Test work - accounting problems with solutions. Drawing up a balance

Test option No. 3

Exercise 1:

1. Determine the correspondence of accounts for transactions and register these transactions in the business transactions journal.

2. Determine the missing transaction amounts.

3. Draw up a turnover sheet for synthetic accounts.

4. Based on the turnover sheet, draw up a balance sheet at the end of the reporting period.

Log of business transactions for the month

| № | Contents of operation | Wiring | Sum |

| 1 | Received supplier invoices for materials | ||

| materials are capitalized at wholesale prices | D10/K60 | 204495 | |

| VAT | D19/K60 | 36809 | |

| 2 | An invoice was received from the transport organization for the delivery and unloading of materials | 3125 | |

| without VAT | D10/K60 | 2648 | |

| VAT | D19/K60 | 477 | |

| 3 | Debited from the current account to pay bills of suppliers and transport organizations | D60/K51 | 207143 |

| 4 | VAT related to the cost of materials received has been restored | D68/K19 | 37286 |

| 5 | Materials released for December at wholesale prices: | ||

| for the production of product A | D25/K10 | 184083 | |

| for the production of product B | D25/K10 | 14837 | |

| for maintenance of equipment of the main workshop | D25K10 | 3550 | |

| for other needs of the main workshop | D26K10 | 2369 | |

| for the needs of the plant management | D26K10 | 1344 | |

| Total | 206183 | ||

| 6 | Part of the transportation and procurement costs related to materials sold is written off: | ||

| for the production of product A | D25/K10 | 5522 | |

| for the production of product B | D25/K10 | 445 | |

| for maintenance of equipment of the main workshop | D25K10 | 106 | |

| for other needs of the main workshop | D26K10 | 71 | |

| for the needs of the plant management | D26K10 | 40 | |

| Total | 6184 | ||

| 7 | An energy sales invoice was received for the electricity consumed: | ||

| for equipment maintenance | D25/K60 | 1552 | |

| for workshop lighting | D25/K60 | 1010 | |

| for plant lighting | D26/K60 | 1705 | |

| Total | 4267 | ||

| 8 | December wages accrued and distributed: | ||

| production workers according to ed. A | D25/K70 | 102527 | |

| production workers according to ed. B | D25/K70 | 7887 | |

| worker servicing equipment | D25/K70 | 20376 | |

| other workshop personnel | D26/K70 | 14675 | |

| plant management personnel | D26/K70 | 30277 | |

| workers during regular vacations | D70/K50 | 5998 | |

| temporary disability benefits accrued | D20/K70 | 1100 | |

| Total | 182840 | ||

| 9 | Amounts are reserved for the upcoming payment of workers' next vacations - in a planned percentage of the basic salary: | ||

| production workers according to ed. A | D25/K96 | 6176 | |

| production workers according to ed. B | D25/K96 | 476 | |

| worker servicing equipment | D25/K96 | 1200 | |

| Total | 7852 | ||

| 10 | Contributions are made for social needs: | ||

| production workers according to ed. A | D25/K69 | 37935 | |

| production workers according to ed. B | D25/K69 | 2918 | |

| worker servicing equipment | D25/K69 | 7539 | |

| other workshop personnel | D26/K69 | 5430 | |

| plant management personnel | D26/K69 | 11202 | |

| workers during regular vacations | D70/K69 | 2219 | |

| Total | 67243 | ||

| 11 | Deducted from the wages of workers and employees for December: | ||

| a) taxes | D70/K68 | 23900 | |

| b) according to writs of execution | D70/K73 | 800 | |

| c) to return the balance of previously issued imprest amounts | D70/71 | 80 | |

| Total | 24780 | ||

| 12 | The contractor's invoice for the current repairs has been received and accepted: | ||

| main workshop equipment | D25/K60 | 6509 | |

| utility workshop buildings | D26/K60 | 5629 | |

| factory office buildings | D26/K60 | 7047 | |

| Total | 19185 | ||

| 13 | An energy sales invoice was received for the heat energy consumed: | ||

| main workshop | D25/K60 | 1200 | |

| plant management | D26/K60 | 421 | |

| Total | 1621 | ||

| 14 | Depreciation for December was calculated on the cost of fixed assets: | ||

| main workshop equipment | D25/K02 | 6580 | |

| main workshop building | D25/K02 | 3720 | |

| factory management buildings | D26/K02 | 3520 | |

| Total | 13820 | ||

| 15 | Received by check from a current account in cash | D50/K51 | 184990 |

| 16 | Taxes withheld from workers and employees, and debt on other tax payments were transferred from the current account | D68/K51 | 28340 |

| 17 | Salaries issued from the cash register | D70/K50 | 18369 |

| 18 | Wages not received on time are deposited | D70/K76 | 1300 |

| 20 | General production expenses related to production costs have been distributed and written off: | ||

| for products A | D20/K25 | 385671 | |

| for products B | D20/K25 | 30468 | |

| Total | 416139 | ||

| 21 | General business expenses related to production costs have been distributed and written off: | ||

| for products A | D20/K26 | 77618 | |

| for products B | D20/K26 | 6112 | |

| Total | 83730 | ||

| 22 | Finished products produced by the main production facility are accepted into the warehouse | D43/K20 | 499869 |

| 23 | Invoices were presented to customers for products supplied to them | D62/K90 | 740864 |

| 24 | The cost of shipped products is written off | D90/K43 | 499869 |

| 25 | Accrued costs for shipment of finished products | D44/K60 | 2340 |

| 26 | The costs of shipping finished products from the departure station are written off from the current account at the expense of the supplier | D60/K51 | 2340 |

| 27 | Received to the bank account from buyers: | D51/K62 | 740864 |

| 28 | Non-production expenses related to products sold are written off | D46/K44 | 2340 |

| 29 | VAT accrued on products sold | D68/K90 | 112982 |

| 30 | The financial result from the sale is identified and listed | D90/K99 | 128013 |

| 31 | Transferred from the current account to pay the contractor's bill for current repairs and energy sales bills for heat energy | D60/K51 | 25073 |

| social insurance authorities | D69/K51 | 18000 | |

| Total | 43073 | ||

| 32 | The deposited salary was returned to the bank account | D51/K70 | 1300 |

Synthetic account balances

| Account name | Sum | |

| 01 | Fixed assets | 2344742 |

| 02 | Depreciation of fixed assets | 342824 |

| 10 | Materials | 170005 |

| 19 | VAT on purchased assets | 26513 |

| 20 | Primary production | 73480 |

| 25 | General production expenses | |

| 26 | General running costs | |

| 43 | Finished products | 213630 |

| 50 | Cash register | 300 |

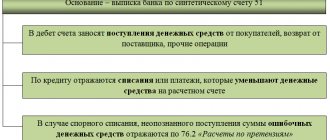

| 51 | Checking account | 84685 |

| 60 | Settlements with suppliers | 23010 |

| 62 | Settlements with customers | 213630 |

| 66 | Short-term bank loan | 280000 |

| 68 | Calculations with the budget | 6600 |

| 69 | Social insurance calculations | 5600 |

| 70 | settlements with personnel for wages | 73400 |

| 71 | Calculations with accountable persons | 100 |

| 76 | Settlements with various debtors and creditors | |

| - debtors | 6200 | |

| - creditors | 7680 | |

| 80 | Authorized capital | 2277905 |

| 84 | retained earnings | 17760 |

| 90 | Sales | |

| 96 | Reserve for upcoming expenses and payments | 7646 |

| 99 | Profit/Loss | 90860 |

Due to the emergence of new options related to ruble balance, we decided to write this article to tell in more detail how you can use your ruble exchange balance on P2P.

Let's first figure out what the RUB fiat balance is.

Ruble (RUB) fiat balance is rubles that are stored in your exchange spot wallet.

We suggest considering two methods for withdrawing ruble funds from an exchange wallet using Binance P2P.

Method No. 1: Buy cryptocurrency with payment in RUB balance

Fiat balance RUB is one of the payment methods on P2P, which means you can buy cryptocurrency and pay for it with your rubles on the exchange. In other words, you will not need to use your bank card or other electronic wallets to make payments.

If, for example, the price of a cryptocurrency on P2P is more profitable than on the spot market, then simply exchange your rubles for one of the six cryptocurrencies available on P2P.

To find exchange offers, go to P2P, then select the "Buy" section and filter ads by the "Fiat Balance RUB" payment method.

Once you find a seller that accepts payment in RUB balance, click “Buy” to place your order.

Next, let's move directly to the payment process.

To make a transfer, you need to know either the email address or phone number associated with your Binance account . If this information is not specified in the order, use the built-in chat to contact the sellers and clarify this information.

Please note that the transfer is carried out within the exchange, between user wallets, and the email or phone number must be linked to the account.

When using a mobile phone, it is extremely important to use the correct country code. Otherwise the translation will not be completed.

Go to your spot wallet, click Withdraw, and select rubles (RUB).

Click “Fiat Transfer” and enter the recipient's email or mobile phone number, transfer amount, and a note (optional). Click the “Continue” button.

After you have entered all the data, check it carefully and confirm the sending of rubles:

For security purposes, the system will ask you to enter a code from SMS, a verification code from email and a 6-digit code from the Google Authenticator application.

Based on the results of a successful transfer, you will receive an SMS and an email notification about the completed transfer.

Make sure the transaction is completed. If you did everything correctly, the transaction will have the Completed status, and your counterparty to the P2P transaction will receive the transfer instantly.

You can check the transaction status on the “Transaction History” page using this link.

All that remains is to complete the P2P transaction. Mark the order as paid and wait for the seller to transfer you the cryptocurrency!

Method No. 2: Exchange RUB balance to rubles on your card

A new pair RUB/RUB has been added to P2P. RUB, which appears in the menu with other cryptocurrencies, is your ruble asset that is stored in your wallet, just like Bitcoin, USDT and other cryptocurrencies.

Therefore, if you need to withdraw your ruble balance in rubles to your card, then go to the “Sell” - “RUB” section. Select rubles (RUB) as fiat in the filter, as well as the payment method.

Despite the fact that direct exchange is carried out with other users of the P2P platform, you can be sure of the security of the transaction, since your ruble balance will be frozen in the order and will not be transferred to the buyer until you receive full payment on your card.

Pay attention to the prices!

The rate of 1.01 in the sell section means that you will receive 1.01 rubles on the card for every 1 ruble of balance, in other words, you can withdraw rubles with a profit of +1%.

Thus, when you withdraw 1000 rubles from your balance, you will receive 1010 rubles to your bank card.

P2P is currently the only way to withdraw rubles on Binance not only without commissions, but also with a profit.

Step-by-step instructions on how to sell your RUB balance in our blog at the link.

In a similar way, you can make a ruble deposit to your Binance wallet.

Go to the “Buy” - “RUB” section. Select a payment method convenient for you from those offered using the filter:

A rate of 1.02 means that you will pay 1.02 rubles from your card for every 1 ruble on your Binance balance, in other words, +2%:

The advantage of P2P is that the platform itself does not charge any fees to users. All prices are offered exclusively by other users, and are formed based on supply and demand in the market

Company balance sheet

| № p/p | Account name | Balance as of December 1 | Turnover for December | Remaining by 1 January | |||

| Debit | Credit | Debit | Credit | Debit | Credit | ||

| 01 | Fixed assets | 2344742 | 356644 | 1988098 | |||

| 02 | Depreciation of fixed assets | 342824 | 13820 | 356644 | |||

| 10 | Materials | 170005 | 204495 | 206183 | 168317 | ||

| 19 | VAT on purchased assets | 26513 | 37286 | 63799 | |||

| 20 | Primary production | 73480 | 499869 | 357148 | 216201 | ||

| 25 | General production expenses | 416139 | 416139 | ||||

| 26 | General running costs | 83730 | 83730 | ||||

| 43 | Finished products | 213630 | 527234 | 740864 | |||

| 44 | Selling expenses | 2340 | 2340 | ||||

| 50 | Cash register | 300 | |||||

| 51 | Checking account | 84685 | 740864 | 465886 | 360963 | ||

| 60 | Settlements with suppliers | 23010 | 213031 | 208764 | 27277 | ||

| 62 | Settlements with customers | 213630 | 527234 | 740864 | |||

| 66 | Short-term bank loan | 280000 | 280000 | ||||

| 68 | Calculations with the budget | 6600 | 26513 | 112982 | 37286 | 55783 | |

| 69 | Social insurance calculations | 5600 | 67243 | 18000 | 54843 | ||

| 70 | settlements with personnel for wages | 73400 | 182840 | 184990 | 71250 | ||

| 71 | Calculations with accountable persons | 100 | 80 | 20 | |||

| 76 | Settlements with various debtors and creditors | 13880 | 6926 | 20806 | |||

| 80 | Authorized capital | 2277905 | 2277905 | ||||

| 84 | retained earnings | 17760 | 17217 | 34977 | |||

| 90 | Sales | ||||||

| 96 | Reserve for upcoming expenses and payments | 7646 | 7852 | 15498 | |||

| 99 | Profit/Loss | 90860 | 37153 | 128013 | |||

| Revolutions | |||||||

Balance sheet

| on | 20 | G. | Codes | ||||||||

| OKUD form | 0710001 | ||||||||||

| Date (day, month, year) | |||||||||||

| Organization | according to OKPO | ||||||||||

| An identification number taxpayer | TIN | ||||||||||

| Type of economic activity | _______________ | according to OKVED | |||||||||

| Organizational and legal form/ type of ownership | _ | ||||||||||

| according to OKOPF/OKFS | |||||||||||

| Unit of measurement: thousand rubles. (million rubles) | according to OKEI | 384 (385) | |||||||||

Location (address) ______________________________

| Explanations | Indicator name | As of 01.01 2011 | As of 01.12 2010 | As of 31.12 20__ |

| ASSETS | ||||

| I. NON-CURRENT ASSETS | ||||

| Intangible assets | ||||

| Research and development results | ||||

| Fixed assets | 1988098 | 2344742 | ||

| Profitable investments in material values | ||||

| Financial investments | ||||

| Deferred tax assets | ||||

| Other noncurrent assets | ||||

| Total for Section I | 1988098 | 2344742 | ||

| II. CURRENT ASSETS | ||||

| Reserves | 448317 | 457115 | ||

| Value added tax on acquired values | 26513 | |||

| Accounts receivable | 6200 | |||

| Financial investments | ||||

| Cash | 360963 | 84985 | ||

| Other current assets | ||||

| Total for Section II | 809280 | 574813 | ||

| BALANCE | 2797378 | 2919555 |

Form 0710001 p. 2

| Explanations | Indicator name | As of 01.01 2011 | As of 01.12 2010 | As of 31.12 20__ |

| PASSIVE | ||||

| III. CAPITAL AND RESERVES | ||||

| Authorized capital (share capital, authorized capital, contributions of partners) | 2277905 | 2277905 | ||

| Own shares purchased from shareholders | ||||

| Revaluation of non-current assets | ||||

| Additional capital (without revaluation) | ||||

| Reserve capital | ||||

| Retained earnings (uncovered loss) | 34977 | 17760 | ||

| Total for Section III | 2312882 | 2295665 | ||

| IV. LONG TERM DUTIES | ||||

| Borrowed funds | ||||

| Deferred tax liabilities | ||||

| Provisions for contingent liabilities | ||||

| Other obligations | ||||

| Total for Section IV | ||||

| V. SHORT-TERM LIABILITIES | 280000 | 280000 | ||

| Borrowed funds | ||||

| Accounts payable | 168317 | 116290 | ||

| revenue of the future periods | 213630 | |||

| Reserves for future expenses | 15498 | 7646 | ||

| Other obligations | 20681 | 6324 | ||

| Total for Section V | 484496 | 740180 | ||

| BALANCE | 2797378 | 2919555 |

| Supervisor | Chief Accountant | |||||||||||

| (signature) | (full name) | (signature) | (full name) | |||||||||

| “ | ” | 20 | G. | |||||||||

Task 2.

Moscow State University of Printing Arts

1.

LESSON 1. CHART OF ACCOUNTS AND BALANCE SHEET OF A COMMERCIAL BANK

When solving the problems brought to your attention in Lesson 1, you must use the Chart of Accounts for accounting in commercial banks of the Russian Federation, on its basis, learn the nature, features of the functioning of balance sheet and off-balance sheet accounts, as well as the principles of constructing balance sheets.

1.1.

Problem 1.1

Accounting for the commercial bank CJSC CB Alta-Bank is maintained using the following balance sheet and off-balance sheet accounts:

| Name of first and second order accounts | Account number from the chart of accounts |

| 1 | 2 |

| Funds | |

| Authorized capital of joint-stock banks, formed from ordinary shares | |

| Reserve Fund | |

| Cash desk of credit organizations | |

| Cash currency and payment documents | |

| Federal budget funds | |

| Correspondent accounts of credit institutions with the Bank of Russia | |

| Special Purpose Funds | |

| Unrealized exchange differences | |

| Correspondent accounts | |

| Funds for material incentives and social development | |

| Shares acquired for resale and under loan agreements | |

| Industrial Development Fund | |

| Loans provided to commercial organizations under federal ownership | |

| Current accounts of state enterprises | |

| Financial lease (leasing) operations | |

| Loans provided to individuals | |

| Overdue debt on loans provided and other placed funds | |

| Settlement (current) accounts of federally owned enterprises | |

| Cash on the way | |

| Mandatory reserves for credit transactions on accounts in Russian currency transferred to the Bank of Russia | |

| Accounts of non-governmental organizations | |

| Precious metals in coins and commemorative medals | |

| Settlements with branches | |

| Unplaced securities | |

| Extra capital | |

| Guarantees issued by the bank | |

| Settlements on the institutional securities market | |

| Calculations for required reserves | |

| Funds from state extra-budgetary funds | |

| Depreciation of fixed assets | |

| Funds for social support of the population |

- Determine which of the following accounts are on-balance sheet or off-balance sheet.

- Characterize the above accounts in terms of their relationship to the balance sheet.

- Determine which balance sheet accounts are first or second order accounts. Explain the differences between them.

- In which sections of the Chart of Accounts for Accounting in Credit Institutions are the above accounts located?

1.2.

Problem 1.2

Below is the balance sheet of a joint-stock commercial bank:

- Determine the balance currency.

- Calculate the main ratios of liquidity, profitability and reliability of the bank.

Balance sheet of Deutsche Bank LLC

(thousand rubles)

| Title of articles | Balance as of 01/01/2003 | |

| Assets | Liabilities | |

| Cash and accounts with the Central Bank of the Russian Federation | 62.900 | 0 |

| Mandatory reserves in the Central Bank of the Russian Federation | 441.682 | 0 |

| Funds in credit institutions | 358.972 | 0 |

| Investments in trading securities | 330.567 | 0 |

| Loan and equivalent debt | 10.832.514 | 0 |

| Loans received by credit institutions from the Bank of the Russian Federation | 4.000.000 | |

| Funds from credit institutions | 0 | 3.885.107 |

| Client funds | 0 | 1.551.867 |

| Provisions for possible loan losses | 108.324 | 0 |

| Interest accrued, including overdue | 15.568 | 0 |

| Fixed assets, intangible assets, business materials | 191.562 | 0 |

| Debt issued | 0 | 40.427 |

| Deferred income from other operations | 0 | 60.000 |

| Reserves for possible losses on derivatives transactions | 0 | 5.695 |

| Securities available for resale | 36 | 0 |

| Deferred expenses for other transactions | 4.546 | 0 |

| Other assets | 176.229 | 0 |

| Authorized capital (ordinary shares and shares) | 0 | 1.030.050 |

| Own shares purchased from shareholders | 0 | 207.050 |

| Share premium | 0 | 303.455 |

| Funds and profits left at the disposal of the credit institution | 0 | 803.300 |

| Profit of the reporting period | 0 | 503.56 |

| Distributed earnings (excluding dividends) | 0 | 137.341 |

| Costs and risks affecting own funds | 4.953 | 0 |

| Total assets: | ||

| Total liabilities: | ||

1.3.

Problem 1.3

- On the balance sheet of CJSC CB Innovation Bank there are the following balances on balance sheet accounts. Draw up a balance sheet for a commercial innovation bank based on first-order accounts.

| Account number | Account name | Amount, thousand rubles |

| 102 | Authorized capital of joint-stock banks, formed from ordinary shares (p) | 1.237.450 |

| 107 | Funds (n) | 1.103.755 |

| 606 | Depreciation of fixed assets (p) | 37.341 |

| 106 | Additional capital (p) | 503.561 |

| 202 | Cash currency and payment documents (a) | 176.905 |

| 407 | Accounts of non-state enterprises (n) | 1.742.539 |

| 301 | Correspondent account(s) | 152.051 |

| 614 | Deferred expenses (a) | 28.438 |

| 613 | Deferred income (n) | 95.047 |

| 451 | Loans provided to non-state financial organizations (a) | 226 |

| 306 | Securities settlements (a) | 362.668 |

| 312 | Loans, deposits and other borrowed funds received by credit institutions from the Bank of Russia (p) | 7.240.004 |

| 322 | Loans and other funds placed with credit institutions (a) | 11.040.703 |

| 415 | Deposits of federally owned financial institutions (n) | 408.100 |

| 454 | Loans provided to individual entrepreneurs (a) | 601.090 |

| 458 | Overdue debt on loans provided and other placed funds (a) | 116.418 |

| 506 | Shares acquired for resale and under loan agreements (a) | 175.45 |

| 508 | Listed shares purchased for investment(s) | 368.202 |

| 515 | Other bills (a) | 36.187 |

| 520 | Issued bonds (n) | 20.000 |

| 521 | Certificates of deposit issued (n) | 30.000 |

| 522 | Savings certificates issued (n) | 50.000 |

| 603 | Settlements with debtors (a) | 175.547 |

| 603 | Settlements with creditors (p) | 766.095 |

| Total assets: | ||

| Total liabilities: |

1.4.

Problem 1.4

Indicate which of the following accounting accounts in a commercial bank are balance sheet, off-balance sheet, active, passive, paired.

| No. | Account name | Answer options | ||

| 1 | 2 | 3 | ||

| 1 | 2 | 3 | 4 | 5 |

| 1 | Authorized capital of a commercial bank | Balanced, Active | Balanced, Passive | Balanced, Paired |

| 2 | Current accounts of non-state commercial organizations | Balanced, Active | Balanced, Passive | Balanced, Paired |

| 3 | Settlements with currency and stock exchanges | Balanced, Active | Balanced, Passive | Balanced, Paired |

| 4 | Guarantees, guarantees issued by the bank | Off-balance sheet, Active | Off-balance sheet, Passive | Off-balance sheet, Paired |

| 5 | Settlement documents for factoring and forfeiting transactions | Off-balance sheet, Active | Off-balance sheet, Passive | Off-balance sheet, Paired |

1.5.

Problem 1.5

Mark the correct accounting entries

(S/s - loan account, R/s - current account).

| No. | Operation | Answer options | ||

| 1 | 2 | 3 | ||

| 1 | 2 | 3 | 4 | 5 |

| 1 | A loan was provided to a non-state commercial organization in accordance with a loan agreement | Debit S/sK Credit R/s | Debit 452K Credit 407 | Debit R/sK Credit S/s |

| 2 | Transferred by payment order of a non-governmental commercial organization | Debit S/sK Credit R/s | Debit 301K Credit S/s | Debit 40702K Credit 30102 |

| 3 | The unused portion of the loan provided is credited to the current account of a non-governmental commercial organization | Debit S/s Credit R/s | Debit R/s Credit S/s | Debit 45202 Credit 40702 |

| 4 | When the loan becomes due, the loan is collected | Debit S/s Credit R/s | Debit S/s Credit 30102 | Debit 40702 Credit 45202 |

| 5 | Accrued interest on the loan was collected | Debit S/s Credit R/s | Debit 40702 Credit 45201 | Debit 45202 Credit 40702 |

1.6.

Problem 1.6

Compile a bank balance (reduced) based on the following data on account balances. In your answer, indicate the amount corresponding to the balance total:

| Account balances | Amount million rubles |

| 1 | 2 |

| Authorized capital of the bank | 70 |

| Cash in bank cash desks | 36 |

| Cash foreign currency and payment documents in foreign currency | 46 |

| Accounts of federally owned enterprises | 34 |

| Local budget funds | 18 |

| Current accounts of state enterprises and organizations | 66 |

| Loan accounts of state enterprises and organizations | 234 |

| Funds in settlements (P) | 262 |

| Correspondent account of a credit institution | 64 |

| Bank fixed assets | 70 |

| Guarantees and guarantees issued by the bank | 30 |

| Balance sheet result? | 350 |

| ? | 382 |

| ? | 450 |

1.7.

Problem 1.7

Choose the correct answer to the questions asked:

| No. | Contents of the question |

| 1 | 2 |

| 1 | Which of the following accounts is a balance sheet: |

| — Guarantees and guarantees issued by the bank — Obligations for long-term loans — Bank income — Strict reporting forms | |

| 2 | Which of the following accounts is passive: |

| — Cash desk — Authorized capital of joint-stock banks formed from ordinary shares — Current accounts of non-state commercial organizations — Loan accounts of non-profit organizations | |

| 3 | Which of the following accounts are paired: |

| — Settlements with suppliers, contractors and customers — Letters of credit for payment — Securities accepted as collateral for loans issued — Incomplete bank settlements | |

| 4 | Which of the following numbers is the off-balance sheet account number: |

| 70101 40702 30102 90901 91705 |