All tax returns, calculations and reports submitted to the Federal Tax Service are subject to a desk audit. This also applies to the calculation of insurance premiums, which from the beginning of 2021 is submitted to the tax authorities, and not to the funds. If, during the inspection, inspectors identify inconsistencies between the information received and the information they have, as well as in other cases, they will require explanations for the calculation of insurance contributions to the tax office. We will talk further about what may serve as a reason for requesting explanations, how to compile them and submit them to the Federal Tax Service.

In what situations do requests for explanations come?

Letters from the tax department about explanations for accrued and paid insurance premiums are not that uncommon. They are usually caused by the fact that tax inspectors did not like something in the reporting submitted to them, for example, they found inconsistencies in the documents submitted by the organization with their own data, or they discovered some erroneous or unreliable information. In particular, doubts may arise in situations where there has been a noticeable decrease in an employee’s salary compared to previous years, when the amount of personal income tax in the 2-NDFL certificate is not identical to the tax payment that “went” to the budget, or a discrepancy between the indicators in the 2-NDFL certificates and the form has been discovered 6-NDFL, etc.

- Form and sample

- Free download

- Online viewing

- Expert tested

FILES

At the same time, the main parameters that tax authorities pay attention to when monitoring insurance premiums are the total amount of payments made by the organization for its employees.

Response to the request of the Federal Tax Service as part of a tax audit

The tax inspectorate may require documents to clarify the results of the next audit or during a “counter” audit of an entity in the context of relations with the company to which clarifying questions are sent.

Checks can be of two types:

- office - on tax territory based on the documents provided;

- on-site – on site.

In both cases, the tax authority may require clarification on the payment of fees, so it has the right to ask for clarifying documents.

A timely and complete response to the tax authorities’ request, along with the necessary documentation, is carried out within the deadlines established by law. The deadline for responding to a tax demand for various types of audits is 10 days from the date of delivery to the counterparty of a desk-type demand, and 5 days for a “counter” request.

Attention: watch a video on the topic of tax audits and disputes with tax authorities, ask your question in the comments to the video and get free legal advice on the YouTube channel, just don’t forget to subscribe:

Allowed sending methods

There are two ways to submit an explanation to the tax authorities. If the company uses an electronic reporting form, then the explanation must be transmitted in this way, otherwise it will not even be considered.

But if an enterprise uses the right to submit reports on paper, then an explanation can be generated on paper and then taken to the tax office in person. If it doesn’t work out in person - no problem, you can send the document through an authorized person (provided that he has a notarized power of attorney) or by regular mail - the date of submission of the explanation in this case will be considered the date when the letter was accepted by the postal employee services.

Types of explanations for insurance premiums to the Federal Tax Service

Explanations on insurance premiums can be submitted to the Federal Tax Service on several grounds, which we will consider in more detail.

Using a reduced insurance premium rate

The company does not submit any application to the Federal Tax Service to establish the right to use a reduced tariff for insurance premiums, and tax authorities see this information on the DAM. To confirm this right, they can send a request to provide documents on the basis of which preferential rates for insurance premiums are used.

Their list depends on what taxation system the business entity uses and what its activities are. For example, a copy of KUDiR, a copy of a certificate of residence in a special economic zone, payment documents, copies of documents on the right to conduct a certain type of activity, etc. can be presented as evidence.

Supporting documents can be issued either electronically or on paper, depending on how the explanations upon request are sent. In addition, they must be drawn up as attachments to the explanation sent.

Use of non-taxable amounts when calculating contributions

When calculating the base for insurance premiums, non-taxable amounts are excluded from it, and to confirm the right to use them, the tax office may request various documents, for example, on sick leave, provision of daily allowances, when paying child benefits, etc.

When drawing up an explanation, you must indicate in detail the grouping of non-taxable payments and the amounts for them, and use copies of available documents for confirmation.

Zero settlement on insurance premiums

All policyholders must submit calculations for insurance premiums, regardless of whether insurance premiums have been accrued or paid or not. In the absence of accruals for contributions, a zero DAM is formed, about which tax authorities may have certain doubts, and then they will send a request for clarification.

As an explanation for the lack of accrual of insurance premiums, one can indicate the reason - suspension of activities and payment of wages. Such an explanation can be sent along with a zero calculation for insurance premiums in order to prevent further questions from the tax office.

What happens if you do not respond to requests for clarification?

Sometimes employees of organizations, for some reason, do not consider it necessary to respond to letters from the tax authority or, out of absent-mindedness, simply forget to do so. Previously, the legislation did not provide for any sanctions for this, but from January 1, 2017, tax authorities received the right to fine enterprises for failure to provide explanations.

Moreover, the fine is quite large: for the first time it is 5 thousand rubles, but if the tax agent commits such a violation again, the amount will increase to 20 thousand rubles.

In addition, we should not forget that employees of the supervisory agency may interpret the taxpayer’s silence in their own way, as a result of which the enterprise may be placed on the schedule of the next on-site tax audits. And this is a more serious danger, because based on the results of such control measures, companies are often subject to more serious administrative penalties (especially relevant, given that there are some flaws in the work of almost any organization).

Response to a tax claim

During inspections, the Federal Tax Service reveals quite a few violations, including those related to the payment of taxes. But there are often cases when the requirement is erroneous. An organization that received such a request, but at the same time paid taxes regularly, is bewildered. Of course, there is no need to pay a debt that does not exist.

But in such a situation, it will still be necessary to give an answer. In which you must indicate what you disagree with and the reasons. This must be supported by documents: receipts, account statements, notifications. In the letter, please indicate the list of attached documents. There is no need to describe everything in great detail, thereby lengthening the text. Everything must be to the point and with evidence. The answer can be sent by registered mail or delivered in person. Also, if the company has an electronic signature, it can be sent through your personal account on the website nalog.ru.

If, however, you have an arrears, then of course, upon receipt of the request, it must be paid within eight days from the date of receipt of the letter. Proof of payment must be attached to the response, which will indicate the amount of payment, for what period and details of the payment document.

How to write an explanation

An explanation of insurance premiums can be written in any form - there is no unified standard. It is recommended that its structure and content comply with the norms and rules adopted for business papers.

It is very important that the explanation clearly describes the reasons for the problem for which tax representatives contacted the company. They need not only to be identified, but also to be argued. In this case, the evidence base should consist not only in words, but also in the presence of relevant supporting papers.

Response to the tax office’s request to provide documents regarding the counterparty

A requirement of this nature is regulated by Art. 93.1 Tax Code of the Russian Federation. It is also mandatory. The request can be either for a specific transaction or in general for documents affecting the taxpayer being audited.

When receiving a request, there are several response options:

- notification to a tax officer about the absence of the requested documents

- provision of available documents within the prescribed period

As a rule, the Federal Tax Service requires the provision of acts, additional agreements, and invoices for certain periods of time for transactions. And of course, it is physically impossible to provide them on time. In this case, the next day after receiving the request, you should send a letter to the tax office about the impossibility of submitting documents on time and indicate how long you can do this. Be sure to indicate the reason: there is a large volume of documents, so we do not have time to prepare everything on time.

All documents must be certified with the signature and seal of the company. Write a covering letter in which you list all the attached documents. Provide information about each document (name, date, number, period).

How to prepare an explanation on paper

For explanations, you can take a regular sheet of paper or a form with company details, but it is better not to write them by hand, but to print them on a computer. After final formation, the document must be signed - it is good if the document contains two autographs: the director and the chief accountant. The explanation should be made in two identical copies, one of which must be sent to the place of request, and the second must be kept with you. If the accounting policy of an enterprise indicates the use of a seal in its current activities, the letter should be endorsed with its help. In the journal of outgoing documentation, you must make a note about the explanation sent (indicating its number and date).

How to write a response from the tax office regarding the provision of explanations or documents?

- Lack of required documents. If documents are missing, the tax office must be notified of this fact. The response should indicate the reasons for the lack of documentation (fire, request for documents by another body, etc.).

- Failure to provide documents on time. You must write in your response the date no later than which the documentation will be presented. Please consider the reasons valid.

- If there are no documents due to factors beyond the taxpayer’s control, then in the response to the tax office’s request for the provision of documents, these reasons are indicated and acts or other certifying factors that caused the impossibility of providing documentation are attached. If it is impossible to provide documentation for other reasons, penalties may be applied to the entity and tax disputes may begin.

- Previously provided documents are requested. If the original accounting forms have already been sent to the tax office and their secondary provision is impossible, you can indicate this in your response and attach copies of these documents with the tax office marking the seizure. Copies must be certified by the company's management.

USEFUL : we will prepare an urgent tax response for you within no more than 24 hours

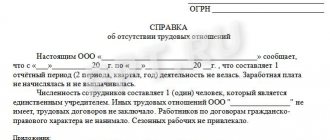

Sample explanation to the tax office

If you have received a request from the tax office to provide an explanation regarding insurance premiums, and you have never made such documents before, look at the example below and read the comments to it - with their help you will probably be able to formulate the letter you need.

- First of all, indicate the addressee in the explanation, i.e. the tax office for which the explanation is intended. Then enter information about the organization in more detail: write its name, details, contact information (address, telephone), be sure to mark the outgoing number of the message. After this, you can move on to the main section.

- First, provide here a link to the number and date of the request that came from the supervisory authority, then begin to formulate the actual explanations. In each specific situation, they depend on what particular circumstances led to questions from tax specialists. But in any case, give an explanation both descriptively (for example, if technical problems or incorrect work of an accountant led to the error, write it down) and documented.

- When referring to documents, indicate their numbers and date of creation. If the reason for which the tax authorities have questions has already been corrected, be sure to note this, as well as the fact that in the future you will take all measures to prevent such situations.

- Finally, be sure to sign the form.

Deadline for response to tax request

It doesn’t matter what demand and on what basis the organization received from the Federal Tax Service. It must be answered within the specified time frame. If ignored, the company will be subject to administrative liability.

The time limit for a response varies and depends on the grounds for the request being sent. The legislator stipulates that the total period is ten days. When checking a group of taxpayers, it can be extended for another 10 days; when checking a foreign company it is 30 days. If a request is received to request documents from a counterparty, the response period is 5 and 10 days, depending on the requested information.

According to general rules, the period begins to be calculated on the next day after receipt of the request and ends on the last day of the established period. The day of receipt is considered the day the letter is received by the company. If, when sending by registered mail, you receive notification of the receipt of a request by mail, and you deliberately do not pick it up, the letter will still be considered delivered and the period will begin to run. Therefore, it is better to take it and answer as required by law.