What's new in 2021 for simplifiers

Tax laws have changed a lot in 2021, and these changes have impacted small businesses in many ways. Significantly more entrepreneurs and small firms have been applying the simplified tax system since 2021, since UTII has been abolished.

From 2021, the rules for calculating limits for the possibility of applying the simplified tax system have been changed. If previously the simplified tax rate was dropped if the income exceeded 150 million rubles for a calendar year and the average number of people on the payroll exceeded 100 people, then from 2021 a transition period when, if the specified values are exceeded, the simplified tax rate remains in the same regime, but are increased .

For other innovations for simplified people in 2021, read the article “ What changes to the simplified tax system should be taken into account in 2021: review .”

In connection with such adjustments, it was necessary to change the declaration form under the simplified tax system. Since the innovations have been in effect since 2021, the updated form will be used for reporting for 2021 .

The new reporting form for the simplified tax system includes the ability to indicate increased rates for increased income. There is also a field for indicating the amount of tax when applying the simplified tax system, by which the simplified tax system can be reduced if the individual entrepreneur was forced to switch from a patent to the simplified tax system before its expiration.

Read more about the new declaration under the simplified tax system in the material “ A new form of declaration of the simplified tax system for 2021 has been approved: when to apply it and what’s new .”

There are no global changes in reporting under the simplified tax system for 2021 .

Next, let's look at the closing of 2021 with simplified ones.

How to submit a declaration under simplification

A simplified tax return can be submitted on paper or electronically via telecommunications channels (TCS). A paper return can be submitted through an authorized representative of the taxpayer or by mail.

In companies using the simplified tax system, the average number of employees does not exceed 100 people. Therefore, they have the right to submit tax reports electronically on their own initiative. Inspections have no right to demand a declaration on TCS from such organizations. Such conclusions follow from paragraphs 3 and 4 of Article 80 of the Tax Code.

Attention: failure to comply with the method of submitting tax reports electronically will result in tax liability. Fine – 200 rubles. for each violation under Article 119.1 of the Tax Code.

Rules for paying the simplified tax system for 2021

The deadlines for paying the simplified tax have remained unchanged for a long time. The final payment for 2021 still falls on different dates for individual entrepreneurs and organizations.

For more information about the deadlines for paying advances under the simplified tax system in 2021, read the article “ What are the deadlines for paying taxes under the simplified tax system in 2021: table (including transfers) .”

When filling out a report on the simplified tax system for 2021 for tax payments, it is important not to make a mistake in the payment details, namely in the KBK. Otherwise, the payment will fall into the unknown , and you will have to spend some time corresponding with the tax office so that all amounts are entered correctly.

You will find the current BCCs for the simplified tax system in 2021 here: “ What are the BCCs for the simplified tax system in 2021: table for organizations and individual entrepreneurs .”

In addition to the KBK, in 2021 you need to pay attention to filling out the details of the Treasury accounts, as they have been changed.

Find out what treasury account details to use in 2021 here: «».

The procedure for submitting a declaration under the simplified tax system for 2020

So, for 2021, the declaration form under the simplified tax system is used as before - approved by order of the Federal Tax Service dated February 26, 2016 No. ММВ-7-3/99.

You can download the current form here:

The deadline for its submission coincides with the deadline for paying tax according to the simplified tax system and differs for organizations and individual entrepreneurs.

For more information about the deadlines for submitting the simplified tax system declaration, read our article “ When to submit reports under the simplified tax system in 2021: deadlines .”

Submit the form to the tax office at the place of registration of the organization/individual entrepreneur in electronic or paper form.

Responsibility for tax violations

Violation of the tax return filing schedule is regulated by Article 119 of the Tax Code of the Russian Federation. The sanctions under this article are as follows:

- a fine of 5% of the amount that should have been paid to the state budget;

- fine for the person responsible for submitting the declaration – 1000 rubles for each day of delay;

- blocking the organization's current account if payment of the fine and filing of a declaration was not made within 10 working days from the date of delay.

Failure to timely submit tax documentation may result in a desk or field tax audit.

What does the simplified tax system declaration include?

Both individual entrepreneurs and organizations must fill out the same declaration form according to the simplified tax system at the end of the 2021 tax period. Differences in the composition of the document depend on the object of taxation that the taxpayer applies.

Let's look at the composition of the simplified tax system declaration and indicate which sections need to be filled out and in what case:

If a taxpayer does not have to fill out a section, then there is no need to submit it with zeros to the tax office.

Title page

At the top of the declaration under the simplified tax system, indicate the TIN. An individual entrepreneur will see it in the notification of registration as an entrepreneur. Organizations, in addition to the TIN, need to indicate the checkpoint. This data can be viewed in the notification of registration of a Russian organization.

Correction number. If you are submitting an initial declaration for the past year, enter “0—” in the “Adjustment number” field.

When you clarify the tax that was declared in a previously submitted declaration, indicate the serial number of the adjustment (for example, “1—” if this is the first clarification, “2—” for the second clarification, etc.)

Taxable period. In the “Tax period” field, indicate the code of the tax period for which you are submitting the declaration. It can be determined in Appendix 1 to the Procedure approved by Order of the Federal Tax Service dated February 26, 2016 No. ММВ-7-3/99. In the year-end declaration, indicate code “34”. When liquidating or reorganizing, write the code “50”, and when switching to another mode – “95”.

In the “Reporting year” field, indicate the year for which you are submitting the declaration – 2021.

Submitted to the tax authority. In the “Submitted to the tax authority” field, enter the Federal Tax Service code at the place of registration. The individual entrepreneur will find it in the notice of registration as an entrepreneur. The organization code is in the notification of registration of a Russian organization. Also, the Federal Tax Service code can be determined by the registration address using the Internet service on the official website of the Federal Tax Service.

In the field “At location (accounting)”, mark with the code where you are submitting the declaration: at the place of residence of the individual entrepreneur - 120, at the location of the organization - 210. This procedure follows from Appendix 2 to the Procedure approved by order of the Federal Tax Service dated February 26, 2016 No. MMV- 7-3/99:

Taxpayer. If the simplified declaration is an individual entrepreneur, then in the “Taxpayer” field, indicate the full last name, first name, patronymic, without abbreviations, as in the passport. Organizations must indicate the full name, which corresponds to the constituent documents. For example, the charter, the constituent agreement.

OKVED. In the field “Code of the type of economic activity according to the OKVED classifier”, indicate the code of the type of entrepreneurial activity. In declarations that you submit from January 1, 2021, indicate codes according to the new OKVED 2 classifier. An exception is updated declarations for periods expired before 2017. Enter in them the same codes that were in the initial declarations. This is stated in the letter of the Federal Tax Service dated November 9, 2016 No. SD-4-3/21206.

Sections 2.1.1 and 2.1.2 are filled out by organizations and entrepreneurs that use the “income” object. Section 2.1.2 is intended for Trade Tax Payers only.

How to fill out the simplified tax system declaration for 2020

Industries affected by the coronavirus, which were exempt from paying taxes, including advance payments under the simplified tax system for the 2nd quarter of 2020, fill out the declaration as usual. The tax authority writes off advance amounts under the simplified tax system for the 2nd quarter of 2021 automatically based on the declaration data.

As a rule, it is more convenient to fill out simplified taxation tax declarations from the end, since the first sections reflect the final results - that is, the tax calculated for payment, and in subsequent sections they enter the data on which the calculation of the final amount is based.

The procedure for filling out the simplified taxation system declaration for 2020

Basic requirements for filling out the report

Order of the Federal Tax Service No. ММВ-7-3/ [email protected] dated February 26, 2016 approved instructions for filling out a declaration under the simplified tax system of income for individual entrepreneurs without employees or with hired personnel. Amounts in this report are entered in whole rubles. Pennies are rounded up. If the document is filled out by hand, you must use blue, purple or black ink.

IMPORTANT!

No corrections are allowed!

Each page of the report is printed on a separate sheet (two-sided printing is prohibited). Typically, when filling out a tax return, taxpayers do not pay attention to the fact that the numbers in the fields are aligned, but this is very important. If the form is filled out by hand, the numbers are entered from the first - left - field; when filling out electronically, the numbers are aligned to the right. If there are free cells left, put a dash. All text values are written in capital block letters.

The rules for filling out reports are the same for all types of property: both for legal entities and individual entrepreneurs.

To make filling out a declaration under the simplified tax system as clear as possible, we have compiled step-by-step instructions and ready-made samples.

Title and Section 3

These sections are filled out in the same way for any object of taxation under the simplified tax system.

The title reflects basic information:

- INN/KPP of the taxpayer;

- its name;

- reporting year;

- tax authority code;

- OKVED;

- telephone;

- FULL NAME. the person who signs the simplified tax system declaration is the taxpayer himself (individual entrepreneur or general director) or his representative.

3 codes on the title deserve attention:

Section 3 is completed by those who receive targeted funding . Data is entered according to the following parameters:

- code of the type of income (the full list of codes is given in Appendix No. 5 to the procedure for filling out a tax return, approved by order of the Federal Tax Service dated February 26, 2016 No. ММВ-7-3/99);

- date of receipt and period of use;

- total cost of target revenues;

- an amount that has not expired;

- the amount used for its intended purpose within the specified period;

- amount misused or not used within the prescribed period.

Declaration of the simplified tax system “income” for 2020

Section 2.1.1

Taxpayer identification:

- “1” – if the taxpayer makes payments to individuals (organizations and individual entrepreneurs with employees);

- “2” – if it does not make payments to individuals (individual entrepreneurs without employees).

This code is needed to understand by how many percent (100 or 50) the advance payment or tax can be reduced.

At the same time, if in the middle of the year the situation with the individual entrepreneurs changed (they were hired in the middle of the year or they were all fired), then they put in the attribute that is valid at the end of the year.

Then fill in the following information line by line:

Important

Please note that the data in the fields must be entered on an accrual basis from the beginning of the year, and not for each quarter separately!

Section 2.1.2

Fill out those whose object of taxation is income, and they pay a trade tax.

The trade fee reduces the calculated advance/tax reduced by the amount of dues paid. That is, the algorithm for reducing the trading fee is as follows:

- We calculate the advance as a percentage of income.

- We reduce the amount received by the contributions actually paid.

- We reduce the balance (if any) by the amount of the trading fee actually paid, down to zero.

We fill out the section according to the following rules:

Important

The cumulative total rule also applies to this section!

Section 1.1

a change in the place of registration during the tax period Otherwise, only line 010 is filled in.

The remaining lines are intended for the calculated advance payment or the tax itself, taking into account the reduction in contributions and trading fees.

How to calculate indicators for these lines is described in detail with formulas under the lines themselves.

Important

This section is no longer filled with an accrual total, like the previous one! Each line takes into account the previous advance payment. Please note that Section 1.1 does not include the amounts of actually paid advances/taxes, but the calculated ones! The tax office will see the actual payments on your personal accounts and compare them with the data of the simplified tax system declaration. If you made all payments on time, then there will be no problems. If any advance is paid late, the tax office will impose a penalty.

Let us note one more point: lines 20, 40, 70, 100 are advances/tax payable . Amounts with a “+” sign.

Lines 50, 80, 110 are advances/tax to reduce . These are amounts with a “-” sign.

If at the end of the year you add up, preserving the signs, the data of all lines, you should get the tax payable or refundable for the year.

The affected industries will be written off the amount indicated in line 040 of the simplified tax system declaration.

For a sample of filling out a declaration for individual entrepreneurs without employees with the taxable object “income,” see our article “ Sample for filling out a simplified taxation system declaration: step-by-step instructions .”

Let's give an example of how an organization fills out the simplified tax system declaration for 2021.

Example 1

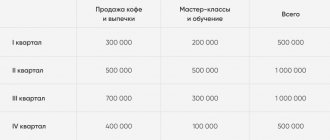

Let LLC "Mart" engage in trade in Moscow. The organization employs 4 employees.

Income amounted to:

- 1st quarter – 500,000 rubles;

- half-year – 1,200,000 rubles;

- 9 months – 1,600,000 rubles;

- year – 2,200,000 rubles.

The organization paid contributions for employees as follows:

- 1st quarter – 150,000 rubles;

- half-year – 280,000 rubles;

- 9 months – 570,000 rubles;

- year – 720,000 rubles.

Payment of trade tax:

- 1st quarter – 30,000 rubles for the 4th quarter of 2021;

- half-year - 60,000 rubles for the 4th quarter of 2021 and the 1st quarter of 2020;

- 9 months – 90,000 rubles for the 4th quarter of 2021, 1st quarter of 2020, 2nd quarter of 2021;

- year - 120,000 rubles for the 4th quarter of 2021, 1st quarter of 2020, 2nd quarter of 2021, 3rd quarter of 2021.

When to submit a simplified declaration

your simplified declaration at the end of the year. The deadline for organizations is no later than March 31 of the following year, for entrepreneurs no later than April 30.

The reporting deadline, which falls on a weekend, is moved to the nearest Monday (Clause 7, Article 6.1 of the Tax Code). Organizations report for 2021 no later than March 31, 2021.

Organizations and individual entrepreneurs that have lost the right to simplification before the end of the year report early. The simplified declaration must be submitted no later than the 25th day of the month following the quarter in which the conditions for applying the simplified tax were violated.

If during the year an organization or individual entrepreneur re-profiles its activities and “winds down” the simplified business, send two documents to the inspectorate. Within 15 working days from the date when the simplifier ceased to conduct business, submit a notice of termination of activity to the simplified tax system. No later than the 25th day of the month following the one in which you stopped operating under the simplified system, submit a tax return to the simplified tax system. This procedure is provided for in Article 346.23 of the Tax Code.

If an organization is liquidated and an individual entrepreneur loses its status, inspectors do not need notification of termination of activities on the simplified tax system. Organizations submit the declaration together with the liquidation balance sheet, and entrepreneurs - no later than April 30 of the following year (letter of the Federal Tax Service dated April 29, 2015 No. SA-4-7/7515).

Delay in a simplified tax return is an offense for which tax and administrative liability is provided (Article 106 of the Tax Code, Articles 2.1 and 15.5 of the Administrative Code).

Declaration of the simplified tax system “Income and expenses” for 2020

Section 2.2

This section is filled in with a cumulative total! That is, data is entered into the fields in total from the beginning of the year, and not in quarterly amounts.

Line by line we fill out section 2.2 like this:

Section 1.2

Unlike section 2.2, data is entered here taking into account calculated advance payments for the previous reporting period.

Fields with OKTMO (lines 010, 030, 060, 090) are filled in all at once only if the place of registration has changed during the tax period. If such an event did not occur, only line 010 is filled in.

We enter the amounts of calculated advances and taxes line by line (all formulas for calculating these amounts are given in the simplified tax system declaration under the field names):

Industries affected by coronavirus will be written off the amount indicated on line 040.

When the object of taxation is “income minus expenses”, any insurance premiums paid - both by individual entrepreneurs for themselves and for any employees - are taken into account as expenses when calculating the tax base. Therefore, filling out the simplified taxation system declaration for individual entrepreneurs and organizations does not differ.

Let's give an example of how an organization fills out the simplified tax system declaration for 2021.

Example 2

Let Mart LLC repair electrical equipment. We will provide data for 2021 to fill out the simplified tax system declaration for 2020.

Income amounted to:

- 1st quarter – 1,200,000 rubles;

- half a year – 2,000,000 rubles;

- 9 months – 2,800,000 rubles;

- year – 3,500,000 rubles;

Expenses amounted to:

- 1st quarter – 800,000 rubles;

- half-year – 1,400,000 rubles;

- 9 months – 2,000,000 rubles;

- year – 2,700,000 rubles.

The deadline for submitting the main reporting of the simplified tax authorities is approaching - the tax declaration paid under the simplified tax system. For 2021, organizations and individual entrepreneurs using the simplified tax system will actually report for the first time using the new declaration form. Read about the specifics of filling it out, as well as how it will be checked as part of a desk audit, in the material provided.

On the procedure for submitting a tax return under the simplified tax system

In 2021, the procedure for submitting a “simplified” tax return has not changed. According to Art. 346.23 of the Tax Code of the Russian Federation, at the end of the tax period, taxpayers submit a tax return to the tax authority at the location of the organization or place of residence of the individual entrepreneur within the following deadlines:

- organizations - no later than March 31 of the year following the expired tax period, that is, no later than 03/31/2017;

- individual entrepreneurs - no later than April 30 of the year following the expired tax period, that is, no later than 05/02/2017 (taking into account the postponement of weekends and holidays).

The form, format of electronic submission and procedure for filling out the declaration under the simplified tax system are approved by Order of the Federal Tax Service of Russia dated February 26, 2016 No. ММВ-7-3/ [email protected]

If the “simplified” person does not submit a declaration within the established time frame, then he will have to pay fines:

- in the amount of 5% of the amount of tax not paid on time, subject to payment (additional payment) on the basis of this declaration, for each full or partial month from the day established for its submission, but not more than 30% of the specified amount and not less than 1,000 rubles. (clause 1 of article 119 of the Tax Code of the Russian Federation);

- in the amount of 300 to 500 rubles. (administrative responsibility of officials) (Article 15.5 of the Code of Administrative Offenses of the Russian Federation).

Before moving directly to the consideration of filling out the declaration form for the simplified tax system, we will answer the most common questions regarding its submission.

Are “simplified” tax collectors required to submit a “simplified” tax return electronically?

So far, the current tax legislation has not established a mandatory procedure for submitting a declaration under the simplified tax system in electronic form, so the choice remains with the “simplified”: the declaration can be submitted both electronically and on paper.

The “simplified” organization did not carry out financial and economic activities in 2021. Should she submit a declaration under the simplified tax system?

Yes, an organization (individual entrepreneur) that has switched to the simplified tax system is required to submit a “simplified” tax return, regardless of whether it carried out its activities or not, whether it received income or losses, or whether there were cash flows through the current account.

The individual entrepreneur did not carry out activities in 2021, there was no movement on the current account. Can he submit a single (simplified) tax return instead of a “simplified” tax return?

Yes, according to paragraph 2 of Art. 80 of the Tax Code of the Russian Federation, a person recognized as a taxpayer for one or more taxes, who does not carry out transactions that result in the movement of funds in his bank accounts (at the organization’s cash desk), and who does not have objects of taxation for these taxes, has the right to submit a single statement for these taxes. (simplified) tax return.

The form of a single (simplified) tax return and the procedure for filling it out were approved by Order of the Ministry of Finance of the Russian Federation dated July 10, 2007 No. 62n.

Please note that a single (simplified) tax return is submitted to the tax authority at the location of the organization or place of residence of the individual no later than the 20th day of the month following the elapsed quarter, half-year, nine months, or calendar year.

Accordingly, for 2021, a single (tax) return had to be submitted to the tax authority no later than January 20, 2017.

Do I need to attach any documents to the tax return under the simplified tax system when submitting it to the tax authority?

No, no documents are required to be submitted to the tax authority along with such a tax return (neither primary documents confirming income or expenses, nor a book of income and expenses, nor a statement of movement on the current account, etc.) are submitted.

The only document that the tax authority has the right to ask for when a taxpayer submits a “simplified” tax return is a power of attorney if the return is submitted by a representative of the taxpayer.

Features of filling out a tax return under the simplified tax system

The declaration of tax paid in connection with the use of the simplified tax system is filled out by “simplified people” in accordance with Chapter. 26.2 Tax Code of the Russian Federation.

It consists of a title page and six sections:

– section 1.1 “The amount of tax (advance tax payment) paid in connection with the application of the simplified taxation system (object of taxation - income), subject to payment (reduction), according to the taxpayer”;

– section 1.2 “The amount of tax (advance tax payment) paid in connection with the application of the simplified taxation system (the object of taxation is income reduced by the amount of expenses), and the minimum tax subject to payment (reduction), according to the taxpayer”;

– section 2.1.1 “Calculation of tax paid in connection with the application of the simplified taxation system (object of taxation – income)”;

– section 2.1.2 “Calculation of the amount of trade tax, which reduces the amount of tax (advance payment of tax) paid in connection with the application of the simplified taxation system (object of taxation - income), calculated based on the results of the tax (reporting) period for the object of taxation from the type of entrepreneurial activities in respect of which a trade fee is established in accordance with Chapter 33 of the Tax Code of the Russian Federation”;

– section 2.2 “Calculation of the tax paid in connection with the application of the simplified taxation system and the minimum tax (object of taxation – income reduced by the amount of expenses)”;

– Section 3 “Report on the intended use of property (including funds), works, services received as part of charitable activities, targeted income, targeted financing.”

It is not necessary to submit all sections of the declaration; depending on the applied taxation object, the corresponding sections are filled out (see below). Section 3 is presented only if targeted funding is received.

The declaration is filled out on the basis of the data in the book of income and expenses, which must be fully formed by the time the declaration is filled out.

Regarding the preparation of the declaration, we note the following:

- all values of the declaration’s cost indicators are indicated in full rubles;

- The taxpayer’s signature certifies not only the title page, but also section. 1.1 and 1.2;

- The fields are filled in with the values of text, numeric, and code indicators from left to right, starting from the first (left) familiarity. When filling out a declaration using software, the values of numerical indicators are aligned to the right (last) space;

- In the absence of any indicator, a dash is placed in all familiar places in the corresponding field. When filling out a declaration using software, it is allowed that there is no framing of the acquaintances and no dashes for unfilled acquaintances.

Object of taxation “income”

If a “simplified person” has chosen the object of taxation “income,” then he must fill out and submit as part of the declaration the sheets given in Table 1.

| Tax return sections | Filling Features |

| Title page | The tax period code (Appendix 1) for 2021 is “34”. Code for the place of submission of the declaration to the tax authority at the place of registration of the taxpayer (Appendix 2): at the place of residence of the individual entrepreneur - “120”, at the location of the Russian organization - “210”. The code for the type of economic activity of the taxpayer is indicated according to OKVED 2 OK 029‑2014 (Letter of the Federal Tax Service of Russia dated November 9, 2016 No. SD-4-3/ [email protected] ) |

| Section 1.1 | The “OKTMO code” for line code 010 is filled out by the taxpayer without fail, and indicators for line codes 030, 060, 090 are indicated only when changing the location of the organization (place of residence of an individual entrepreneur). The amounts of advance payments paid no later than the following dates are calculated: 04/25/2016, 07/25/2016 and 10/25/2016. Line code 100 reflects the amount of tax subject to additional payment for the tax period, taking into account previously calculated amounts of advance tax payments. If the resulting figure is less than zero, then line 110 is filled in - the amount of tax to be reduced |

| Section 2.1.1 | The tax amount is calculated on a cumulative basis: the first quarter, half a year, nine months and the tax period. By line codes, the cumulative total is indicated: – according to line codes 110 – 113 – the amount of income received; – according to line codes 130 – 132 – the amount of the advance tax payment; – according to line code 133 – the amount of tax for the tax period; – according to line codes 140 – 143 – the amount of insurance premiums paid to employees of temporary disability benefits and payments (contributions) under voluntary personal insurance contracts provided for in clause 3.1 of Art. 346.21 Tax Code of the Russian Federation |

| Section 2.1.2 | Filled out only in the case of carrying out types of business activities in respect of which, in accordance with Chapter. 33 of the Tax Code of the Russian Federation establishes a trade tax. All indicator values are indicated on an accrual basis. Line codes 110 – 143 indicate indicators only for the type of business activity for which the trade fee is established. Indicator values reflected by line codes 110 – 143 sections. 2.1.2, are included in the values of indicators for line codes 110 - 143 sections. 2.1.1. The amount of the trade fee indicated on lines 160 – 163 is taken into account when filling out section. 1.1 when calculating advance payments and tax for the tax period. The amount of the trade fee that reduces the tax cannot be greater than the difference between the tax and insurance premiums from the type of activity in respect of which the trade fee is paid. In this case, the amount of the trade fee cannot exceed the difference between the amount of tax and the amount of insurance premiums for the taxpayer as a whole |

| Section 3 | Section 3 is filled out by taxpayers who received targeted financing, targeted revenues and other funds specified in clauses 1 and 2 of Art. 251 Tax Code of the Russian Federation. Section 3 does not include funds in the form of grants to autonomous institutions. The names and codes of targeted funds are given in Appendix 5. Section 3 contains data from the previous tax period on funds received but not used, the period of use of which has not expired, as well as those for which there is no period of use. |

Object of taxation “income minus expenses”

If a “simplified” person has chosen the object of taxation “income minus expenses,” then he must fill out and submit as part of the declaration the sheets given in Table 2.

table 2

| Tax return sections | Filling Features |

| Title page | The tax period code (Appendix 1) for 2021 is “34”. Code for the place of submission of the declaration to the tax authority at the place of registration of the taxpayer (Appendix 2): at the place of residence of the individual entrepreneur - “120”, at the location of the Russian organization - “210”. The code for the type of economic activity of the taxpayer is indicated according to OKVED 2 OK 029‑2014 (Letter of the Federal Tax Service of Russia No. SD-4-3/ [email protected] ) |

| Section 1.2 | The “OKTMO code” for line code 010 is filled out by the taxpayer without fail, and indicators for line codes 030, 060, 090 are indicated only when changing the location of the organization (place of residence of an individual entrepreneur). The amounts of advance payments for the first quarter, half of the year and nine months of 2021 are calculated based on the data from section. 2.2. Line 100 is filled in if the value on line 100 is greater than or equal to zero and the amount of calculated tax is greater than or equal to the amount of the minimum tax. Line 110 is completed if the amount of calculated advance payments is greater than the amount of calculated tax, and also provided that the amount of calculated tax is greater than or equal to the amount of the minimum tax. If the amount of calculated tax for a tax period is less than the amount of calculated minimum tax, then the amount of tax to be reduced for the tax period is indicated minus the amount of the minimum tax payable for the tax period. This indicator is reflected provided that the amount of calculated tax is less than the minimum tax and the amount of calculated advance payments for tax is greater than the amount of calculated minimum tax. Line 120 is completed if the amount of calculated tax for the tax period is less than the amount of the calculated minimum tax, the amount of the minimum tax payable for the tax period is indicated minus the amount of calculated advance tax payments. If the amount of the minimum tax payable for the tax period is less than the amount of advance payments for tax minus the amount of advance payments for tax to be reduced, reflected under line codes 050 and 080 of section. 1.2, then line code 120 is marked with a dash |

| Section 2.2 | By line codes, the cumulative total is indicated: – according to line codes 210 – 213 – the amount of income received; – according to line codes 220 – 223 – the amount of expenses incurred; – according to line codes 240 – 243 – tax base; – according to line codes 250 – 253 – the amount of loss received; – according to line codes 270 – 273 – the amount of calculated tax. The amount of loss received in the previous tax period is reflected separately using line code 230. The amount of the calculated minimum tax is entered using line code 280 |

| Section 3 | Section 3 is filled out by taxpayers who received targeted financing, targeted revenues and other funds specified in clauses 1 and 2 of Art. 251 Tax Code of the Russian Federation. Section 3 does not include funds in the form of grants to autonomous institutions. The names and codes of targeted funds are given in Appendix 5. Section 3 contains data from the previous tax period on funds received but not used, the period of use of which has not expired, and also for which there is no period of use |

Control ratios for tax returns under the simplified tax system

The control ratios for the “simplified” tax return are given in the Letter of the Federal Tax Service of Russia dated May 30, 2016 No. SD-4-3/ [email protected]

Control ratios are in principle issued for use in the practical work of tax authorities. At the same time, taxpayers, including “simplified” tax returns, can check their tax returns under the simplified tax system using these ratios, which will allow them to correctly calculate the “simplified” tax and avoid additional communication with tax authorities.

After all, if the control ratios are not met, the tax inspector will have to inform the taxpayer about this with a requirement to provide the necessary explanations within five days or make appropriate corrections within the prescribed period; if this requires the taxpayer to appear directly at the tax authority, then send a notice of summoning the taxpayer (fee payer, tax agent) to give explanations. If, after reviewing the provided explanations and documents, or in the absence of explanations, a violation of the legislation on taxes and fees is established, then an inspection report is drawn up in accordance with Art. 100 Tax Code of the Russian Federation. Please note that the inspector performs these actions in a non-automated mode during the desk audit of a tax return under the simplified tax system.

Control ratios according to the said declaration are divided into intra-document and inter-document.

Intra-document relationships establish rules between different sections of the declaration:

- when applying the object of taxation “income” - between Sec. 1.1 and sec. 2.1.1 and 2.1.2;

- when applying the object of taxation “income minus expenses” - between Sec. 1.2 and sec. 2.2.

In principle, these relationships echo the formulas that are indicated in the declaration form itself. If all calculations are made correctly, then the control ratios will be satisfied.

Inter-document control relationships establish rules using external sources (for example, reports on insurance premiums RSV-1 Pension Fund, 4‑FSS). Since the tax authorities have this information thanks to interdepartmental exchange with the Pension Fund of the Russian Federation and the Social Insurance Fund, these relationships, as well as intra-document ones, are monitored automatically during the desk audit of the tax return under the simplified tax system. Please note that starting from 2021, reporting on insurance premiums will be submitted to the tax authorities, so tax authorities will have information about accrued and paid insurance premiums directly. So the “simplified” people must check the amounts of paid insurance premiums, benefits, payments under insurance contracts (clause 3.1 of Article 346.21 of the Tax Code of the Russian Federation), by which the amount of tax is reduced when applying the object of taxation “income” and which are indicated in the reports on insurance premiums.

As stated above, when submitting a tax return under the simplified tax system, there is no need to submit additional documents to the tax authority, including a ledger for recording income and expenses. But as part of a desk audit based on Art. 88 of the Tax Code of the Russian Federation, in established cases, the tax authority has the right to request from the taxpayer explanations supported by documents. In this case, in particular, the book of income and expenses and primary documents may be required. These actions are already carried out by tax authorities in a non-automated mode.

Tax authorities have the right to request additional documents as part of a desk audit in the following cases:

- identifying errors in the declaration;

- identifying contradictions between the information contained in the declaration and the information contained in the documents available to the tax authority;

- statement in the loss declaration.

Let us note that when applying the taxation object “income minus expenses”, a loss may be incurred as a result of financial and economic activities. In this case, the minimum tax is paid. In this situation, the “simplified person” must be prepared for the fact that the tax authority has the right to demand that the taxpayer provide, within five days, the necessary explanations justifying the amount of the loss received.

When requesting additional documents from “simplified people” as part of a desk audit, as a rule, tax officials require the presentation of a book of income and expenses. The control relationships between the tax return and the book of income and expenses (KUDR) are shown in Table 3.

Table 3

| Control ratio | Norm ch. 26.2 Tax Code of the Russian Federation | Violation in case of failure to comply with the control ratio |

| Object of taxation “income” | ||

| Sections 2.1.1, 2.1.2 line 110 = KUDR section. I column 4 (total for the first quarter); | Article 346.15 | Incorrect determination of income taken into account when calculating the tax base: – for the first quarter; |

| section 2.1.1, 2.1.2 line 111 = KUDR section. I column 4 (total for half a year); | – for half a year; | |

| section 2.1.1, 2.1.2 line 112 = KUDR section. I column 4 (total for nine months); | – in nine months; | |

| section 2.1.1, 2.1.2 line 113 = KUDR section. I column 4 (total for the year, certificate to section I line 010) | – for the tax period | |

| Object of taxation “income minus expenses” | ||

| Section 2.2 line 210 = KUDR section. I column 4 (total for the first quarter); | Article 346.15 | Incorrect determination of income taken into account when calculating the tax base: – for the first quarter; |

| section 2.2 line 211 = KUDR section. I column 4 (total for half a year); | – for half a year; | |

| section 2.2 line 212 = KUDR section. I column 4 (total for nine months); | – in nine months; | |

| section 2.2 line 213 = KUDR section. I column 4 (total for the year, certificate to section I line 010) | – for the tax period | |

| Section 2.2 line 220 = KUDR section. Column I 5 (total for the first quarter); | Article 346.16 | Incorrect determination of expenses taken into account when calculating the tax base: – for the first quarter; |

| section 2.2 line 221 = KUDR section. I column 5 (total for half a year); | – for half a year; | |

| section 2.2 line 222 = KUDR section. I column 5 (total for nine months); | – in nine months; | |

| section 2.2 line 223 = KUDR section. I column 5 (total for the year, certificate to section I line 020) | – for the tax period; | |

| Section 2.2 line 230 = KUDR section. III line 130) | Clause 7 of Art. 346.18 | Incorrect (unjustified) reduction of the tax base for the tax period |

The deadlines for submitting a tax return under the simplified tax system for 2021 are suitable: no later than 03/31/2017 (for organizations) and no later than 05/02/2017 (for individual entrepreneurs).

For 2021, “simplified” must report on a new tax return form, the specifics of filling out which are discussed in this material.

To help organizations and individual entrepreneurs using the simplified tax system, control ratios to the tax return are also considered, including the relationship between the indicators of the declaration and the book of income and expenses.