KBK for payment of transport tax

Transport tax is paid by all vehicle owners: legal entities, organizations and individuals. Its size depends on the amount of horsepower included in the engine power of the vehicle. This is a regional tax, so it must be paid to the budget of the region where the car is registered. But the tax return must be filed at the place of registration of the taxpayer.

Legal entities are required to independently calculate the amount of transport tax, as well as report on its payment before February 1. Whether an advance payment is needed or the tax must be transferred all at once is decided by the regional tax authority.

***

To understand why it is necessary to make a transfer to the budget upon request with KBK 18211603010016000140, you need to know the content of the claims from the fiscal authorities. It is immediately necessary to take into account that this BCC is used if it is necessary to collect fines for various violations of tax legislation.

If the company incorrectly indicates the code in the order, this will not have any consequences for it, however, to correct the situation, it will have to provide a special statement indicating the correct BCC. There is no need to transfer the amount again; previously transferred funds will be counted towards its repayment immediately, despite the incorrect code.

Similar articles

- Penalty for failure to provide 6-NDFL

- KBK fine transport tax 2018

- KBK for organizations and individuals on transport tax

- Property tax - current BCC for organizations

- KBK for personal income tax for employees

KBK for personal income tax in 2021: table

- Federal Treasury account (field 17);

- Payer's TIN (field 60);

- Payer checkpoint (field 102);

- recipient's TIN (field 61);

- Recipient's checkpoint (field 103);

- “payer” detail (field 8);

- “recipient” detail (field 16);

- basis for payment (field 106);

- payer status (field 101);

- tax period indicator (field 107); KBK (field 104).

If the payment has not been received by the budget, then the payment cannot be clarified, and the tax agent’s obligation to transfer personal income tax is considered unfulfilled (for example, if the money has not been received by the budget system due to an error in the Federal Treasury account number). In this case, the tax agent must:

Kbk personal income tax fine 2021 for legal entities 18211603010016000140

KBK must be indicated in any payment order for the transfer of tax fees and other contributions, including fines. This concept allows you to make sure that the money goes in the right direction. And the payer will not be subject to any penalties for late repayment of obligations.

All accountants often receive messages about changes in the payment procedure to the state budget. And they are required to pay a certain tax or fee according to these details. If he violates the current legislation and refuses this requirement, then he faces administrative or criminal punishment.

Sample of filling out a payment slip for payment of a fine KBC 18211603010016000140

To confirm filling out the form about the organization, you need to click - OK Company details are entered using the commands - recipient's account - Add In the window that appears, you need to fill in the fields containing the information necessary for the transfer. Confirmation of the entry is carried out by clicking on the button - OK. After entering the data of the participants in the procedure, you need to enter basic information. The official involved in drawing up the form must indicate the transfer amount and the order of the action. The system can automatically calculate the personal income tax percentage. Filling is completed.

If the payment is drawn up to pay off a fine or penalty, the value 0 is entered in the line. Field 108 When filling out the column, the person responsible for drawing up the documentation must indicate the requirement number. It should be remembered that the symbol “No” does not need to be inserted. Field 109 Here the official must enter the date. You must rely on field 108. The date is indicated in numbers.

Do you have any questions about filling out payment forms? Ask them on our forum. On this thread, for example, you can clarify what to do if you sent a payment order indicating the wrong KBK: https://forum.nalog-nalog.ru/drugie-voprosy-po-uchetu-i-nalogam/nevernyj-kbk-a -what-konkretno-delat/

First of all, let’s figure out what the meaning of KBK is 18211603010016000140. To administer budget revenues, each type of payment has a special code - KBK (budget classification code). It must be indicated in each payment order for the payment of funds to the budget, as well as in tax reporting sent to the Federal Tax Service, Social Insurance Fund and other government agencies.

BCC for personal income tax fines 2021

It should be noted that the tax agent will have to pay a fine only if he had the opportunity to fulfill the obligations imposed by law, but did not do so. Sometimes this is not possible, for example, when an individual’s income is in kind. Tax cannot be withheld from such income; therefore, there cannot be a fine.

Since the tax agent does not have the right to pay this tax from his own funds, if the tax amount is not withheld, there will be no penalty, and the tax agent cannot be obliged to pay the tax itself. He will have to pay the fine amount.

We recommend reading: Transport tax benefits in the Moscow region for labor veterans

Kbk 18211603010016000140 fine 200 rubles issue a payment

In accordance with current legislation, this is a fine that must be paid to the state for violations of tax legislation. Why are they needed? Such codes are necessary for introduction in order to streamline all payments - receipts into the current budget and expenditures.

Sometimes there are quite confusing situations. When, it would seem, an accountant clearly copes with his duties, the tax base is not underestimated, so why in this case do the tax authorities charge a fine, which must be paid within the allotted time period according to the KBK code 18211603010016000140? There are actually plenty of reasons. Therefore, questions from managers about what the KBK code is 18211603010016000140, for which a fine of 200 rubles was assessed to their organization, are most often addressed to their accountants.

There are actually plenty of reasons. Therefore, questions from managers about what the KBK code is 18211603010016000140, for which a fine of 200 rubles was assessed to their organization, are most often addressed to their accountants. But if you read in more detail what kind of fines are paid under this code, then many organizations and institutions will understand that to receive a fine from the tax office, sometimes you don’t even need a clear violation, sometimes even filing reports in paper format is enough.

Intentional failure to pay or incomplete payment of tax (fee) amounts, a fine in the amount of 40% of the unpaid amount of tax 123 Failure of a tax agent to fulfill the obligation to withhold and (or) transfer tax The penalty is 20% of the amount that was to be transferred. Article 126.p.1 Failure to provide the tax authority with information necessary to carry out tax control within the prescribed period. 200 rubles for each document not provided Art. 126. clause 2 Refusal to provide information necessary to carry out control to the tax authorities. 10,000.00 Article 128 Failure to appear or evasion of appearance without good reason. 1000.00 Article 128 Unlawful refusal of a witness to testify, as well as giving knowingly false testimony. 3000.00 St. 129 clause 1 Refusal of an expert, translator or specialist to participate in a tax audit 500.00 Art.

Kbk personal income tax fine 2021 for legal entities 18211603010016000140

Budget classification codes are used when transferring funds to the budget in order to ensure their correct distribution. KBK personal income tax for employees is necessary for organizations, legal entities when transferring tax for employees, individual entrepreneurs use other indicators on the general system. The deadline for paying the fee is indicated in hours. Vacation and sick leave benefits are also subject to this mandatory fee, but it is paid no later than the last day of the month in which they were paid to the taxpayer. You can calculate the tax amount using a calculator.

Let's take a closer look at what these articles of the code are and what fines are paid under them. KBK for what is the fine in rubles and what is the tax So, KBK - decoding - for what tax is the fine paid with it? This code is indicated when transferring penalties for the following violations: For late submission of an application for tax registration or generally working without registration with the Federal Tax Service, art. Failure to comply with the method of submitting a tax return, Art.

KBC collection of taxes and fees including penalties

- 1 Kbk collection of taxes and fees including penalties

- 2 “New” BCCs for non-tax payments

- 3 Kbk for payment of fines in 2021 and 2021

- 4 KBK penalties for insurance premiums in 2021 - 2021

- 5 Kbk collection of taxes and fees including penalties

- 6 Code “KBK 18211603010016000140” - Monetary penalties (fines) for violation of the legislation on taxes and fees provided for in Articles 116, 118, paragraph 2 of Article 119, Article 1191, paragraphs 1 and 2 of Article 120, Articles 125, 126, 128, 129, 1291, Articles 1294, 132, 133, 134, 135, 1351 and 1352 of the Tax Code of the Russian Federation, as well as fines, the collection of which is carried out on the basis of the previously existing Article 117 of the Tax Code of the Russian Federation

- 7 Budget Classification Codes (BCC) - Fines, sanctions, payments for damages

- 8 Collection of taxes and fees, including penalties

- 9 Income tax: KBK-2019

- 10 18211603010016000140 KBK transcript 2021: what the fine is for

182 1 1600 140 Monetary penalties (fines) for administrative offenses in the field of taxes and fees provided for by the Code of the Russian Federation on Administrative Offenses

I don’t know what administrative violation was committed, but the KBK seems to be correct.

A change in the 14th digit in the BCC for a specific tax is associated with the payment of the tax itself - 1, penalty - 2, fine - 3.

Monetary penalties (fines) for violation of the legislation on taxes and fees provided for in Articles 116, 117, 118, paragraphs 1 and 2 of Article 120, Articles 125, 126, 128, 129, 1291, 132, 133, 134, 135, 1351 of the Tax Code Russian Federation Oksana, look at what is written in the requirement (what violation, article), because such a code also exists.

“New” BCCs for non-tax payments

"book", 2007, N 1

September 18, 2006

The Treasury of the Russian Federation clarified the procedure for indicating numbers in 14 - 17 digits of budget classification codes (KBK).

Since the introduction of 20-bit KBK, it has been established that 14 - 17 digits of the KBK can have the following meanings:

- “1000” (upon payment of the payment amount);

- “2000” (when paying penalties and interest on the payment);

- “3000” (upon payment of the amount of the monetary penalty (fine) on the payment).

These figures, depending on the specific situation, should have been indicated in the KBK when transferring to the budget any types of income administered by the Federal Tax Service of Russia or the Federal Customs Service of Russia.

But the Federal Tax Service of Russia is not only the administrator of purely tax payments, fees and state duties, but also performs the functions of state registration of legal entities and individual entrepreneurs, imposes and collects fines for violations of the law, etc.

That is, it also administers payments for which the indication of “non-zero” values in 14 - 17 digits of the KBK is incorrect. Therefore, the Russian Ministry of Finance introduced a clarification into the Instructions, according to which a “non-zero” value in the given BCC categories should be indicated only when paying taxes and fees (including debt amounts).

Thus, when paying other types of payments to the budget administered by the Federal Tax Service of Russia, “0000” should be indicated in 14 - 17 digits of the BCC.

True, the July changes to the Directives were published only in September and the clarification Letter from the Treasury of the Russian Federation appeared in the same month.

Therefore, on most regional tax websites, and even in the tax inspectorates themselves, information is still posted about indicating the value “1000” in 14 - 17 digits of the BCC when paying all payments administered by the Federal Tax Service of Russia (in particular, fees for providing information from state registers ).

Information on changes to the BCC for non-tax payments is posted on the websites: https://www.mosnalog.ru/page.asp? >

According to available information, the tax authorities in Moscow and the Bryansk region were the first to draw taxpayers’ attention to the change in payment details.

Taxpayers who have not been notified by local tax authorities about changes in the BCC of non-tax payments are better off not taking the initiative and paying them in accordance with the Instructions. Firstly, not all banks may be ready to process payments using the “new” BCC.

Secondly, you may have to spend a lot of time proving to the tax authority the legality of your actions.

Therefore, in order to avoid possible difficulties, it is more advisable to make the payments indicated in the table using the correct details only after the local tax authority has officially informed you about this.

Kbk for payment of fines in 2021 and 2021

The article describes the KBK for monetary penalties - fines in 2021 for failure to comply with the norms of the tax code, the code of administrative offenses and codes that indicate payments for failure to comply with road safety.

Individuals and enterprises sometimes violate the law unintentionally, but in any case, non-compliance entails punishment in accordance with the Code of Administrative Offenses and the Tax Code of the Russian Federation. Before paying penalties, you must fill out a payment slip indicating the BCC for the fine. The code will tell the recipient what kind of payment it is and will help to credit the money to the appropriate budget in a timely manner.

Administrative offenses

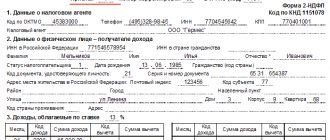

KBC for payment of penalties for personal income tax for 2021

Tax agents now have to report on personal income tax not only annually, but also quarterly. Quarterly reporting (form 6-NDFL) applies only to employers. It must be submitted based on the results of reporting periods, determined quarterly on an accrual basis, on the last day of the month following the next period. The reporting contains general tax information for all employees as a whole.

- 182 1 0100 110 - penalties for personal income tax transferred by tax agents.

- 182 1 0100 110 - penalties for personal income tax for individual entrepreneurs, lawyers, notaries.

- 182 1 0100 110 - penalties for personal income tax for individuals who received income listed in Art. 228 Tax Code of the Russian Federation.

- 182 1 0100 110 - penalties for personal income tax for non-residents on payments made in accordance with Art. 227.1 Tax Code of the Russian Federation.

KBC penalties for personal income tax in 2021 for legal entities

Legal entities pay penalties for personal income tax if, as tax agents, they do not transfer the tax to the budget on time (Article 75 of the Tax Code of the Russian Federation). The duty of a tax agent arises when taxable income is paid to individuals.

In 2021, the BCC of penalties for personal income tax has not changed. You will have to pay them if you are more than one day late in paying your tax. Let's consider the code for the budget classification of penalties for personal income tax, the procedure for their calculation and a sample payment order for transferring the amount to the budget.

KBK 18211603010016000140: what is the fine of 200 rubles for and what is the tax

So, KBK 18211603010016000140 - transcript 2018-2019 - what tax is the fine paid with it? This code is indicated when listing penalties for the following violations:

- For late submission of an application for tax registration or generally working without registration with the Federal Tax Service (Article 116 of the Tax Code of the Russian Federation).

- Failure to comply with the method of submitting a tax return (Article 119.1 of the Tax Code of the Russian Federation) is for which a fine of 200 rubles is imposed under KBK 18211603010016000140.

We will explain in what form you need to submit tax returns in the article “Procedure for submitting tax reports via the Internet.”

- When the managing partner submits financial statements of the partnership with unreliable data (Article 119.2 of the Tax Code of the Russian Federation).

- Gross violation of tax accounting rules is grounds for a fine under Art. 120 (clauses 1 and 2) of the Tax Code of the Russian Federation.

The article “How to maintain tax accounting registers (sample)” will tell you how to organize accounting of income and expenses for tax purposes without errors.

- Violation of the procedure for using pledged or seized property (Article 125 of the Tax Code of the Russian Federation).

- Failure to provide information necessary for tax control (Article 126 of the Tax Code of the Russian Federation). If, for example, you do not provide the primary information during a counter-inspection of the counterparty by the tax authorities, then you will face a fine of 200 rubles. for each document not presented (clause 1). And if the tax agent does not submit a personal income tax calculation on time (clause 1.2), then this is also a reason for a fine (that’s why the fine is 1000 rubles according to KBK 18211603010016000140).

For more information on how tax authorities should conduct a counter audit, read the article “Features of conducting a counter tax audit.”

- Submission by a tax agent of documents with false information (Article 126.1 of the Tax Code of the Russian Federation).

- Failure to appear at a tax violation case as a witness (Article 128 of the Tax Code of the Russian Federation).

- Refusal to assist in conducting a tax audit or issuing a knowingly false conclusion, being an expert in any field or a translator (Article 129 of the Tax Code of the Russian Federation).

- Silencing important information, provided that you have information that you should have reported to the tax authorities (Article 129.1 of the Tax Code of the Russian Federation).

- Failure to submit information about controlled transactions or submitting them with incorrect data (Article 129.4 of the Tax Code of the Russian Federation).

- Violations that banking organizations can commit: opening a current account for a businessman or company without the necessary documents, violation of deadlines for the execution of payment orders for the payment of taxes, illegal continuation of transactions on the taxpayer's current account, failure to fulfill the obligation to submit account statements to the tax authority, violation of the rules for working with electronic money (Articles 132, 133, 134, 135, 135.1, 135.2 of the Tax Code of the Russian Federation).

For each of these articles, the Tax Code of the Russian Federation provides for different amounts of fines for the taxpayer. The smallest fine is 200 rubles. - this is a penalty for violations under Art. 119.1 of the Tax Code of the Russian Federation and 126 (clause 1).

Kbk for personal income tax fine in 2021

For “unfortunate” contributions, penalties are transferred to the Social Insurance Fund according to the previously valid BCC - 393 1 0200160. The tariffs in force in the general case will also be applied in 2021 (previously they were set for 2021 inclusive). Within the established limit of the base for 2021. Additional tariff according to list 1 Payment for the transfer of a fine for personal income tax. Therefore, check whether you mistakenly indicated the BCC for the transport tax of individuals in 2021 - 18210604012021000110. In this article, we will consider the current BCC for personal income tax in 2021.

We recommend reading: How to get a million from the state for a young specialist

In 2021, as before, the BCC for the payment of penalties for personal income tax was approved by Order of the Ministry of Finance dated July 1, 2021 No. 65n. So, for example, the BCC for insurance premiums has changed. KBK simplified tax system with “minimum tax” in 2021. Debts, penalties and fines accrued before 2021 for medical payments of individual entrepreneurs are repaid for themselves according to the KBK, in which units are placed on 16-17 acquaintances. Using the example of KBK 18210102021012100110, we can decipher what tax merchants and companies will have to pay in 2021.

KBK penalties for personal income tax

Individual entrepreneurs who do not apply special regimes, as well as notaries engaged in private practice, lawyers who have established law offices, and other persons engaged in private practice, pay personal income tax independently on the basis of a submitted tax return no later than July 15 of the year following the previous year (clause 6 Article 227 of the Tax Code of the Russian Federation). In addition, such persons must pay advance payments during the year within the time limits specified in clause 9 of Art. 227 Tax Code of the Russian Federation.

Let us remind you that tax agents must transfer calculated and withheld personal income tax no later than the day following the day the income was paid. Personal income tax on sick leave benefits and vacation pay is transferred no later than the last day of the month in which such payments were made (clause 6 of Article 226 of the Tax Code of the Russian Federation).

KBK 18211603010016000140: transcript 2021, for which the fine

- If a company or businessman operates illegally, that is, they have not registered with the Federal Tax Service. Another option is that you were late in submitting documents for registration;

- The tax return was not filed in the proper form;

- The data at her request were not sent to the Federal Tax Service in a timely manner;

- Accounting for income and expenses was carried out in violation of the law.

Often, organizations and individual entrepreneurs receive demands from the tax office to pay taxes or fines. Sometimes these requirements contain only the BCC. Having received such a budget classification code, you have to rack your brains for a long time about what you need to pay for the fine.

Decoding KBK 18211603010016000140 (2018–2019)

Our readers - practicing accountants - often receive letters from the tax office demanding the payment of a certain tax or fee.

This happens if the taxpayer violated the law and did not transfer any payment to the budget on time in full. In this case, tax authorities are required to indicate the name of the tax for which the claims arose, its BCC (for example, BCC 18211603010016000140) and a number of other information. For information on how a demand for payment of taxes and fees should be filed, read the materials in the section “Request for payment of taxes and fees in 2018–2019.”

But the document that instructs the company to pay according to BCC 18211603010016000140 raises the most questions - what was the fine for in this case and what does this BCC mean?

First of all, let’s figure out what the meaning of KBK is 18211603010016000140. To administer budget revenues, each type of payment has a special code - KBK (budget classification code). It must be indicated in each payment order for the payment of funds to the budget, as well as in tax reporting sent to the Federal Tax Service, Social Insurance Fund and other government agencies.

The full list of codes is contained in the KBK classifier (order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n). It is in it that you need to look for the decoding of 2018-2019 KBK 18211603010016000140. According to the classifier (in the current edition) indicating KBK 18211603010016000140 - decoding for which the fine is in 2018-2019 - the taxpayer must transfer the fine for violation of tax legislation under the following articles Tax Code of the Russian Federation: 116 , 119.1, 119.2, 120 (paragraphs 1 and 2), 125, 126, 126.1, 128, 129, 129.1, 129.4, 132, 133, 134, 135, 135.1, 135.2.

Let's take a closer look at what these articles of the code are and what fines are paid under them.

Do you have any questions about filling out payment forms? Ask them on our forum. On this thread, for example, you can clarify what to do if you sent a payment order indicating the wrong BCC.

KBK for payment of property tax with changes in 2021

The property tax is required to be paid by ordinary citizens - “owners of houses, factories, apartments, cottages”, as well as organizations. Thus, taxpayers for this obligation are companies that own taxable real estate, as well as some movable property (depreciation groups 3-10). However, from 01/01/2021 the composition of the tax base will be changed, this is discussed below.

Rates and benefits for movable assets were set at the regional level. Some constituent entities of the Russian Federation have provided for complete exemption of taxpayers from paying tax on movable fixed assets. Other regions have approved reduced rates. However, there are also those areas in which the tax on movable assets was calculated at the maximum - 1.1%.

What kind of KBK 18211603010016000140

- Violation of the procedure for using pledged or seized property (Article 125 of the Tax Code of the Russian Federation).

- Failure to provide information necessary for tax control (Article 126 of the Tax Code of the Russian Federation). If, for example, you do not provide the primary information during a counter-inspection of the counterparty by the tax authorities, then you will face a fine of 200 rubles. for each document not presented (clause 1). And if the tax agent does not submit a personal income tax calculation on time (clause 1.2), then this is also a reason for a fine (that’s why the fine is 1000 rubles according to KBK 18211603010016000140).

- the procedure for registering with the Federal Tax Service was violated (Article 116 of the Tax Code of the Russian Federation);

- the tax return is submitted to the regulatory authority in paper form, provided that the company had to submit an electronic version of the document (Article 119.1 of the Tax Code of the Russian Federation);

- A gross violation of tax accounting was revealed - lack of primary documentation, accounting and tax registers were not maintained, VAT amounts do not have documentary evidence in the form of invoices, etc. (Article 120 of the Tax Code of the Russian Federation);

- tax reporting was not submitted on time (Article 126 of the Tax Code of the Russian Federation);

- submission of false reports by a tax agent, for example, errors in 2-NDFL certificates or 6-NDFL calculations (Article 126.1 of the Tax Code of the Russian Federation);

- the enterprise ignored the tax authorities’ request to provide explanations (Article 129.1 of the Tax Code of the Russian Federation);

- no notification was submitted for controlled transactions (Article 129.4 of the Tax Code of the Russian Federation).

We recommend reading: Car tax benefits for Saratov pensioners

KBK 18211603010016000140 - what tax or what sanctions

No one is immune from mistakes, and they periodically arise in the work of anyone, even the most responsible specialist. Accountants are no exception. Often their mistakes lead to financial consequences, resulting in the company being issued fines by the tax authorities. The reasons for this may be late tax payment, partial underpayment or complete non-transfer. The requirements of the Federal Tax Service are formalized in writing with the obligatory indication of the BCC and the name of the tax. They contain a notification to the payer that he has debts on budget obligations, which he will have to pay within the allotted time frame. In addition to the amount to be paid, it must indicate the deadline for repayment, and also provide information about what measures the Federal Tax Service will take in the event of non-fulfillment of the requirement. The demand must be made within 3 months from the date of discovery of the fact of arrears. If the debt is determined based on the results of an on-site inspection, then the period for this is reduced to 20 days from the moment the decision on it comes into force. In most cases, the request specifies a period for payment of the debt of 10 days.

Quite often, when receiving such notifications, the accountant wonders what the fine is for under the Code of Criminal Code 8211603010016000140.

IMPORTANT! In order to simplify and automate control procedures for fiscal direction, each tax is assigned a digital identifier, which is called the KBK. There is a requirement for all payers to indicate it in all payment documents, both for taxes and insurance contributions to extra-budgetary funds, as well as in declarations.

The list of all identifiers available for use is reflected in the KBK classifier, introduced by order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n. According to the BCC indicated by us, fines related to tax offenses under Art. 116, 118, 119.1, 120, 125, 126, 128, 129, 129.1, 132, 133, 134, 135, 135.1 Tax Code of the Russian Federation.

Budget Classification Codes (BCC)

The third BCC (10th category 4) is intended for employers who transfer personal income tax withheld from the salaries of foreign workers arriving from a “visa-free” country. If a number of conditions are met, such tax is reduced by the amount of the advance paid by the foreigner when obtaining a patent.

The first BCC (10th category 1) is intended for employers who are tax agents. They indicate this code when transferring to the budget personal income tax withheld from salaries and other income of employees (except for foreigners from “visa-free” countries), as well as when paying tax withheld when paying dividends to the founder.

Kbk 18211603010016000140 for which the fine is 1000 rubles

The use of budget classification in the form of a code helps relevant government institutions track and classify the receipt of funds from taxpayers and their distribution across budgets of all levels.

In accordance with current legislation, organizations must submit a VAT return no later than March 28. If for any reason a violation of the procedure established by law occurs, this entails a fine, the amount of which depends on certain circumstances. If the organization continues to evade paying taxes, this will lead to serious consequences and even imprisonment of criminals.

What is the fine for under KBK 18211603010016000140 - decoding 2017

Here is the transcript of KBK 18211603010016000140 . Having received a notification with the specified code, you need to understand that this is a consequence of one of the following omissions:

- Late registration or lack thereof with the Federal Tax Service, entailing, on the basis of Art. 116 of the Tax Code of the Russian Federation, a fine of 200 rubles.

- Previously (until May 2014), a fine was applied for late notification of tax authorities about the opening or closing of a bank account. After the adoption of Law No. 52-FZ of April 2, 2014, this obligation was canceled, but the digital identifier remained in the classifier.

- Failure to submit within the prescribed period and according to the legally approved tax reporting form, on the basis of Art. 119.1 of the Tax Code of the Russian Federation, entails a fine of 100 rubles. In particular, for most types of tax reporting, an electronic format is provided for transmitting it to inspectors, and violation of this procedure may result in a fine.

- A significant discrepancy between the procedure for maintaining tax accounting and the established rules is subject to punishment on the basis of Art. 120 Tax Code of the Russian Federation.

- Illegal use of seized or pledged property.

- Refusal to provide tax authorities with information requested by them to conduct control procedures. For example, if there is no primary documentation sent to the inspection during a counter inspection, the organization faces a fine of 200 rubles for each document.

- Ignoring the obligation to appear in court as a witness in a tax crime.

- Resistance to the administration process or provision of false data to the reviewer by a subject acting as an expert.

- Failure to report information important for tax administration, provided that it was known to the payer on the basis of Art. 129.1 Tax Code of the Russian Federation.

- Offenses that credit institutions can commit: registering a bank account without having all the necessary documents;

- failure to meet deadlines for transferring taxes when executing payment orders;

- continuation of the movement of funds through the company’s frozen account;

- failure to provide bank statements to the Federal Tax Service.

All of the listed offenses require penalties of varying amounts in the form of fines for their commission.

The application of liability in the amount of 200 rubles is provided for in Art. 119 Tax Code of the Russian Federation:

- for failure to comply with the format for transmitting tax reporting, in particular, providing it in paper form instead of electronically;

- failure to provide documents to representatives of the Federal Tax Service during a counter inspection - in such a situation, 200 rubles are charged for each document not received under Art. 120 Tax Code of the Russian Federation.

It will be noteworthy that if the company does not respond to the inspection’s claims regarding the reporting format, then it will actually miss the deadline allotted for submitting the reports and will additionally be punished under Art. 119 of the Tax Code of the Russian Federation.

Kbk fine for personal income tax 2021

Legal entities and individual entrepreneurs pay personal income tax at different times. Thus, a legal entity contributes tax funds on a monthly accrual basis, individual entrepreneurs - quarterly, individuals - once a year. Also, the payment date depends on the type of profit subject to levy.

Mandatory payments include vacation pay and temporary disability benefits. If vacation pay is calculated independently by the employer, then sick leave benefits are paid only on the basis of the presentation of sick leave by the sick employee. Reporting on these amounts is prepared on the last day of the month when the accrual occurs. The employer has the right to pay these amounts along with the salary. The tax on these payments must be transferred the next day after they are deducted from the employee.