The obligation of enterprises is to submit to the Federal Tax Service information on the income of personnel and individuals working under civil servants' agreements. This information is reflected in Form 2-NDFL certificates compiled for each employee who received payments - wages, compensation, incentives, etc. If the submitted certificates for the reporting year or other earlier periods reveal erroneous or unreliable data, the company will have to submit corrected information. Let's talk about how to correctly submit an adjustment for 2-NDFL.

Adjustment of 2-NDFL for 2021

No one is immune from annoying mistakes; they can be made in writing a person’s full name, date of birth, tax identification number, passport data, certificate codes, as well as in the amounts of income received and deductions due.

Is it possible to submit an adjustment for 2-NDFL? Not only is it possible, but it is also necessary. Moreover, the company will not have to re-issue a complete block of information on the enterprise due to inaccuracies in one or more certificates. Since 2-NDFL certificates are compiled for each employee, if an error is made in a certain document, the adjustment can only be submitted based on it.

Any error found must be corrected, except for changes that occurred after the information was submitted to the Federal Tax Service. For example, a change in personal information when changing a passport, which occurred after submission to the tax office, is not considered a company error and is exempt from filing adjustments in this regard.

Responsibility

According to the law, the fine for adjusting 2-personal income tax is 500 rubles for each certificate (Article 126.1 of the Tax Code of the Russian Federation). It does not threaten you if you manage to find the error before the Federal Tax Service and submit the correct version of the certificate. But if you do it ahead of schedule - before 04/02/2018 - it will not save you from a fine! (see letter of the Ministry of Finance dated June 30, 2016 No. 03-04-06/38424).

Section 2 of the income certificate with information about the individual: how to make a 2-NDFL adjustment in “Taxpayer” if the personal information, along with the change of passport, was updated after the certificates were submitted to the Federal Tax Service? It's simple: this is not considered an error. It is also not necessary to send the correction.

And vice versa: if at the time of filling out the corrective certificate 2-NDFL for previous tax periods, a person’s personal data has changed, Section 2 must be filled out taking into account these changes (letter of the Federal Tax Service dated March 27, 2018 N GD-4-11/5667).

What is an adjustment to a 2-NDFL certificate for the Federal Tax Service?

In addition to the necessary correction of information in the submitted certificate, the adjustment form must differ from the original one in the date and correction code. Here are the rules to follow when making adjustments:

- When submitting the primary form 2-NDFL, “00” is entered in the “Adjustment code” field; each corrected certificate is coded in numerical order - 01, 02, etc. the number of possible adjustments can be any – up to 98;

- The corrected document is submitted in the form that was valid in the period for which the information is corrected;

- The 2-NDFL certificate number remains unchanged during the adjustment, i.e., the same number that was assigned to the primary form;

- The 2-NDFL adjustment is dated to the actual date of preparation.

In addition, in order to avoid unnecessary questions from the Federal Tax Service, it is advisable to attach a cover letter listing the corrections made to the corrective certificates.

Deadline for submitting 2-NDFL certificates and penalties for violations

Certificate 2-NDFL with feature 2 must be submitted no later than March 1 of the year following the year of payment of income, and a certificate with feature 1 must be submitted no later than April 1 (clause 5 of Article 226, clause 2 of Article 230 of the Tax Code of the Russian Federation).

Thus, for 2021 you must submit 2-NDFL certificates (clause 7, article 6.1 of the Tax Code of the Russian Federation):

- with sign 2 – no later than 03/01/2018;

- with sign 1 – no later than 04/02/2018 (April 1, 2017 – a day off).

If you do not submit 2-NDFL certificates on time, then two fines may be imposed simultaneously:

- per organization – in the amount of 200 rubles. for each certificate (clause 1 of article 126 of the Tax Code of the Russian Federation);

- for an official of the organization - in the amount of 300 to 500 rubles. (Part 1 of Article 15.6 of the Code of Administrative Offenses of the Russian Federation).

If the Federal Tax Service discovers that the 2-NDFL certificate contains false information, for example, an incorrect TIN (assigned to another person), a fine of 500 rubles will be imposed on the organization.

for each certificate with errors. A fine for false data can be avoided if the tax agent independently identifies an error in the 2-NDFL certificate for 2021 and submits a corrective 2-NDFL certificate in a timely manner (before the Federal Tax Service Inspectorate finds the error).

Correction number 99 in certificate 2-NDFL

It happens that a company submits information that does not need to be corrected, but simply cancelled. For this purpose, a special correction code is provided - 99. By entering it into the correction copy of the certificate, the previously transmitted information is neutralized. In such an adjustment, only section 1 “Data about the tax agent” and section 2 “Data about the individual” are filled out. The remaining sections are not completed.

Thus, a distinction is made between corrective forms, which are filled out to correct the information provided, and cancellation forms, the submission of which cancels them.

Cancellation certificate

A special situation is adjustment number “99” in 2-NDFL. This special code is entered for those cases when the certificate does not need to be corrected, but certain information from it needs to be canceled. Typical examples are when 2-NDFL was submitted to the wrong inspectorate or to the wrong person.

When indicating the adjustment “99” in the 2-NDFL certificate, only the first section “Data about the tax agent” and the second section “Data about the recipient of the income” are filled out.

According to the rules for filling out 2-NDFL, the “99” adjustment allows the remaining sections of the certificate not to be filled out.

How to correctly fill out the 2-NDFL adjustment

By Order of the Federal Tax Service of Russia dated January 17, 2018 No. ММВ-7-11/ [email protected] changes were made to Form 2-NDFL, but it is allowed to submit information for 2021 using both the updated form and the one previously adopted by Order of the Federal Tax Service dated October 30, 2015 No. ММВ-7-11/ [email protected] A similar rule applies to the adjustment of 2-personal income tax in 2021, but, of course, the corrected versions must be submitted on the same forms that were used when submitting the initial certificates .

In practice, tax agents, guided by Order No. ММВ-7-11/ [email protected] , enter all data into the adjustment, not just the corrected one, assign the previous document number, change the adjustment code, the date of the certificate, and submit it to the Federal Tax Service. Let's look at a few examples.

Example 1: how to make a 2-NDFL adjustment in the “taxpayer” field

The “taxpayer status” field is coded as “1” if the employee is a tax resident and his income is taxed at a rate of 13%. Code “2” is used to designate non-residents whose income is subject to taxation at a rate of 30%.

If the income of a non-resident employee was taxed at a rate of 13% (which in practice happens extremely rarely), and the taxpayer code in the certificate is “1”, it is impossible to get by only by adjusting the certificate. You will have to submit two correction forms:

- in the first, you should change the payer code to “2”, recalculate the amount of accrued and withheld tax;

- Since it is impossible to withhold the under-accrued personal income tax from the employee for the reporting year, the accountant draws up a second certificate, where he will put the adjustment flag “2”, indicating the presence of unwithheld tax amounts. Field 3 will indicate income not included in the tax base, and field 5 will indicate the amount of accrued and not withheld personal income tax.

Example 2: tax was not withheld from the taxable share of a valuable gift given to an employee

If this error is detected, it is necessary to make an adjustment to the 2-NDFL certificate:

- with sign “1”, adding the unaccounted amount of income, recalculate the tax base and calculated tax;

- with sign “2”, indicating the amount of tax not withheld.

When to make an adjustment

Many tax agents, especially beginners, are wondering whether it is possible to submit a 2-NDFL adjustment. In fact, it is possible, or rather, it is very necessary. Thus, from the procedure for issuing a 2-NDFL certificate (approved by order of the Federal Tax Service dated October 30, 2015 No. ММВ-7-11/485, hereinafter also referred to as the Procedure), the following answer to the question of whether it is possible to submit a 2-NDFL adjustment follows: this is not the right, but rather even the responsibility of every tax agent for personal income tax.

If we take the 2-NDFL adjustment for 2021, then it is necessary if the employer in 2021, after submitting the relevant certificate to the Federal Tax Service, recalculated the tax for 2021 and realized that it is necessary to clarify the tax obligations of a particular individual - the recipient of income from him. For example, due to:

- a trivial typo;

- omissions of the enterprise accountant;

- counting error, etc.

In any case, you need to know how to make a 2-NDFL adjustment, since the new certificate corrects inaccurate data from the previous certificate.

Based on letters from the Ministry of Finance dated June 30, 2016 No. 03-04-06/38424, Federal Tax Service dated August 9, 2016 No. GD-4-11/14515, false information (there is no legal definition in the law) is any (!) errors in certificates 2- Personal income tax. For example:

- incorrect amount;

- incorrect TIN;

- error in the income and/or deduction code;

- failure to indicate the amount of personal income tax that could not be withheld;

- errors in personal data of payers (for example, adjustment of passport data in 2-NDFL), etc.

In these cases, an adjustment is made to the 2-personal income tax for 2021. This will be the so-called corrective (clarifying) income certificate.

Also see “Taxpayer status in certificate 2-NDFL”.

How to prepare an adjustment

To make an adjustment means to fill out the information for an individual again, but with the correct information and details. Algorithm for retaking 2-NDFL for an employee in 2021 in five steps:

- In field No. - the number of the submitted certificate, which contains inaccuracies.

- In the field “from__.___.__” - the date of registration of the clarifying information.

- In the “Adjustment number” field - a number starting with 01. For example, 03 means that you are submitting a third corrected form for this employee.

- Indicators (information) in which an error was made in the previously provided forms should now be indicated correctly.

- Indicators (information) that did not contain errors in the previously provided certificates should be duplicated.

Sample on how to submit a 2-NDFL adjustment for 1 employee (or several employees) for 2021:

Adjusting the 2-NDFL report in 1C programs

Published 03/02/2021 07:01 Author: Administrator Well, colleagues, on this topic we are completing our series of articles on the 2-NDFL report. Despite the fact that this report will be abolished from 2021, we will still continue to submit it as part of the updated 6-NDFL report. Moreover, there are often cases when, having already submitted a report and received a positive protocol, an accountant finds an error, which entails an adjustment for employees. Therefore, we decided to prepare for you a mini-instruction on what to do if you suddenly find yourself in such a situation. Let's consider the topic using the example of the 1C program: Salaries and personnel management, edition 3.1, however, the algorithm of actions is also valid for the 1C program: Enterprise Accounting ed. 3.0.

When making adjustments, follow the basic rules:

The reference number for the problem employee in the adjustment report must match that in the primary report.

If the 2-NDFL certificate is completely cancelled, the correction number field is set to “99”.

Corrective – corrective reporting is submitted if errors are detected in the previously provided information.

The slide below shows typical errors in form 2-NDFL:

Remember the most important thing: the 2-NDFL adjustment declaration is submitted only for the employee for whom problems arose in the primary report.

Next, we will provide an algorithm for your actions depending on the status of the submitted report.

Situation No. 1: the status of the primary report 2-NDFL is “Passed”, a positive report was received, but the accountant found an error and now an adjustment is required

Let's consider a conditional example: at Karamelka LLC, the accountant submitted 2-NDFL certificates for 2021 to the Federal Tax Service, but subsequently it became necessary to make an adjustment for one employee - S.G. Ivanov. In 1C: ZUP ed. 3.1 there is a mark indicating that the document has been accepted by the Federal Tax Service.

If the checkbox “Certificates accepted by the tax authority and archived” is checked, then the document is closed for editing and correction.

Let us immediately remind you of the basic rule for sending any adjustment reports to 1C: there is no need to try to correct the data in an already submitted primary report, much less send it again!

Any adjustment is ALWAYS a new report in the 1C database!

When generating the primary certificate at the Federal Tax Service, the adjustment number field is set to “00”. Look at the reference number of the employee for whom you want to create an adjustment.

Let's look at the step-by-step creation of a corrective certificate “2-NDFL”.

Step 1. Go to the journal “2-NDFL Certificates for transmission to the tax authority” - section “Taxes and Contributions”.

Step 2. Click the "Create" button.

Step 3. Select the “Corrective” certificate type. The correction number is set automatically from 1 to 98.

When you select the “Cancelling” option, the correction number is automatically set to 99. This is the correct behavior of the program!

Corrective certificates are filled out automatically for persons for whom data was transferred and changes were made to the program.

If an error is detected for which automatic completion is not provided, for example, an incorrect address, passport data or other personal data is specified, then use the “Selection” button.

After selecting the type of information to be transmitted – “Correcting”, using the “Selection” button, indicate the employee for whom changes are being made.

The program will automatically issue the next certificate number.

Step 4. But since we need the certificate number to be originally submitted, click on the employee’s line and, in the certificate form that opens, change its number.

The reference number has been changed in the adjusted report.

Let us remind you that Ivanov’s certificate number 1 is not the serial number of the column, but the certificate number assigned to it by the program.

If, for example, we needed to correct the data, for example, about employee Pirogova, then in the corrective report we need to put reference number 3, because in the initial report the program assigned it this number 3.

Step 5. Click the “Print” button - “Income Certificate (2-NDFL)”.

In the printed form of the 2-NDFL certificate, you can see that the certificate number is kept the same, and the adjustment number is set to 01.

Step 6. Process the document, check it and send it to the regulatory authority using the “Send” or “Upload” button, or send it using a third-party program (VLSI, Contour, etc.).

Situation No. 2: status of the primary report 2-NDFL “Partially submitted”

In this case, carefully read the protocol and its annexes.

Often, the protocol indicates which certificate numbers were accepted by the tax authority, and the appendix to the protocol indicates the employees and the reasons why they were rejected by the controllers.

In this case, it is necessary to correct the errors in the 1C database, create a corrective report No. 1, fill it out with the corrected employees, CORRECT THEIR REFERENCE NUMBERS to the numbers from the primary report and send again.

If again one of the employees did not pass the control of the Federal Tax Service, then we again correct the errors in 1C, create a corrective report No. 2, fill it out with the corrected employees, CORRECT THEIR REFERENCE NUMBERS to the numbers from the primary report and send it again.

Situation No. 3: status of the primary report 2-NDFL “Not submitted”

In this case, we eliminate all errors described in the protocol and create a NEW PRIMARY report. There is no need to submit adjusting statements here, since the initial report was not accepted at all.

We fill out a new certificate under the same number, indicating in the “Adjustment number” field the number “00” and the new date.

If you fail to submit a new report on time, you will face a fine under Article 126 of the Tax Code of the Russian Federation (200 rubles for each document).

Colleagues, we sincerely wish that such situations happen to you as little as possible!

Authors of the article: Olga Kruglova

Irina Plotnikova

Did you like the article? Subscribe to the newsletter for new materials

Add a comment

JComments

How to check reporting information

Before sending the corrected information to the tax office, you need to check the information. How to correctly check a report, what to compare information with - consider important recommendations:

- Information on income and deductions must match the organization’s accounting data. Check the information on the income tax certificate with the employee’s personal card. Also monitor the indicators of payroll records and wage journals. The information must match the monthly accounting data.

- If, in addition to wages and remuneration for labor, other types of income are accrued to employees, then it is necessary to include information in the 2-NDFL adjustment. Example: an organization pays dividends to subordinates, distributes profits, or pays for health packages. Include such income in the 2-NDFL certificate according to the appropriate income code.

- Different tax rates apply to different categories of income. For each bet you will have to draw up a separate application (clause 1.19 of the Procedure).

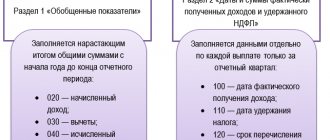

- Similar rules apply to the adjustment attribute field in the 2-NDFL certificate. If the tax is withheld by the employer on time, then indicator “1” is indicated. If it is impossible to withhold income tax, then sign “2” is indicated in the 2-NDFL certificate.

- The deadlines for submitting reports for various characteristics of a taxpayer have been equalized. Report by March 1 of the year following the reporting year. If the due date falls on a weekend, submit the form on the first working day.

IMPORTANT!

Deductions and benefits for personal income tax are documented. Applications, certificates of study, birth certificates and other papers must be collected annually from subordinates. Based on the received certificates, adjust the benefits and deductions provided.