.

If in the current year the company/organization did not write off losses in full, then the total amount of unused losses should be indicated in line 150.

In lines 160-250 it is necessary to enter this amount by year of occurrence of certain losses.

An example of filling out Section III of the Income and Expense Accounting Book

Zvezda LLC has been applying the simplified tax system with the object of taxation being income minus expenses since 2012. For 2014 and 2015, the organization received losses in the amount of 110,500 rubles. and 183,400 rub. respectively. For 2017, the tax base under the simplified tax system (that is, the excess of income over expenses) amounted to 285,500 rubles. The organization decided to reduce the 2021 tax base by the amount of past losses. In previous years of application of the simplified tax system, the tax base for losses was not reduced. Let's fill out section III of the Accounting Book.

In line 010 we will show the total amount of past losses received when applying the simplified tax system. It is equal to 293,900 rubles. (RUB 110,500 + RUB 183,400).

In lines 020 and 030 we will write down the amounts of losses for 2014 and 2015.

In line 120 we will reflect the tax base for 2021 - 285,500 rubles. This is less than the amount of losses, and the accountant of Zvezda LLC decided to reduce the tax base to zero, that is, by 285,500 rubles. We will indicate this amount in line 130.

There will be a dash in line 140, since there are no losses for 2021.

The amount of unused losses is RUB 8,400. (293,900 rubles - 285,500 rubles) will be written in line 150. It can be kept in mind when calculating the tax base for the following periods. The losses received earlier are used first. Therefore, we will assume that the loss for 2014 has been fully utilized. And in line 160 we indicate the year 2015 and repeat the value of 8400 rubles.

Situation. The organization worked under the simplified tax system, then under the general regime, and then returned to the “simplified” regime. How to fill out section III of the Accounting Book

The tax base under the simplified system can be reduced only by losses received when applying the simplified tax system with the object of income minus expenses. Thus, losses incurred under the general regime for organizations and entrepreneurs who switched to the “simplified system” are not taken into account.

But sometimes it also happens that an organization worked on the simplified tax system with the object income minus expenses, then switched to the general regime, and then returned to the “simplified system” with the object income minus expenses. Question: is it possible to reduce the tax base for those losses that were received during the previous application of the simplified tax system? The answer is yes. If ten years have not passed since the receipt of losses, then it is allowed to reduce the tax base for them under the simplified tax system (clause 7 of article 346.18 of the Tax Code of the Russian Federation). It does not matter that they were obtained during the previous application of the “simplified procedure”, the main thing is that these were losses not of the general regime. namely the simplified tax system. The Russian Ministry of Finance shares the same opinion in letter dated January 28, 2011 No. 03-11-11/18.

The procedure for filling out KUDiR from 2021: changes made

The changes include the cancellation of certification of KUDiR with the seal of an individual entrepreneur if it is not available. There is also a clarification that in section No. 5 of the Book, entrepreneurs should indicate all insurance costs: contributions from the minimum wage / contributions from income.

Among other things, section No. 6 was added to the document. It should be filled out exclusively by trade tax (TC) payers with the “Revenue” object.

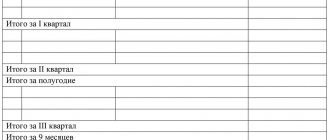

Section No. 6. The value of the TS, which reduces the amount of tax paid due to the application of the simplified tax system, calculated for the object of taxation directly from the type of business activity in relation to which the TS was established.

| No. | Date and number of the primary document | The period for which the trade fee was | trade fee paid |

| 1 | 2 | 3 | 4 |

| … | … | … | … |

| … | … | … | … |

| … | … | … | … |

| Total for the first quarter | … | ||

| … | … | … | … |

| … | … | … | … |

| … | … | … | … |

| Total for the second quarter | … | ||

| Total for the half year | … | ||

| … | … | … | … |

| … | … | … | … |

| … | … | … | … |

| Total for the third quarter | … | ||

| Total for 9 months | … | ||

| … | … | … | … |

| … | … | … | … |

| … | … | … | … |

| Total for the fourth quarter | … | ||

| Total for the year | … | ||

Section No. 6 KUDiR should be filled out by firms/organizations on the simplified tax system for “Revenue” objects. The amount of the vehicle that was paid is entered here.

Column 1 contains the serial number of the transaction that is being registered.

Column 2 is filled in with information regarding the date and number of the primary document on the basis of which the registered transaction was carried out.

In column 3 you should enter information about the period for which the vehicle payment was made.

In column 4, enter the amount of the vehicle that was paid.

Certification of KUDiR for 2021 and 2021 in the inspection: is it necessary?

Thus, it became known that the certification of the Book for 2021 and 2021 should not be done at the tax office.

Let us remind you that in the old KUDiR forms there were columns on the title page - tax officials’ marks were placed in them. The new form, which has been used since 2021, does not contain a corresponding line on the title page in which a representative of the tax office must sign.

These forms were approved by order No. 135n dated October 22, 2012 by the Ministry of Finance. Already from 01/01/2017, the changes described above will be made to the Book, but they do not at all affect its certification by tax authorities. In other words, the Book for 2021 is not certified by the Federal Tax Service.

KUDiR in 2021 (sample)

Income taken into account under the simplified tax system

The table provides explanations from representatives of the Ministry of Finance and the Federal Tax Service on the issue of accounting for income under the simplified tax system, which were given in 2021: the given income is taken into account when determining the tax base.

| Position of the supervisory authority | Document details |

| Income of homeowners associations, housing cooperatives, management companies | |

| Mandatory payments received to the account of the HOA, in particular the amounts of payments by homeowners (both members of the HOA and non-HOA members) for housing and communal services, as well as receipts from persons who are not members of the HOA, are taken into account as part of income when determining the object of taxation tax paid in connection with the use of simplified taxation system. If the entrepreneurial activity of the HOA, based on contractual obligations, is an intermediary activity for the purchase of housing and communal services on behalf of the owners of premises in an apartment building, the income of the HOA will be commission, agency or other similar remuneration | Letters of the Ministry of Finance of Russia dated January 27, 2017 No. 03-11-11/4260, dated July 3, 2017 No. 03-11-11/41853 |

| Article 251 of the Tax Code of the Russian Federation does not provide for the exclusion from the income of the management company of payments for utility services using increasing coefficients to the consumption standard for the corresponding service coming from consumers - owners of premises in apartment buildings. Accordingly, these amounts are taken into account in income under the simplified tax system. | Letter of the Ministry of Finance of Russia dated March 27, 2017 No. 03‑11‑06/2/17393 |

| The amounts of payments by homeowners for housing and communal services received into the account of a commercial organization must be taken into account as part of its income when determining the base for the tax paid in connection with the use of the simplified tax system. If the business activity of the management organization, based on contractual obligations, is an intermediary activity on behalf of the owners of premises in an apartment building for the purchase of utilities, the income of this organization will be a commission, agency or other similar remuneration. Income of management organizations (including homeowners' associations, housing cooperatives) in the form of payments by premises owners for utility services provided to them does not belong to targeted revenues and targeted financing. Therefore, these incomes are taken into account as income when determining the object of taxation paid in connection with the application of the simplified taxation system. If the entrepreneurial activity of the HOA (HCC), based on contractual obligations, is an intermediary activity for the purchase of housing and communal services on behalf of the owners of premises in an apartment building, the income of the HOA (HCC) will be commission, agency or other similar remuneration | Letters of the Federal Tax Service of Russia dated July 17, 2017 No. SD-19-3/ [email protected] , Ministry of Finance of Russia dated August 4, 2017 No. 03-11-11/49885, dated August 18, 2017 No. 03-11-11/53260 |

| Intermediary agreements | |

| The income of an individual entrepreneur - principal, received under commission agreements, is recognized as the entire amount of money received by the principal, including the commission agent's commission. The date of receipt of income for the principal will be the day the specified funds are received in bank accounts and (or) at the principal's cash desk | Letters of the Ministry of Finance of Russia dated April 20, 2017 No. 03‑11‑11/23918, dated June 15, 2017 No. 03‑11‑06/2/37038 |

| A taxpayer who uses the simplified tax system, carries out activities under an agency agreement and receives remuneration for services provided, when determining the tax base, takes into account only the amount of the agency fee | Letters of the Ministry of Finance of Russia dated June 27, 2017 No. 03-11-06/2/40301, dated August 14, 2017 No. 03-11-11/51901 |

| When determining the object of taxation when calculating the base for the tax paid in connection with the application of the simplified tax system, the income of the agent organization is the amount of the agency fee received. The date of receipt of income for the principal (supplier of goods, works, services) will be the day clients pay for the services provided to them, that is, the day payments are received from clients in accordance with the agency agreement to bank accounts and (or) to the agent’s cash desk or through a payment terminal | Letter of the Federal Tax Service of Russia dated 08/04/2017 No. SD-4-3/ [email protected] |

| The income of principals using the simplified tax system should not be reduced by the amount of agency fees withheld by the agent from sales proceeds received from buyers of goods. In this case, the principal’s income is the entire amount of revenue from the sale of services received to the agent’s account | Letter of the Ministry of Finance of Russia dated June 27, 2017 No. 03‑11‑06/2/40309 |

| Inventory results | |

| The cost of surplus goods identified as a result of inventory is included in the income taken into account when determining the base for the tax paid in connection with the use of the simplified tax system. The organization must take into account the income that will be received during the further sale of surplus goods identified as a result of the inventory when determining the base for the tax paid in connection with the use of the simplified tax system. | Letters of the Ministry of Finance of Russia dated May 18, 2017 No. 03-11-06/2/30304, dated August 24, 2017 No. 03-11-06/2/54380 |

| Compensations, subsidies | |

| The amount of monetary compensation received from the budget of the city of Moscow by the owner of a demolished real estate property that is an unauthorized construction is taken into account as part of income when determining the object of taxation paid in connection with the application of the simplified tax system in the reporting (tax) period of its receipt | Letters of the Ministry of Finance of Russia dated February 16, 2017 No. 03‑11‑06/2/8712, dated February 17, 2017 No. 03‑ 11‑06/2/9151 |

| Subsidies received by agricultural producers in order to reimburse the costs of purchasing agricultural equipment, in Art. 251 of the Tax Code of the Russian Federation are not named, therefore, they are subject to accounting when determining the base for the tax paid in connection with the use of the simplified tax system | Letter of the Ministry of Finance of Russia dated August 24, 2017 No. 03‑03‑07/54271 |

| Income not taken into account when determining the tax base for corporate income tax is defined in Art. 251 Tax Code of the Russian Federation . The list of such income is exhaustive. Subsidies received in accordance with Federal Law No. 209-FZ are not named in this list, and therefore are taken into account by taxpayers as part of income when determining the object of taxation paid in connection with the use of the simplified tax system | Letter of the Ministry of Finance of Russia dated September 28, 2017 No. 03‑11‑06/2/62961 |

| Leasing payments | |

| The amount of lease payments received under a financial lease (leasing) agreement is determined by taxpayers-lessors using the simplified tax system based on all receipts associated with payments for services sold. Thus, the entire amount of leasing payments (including the redemption price of the leased asset) is taken into account by taxpayers-lessors as part of income when determining the object of taxation paid in connection with the use of the simplified tax system | Letter of the Ministry of Finance of Russia dated 08/04/2017 No. 03‑11‑11/49896 |

| Rewards for the use of copyright and related rights objects | |

| The income of the copyright holder is the entire amount of remuneration for the use of objects of copyright and related rights. In this case, income is recognized at the time (on the date) of receipt of funds to the bank account and (or) to the cash desk of the copyright holder and related rights | Letter of the Ministry of Finance of Russia dated 03/01/2017 No. 03‑11‑11/11479 |

| Apartment cost | |

| A taxpayer applying the simplified tax system includes in income from the sale of goods (work, services) the cost of an apartment received as payment for services rendered, as well as the cost of the sold apartment | Letter of the Ministry of Finance of Russia dated July 17, 2017 No. 03‑11‑11/45308 |

| Rent payments and reimbursement of utility costs | |

| In the case when the activity of providing non-residential premises for rent is carried out within the framework of the simplified taxation system, rental payments from the owner of the leased premises - an individual entrepreneur are taken into account as part of income when determining the object of taxation paid in connection with the application of the simplified taxation system in the reporting (tax) period of their receipt | Letter of the Ministry of Finance of Russia dated February 14, 2017 No. 03‑11‑11/8272 |

| The amount of reimbursement of expenses for utility services is taken into account by taxpayers in income when calculating the base for the tax paid in connection with the use of the simplified tax system | Letters of the Ministry of Finance of Russia dated 03/21/2017 No. 03-11-11/16222, dated 05/22/2017 No. 03-11-06/2/31137, dated 09/28/2017 No. 03-11-06/2/62942 |

| Income of an individual entrepreneur | |

| Income in the form of interest received by an individual entrepreneur from carrying out business activities of providing loans is taken into account as part of income when determining the object of taxation paid in connection with the application of the simplified tax system | Letters of the Ministry of Finance of Russia dated March 22, 2017 No. 03-08-05/16586, dated August 1, 2017 No. 03-11-11/48831, dated February 17, 2017 No. 03-11-11/9073 |

| An individual entrepreneur using the simplified tax system, when receiving income from the assignment of the right of claim under an agreement for participation in shared construction to an individual, takes this income into account when determining the tax base | Letter of the Ministry of Finance of Russia dated July 18, 2017 No. 03‑11‑11/45709 |

| If the land plot and the buildings located on it were used by an individual entrepreneur in business activities, income from the sale of this property should be taken into account as part of income when determining the tax base paid in connection with the use of the simplified tax system | Letter of the Ministry of Finance of Russia dated May 16, 2017 No. 03‑11‑11/29521 |

| A taxpayer applying the simplified tax system, when determining the tax base, determines income from sales taking into account the proceeds from the sale of property previously used in business activities, regardless of the use of the current or current account of an individual registered as an individual entrepreneur for the purpose of selling such property | Letters of the Ministry of Finance of Russia dated October 18, 2017 No. 03-11-11/68158, dated October 25, 2017 No. 03-11-11/70108 |

| Date of receipt of income | |

| When individuals pay for the services of an organization using the simplified tax system through bank branches, income is taken into account on the date of receipt of funds into its current account | Letter of the Ministry of Finance of Russia dated October 5, 2017 No. 03‑01‑15/65071 |

| The date of receipt of income by an organization that uses the simplified tax system and is not a participant in the budget process is the date the funds are credited to the organization’s current account | Letter of the Ministry of Finance of Russia dated July 26, 2017 No. 03‑11‑06/2/47414 |

| The date of receipt of income by a construction organization - contractor, payment for the services of which is carried out by the customer by concluding agreements for shared participation in the construction of housing, is the date of signing by the parties of the act of offset of counterclaims. In the event that the customer transfers equity participation agreements to the contractor as an advance payment for the upcoming construction work of the contractor, the date of receipt of the contractor's income is the date of receipt of the specified contracts from the customer. When the contractor assigns the right of claim under equity participation agreements to individuals and receives funds, the date of receipt of income is the date of receipt of funds to the current account and (or) to the contractor’s cash desk. | Letter of the Ministry of Finance of Russia dated July 31, 2017 No. 03‑11‑11/48724 |

| The date of receipt of income by an organization that uses the simplified tax system and is a contractor under a government contract is the date the funds are credited to the organization’s bank account | Letter of the Ministry of Finance of Russia dated October 20, 2017 No. 03‑11‑06/2/68759 |

KUDiR forms

Depending on the taxation system in 2021, the following forms for the book of income and expenses are used:

- KUDiR for simplified taxation system (suitable for individual entrepreneurs and organizations)

- KUDiR for OSN

- KUDiR for Unified Agricultural Tax

- KUD (income book) for PSN

Filling out KUDiR

Basic rules for conducting KUDiR:

- For each tax period, a new book of income and expenses is opened.

- Each operation is entered in chronological order on a separate line and confirmed by the appropriate document (agreement, check, invoice, payment order, etc.)

- Replenishment of the account, increase in the authorized capital are not recognized as income and, accordingly, are not entered into the KUDiR.

- KUDiR can be used in paper or electronic form. When maintaining a book in electronic form, at the end of the tax period, KUDiR must be transferred to paper media

- The book must be laced, numbered and confirmed by the manager’s signature and seal (if any)

- Unfilled sections of KUDiR are still printed and stapled in the general order

- In the absence of activity, profit or expenses, individual entrepreneurs and organizations must still have zero KUDiR

Results

Maintaining KUDiR, according to which tax is calculated, is mandatory when applying the simplified tax system.

The form of this book and the basic rules for filling it out are valid for both objects for calculating the simplified tax system. A peculiarity of the design of KUDiR under the simplified tax system “income minus expenses” is that 3 sections out of 5, forming the main part of the book, are intended for this taxable object. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.