Financial statements

During reorganization, the newly formed enterprise undertakes the obligation to submit year-end reporting for its predecessor within three months after the end of the year (Article 23-1(5) of the Tax Code). A copy of the reporting is submitted, in addition to the Federal Tax Service, to the statistics service. The period for which information is included in it: from the beginning of the year until the date preceding the date of state registration of the results of the reorganization.

How are the financial statements of an organization prepared during reorganization in the form of merger ?

The assignee also prepares reports for himself – the so-called introductory reports. It is formed from the data transferred by the predecessor on the basis of the transfer deed and adjusted to the amounts of business transactions that took place after its preparation. Typically, the act is drawn up as close as possible to the date of reorganization, and then the data, together with the adjustment amounts as of the registration date, are entered into the balance sheets and transferred to the successor (Federal Law No. 402 of 06-12-11, Articles 16-6,7) . Additions to the act are recorded.

Attention! Public sector organizations are exempt from compiling primary reporting.

The first reports after the reorganization are not submitted to the regulatory authorities: the obligation to submit them arises only at the end of the year.

How to draw up and approve a transfer deed during the reorganization of a legal entity ?

Initial stage of joining

A merger is a form of reorganization in which one or more organizations cease to exist as separate legal entities and become part of another company. In what follows, for simplicity, we will refer to the affiliating organization as the “main” organization.

The starting point is for the owners to make an appropriate decision. It must be sent to the “registering” Federal Tax Service within three working days, along with a written message about the start of the accession. Having received these papers, inspectors must make an entry in the state register stating that the companies are in the process of reorganization. Officials are given three working days for this.

In addition, companies are required to inform the Pension Fund and the Social Insurance Fund office in writing about the upcoming accession. This should also be done within three working days (clause 3 of part 3 of article 28 of the Federal Law of July 24, 2009 No. 212-FZ).

Then twice, at intervals of a month, a notice of the reorganization is supposed to be published in special publications. And also, within five working days from the date of filing the application with the Federal Tax Service, notify all known creditors about the initiated process (Article 13.1 of the Federal Law of 08.08.01 No. 129-FZ “On State Registration of Legal Entities and Individual Entrepreneurs”).

Next, you should prepare a new version of the constituent documents of the company, which is being joined by another legal entity. At this stage, it is also necessary to conduct an inventory of the property and obligations of all participants - and the joining organization. This is stated in paragraph 2 of Article 12 of the Federal Law of November 21, 1996 No. 129-FZ “On Accounting”.

Forms of reorganization

The Civil Code specifies five forms of reorganization:

- merger;

- accession;

- separation;

- selection;

- transformation.

In this case, the forms can be combined simultaneously (Article 57 of the Civil Code of the Russian Federation). For example, split and join, split and join, split and merge, or split and merge.

A legal entity is considered reorganized, with the exception of cases when this occurs in the form of affiliation, from the moment of state registration of legal entities created as a result of the reorganization. When one legal entity merges with another, the first of them is considered reorganized from the moment an entry is made in the Unified State Register of Legal Entities about the termination of the activities of the merged legal entity.

As a rule, reorganization always has reasons and goals. In some cases, it is carried out voluntarily, at the request of the legal entity itself, or by the decision of the founders. And in this case, the reorganization is carried out in any of the listed forms.

Sometimes, in order to limit the monopolistic activities of a company, forced reorganization occurs - in the form of division and spin-off. This procedure is provided for in Art. 38 of the Federal Law of July 26, 2006 No. 135-FZ.

Another procedure by which a legal entity can be reorganized is privatization.

What does the Tax Code say regarding the reorganization of a legal entity?

According to paragraphs 1 and 2 of Art. 50 of the Tax Code of the Russian Federation, the successor(s) of a reorganized legal entity are entrusted with:

- the obligation to pay taxes of a reorganized legal entity, regardless of whether the facts and (or) circumstances of non-fulfillment or improper fulfillment of this obligation by the reorganized legal entity were known to the successor (legal successors) before the completion of the reorganization;

- the obligation to pay all penalties for the obligations transferred to him;

- the obligation to pay the due amounts of fines imposed on a legal entity for committing tax offenses before the completion of its reorganization.

Note:

By virtue of clause 3 of Art. 50 of the Tax Code of the Russian Federation, the reorganization of a legal entity does not change the deadlines for fulfilling the obligation to pay taxes by the legal successor(s) of this legal entity.

Let us outline some nuances associated with the form of reorganization:

- when several legal entities merge, their legal successor in terms of fulfilling the obligation to pay taxes is the legal entity that arises as a result of such merger;

- when one legal entity merges with another legal entity, the legal successor of the merged legal entity in terms of fulfilling the obligation to pay taxes is the legal entity that merged it;

- upon division, legal entities arising as a result of such division are recognized as legal successors of the reorganized legal entity in terms of fulfilling the obligation to pay taxes. If there are several legal successors, the share of participation of each of them in the performance of the duties of the reorganized legal entity to pay taxes is determined in the manner prescribed by civil law;

- when one or more legal entities are separated from a legal entity, succession in relation to the reorganized legal entity in terms of the fulfillment of its obligation to pay taxes (penalties, fines) does not arise. If, as a result of the separation of one or more legal entities from a legal entity, the taxpayer is unable to fulfill in full the obligation to pay taxes (penalties, fines) and such reorganization was aimed at failure to fulfill this obligation, by a court decision the separated legal entities may jointly and severally fulfill the obligation for the payment of taxes (penalties, fines) of a reorganized legal entity;

- when one legal entity is transformed into another legal entity, the newly created legal entity is recognized as the legal successor of the reorganized legal entity in terms of fulfilling the obligation to pay taxes.

Period until completion of accession

Next you need to collect a package of documents. It consists of a deed of transfer, an application for state registration of the acquiring legal entity, a decision on reorganization, a document on payment of state duty and other papers. The full list is given in paragraph 1 of Article 14 of the Federal Law of 08.08.01 No. 129-FZ.

The package of documents must be submitted to the “registering” tax office and wait for it to make an entry in the Unified State Register of Legal Entities. The appearance of such a record will mean that the company being merged has ceased to exist, and the “main” has begun to operate in a new capacity.

While the waiting period lasts, the joining organization continues to operate. In particular, it calculates wages, depreciation, issues invoices and issues invoices and invoices.

What documents will be required?

Now let's look at what documentation is needed to carry out the reorganization process.

First of all, you should provide the following documents to the Federal Tax Service:

- Charter of the company.

- Registration certificate.

- Certificate of tax registration.

- Extract from the Unified State Register of Legal Entities.

- Minutes of the meeting of the founders on the creation of the LLC.

- Decision on the appointment of management.

- A copy of the passport and TIN of the manager.

- Enterprise balance sheet.

- Lists of debtors and creditors.

- Statement.

- Document confirming payment of state duty.

- A copy of the document on which the procedures will be performed (agreement).

- The act of transferring the rights and obligations of company participants.

The tax authority can review the received package of documents within 30-45 days. If the documentation is completed correctly, the Federal Tax Service must inform the applicant about changes made to the State Register.

Tax reporting

Despite the variety of reorganization options, there are common points when submitting tax reports. They are set out in Art. 55 of the Tax Code of the Russian Federation: the tax period ends with the date of transformation, except for VAT and other taxes with a tax period of “quarter” (“month”). Let's consider the most significant of them.

Income tax

Reporting is submitted based on the data of the tax period from the beginning of the year until the transformation, which means that this responsibility will fall on the accounting service of the legal successor. In practice, the successor is obliged to calculate two declarations: for the predecessor and for himself, without missing the deadline for submitting them. The law requires submitting the declaration no later than March 28 of the following year. Often, the tax office requires reporting to be submitted earlier - within the deadline used for calculating advance payments (by the 28th of the following month).

Property tax

Rent by analogy with income tax. When submitting reports for a predecessor, it is important to remember that it is not data on the advance payment that is provided, but a declaration for the period in which the reorganization took place.

The standard deadline is March 30 next year. As in the situation with income tax, in the case of transformation, the Federal Tax Service often requires submitting a declaration earlier: within the deadlines provided for advance payments, before the 30th day of the month following the reporting period.

VAT

In this case, the tax period is quarterly, and therefore there are peculiarities of filing a declaration during the transformation. It follows from the filling instructions that the predecessor declares his data received before the transformation, and the successor declares his data recorded after the date of reorganization.

However, the Federal Tax Service in letter No. 24-15 / [email protected] dated May 13, 2015 offers an explanation according to which the successor can draw up a single declaration that includes the indicators of both the predecessor and his own. It also contains an option in which the predecessor, having received the consent of the Federal Tax Service in writing, submits the declaration independently and ahead of schedule for himself, before the reorganization is completed with registration. The deadline for filing a declaration is until the 25th day of the month following the reporting period (quarter).

Simplified tax

The rules are identical to those applied to income tax. The declaration includes the period from the beginning of the year until the transformation; it is submitted by the legal successor. The standard deadline is March 31 of the year following the reorganization.

Personal income tax

2-NDFL certificates, according to the law, are submitted before April 1 of the following year (Article 230(2) of the Tax Code of the Russian Federation). Fiscal authorities often require early submission of information from the predecessor, arguing that there is an obligation to do this before the transformation. At the same time, according to the regulatory services, the legal successor submits information for himself, until 1.02. The position is contained in a number of letters and clarifications of the Ministry of Finance and the Federal Tax Service (for example, letter of the Ministry of Finance No. 03-04-06/8-173 dated 19-07-11 ), has obvious legal flaws and can be legally challenged. The legal successor has the opportunity to submit information for himself and for the company existing before the transformation.

Other declarations are submitted similarly, within the time limits established by law: by quarter (month) or by annual indicators. As a standard, the successor prepares two packages of documents: with data for himself and his predecessor. The submission of corrective information is the responsibility of the assignee.

Attention! Declaring indicators to the Federal Tax Service before conversion - “in advance” - can lead to their significant distortion. It is justified only in a situation where economic activity at the predecessor enterprise is not actually carried out until the specified date.

When determining the deadline for submitting information, the transfer of dates to a later date, due to weekends and holidays, is taken into account.

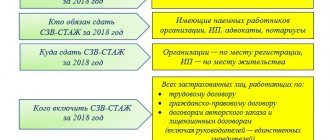

How to submit 6 personal income taxes during reorganization -

HOW TO SUBMIT 6 PIT DURING REORGANIZATION

of this article

Calculation according to form 6-NDFL in 2021

Calculation of 6-NDFL is another type of reporting for all employers. It must be taken by organizations and individual entrepreneurs with employees starting from the 1st quarter of 2021.

Unlike 2-NDFL certificates (the issuance of which has not been canceled), form 6-NDFL is compiled not separately for each employee, but for the entire company or individual entrepreneur as a whole.

It is worth noting that many individual entrepreneurs and organizations use special programs or online services to simplify the process of generating and submitting 6-NDFL calculations.

6-NDFL must be submitted to the same Federal Tax Service to which the personal income tax was transferred. The address and contact details of your tax office can be found using this service

Calculation of 6-NDFL must be submitted quarterly

. The deadline for submission is the last day of the first month of the next quarter.

Field “Tax period (year)”

. The year of the tax period for which the calculation is submitted is indicated (for example, 2016).

Field “Submitted to the tax authority (code)”

. The code of the tax authority to which the 6-NDFL calculation is submitted is indicated. You can find out your Federal Tax Service code using this service.

Field “At location (accounting) (code)”

.

The code for the place where the calculation is submitted to the tax authority is indicated ( see Appendix 2

).

Individual entrepreneurs using UTII or PSN indicate the OKTMO code of the municipality in which they are registered as payers of these taxes.

Field "On pages"

. This field indicates the number of pages that make up the 6-NDFL calculation (for example, “002”).

Line 020 is the generalized amount of accrued income for all employees on an accrual basis from the beginning of the tax period.

Line 025 is the generalized amount of accrued dividends for all employees on an accrual basis from the beginning of the tax period.

Line 040 is the generalized amount of calculated personal income tax for all employees on an accrual basis from the beginning of the tax period.

Line 045 is the generalized amount of calculated tax on income in the form of dividends on an accrual basis from the beginning of the tax period.

Line 080 – the total amount of tax not withheld by the tax agent, cumulatively from the beginning of the tax period.

Line 130 is the generalized amount of income actually received (without subtracting the amount of withheld tax) on the date indicated in line 100.

How to draw up and submit a calculation using Form 6-NDFL

Andrey Kizimov, Candidate of Economic Sciences, Deputy Director of the Department of Tax and Customs Tariff Policy of the Ministry of Finance of Russia

For the first time, Form 6-NDFL must be submitted for the first quarter of 2021 (Part 3 of Article 2, Part 3 of Article 4 of the Law of May 2, 2015 No. 113-FZ). Deadline – until May 4, 2021 (inclusive).

Complete Form 6-NDFL for each separate division. Even if these divisions are registered with the same tax office

- title page;

- section 1 “Generalized indicators”;

- Section 2 “Dates and amounts of income actually received and withheld personal income tax.”

Such rules are spelled out in paragraphs 1.2–1.12 of the Procedure approved by Order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/450.

In the “Adjustment number” line of the primary calculation, enter “000”. If you are submitting a corrected calculation, indicate the serial number of the correction (“001”, “002”, etc.).

- 21 – when submitting payments for the first quarter;

- 31 – when submitting payments for the six months;

- 33 – when submitting payments for nine months;

- 34 – when submitting the calculation for the year.

For each tax rate, you need to create a separate section 1. In such a situation, fill out lines 060–090 only on the first page.

On line 020, reflect all employee income on an accrual basis from the beginning of the year. On line 025, highlight dividend income.

In line 050, indicate the amount of fixed advance payments that are offset against personal income tax on the income of foreigners working under patents.

Reporting 6 personal income taxes in the 1C program Salary and Human Resources Management

In line 060, indicate the number of people who received income during the reporting (tax) period.

Such rules are established by clause 3.3 of the Procedure approved by order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/450.

Reflect the total amount of income on line 020, and the non-taxable amount on line 030, section 1 of form 6-NDFL.

This is stated in paragraphs 4.1–4.2 of the Procedure approved by order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/450.

On line 110 of section 2, indicate the date of tax withholding, that is, the date when the salary was issued from the cash register or transferred to the employee’s account.

On line 130 of section 2, indicate the amount of salary actually paid, and on line 140 - the amount of personal income tax, which in this situation will be zero.

- on line 100 – 12/31/2015;

Source: https://reorga.ru/kak-sdat-6-ndfl-pri-reorganizacii/

If the debtor joined the creditor

It happens that the merged company is a debtor, and the “main” company is a creditor. Then, after the reorganization, the creditor and debtor become one, and the debts are automatically repaid.

Does the successor company have taxable income in the amount of the predecessor's debt? Two years ago, officials answered this question positively (letter of the Ministry of Finance of Russia dated 10/07/09 No. 03-03-06/1/655). But then they changed their point of view and began to argue the opposite: the assignee has no taxable income (letters from the Ministry of Finance of Russia dated July 30, 2010 No. 03-03-06/1/502 and dated November 29, 2010 No. 03-03-06/1/744 ). It is the last conclusion, in our opinion, that corresponds to the law.

The opposite situation is also possible, when the lender joins the borrower. Here, the assignee also does not have to show income in the form of former debt. The Ministry of Finance of Russia agrees with this in letter dated November 15, 2010 No. 03-11-06/2/177. True, it talks about income under a simplified system, but this does not change the essence of the matter.

Let us add that interest on the loan accrued before the reorganization does not need to be adjusted after the merger. This was reported by specialists from the financial department in a letter dated March 14, 2011 No. 03-03-06/1/135.

Organizational violations.

The so-called organizational violations include such violations as failure to comply with the deadlines for submitting Form 6-NDFL, the method of submission, submitting a calculation in the case of a separate division not at its location, etc.

Violation of the deadline for submitting form 6-NDFL. As practice shows, violations of reporting deadlines still occur. Let us remind you that the calculation in form 6-NDFL for the first quarter, six months, nine months is submitted to the tax authority no later than the last day of the month following the corresponding period, for the year - no later than April 1 of the year following the expired tax period (clause 2 Article 230 of the Tax Code of the Russian Federation).

Violation of the deadline for submitting Form 6-NDFL is subject to liability in the form of a fine in the amount of 1,000 rubles. for each full and partial month, starting from the day established for submitting the calculation (clause 1.2 of Article 126 of the Tax Code of the Russian Federation).

In addition, in the event of failure to submit a calculation in Form 6-NDFL within ten days after the expiration of the established period for submitting such a calculation, the head (deputy head) of the tax authority makes a decision to suspend the operations of the tax agent on his bank accounts and transfers of his electronic funds (p 3.2 Article 76 of the Tax Code of the Russian Federation).

Submission of form 6-NDFL on paper instead of electronically. A tax agent, if the number of individuals who received income in the tax period is more than 25 people, is obliged to submit to the tax authority a calculation in form 6-NDFL in electronic form via telecommunication channels (clause 2 of Article 230 of the Tax Code of the Russian Federation).

Errors when filling out the checkpoint and OKTMO. Discrepancies between OKTMO codes in calculations and personal income tax payments lead to the appearance of unjustified overpayments and arrears (clause 7 of Article 226 of the Tax Code of the Russian Federation).

If, when filling out a calculation in Form 6-NDFL, a tax agent made a mistake regarding the indication of the checkpoint or OKTMO, then if this fact is discovered, the tax agent must submit two calculations in Form 6-NDFL to the tax authority at the place of registration:

- updated calculation to the previously presented one, indicating the corresponding checkpoints or OKTMO and zero indicators for all sections of the calculation;

- initial calculation indicating the correct checkpoint or OKTMO.

Such clarifications are also given in the Letter of the Federal Tax Service of Russia dated August 12, 2016 No. GD-4-11/ [email protected]

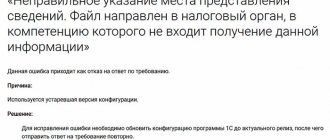

Submission of form 6-NDFL by separate divisions of the organization not at their location. The calculation in Form 6-NDFL is filled out by the tax agent separately for each separate division registered, including those cases where separate divisions are located in the same municipality.

Submission by an organization (a separate division) of a form after a change of location to the old location. Often, organizations (separate divisions) that have changed their location continue to submit Form 6-NDFL at their previous location. This is not true.

After registration with the tax authority at the new location of the organization (separate division), the tax agent submits to the tax authority at the new location calculations in Form 6-NDFL, namely:

- calculation in form 6-NDFL - for the period of registration with the tax authority at the previous location, indicating OKTMO to the previous location of the organization (separate division);

- calculation in form 6-NDFL - for the period after registration with the tax authority at the new location, indicating OKTMO at the new location of the organization (separate division).

In this case, the calculation indicates the checkpoint of the organization (separate division), assigned by the tax authority at the new location of the organization (separate division) (Letter of the Federal Tax Service of Russia dated December 27, 2016 No. BS-4-11 / [email protected] ).

Personal income tax reporting

Merger, like all other forms of reorganization, does not interrupt the tax period for personal income tax. This is explained by the fact that the company is not a taxpayer, but a tax agent. In addition, labor relations with personnel continue, as stated in Article 75 of the Labor Code of the Russian Federation. This means that there is no need to submit any interim reporting on personal income tax during reorganization.

There is one important nuance here: if an employee brings a notice for property deduction, where the predecessor organization is indicated as the employer, the accounting department of the successor company must refuse him. The employee will have to go to the tax office again and get another notice confirming the deduction related to the legal successor. Such clarifications were given by the Russian Ministry of Finance in letter dated August 25, 2011 No. 03-04-05/7-599. In practice, inspectors everywhere follow these clarifications and cancel the deduction provided under an “outdated” notification.

Work on mistakes.

Since the introduction of Form 6-NDFL, tax agents have had many questions about filling it out. In this regard, many mistakes were made. The Federal Tax Service summarized the violations in terms of filling out and submitting calculations in form 6-NDFL (Letter dated November 1, 2017 No. GD-4-11/ [email protected] ). To help tax agents correctly fill out Form 6-NDFL for 2017, we offer an overview of errors made by tax agents and identified by tax authorities, and most importantly, we will tell you how to fill it out correctly.

Tax officials cite the following reasons for violations:

- non-compliance with the provisions of the Tax Code of the Russian Federation;

- non-compliance with the procedure for filling out the calculation in Form 6-NDFL;

- non-compliance with control ratios of calculation indicators;

- non-compliance with the explanations of the Federal Tax Service;

- errors when filling out reports.

All of the above violations are divided into groups based on the nature of their commission.