Most often, individual entrepreneurs choose a simplified taxation system, since it is truly simpler and, in most cases, more financially profitable.

Being under a simplified tax payment regime, legal entities and individual entrepreneurs are exempt from some taxes required under the main taxation system.

So, if you are an entrepreneur, then you have no tax as an individual on business income, no VAT, with the exception of possible tax upon import at customs or execution of a simple partnership agreement or trust management of property.

There are options when there is no property tax used in business activities. Today, “simplified” does not exclude tax on property used in your business with cadastral value. But if your type of real estate is not on the cadastral list, then there is no tax accordingly. However, much depends on the subject; everyone has their own concepts about tax-free real estate and their own preferences. If you still need to pay this type of tax, then you, as an individual entrepreneur, do not calculate it yourself and do not submit any declarations. The tax office does this for you by sending you a completed notification. You must only pay the specified amount no later than December 1 of the year following the billing year.

Important! Your taxes as an individual entrepreneur are in no way related to the taxes of your employees.

Filling out the simplified tax system declaration for 2021 (“income”).

Declaration under the simplified tax system “income” 2021 is a tax report that payers of the “simplified” tax for 2017 must submit. It contains information about income received and expenses incurred that reduce tax. The simplified tax system “income” declaration reflects the calculation and payment of advance payments to the state budget.

Filling out the simplified tax system “income” declaration 2021 has its own nuances. In 2018, the declaration under the simplified tax system “income” for 2021 is filled out according to the form approved by order of the Federal Tax Service of the Russian Federation on February 26, 2016 No. ММВ-7-3 / [email protected] Then the barcode on the title page was changed in the form and new fields were added for entering information on payment of trade tax.

Submitting a report using an outdated form is a serious violation for which the Federal Tax Service has the right to impose a fine and block the current account of a business entity.

How to calculate tax

Tax is calculated simply: the tax base is multiplied by the tax rate.

The simplified tax system has two options for calculating the tax base and two rates. They depend on the chosen tax regime.

If your mode is “income”, then your tax base is the sum of your entire entrepreneurial income for the required period. Your tax rate in this case is 6%.

If you chose the “income minus expenses” mode, then the tax base fully corresponds to the name of the mode, that is, it is the difference between all business profits for the required period and the expenses incurred by the business. But there are expenses that the law does not allow to be deducted from the tax base. More information about this is in the Tax Code, namely in Article 346.16. In this mode, the tax rate is 15%.

Regional authorities have the right to lower these rates both for all entrepreneurs and for certain categories.

Procedure for filling out the report

The declaration consists of a title page and six sections. When preparing the simplified tax system “income” declaration for 2021, the filling rules approved by the same order as the form are applied. Among the main requirements it is necessary to highlight the following:

- Individual entrepreneurs and organizations using the simplified tax system must fill out the title page and sections directly related to the object of taxation;

- when filling out the simplified taxation system “income” declaration, section 3 is attached only to “simplified people” who received funds as part of targeted financing;

- the report does not need to be stapled, it is better to fasten it with a paper clip;

- all indicators are indicated in full rubles, without kopecks;

- It is recommended to write in black ink;

- all letters must be printed in capitals (the same applies to filling out on a computer);

- errors in the document cannot be corrected using a correction tool;

- all pages must be numbered;

- You can specify only one indicator in each field;

- Document printing should only be one-sided;

- empty cells must be filled with dashes.

An example of filling out the simplified tax system “income” declaration for 2021 is presented below.

Rule two - the base and tax are NOT written quarterly

In the declaration, the individual entrepreneur reflects his income, expenses and taxes paid. Each amount in the corresponding column is written not for its specific quarter, but as a cumulative total.

For example, no one will have problems with the first quarter, but there may already be problems with the second. So for the second quarter, you indicate income, expenses and taxes as the amount for two quarters together, and not separately for the second. That is, you sum up the indicators of the first and second quarters and write the resulting amount in the columns of the second quarter.

Thus, for the third quarter you report the sum of the three quarters together, and for the fourth quarter you report the sum for the entire year.

How to fill out a simplified taxation system declaration: sequence of actions

- Check that the existing report form is up to date. A sample of the current simplified taxation system “income” declaration form can be downloaded here.

- Determine which sections need to be completed. If “Income” is selected as the object of taxation, the taxpayer must fill out: title page, sections 1.1, 2.1.1. and 2.1.2. There is no need to submit unnecessary sheets. The example given here for filling out a declaration under the simplified tax system “income” can be taken as a basis when drawing up a similar reporting form for your own individual entrepreneur or company.

- Fill in the fields on the title page: indicate the TIN and KPP, activity code according to OKVED. In the “Taxpayer” field, enter the name of the organization or full name of the entrepreneur. All codes necessary for filling out the title page are contained in the appendices to the Procedure for filling out the declaration. The section intended to be filled out by the Federal Tax Service inspector should be left blank.

- Complete sections 2.1.1 and 2.1.2. In this case, you can use the calculation formulas indicated in the form. In sections 2.1.1 and 2.1.2, line 140 of the declaration under the simplified tax system “income”, as well as lines 141-143 are intended to indicate the amounts of payments, the list of which is given in clause 3.1 of Art. 346.21 of the Tax Code of the Russian Federation (paid insurance premiums, sick leave, contributions for voluntary personal insurance). Using these payments makes it possible to reduce the amount of tax payable.

- If a business entity does not pay the trade fee, there is no need to fill out section 2.1.2.

- Proceed to filling out section 1.1. Here you need to indicate the OKTMO code, the amount of advance payments to be paid, the amount of taxes subject to additional payment or reduction for the tax period.

- If during the reporting period an individual entrepreneur or organization received funds in the form of targeted revenues, it is necessary to fill out section 3. Information on each receipt is indicated here.

How to submit 3 personal income taxes to an individual entrepreneur

Form 3-NDFL is submitted to the tax office at the place of registration of the individual entrepreneur. The declaration can be submitted either on paper or electronically. A sample document can be obtained from the inspector or downloaded from the official website of the Federal Tax Service.

The deadline for filing personal income tax declaration 3 is April 30 of the year following the reporting period. An exception to the established rules applies only to a declaration filed for the purpose of obtaining tax deductions. In this case, there is no time frame; you just need to remember the statute of limitations, which is 3 years.

Separately, we should dwell on the situation with the loss of the simplified tax system. If you need to submit a declaration due to a change in the taxation regime, you must inform the tax office about this within 15 days.

You will also have to provide a package of documents, incl. declarations for HSS and 4-NDFL. The last form assumes a forecast for future personal income tax transfers for the reporting period, on the basis of which advance payments are formed for transfers based on the results of the 2nd, 3rd and 4th quarters.

Zero declaration

How to fill out a declaration under the simplified tax system “income” if the entity did not carry out activities during the year? In such cases, you only need to fill out the title page. On all other pages, the INN/KPP, OKTMO code, and taxpayer characteristics are written down. In the cells where the amounts of income, taxes and payments should be indicated, dashes are added. The report must be submitted to the Federal Tax Service within the deadlines established for reporting. The example of filling out the “zero line” given here for the simplified tax system “income” declaration 2021 clearly demonstrates what a well-drafted document should look like.

Declaration under the simplified tax system “income” 2021 (sample of filling out the “zero line”)

Deadline for filing a declaration with the Federal Tax Service

| Tax regime name | Name of the declaration | Deadline for filing a declaration with the Federal Tax Service |

| Simplified taxation system (STS) | Declaration of the simplified tax system | Based on the results of the calendar year (but no later than April 30 of the following year) |

| General taxation system (GTS) | Declaration 3-NDFL | Based on the results of the calendar year (but no later than April 30 of the following year) |

| Declaration 4-NDFL | No later than 5 days after the end of the month in which the first income appeared | |

| VAT declaration | Based on the results of each quarter (but no later than the 20th day of the first month of the next quarter) |

An example of filling out a declaration under the simplified tax system “income” if there is an activity

IP Karpov V.S. works without employees on the simplified tax system “income”. The tax rate is 6%.

In 2021 he earned:

- in the first quarter – 178,000 rubles;

- in the second quarter - 165,000 rubles, total income for the half-year amounted to 343,000 rubles. (178,000 + 165,000);

- in the third quarter - 172,000 rubles, total income for 9 months amounted to 515,000 rubles. (178,000 + 165,000 + 172,000);

- in the fourth quarter - 169,000 rubles, total annual income amounted to 684,000 rubles. (178,000 + 165,000 + 172,000 + 169,000).

We will reflect these amounts on lines 110-113 of section 2.1.1.

The amount of calculated advances for quarters on an accrual basis is reflected in lines 130-133 of section 2.1.1:

- For the 1st quarter – 10,680 rubles.

- For half a year – 20,580 rubles.

- For 9 months – 30,900 rubles.

- For the year – 41,040 rubles.

During 2021, the individual entrepreneur paid “for himself” fixed insurance premiums in the total amount of 27,990 rubles, including the following transferred to the Federal Tax Service:

- in the 1st, 2nd and 3rd quarter - 6500 rubles each,

- in the 4th quarter 8490 rub.

These expenses will be reflected on an accrual basis in lines 140-143 of section 2.1.1.

Section 1.1 is filled out based on the data in section 2.1.1:

- Line 020 (page 130 − page 140 of section 2.1.1) = 10,680 – 6500 = 4180 rub.

- Line 040 (page 131 − page 141 of section 2.1.1) - line 020 of section 1.1 = 20,580 – 13,000 – 4180 = 3,400 rubles.

- Line 070 (page 131 − page 141 of section 2.1.1) – (line 020 + line 040 of section 1.1) = 30,900 – 19,500 – 7580 = 3820 rub.

- Line 100 (page 131 − page 141 of section 2.1.1) – (line 020 + line 040 + line 070 of section 1.1) = 41,040 – 27,990 – 11,400 = 1,650 rubles.

How to fill out a declaration under the simplified tax system “income” for 2021 for an individual entrepreneur without employees?

Important information! Pay special attention to the fact that they promise to write off taxes and contributions for the second quarter of 2021 for those individual entrepreneurs who belong to the most affected areas of the economy. They also promise to reduce insurance premiums by 12,130 rubles for such individual entrepreneurs (read more at this link). Read about other measures to support individual entrepreneurs in connection with the pandemic at this link. Important update. The declaration under the simplified tax system is expected to be updated. The procedure for filling it out will change slightly, as I wrote about at this link:

The declaration under the simplified tax system will change in 2021. This is important, take note.

What form should I use to submit a declaration under the simplified tax system for 2021? Old or new?

I remind you that you can subscribe to my video channel on Youtube using this link:

https://www.youtube.com/c/DmitryRobionek

But we submit the declaration under the simplified tax system for 2021 using the “old” form, which I describe below.

Good afternoon, dear individual entrepreneurs!

We have already learned how to fill out a zero declaration under the simplified tax system in this short article:

Of course, most individual entrepreneurs work and receive real income. In this case, they need to fill out a declaration for individual entrepreneurs, where there are cash receipts for the reporting year. That is, today we will talk about filling out a NON-zero declaration.

Before starting the article, I note that the form of the declaration under the simplified tax system may change in 2021. Therefore, it is better to use accounting programs and services that are regularly updated by developers. And in no case should you keep records completely manually, since everything changes too quickly.

So, let's look at the issue of filling out a NON-zero declaration using a specific example:

- Individual entrepreneur on a simplified basis (USN 6%) without employees;

- The individual entrepreneur has not switched to a regime where the tax according to the simplified tax system is calculated by the Federal Tax Service (it is expected that from July 1, 2021, it will be possible to voluntarily refuse to submit a declaration under the simplified tax system “income” for those individual entrepreneurs who use online cash registers. At the time of writing this article, this is so far the draft law. Read more here).

- You need to draw up a declaration for 2021 (if you draw up a declaration for 2021, remember that the amount of insurance contributions for pension and health insurance will be different);

- An individual entrepreneur is not a payer of the trade tax;

- Throughout the year, the rate of 6% for the simplified tax system was maintained;

- The individual entrepreneur worked for a full year;

- There was income for the reporting year.

- All contributions to compulsory pension and health insurance were made in full and on time;

- The individual entrepreneur did not receive property (including money), work, services as part of charitable activities, targeted income, or targeted financing.

- The declaration must be in the 2021 form (according to the order of the Federal Tax Service dated February 26, 2016 No. ММВ-7-3 / [email protected] )

What program will we use to draw up a declaration under the simplified tax system?

We will use an excellent (and free) program called “Legal Taxpayer”.

Don't be afraid, I have detailed instructions on how to install and configure it. Read this article first and install it on your computer:

https://dmitry-robionek.ru/soft-for-biz/nalogoplatelshhik-jurlic.html

We will assume that you have installed the program and entered your individual entrepreneur details correctly.

Important. The “Legal Taxpayer” program is constantly updated. This means that it must be updated to the latest version before completing the declaration. The program itself can be downloaded here: https://www.nalog.ru/rn77/program/5961229/

Step 1: Launch the “Legal Taxpayer” program

And immediately in the menu “Documents” - “Tax reporting” we create a tax return template according to the simplified tax system. To do this, click on the icon with the “Create” icon

And then select form No. 1152017 “Declaration of tax paid in connection with the application of the simplified taxation system”

Yes, another important point

Before drawing up the declaration, it is necessary to indicate the year for which we will draw it up. To do this, you need to select the tax period in the upper right corner of the program.

For example, for the declaration for 2021 you need to set the following settings:

By analogy, you can set other periods for the declaration. For example, if you are creating a declaration for 2021, then it is clear that you need to indicate 2021.

Step 2: Fill out the Cover Sheet

The first thing we see is the title page of the declaration, which must be filled out correctly.

Naturally, I took as an example the fairy-tale character Ivan Ivanovich Ivanov from the city of Ivanovo =) You insert your REAL details for the individual entrepreneur.

Some data is pulled up automatically. For example, full name and tax identification number, your tax office number, OKTMO...

Let me remind you that the “Legal Taxpayer” program must first be configured, and once again I refer you to this article:

https://dmitry-robionek.ru/soft-for-biz/nalogoplatelshhik-jurlic.html

The fields highlighted in brown need to be corrected.

1. Since we are making a declaration for the year, then the period must be set accordingly. Just select the code “34” “Calendar year” (see picture)

It should look like this:

Next, you need to add your BASIC code according to the OKVED classifier. Let me remind you that when registering an individual entrepreneur, you indicated the main and additional activity codes for your business.

Important: Please note that in the summer of 2021, new activity codes under OKVED-2 were introduced. This means that in the declaration for 2016 (and for subsequent years) it is necessary to indicate new codes, according to OKVED-2. If you indicate the old OKVED-1 code, the declaration will not be accepted. Read more here:

Here you need to specify the main activity code. For example, I indicated the main code 62.09. Of course, it may be different for you.

If you submit the declaration yourself, then you DO NOT need to touch anything in these cells. (see picture below)

We are not touching anything here, since we will be delivering the property ourselves, without representatives. There should be a unit.

We don’t touch anything else on the title page, since we will submit the declaration during a personal visit, without representatives.

Step: Fill out section 1.1 of our declaration

At the very bottom of the program, click on the “Section 1.1” tab and you will see a new sheet that also needs to be filled out.

Many people are scared because it is inactive by default and does not allow you to fill in the necessary data.

It's okay, we can handle it =)

To activate this section, you need to click on this “Add Section” icon (see the figure below), and the sheet will immediately be available for editing.

Everything is quite simple here: you just need to register your OKTMO code (All-Russian Classifier of Territories of Municipal Entities) in line 010.

If you don’t know what OKTMO is, then read it here. In my example, the non-existent OKTMO 1111111 is indicated.

You indicate your real OKTMO code, which you can check with your tax office. By the way, there you can also clarify the code of your Federal Tax Service, which must be indicated on the title page (in our example, this is code 3701).

We don’t touch anything else on sheet 1.1 of our declaration.

But if OKTMO has changed during the year, then you must indicate the new code in the appropriate lines. This can happen, for example, when changing the details of the tax office, or when changing the place of residence of the individual entrepreneur.

Step: Fill out section 2.1.1 “Calculation of tax paid in connection with the application of the simplified taxation system (object of taxation - income)”

Again, at the very bottom of our document, select the appropriate tab:

“Section 2.1.1” and activate the sheet with the “Add Section” button (in the same way as we activated the previous sheet)

And we see the most important sheet of our declaration that will have to be filled out =)

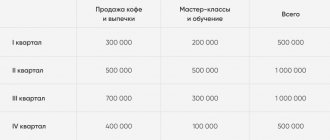

Here you need to enter data on the income of our individual entrepreneur for the reporting year. Suppose a certain Ivan Ivanovich Ivanov received the following quarterly income for the year:

- Quarter 1: 200,000 rubles;

- Quarter 2: 250,000 rubles;

- Quarter 3: 400,000 rubles;

- Quarter 4: 200,000 rubles;

For convenience, I took small amounts of income and rounded to zero to make it easier to count. It is clear that you may have amounts in kopecks, in which case you need to round up to whole rubles according to the rules of arithmetic.

Please note that lines No. 110, 111, 112, 113 of the declaration must be filled in with an INCREMENTAL total:

- 200 000

- 450 000

- 850 000

- 1 050 000

That is, we sum up each quarter with the previous quarters!

Let our individual entrepreneur pay mandatory contributions to pension and health insurance as follows:

- Quarter 1: 10218.50 rubles

- Quarter 2: 10218.50 rubles

- Quarter 3: 10218.50 rubles

- Quarter 4: 10218.50 rubles

Then fill in No. 140, 141, 142, 143 as follows:

- 10219

- 20437

- 30656

- 40874

(taking into account rounding to whole rubles, according to the rules of arithmetic)

Once again, I would like to draw your attention to the fact that we contribute income and contributions to pension and health insurance on an ACCRUAL TOTAL. Otherwise, the declaration will be incorrect.

Of course, you provide information on your contributions to compulsory health and pension insurance.

Also, if at the end of the previous year you paid 1% over 300,000 rubles for compulsory pension insurance, then this amount is also included in the declaration. If you paid 1% of the amount exceeding 300,000 rubles of annual income during the reporting year, then take them into account too.

So, in lines No. 140, 141, 142, 143 of the declaration, it is necessary to make mandatory insurance contributions on an accrual basis.

IMPORTANT:

Pay attention to the hints on these lines!

The fact is that lines 140-143 should not exceed the corresponding values of lines 130-133 (this is due to tax deductions for mandatory contributions to pension and health insurance from tax under the simplified tax system)

We also need to indicate the tax rate according to the simplified tax system in lines 120-123 for the quarter, half-year, 9 months. and for a year.

This is done very simply. To do this, just click on the desired field and select a rate of 6% (let me remind you that we are considering individual entrepreneurs on the simplified tax system of 6% without income and employees).

Yes, one more thing. In field 102, enter the number “2”. It means that the declaration is submitted by an individual entrepreneur without employees:

2 – individual entrepreneur who does not make payments or other remuneration to individuals

After filling out the lines:

- 110-113

- 120-123

- 140-143

press the “P” key to recalculate the declaration formulas.

Lines 130-133 will be filled in automatically.

This is what we should get:

Everything is ready, all that remains is to send it to print

But first, let me remind you that you need to pay tax according to the simplified tax system for the year by April 30, following the reporting year! It is better to do this before submitting the declaration, of course.

That is, we first pay tax according to the simplified tax system, and then submit the declaration. In order to pay this tax according to the simplified tax system, it is necessary to generate a separate payment slip (or receipt) for the tax service.

Paid programs (for example, 1C-Entrepreneur) generate it automatically, right during the preparation of the declaration itself. By the way, in 1C it is created completely automatically, based on the cash flow data that the entrepreneur enters into the program Therefore, it is better to immediately target paid accounting programs.

Step: Submit your tax return

But let's return to the article... First, we check that the declaration is filled out correctly using the program. To do this, click on the button with the “K” icon - “document control”.

If there are filling errors, you will see them at the bottom of the program screen.

If the declaration has been checked for control values, you will see the message:

After checking the declaration, we print it in TWO copies and go to your tax office, where you are registered. You need to sign the declaration at the tax office, not at home.

Now you don’t need to file anything (this has been the case since 2015). You give one copy to the inspector, and he signs the other, stamps it and gives it to you. You keep it, don’t lose it =)

And don’t forget to pay the tax according to the simplified tax system before submitting the declaration itself!

Example of a completed declaration

For clarity, I present the result of our scientific research =)

This is what we ended up with:

PS Despite the fact that the program that we have studied in this manual is very good, I still recommend using paid accounting programs and services. The fact is that they generate declarations based on ALREADY entered data on business transactions of individual entrepreneurs.

Here, they still need to be correctly prepared and entered. And if there was an error somewhere in the source data (for example, the numbers were rounded incorrectly), then the declaration will be incorrect, despite the control check of the data.

Therefore, still look towards paid programs that allow you to prepare not only declarations, but also do many other operations. For example, generate the same receipts (or payment orders) for payment of mandatory insurance premiums for individual entrepreneurs.

PS The article contains screenshots of the “Legal Taxpayer” program. You can find it on the official website of the Federal Tax Service of the Russian Federation at this link: https://www.nalog.ru/rn77/program/5961229/

Best regards, Dmitry.

Receive the most important news for individual entrepreneurs by email!

Stay up to date with changes!

By clicking on the “Subscribe!” button, you consent to the newsletter, the processing of your personal data and agree to the privacy policy.