How to set up the reflection of the government contract ID in invoices in 1C

Regulatory regulation

Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137, which is responsible for the form of the invoice, has been updated (Resolution of the Government of the Russian Federation dated May 25, 2017 N 625). Let's look at the innovations regarding the issuance of paper invoices.

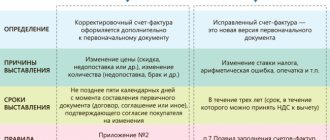

Main change : Added new line 8 “Identifier of government contract, agreement (agreement)” for the invoice (UPD) and similar data is reflected in line 5 of the adjustment invoice. This detail is indicated only if the Organization works under government contracts and such a code is assigned to the contract.

and samples of filling from 07/01/2017:

- Invoice;

- Adjustment invoice;

- Universal transfer document (UDD).

Accounting in 1C

Step. 1. In order for invoices to reflect the identifier of a government contract, in the Main – Settings – Functionality on the Calculations , select the “Invoices for government orders” checkbox (Fig. 1):

Rice. 1

Step. 2 . Open the primary document “Sales (acts, invoices)”, issue an invoice and follow the link to the invoice form to indicate the identifier (Fig. 2):

Rice. 2

Step. 3 . Enter the necessary information in the “Government Contract ID” field in the invoice (Fig. 3):

Rice. 3

The identifier can contain 20 or 25 characters depending on the type of contract (Fig. 4):

Rice. 4

Contracts worth less than RUB 100,000. no identifier is assigned.

The Federal Tax Service has posted a reminder on its portal that the identifier must also be indicated in the advance invoice.

The new analytics “Government Contract Identifier” will now allow fiscal authorities to gain additional control over the use of federal budget funds.

The invoice form from July 1, 2017 has the following form (Fig. 5):

Rice. 5

UPD form recommended for use from July 1, 2017 (Fig. 6):

Rice. 6

Adjustment invoice form (Fig. 7):

Rice. 7

Sample filling

The document is drawn up and completed according to approved forms. As with a regular invoice, the advance payment document must contain the following information:

- number;

- date of;

- physical characteristics of the product;

- name of the company and addresses of the seller and buyer;

- TIN, checkpoint of both parties.

How to register a s/f when receiving an advance on sales

The peculiarities of filling out the document are related to the fact that it must reflect the fact of receipt of an advance payment. For this purpose, the invoice must include:

- details of the payment order on the basis of which the advance was paid. A dash is placed only in the case of a non-monetary advance;

- type of currency and its code;

- prepayment amount.

Please note that each invoice must be issued on a separate sheet.

Calculation of the VAT rate and reflection of the tax amount

The moment of determining the VAT tax base in the case of receiving an advance is directly related to the date of receipt of the advance payment for goods or services. When receiving money to a current account or receiving payment in kind, an advance invoice must be issued. To calculate the amount of VAT payable to the budget at the end of the quarter or year, you must use the estimated rate.

The above means that having received an advance payment for the supply of goods, performance of work or provision of services, the seller must calculate VAT payable to the budget at the calculated rate of 18/118 or 10/110 (Clause 4 of Article 164 of the Tax Code of the Russian Federation). Which tax rate to apply depends on the rate at which the sale of goods, performance of work or provision of services for which the advance was received is taxed.

Changes in the electronic invoice format from 07/01/2017

We remind you that from July 1, 2021, only new electronic formats of invoices should be used (Order of the Federal Tax Service of the Russian Federation dated March 24, 2016 No. ММВ-7-15/155) and adjustment invoices (Order of the Federal Tax Service of the Russian Federation dated April 13, 2016 No. ММВ- 7-15/189). Previous formats are completely no longer valid.

Moreover, during the transition period from 05/07/2016 to 06/30/2017, both new and old formats are valid (approved by Order of the Federal Tax Service of the Russian Federation dated 03/04/2015 No. ММВ-7-6 / [email protected] ).

The new electronic format has become universal; it combines the functions of both an invoice and a shipping document. This allows you to reduce the volume of documents and avoid discrepancies in the preparation of the primary document. Thus, using the new format it is possible to send both an invoice and an UTD; the previous format did not allow this.

In 1C:Enterprise 8 software products, new invoice formats have already been implemented.

How to download and fill out an invoice form in a few minutes?

Using the MyWarehouse service allows you to do this even without knowledge of accounting and special terminology. You can invoice in a few seconds and complete it in a couple of minutes. Each stage of working with the document is accompanied by appropriate comments and recommendations. Explanatory information is attached to the forms.

This allows:

- Save up to 70% of the time spent on registration;

- Eliminate errors when filling out;

- automatically create an archive of printed documents and maintain continuous numbering;

- export completed forms to Excel and PDF.

The next wave of VAT changes

A number of more amendments related to VAT are expected soon. The next amendments to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137 are pending approval.

The document has already been published on the federal portal of draft regulatory legal acts (NLA), ID 02/07/09-16/00053297.

Taxpayers will see changes in the sales book, new rules for working with corrective invoices, a line will be added to reflect the code of the type of goods according to the EAEU Commodity Classification for Foreign Economic Activity in the invoice when exporting to the EAEU countries, etc.

The Federal Tax Service also plans to expand the list of codes for types of VAT transactions and update the VAT Declaration.

Filling out and submitting the form by the supplier

The tax code does not provide for exceptions for the presentation of the form. However, there is a Russian government decree that indicates cases where an invoice may not be issued. Let's list them:

- an advance is issued for the supply of products that will be produced in 6 months or later;

- the payment was made for a transaction for which the VAT rate is 0 or is not paid;

- the company does not pay VAT under Article 145 of the Tax Code of the Russian Federation.

The period within which the document must be issued

The selling company is obliged to draw up and send an invoice to the buyer no later than 5 days from the date of receipt of funds or payment in kind.

Notifications on the regulatory legal acts portal

- VAT codes, ID 02/08/06-17/00067207

- VAT return, ID 02/08/06-17/00067201

Give your rating to this article: ( 4 ratings, average: 4.00 out of 5)

Registered users have access to more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP

Registered users have access to more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP

I am already registered

After registering, you will receive a link to the specified address to watch more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP 8 (free)

By submitting this form, you agree to the Privacy Policy and consent to the processing of personal data

Login to your account

Forgot your password?

How to issue an advance invoice to a buyer

The tabular part of the document is filled in with the name of the goods or description of the work (services) for which the advance payment has been charged. It is important to take into account that all names must match those specified in the supply contract or for the provision of the relevant services. It is not prohibited to include generic names, such as “industrial products” or “welding services.”

A sample of a completed invoice is provided below.

Header of an invoice filled out in accordance with all the rules: this document can be safely accepted for accounting

The document must indicate the tax rate (Article 164 of the Tax Code of the Russian Federation), the amount of VAT presented and the amount of the advance payment.

The management of the company, as well as the chief accountant, are responsible for signing. It is allowed to delegate these responsibilities to other officials if there is a corresponding order from management on the transfer of powers.

The content of the invoice contains a link to the supply agreement, the tax rate, the amount of VAT and the amount of the advance received

Accounting and numbering

An advance invoice is a regular invoice, but with certain conditions (prepayment). Accordingly, the question of its numbering arises very often. The law (Government Decree No. 1137) states that the chronological order is the same for all invoices. This means that the advance invoice is numbered in the general order.

Some accountants keep separate records, which is not entirely true. Although there is no liability for this, for consolidation during checks, the correct sequence makes things easier. For convenience, you can put notes in the form of letter values (101/AB).

Video: how to issue and process advance invoices

Filling out an advance invoice is not difficult. In order for the written document to be accepted for credit, you must be careful and avoid common mistakes. Records should be kept in a log book, as required by law, failure to comply with which may result in fines.

- Sergey Saltykov

My name is Sergey. I have completed higher education in management. I am 24 years old, I started writing articles while still a student. Freelancing for more than three years. I am ready to carry out orders on various topics, as I love to develop.

Responsibility for violating the rules for filling out documents

Do not forget about timely issuance of invoices. Many accountants, not very puzzled by this fact, find themselves in a difficult situation upon the arrival of the tax inspector. With large volumes of sales of goods, they are unable to issue hundreds of advance documents at a time.

However, it is not so difficult to track the transfer of an advance, and if this fact is discovered, the tax office charges VAT. And this happens throughout the reporting period. It is no longer possible to make a request for a deduction, and the company receives an additional tax and a considerable fine of up to 10,000 rubles (Article 120 of the Tax Code of the Russian Federation). If violations continue in other reporting periods, the fine will increase 3 times.

Typical problems during registration

First of all, it is worth noting errors that do not affect the validity of the document and cannot be grounds for refusing to deduct VAT. Errors that do not interfere with the identification of VAT payers:

- addresses of the seller or buyer;

- tax rates;

- VAT amounts;

- name and price of goods and services.

If there is no information, instead of a dash, you can leave the field blank. O and other similar ones are also allowed.

What errors prevent VAT refunds?

Among the shortcomings in the design there are those that interfere with receiving a VAT refund. List of the most common critical errors:

- incorrect filling of the TIN and KPP;

- incorrect or unspecified document number;

- lack of information about the country of origin for foreign products.

Many accountants required to issue invoices are accustomed to giving priority to the actual address of the buyer. In fact, the main thing for identifying a counterparty is the legal address.